After a car accident, insurance companies calculate your vehicle’s value using methods that aren’t always transparent. Understanding how this valuation works protects you from accepting unfair settlements.

At Schaar & Silva LLP, we’ve helped Santa Cruz County residents navigate damage claims and recognize when valuations fall short. This vehicle damage valuation guide walks you through the assessment process, common pitfalls, and your rights.

How Insurers Calculate Your Vehicle’s Damage Value

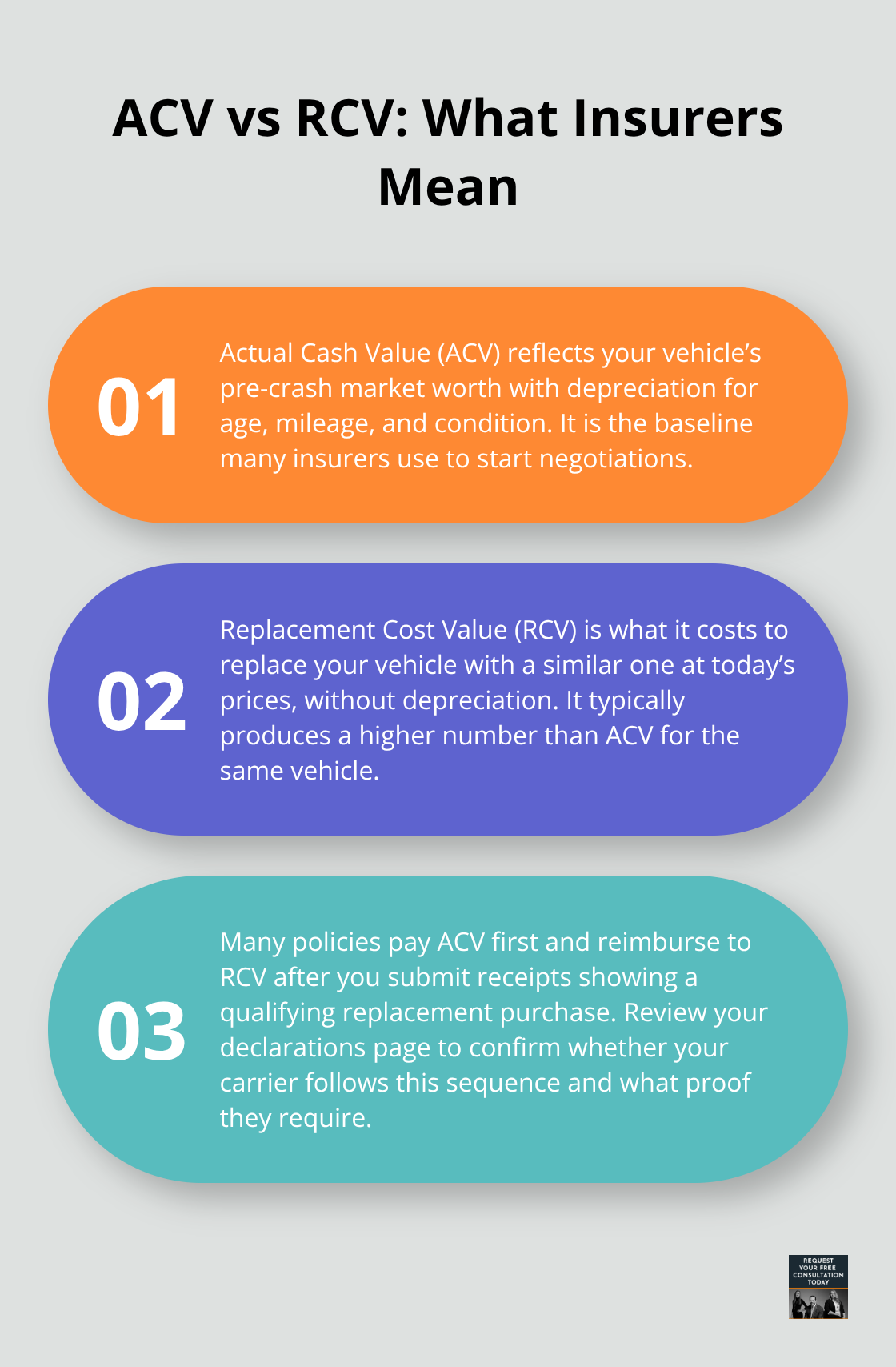

Insurance adjusters use two primary valuation methods after an accident: Actual Cash Value (ACV) and Replacement Cost Value (RCV). ACV reflects what your vehicle was worth before the crash, accounting for depreciation based on age, mileage, and condition. RCV is what it costs to replace your vehicle with a similar one at current market prices, without factoring in depreciation. Most insurers start with ACV offers and may only pay RCV later after you provide receipts for replacement purchases, potentially leaving you to cover costs out-of-pocket temporarily. Check your policy’s declarations page to see which method applies and whether your insurer pays ACV first and then reimburses the difference to RCV.

The problem is that adjusters frequently rely on NADA Guides (National Automotive Dealers Association) to establish your vehicle’s pre-accident value, but these guides consistently underestimate local repair costs. A car valued at $15,000 on NADA might actually require $18,000 or more to repair in Santa Cruz County due to local labor rates and parts availability. California law does not require insurers to rely exclusively on NADA guides, which means obtaining independent estimates from local shops weakens the insurer’s reliance on a single valuation and strengthens your negotiating position significantly.

What Three Independent Estimates Reveal

