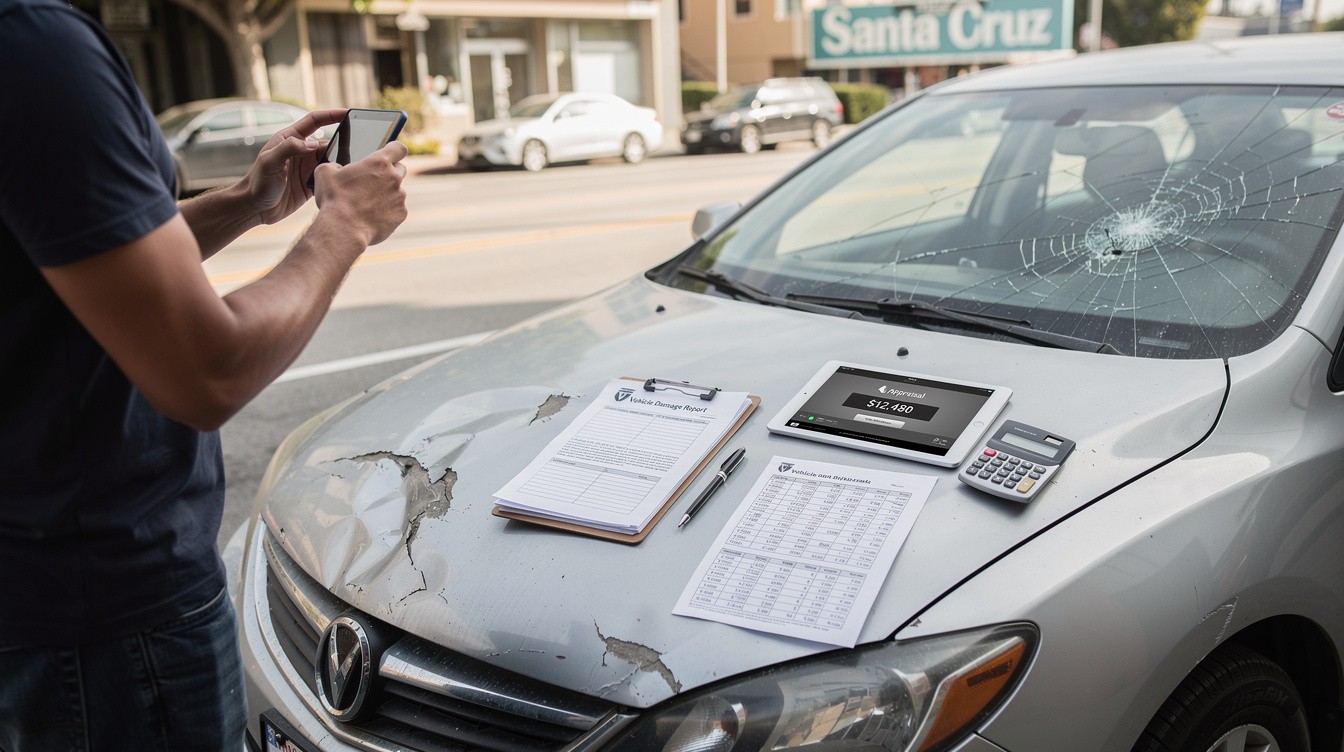

A car accident in Santa Cruz County leaves you with more than just physical damage-it creates a financial burden that needs proper documentation. Getting the right valuation for your vehicle loss determines whether you recover fairly or accept less than you deserve.

We at Schaar & Silva LLP have seen countless claims undervalued because people didn’t know what steps to take first. This guide walks you through the process of documenting damage, understanding how insurers calculate value, and avoiding the mistakes that cost you money.

Build Your Documentation Foundation Right After the Accident

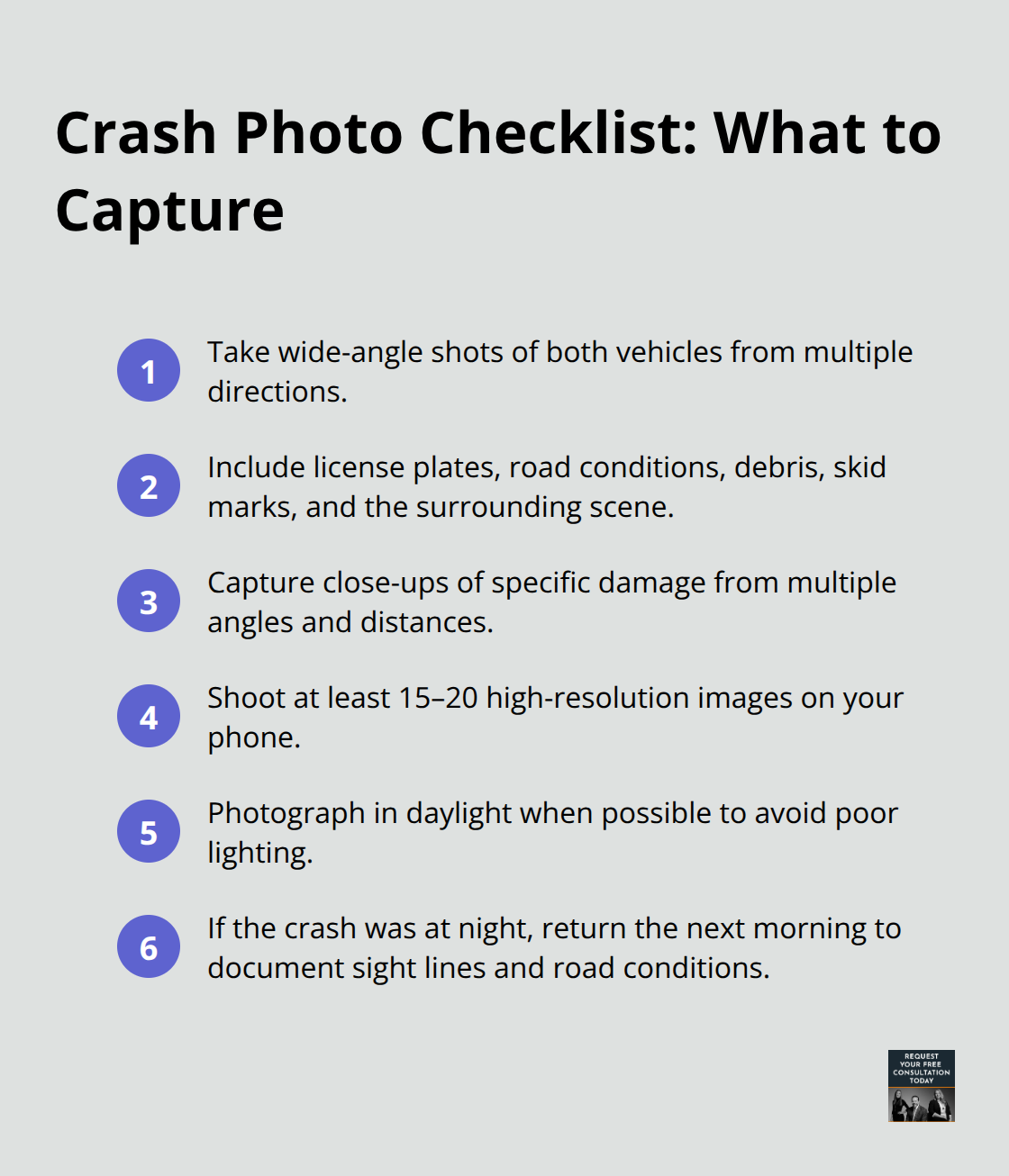

Photograph Everything Immediately

The first hours after a Santa Cruz vehicle accident determine how much you’ll recover. Insurance adjusters make decisions based on what you document, not on what actually happened. Start photographing immediately-don’t wait for the adjuster to arrive. Take wide-angle shots of both vehicles from multiple directions, capturing license plates, the surrounding scene, road conditions, debris, and skid marks. Close-ups matter too: photograph specific damage areas from different angles and distances. Use your phone’s high-resolution camera and take at least 15–20 images. If you have access to a better camera, use it.