Collect repair estimates from at least three different licensed Santa Cruz shops before accepting any settlement offer. Present these written estimates to the adjuster and request written explanations for any valuation discrepancies to prevent lowball offers from becoming final. The gap between a low initial offer and real repair costs commonly ranges from $2,000 to $5,000, and multiple credible estimates make it harder for insurers to ignore your position.

Hidden damage such as frame misalignment, water intrusion behind panels, or suspension component failure can add $5,000 to $10,000 to the final repair bill and often goes undetected during initial inspections. Insist on a full pre-repair mechanical inspection from a licensed Santa Cruz technician who specifically checks frame straightness, suspension integrity, and electrical system damage before repairs begin. When the adjuster schedules an inspection, have your three independent estimates and pre-accident photos ready in writing so you can reference them immediately. California law allows you to rely on repairs performed at your chosen shop if they meet accepted trade standards, which gives you leverage when insurers resist local shop estimates.

Using Professional Appraisals to Challenge Low Valuations

Hire an independent certified appraiser to document your vehicle’s pre-crash condition and compare it to current market data. The typical upfront cost is $300 to $600, but this investment often justifies a $2,000 to $5,000 or higher settlement increase. California law supports your right to an independent valuation, and presenting this professional assessment shifts negotiation dynamics away from the insurer’s one-sided estimate.

When you submit a complete file containing your independent appraisal, three shop estimates, police report, and pre-accident photos, organized documentation makes it difficult for insurers to ignore your position. The next section covers the specific factors that influence how adjusters calculate your vehicle’s damage valuation and why some vehicles receive lower assessments than others.