Poor lighting kills claim value, so photograph in daylight when possible. If the accident occurred at night, return to the scene the next morning to capture the road conditions and sight lines that contributed to the crash.

Obtain Official Reports and Witness Statements

The police report carries significant weight with insurers. Obtain it within 48 hours and record the officer’s name, badge number, and report number. The officer’s observations about fault, road conditions, and vehicle damage strengthen your position against the insurance company’s narrative. Gather contact information from any witnesses at the scene-their independent statements provide leverage that the insurer cannot easily dismiss.

Collect Multiple Repair Estimates from Local Shops

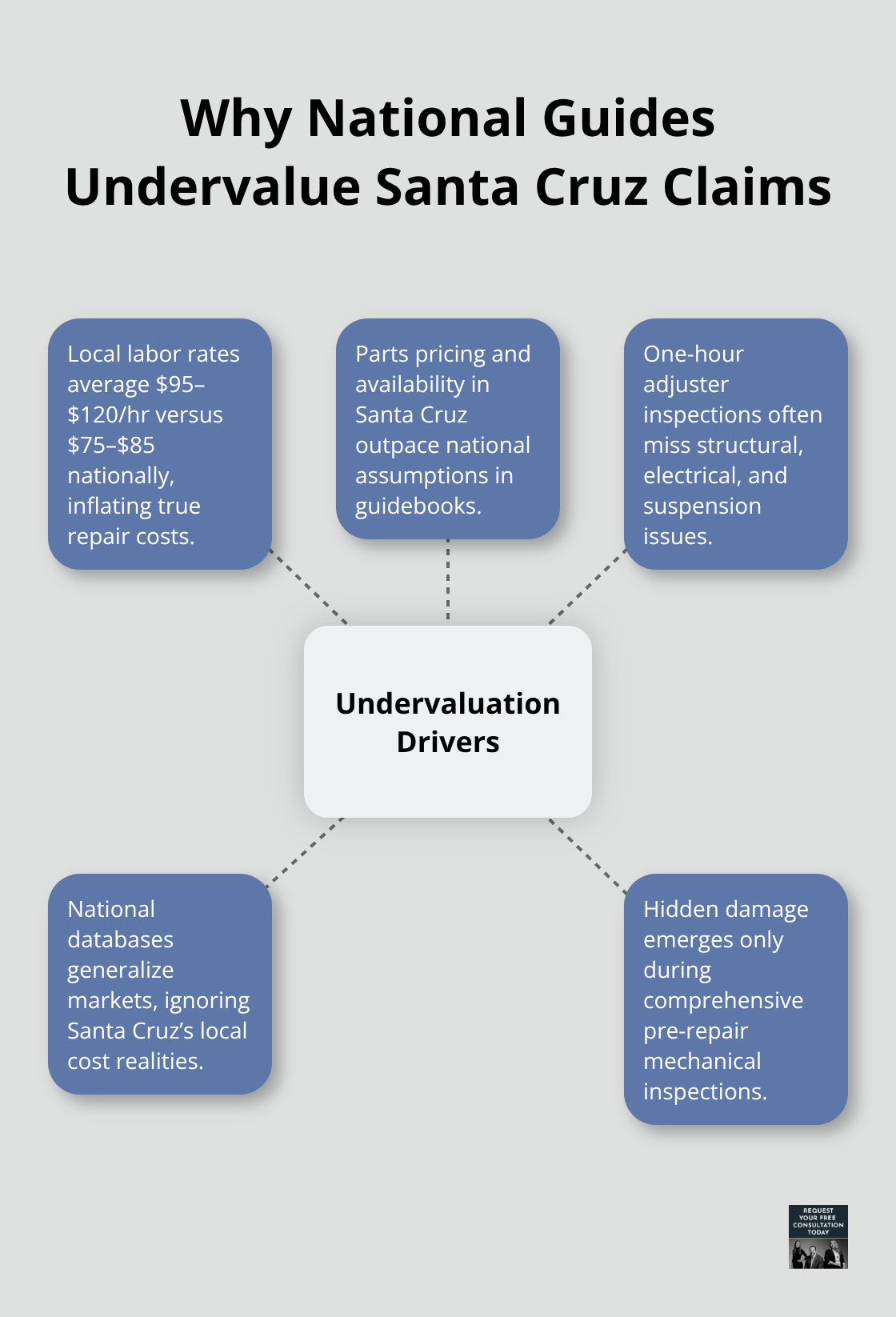

Three independent repair estimates from Santa Cruz shops (not the insurer’s preferred vendors) reveal actual local costs. The gap between these estimates and what the adjuster offers typically ranges from $2,000 to $5,000 because NADA Guides often undervalue Santa Cruz labor rates and parts availability. A licensed technician must conduct a full pre-repair mechanical inspection focusing on frame straightness, suspension integrity, and electrical system damage. Hidden issues like frame misalignment or water intrusion can add $5,000–$10,000 to actual repair costs that the adjuster’s one-hour inspection missed.

Document Personal Items and Organize Your File

Keep receipts and photographs of all damaged personal items inside the vehicle at the time of the crash: laptops, glasses, clothing, tools. Organize everything in a dated file. California’s three-year statute of limitations gives you time, but organized documentation now prevents disputes later. Present this complete file to the adjuster in writing, not over the phone-written submission creates leverage and a clear record of what you submitted and when.

The strength of your documentation directly influences how the insurance company values your loss and whether they accept your claim as presented or push back with lowball offers.

How Insurers Calculate What Your Vehicle Is Worth

Insurance companies use three overlapping methods to determine vehicle value, and understanding each one exposes where they systematically undervalue Santa Cruz claims.

National Valuation Guides Miss Local Market Reality

Adjusters pull data from NADA Guides, Kelley Blue Book, or similar databases to establish a baseline value. These national guides consistently underestimate Santa Cruz labor rates and parts costs. A 2024 analysis of Santa Cruz repair shops showed local labor rates averaging $95–$120 per hour, while NADA benchmarks typically reflect $75–$85 nationally. That gap compounds across a multi-thousand-dollar repair, creating systematic undervaluation baked into the initial offer. The adjuster’s one-hour inspection frequently misses structural damage, water intrusion, electrical system failures, and suspension issues that emerge only during detailed pre-repair mechanical inspection.

Local Repair Estimates Counter National Benchmarks

Repair cost estimates from certified mechanics in Santa Cruz must become your primary counter-evidence. When you present three written estimates from local shops, you present actual Santa Cruz pricing, not theoretical national averages. Hidden frame misalignment alone can add $5,000–$10,000 to final repair costs. These estimates force the adjuster to justify why their national database should override concrete local pricing from shops that will actually perform the work.

Independent Appraisals Establish Pre-Accident Condition

Hire an independent certified appraiser ($300–$600) to document your vehicle’s pre-accident condition and compare it directly to current market data. California law supports independent valuation as a legitimate counter to the insurer’s position, and this documentation typically justifies a $2,000–$5,000 settlement increase. Depreciation and vehicle age factor heavily into the calculation, but insurers often apply depreciation rates that don’t reflect Santa Cruz’s used vehicle market. A vehicle with higher-than-average maintenance records, recent major repairs, or lower mileage deserves adjustment upward from the base NADA value.