What Drives Your Vehicle’s Damage Assessment

Age, Mileage, and Maintenance Records Shape Your Valuation

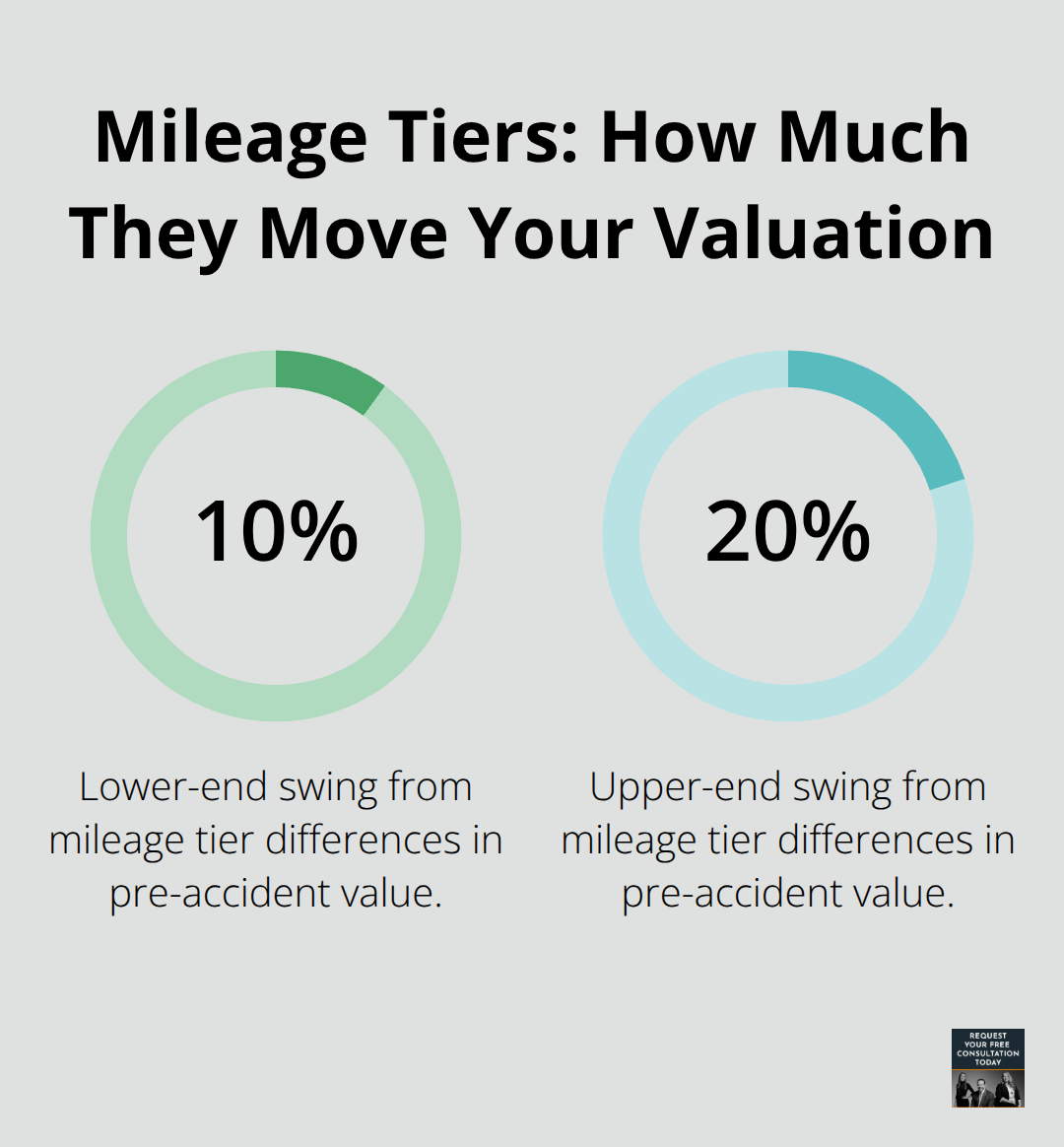

Your vehicle’s age, mileage, and maintenance history form the foundation of how adjusters calculate damage value, and these factors matter far more than most people realize. A 2015 Honda Civic with 95,000 miles and full service records receives a higher pre-accident valuation than an identical model with 120,000 miles and spotty maintenance documentation, even if both vehicles sustained identical damage. Adjusters use Kelley Blue Book values as their baseline, and KBB explicitly factors in mileage brackets to establish pre-accident market value. The difference between mileage tiers swings your valuation by 10 to 20 percent, which translates to hundreds or thousands of dollars in settlement offers.

Gather your maintenance receipts, service records, and any documentation showing regular oil changes, tire rotations, and major repairs before you meet with the adjuster. This evidence protects you from being penalized for wear and tear that the adjuster might otherwise blame on neglect rather than normal use.

Structural Damage and Hidden Costs

The type and extent of damage determines whether your claim stays within standard repair territory or enters the hidden-damage zone where costs explode. Frame misalignment, water intrusion behind door panels, and electrical system damage are structural issues that adjusters often miss during their initial walk-around inspection, yet they routinely add $5,000 to $10,000 to the final repair bill. Demand a full pre-repair mechanical inspection from a licensed Santa Cruz technician before accepting any settlement offer, and specifically request that the technician check frame straightness using laser alignment equipment, suspension integrity, and electrical continuity.

When the repair shop uncovers hidden damage during the actual repair process, submit updated estimates to the adjuster immediately with a written explanation of what was found. California law requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, but legitimate additional damage discovered mid-repair can extend this timeline. Present these updated estimates alongside your original three shop estimates so the adjuster sees a complete picture of what the vehicle actually requires, not just what was visible at first glance.