Close the Valuation Gap Before Settlement

The gap between the adjuster’s initial offer and actual local repair costs is not accidental-it reflects reliance on national guides that don’t account for Santa Cruz market realities. Three shop estimates, a full pre-repair mechanical inspection, and an independent appraisal create the documentation needed to challenge lowball offers. Once you’ve built this evidence, you’re ready to understand the mistakes that many claimants make when presenting their case to the insurance company.

Common Mistakes That Reduce Your Claim Value

Accept Nothing Without Evidence

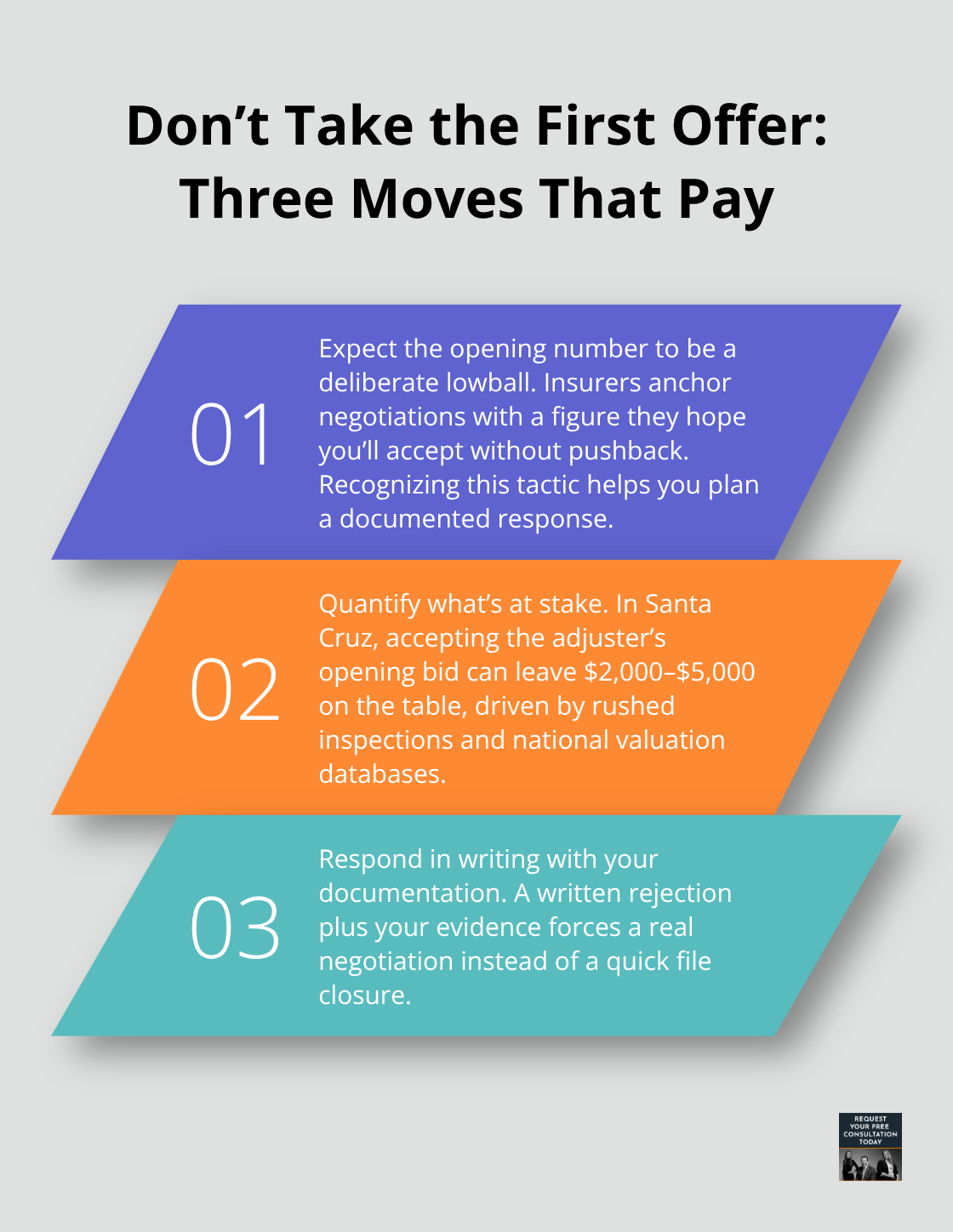

The moment an insurance adjuster sends you an initial settlement offer, they’re counting on you to accept it without question. That first number is deliberately low-not because of incomplete information, but because insurers know most people won’t push back. A Santa Cruz claimant who accepts the adjuster’s opening bid typically leaves $2,000 to $5,000 on the table. The adjuster’s one-hour vehicle inspection and reliance on national valuation databases create systematic undervaluation, yet many people treat that initial offer as final.

Rejecting it in writing and presenting your documentation forces a genuine negotiation rather than accepting a number designed to close your file quickly.

Build Concrete Evidence Before Negotiating

The insurance company has already calculated their risk and decided what they’ll pay if you fight. Your job is to make fighting more expensive for them than paying fairly. When you submit three independent repair estimates from certified Santa Cruz mechanics, a full pre-repair mechanical inspection documenting frame and suspension integrity, and an independent appraisal, you shift the conversation from what the adjuster thinks your vehicle is worth to what Santa Cruz shops actually charge to fix it. This is not theoretical leverage-it’s concrete evidence that forces the adjuster to justify their position in writing or increase the offer.

Invest in an Independent Appraisal

Many claimants fail to hire an independent appraiser because they assume the adjuster’s valuation is close enough or because $300–$600 feels expensive. That assumption costs them thousands. An independent certified appraiser documents your vehicle’s pre-accident condition, identifies depreciation errors in the adjuster’s calculation, and produces a written report that California courts recognize as legitimate valuation evidence. When your appraisal contradicts the adjuster’s number by $2,000 or more, you’ve created the foundation for a settlement increase that covers the appraiser’s fee and then some.

Counter Depreciation With Documentation

The pre-accident vehicle condition matters enormously because insurers apply generic depreciation rates that don’t account for your vehicle’s actual maintenance history, mileage, or market position in Santa Cruz County. A well-maintained vehicle with recent major repairs or lower-than-average mileage deserves adjustment upward from the baseline NADA value, yet adjusters rarely make those adjustments without documentation forcing them to. Photograph your vehicle’s interior and exterior condition before the accident if possible, or gather service records proving regular maintenance and major repairs completed before the crash. These records directly counter depreciation calculations that treat all ten-year-old vehicles identically.

Submit Everything in Writing

Once you’ve built this complete documentation package (repair estimates, mechanical inspection, independent appraisal, and pre-accident condition records), present everything to the adjuster in a single written submission. Phone calls disappear from records; written submissions create accountability and a clear timeline of what you presented and when they received it.

Final Thoughts

The documentation you’ve gathered and the valuation evidence you’ve built directly determine whether you recover fairly from your Santa Cruz property damage claim. Insurance companies count on claimants accepting initial offers without question, but you now understand how adjusters systematically undervalue vehicles using national databases that ignore local repair costs and market conditions. Three independent repair estimates, a full pre-repair mechanical inspection, and a certified appraisal shift the negotiation entirely in your favor.

Handling this process alone is possible, but the stakes are high-missing deadlines, submitting incomplete documentation, or accepting a lowball settlement without professional review costs you thousands. We at Schaar & Silva LLP have guided Santa Cruz County residents through property damage claims for years, and we’ve seen firsthand how proper documentation and strategic negotiation increase recovery amounts by $2,000 to $5,000 or more. You don’t have to navigate insurance company tactics alone.

Contact Schaar & Silva LLP for a free case evaluation. We’ll review your documentation, explain what your claim is actually worth, and advise whether negotiation or legal action makes sense for your situation.