Documentation That Strengthens Your Position

Written estimates from multiple shops carry far more weight than verbal discussions with adjusters. California law allows you to rely on repairs performed at your chosen shop if they meet accepted trade standards, which gives you leverage when insurers resist local shop estimates. Collect repair estimates from at least three different licensed Santa Cruz shops before accepting any settlement offer, and present these written estimates to the adjuster with requests for written explanations of any valuation discrepancies.

The gap between a low initial offer and real repair costs commonly ranges from $2,000 to $5,000. Multiple credible estimates make it harder for insurers to ignore your position and force them to justify their numbers in writing. When you submit a complete file containing three shop estimates, police report, and pre-accident photos (organized chronologically), documentation makes it difficult for insurers to dismiss your claim without serious consideration.

The specific factors that influence your valuation extend beyond what adjusters see at first glance-they also include what happens when you challenge their initial assessment and present evidence that contradicts their numbers.

What Mistakes Cost You in Damage Valuations

Most Santa Cruz County residents make three critical errors that hand thousands of dollars to insurance companies. First, they accept repair cost estimates without verifying them against actual local shop pricing. Second, they fail to photograph and document every piece of damage immediately after the accident, leaving adjusters free to claim certain damage was pre-existing. Third, and most costly, they accept the initial settlement offer without presenting evidence that contradicts the insurer’s valuation. These mistakes compound because adjusters count on claimants not knowing what their vehicles actually cost to repair locally.

Why NADA Guides Fail Your Claim

When you skip independent estimates, you allow NADA Guides to set your settlement amount, even though those guides regularly undervalue Santa Cruz County repairs by $2,000 to $5,000 or more due to local labor rates and parts sourcing. The California Department of Insurance acknowledges that insurers must settle claims within 40 days after proof of loss, but this timeline pressure works against you if you haven’t prepared documentation in advance. Your first conversation with an adjuster should never happen without at least three written repair estimates from licensed local shops already in your file. These estimates aren’t suggestions-they’re evidence that forces the adjuster to justify any deviation in writing.

When Liberty Mutual offered only $400 on a diminished value claim for a 2024 Hyundai Tucson, the claimant’s calculated range based on the Mabry formula showed $650 to $715 was defensible, proving that initial offers are rarely fair assessments of actual loss.

Documentation That Prevents Lowball Offers

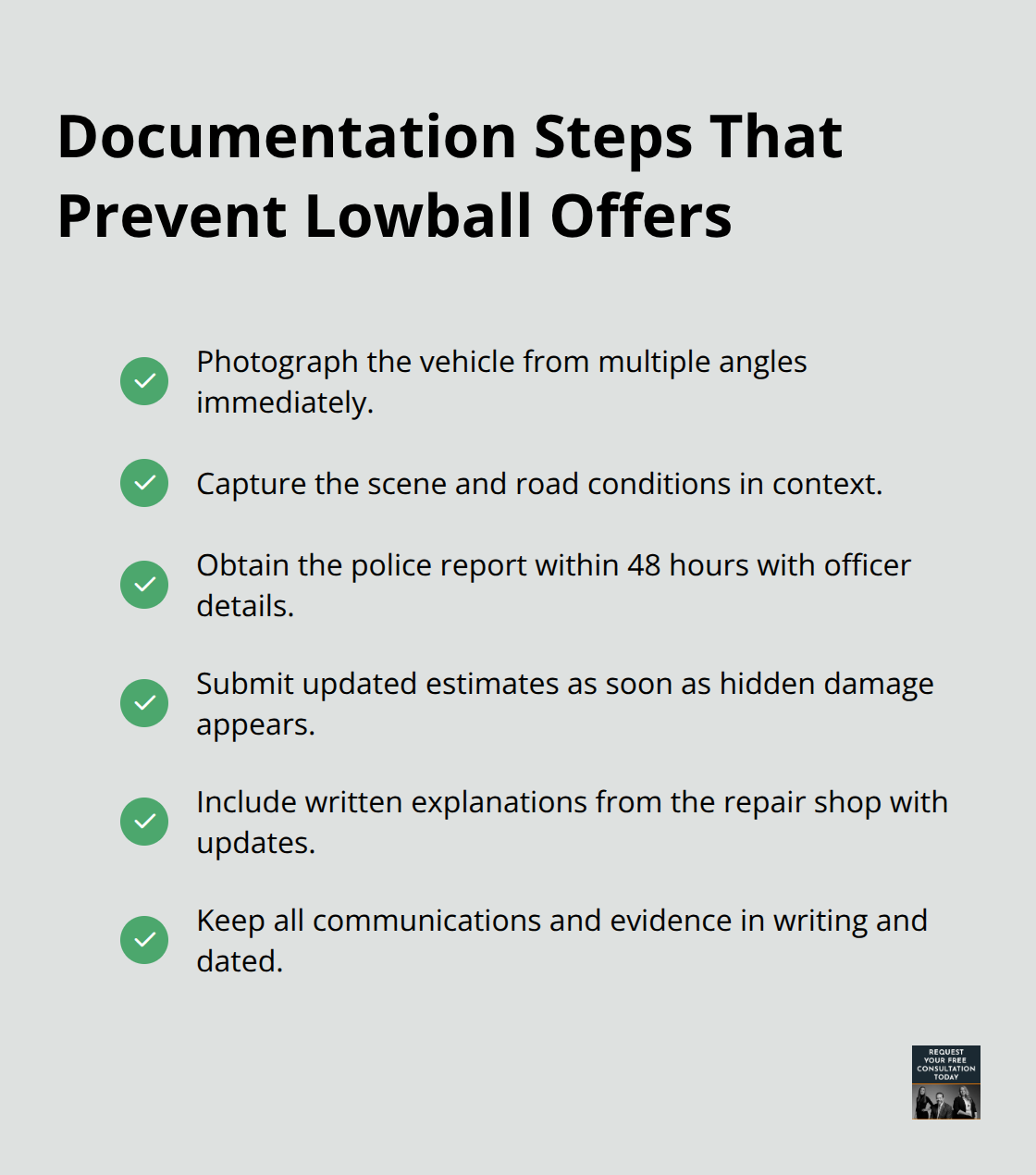

Photograph your vehicle from multiple angles immediately after the accident, capture the surrounding scene and road conditions, and obtain your police report within 48 hours while noting the officer’s name, badge number, and report number. This documentation prevents adjusters from later claiming damage was minor or pre-existing when photos clearly show otherwise. When hidden damage emerges during repairs (frame misalignment, water intrusion, electrical failures), submit updated estimates to the adjuster immediately with written explanations of what the repair shop discovered.

Organize everything chronologically in a dated file: police report, initial photos, three independent repair estimates, updated estimates if hidden damage appears, and pre-accident maintenance records. Present this complete package when you negotiate, not piecemeal over phone calls. California law allows you to rely on repairs performed at your chosen shop if they meet accepted trade standards, so don’t let adjusters pressure you into their preferred vendor network.

Forcing Fair Settlements Through Appraisal

If negotiations stall after you’ve presented solid documentation, invoke California’s appraisal provision: both sides select appraisers, a neutral umpire is chosen, and the umpire’s decision becomes binding. This mechanism often motivates insurers to improve their offers rather than face an independent determination. Many claimants settle for thousands less than they deserve simply because they negotiated verbally instead of in writing, leaving no record of what was actually disputed or agreed to.

Final Thoughts

Insurance companies treat initial offers as negotiating positions, not final settlements, and California law backs your right to challenge any valuation with independent evidence. You can obtain appraisals, repair estimates from shops of your choosing, and professional assessments that contradict the insurer’s numbers. This vehicle damage valuation guide demonstrates that organized documentation, multiple repair estimates, and written communication create leverage that verbal discussions never will.

If the adjuster’s valuation falls $2,000 or more below your three independent estimates, submit those estimates in writing and request written justification for the gap. When the insurer still resists, hire a certified appraiser to formally challenge their valuation or invoke California’s appraisal provision to force an independent determination. Track all communications in writing, keep copies of every estimate and photo, and maintain this file for at least three years under California’s property damage statute of limitations.

We at Schaar & Silva LLP assist Santa Cruz County residents in evaluating property damage claims and ensuring fair valuations for their losses. Our team reviews your documentation, identifies gaps in the insurer’s assessment, and guides you toward settlements that reflect actual repair costs rather than underestimated guide values. Contact Schaar & Silva LLP to discuss your specific situation and explore your options for recovery.