A car accident leaves you with more than just physical injuries-you’re facing vehicle damage repairs and a confusing insurance process. Insurance companies don’t always offer fair settlements, and many people accept lowball offers without understanding their options.

We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland navigate insurance claims and fight for the compensation they deserve. This guide walks you through coverage types, the claims process, and how to challenge unfair offers.

What Coverage Do You Actually Need for Vehicle Damage?

Collision Coverage Protects Your Vehicle in Impact Accidents

Collision coverage pays for damage to your vehicle when it hits another car, object, or structure. If you financed or leased your vehicle, your lender requires this coverage. The California Department of Insurance confirms that collision coverage reimburses repair costs or the actual cash value of your vehicle, whichever is less. Your deductible matters significantly-a $500 deductible instead of $250 can lower your premium by 15 to 30 percent annually, but you’ll pay more out of pocket after an accident.

Many drivers in Oakland and Sacramento underestimate repair costs. A typical fender-bender runs $2,500 to $7,500, and major collisions easily exceed $15,000. If your vehicle is worth less than $10,000, the math becomes critical-paying collision premiums on an older car might not make financial sense unless you cannot afford to replace it.

Comprehensive Coverage Handles Non-Collision Damage

Comprehensive coverage handles non-collision damage: theft, vandalism, weather, fire, and animal strikes. In Santa Cruz County and the greater Bay Area, vehicle theft claims have risen steadily, making comprehensive coverage valuable if you park on the street. The California Department of Insurance notes that comprehensive coverage also reimburses based on actual cash value or repair cost, whichever is lower.

Liability and Property Damage Coverage Protect Others, Not Your Vehicle

Liability coverage is mandatory in California, with minimums of $15,000 per person and $30,000 per incident for bodily injury, plus $5,000 for property damage, according to the California DMV. However, liability only covers damage you cause to others-it does nothing for your own vehicle. Many drivers confuse this distinction and assume their liability policy protects their car. Property damage liability covers the other vehicle or structures you hit, not yours.

If the other driver is uninsured or underinsured, your uninsured motorist property damage coverage (if you purchased it) steps in. California law permits you to claim diminished value-the reduction in your vehicle’s resale value after an accident. Insurers rarely volunteer this loss, so you must document your vehicle’s condition before and after the accident with detailed photos and maintenance records to support a diminished value claim.

Understanding these coverage types helps you make informed decisions about your policy. The next section walks you through what happens immediately after an accident and how to document everything properly to protect your claim.

Getting Your Claim Right From the Start

Document the Accident Scene Thoroughly

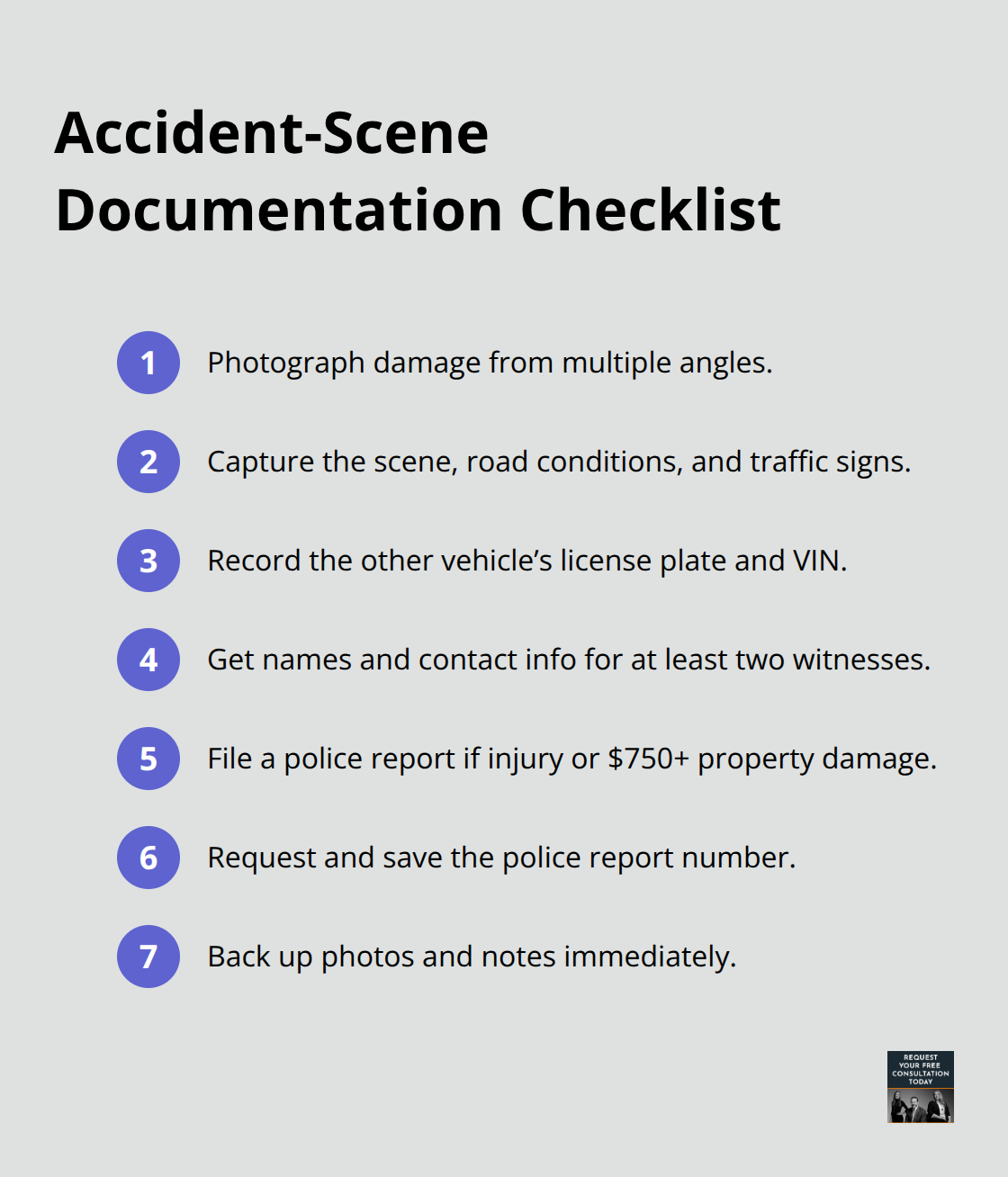

The moments after a collision determine whether you receive fair compensation or accept a lowball settlement. Start documenting immediately at the scene, even if you’re injured. Take photos of vehicle damage from multiple angles, capture the accident location, road conditions, traffic signs, and the other vehicle’s license plate and VIN.

Visual evidence strengthens your claim significantly. Include wide shots showing how vehicles are positioned and close-ups of specific damage areas. If your phone dies or you forget details later, this photographic record becomes your backup.

Collect the other driver’s name, address, phone number, driver’s license number, license plate, vehicle make and model, and insurance information. Get names and contact information from at least two witnesses, as their statements often carry more weight than yours alone when disputes arise. File a police report if there’s injury or property damage exceeding $750, as required by California law within 10 days of the accident. Request the police report number immediately and save it.

Contact Your Insurer Quickly and Strategically

Contact your insurer within 24 hours of the accident, not days later. The California Department of Insurance requires insurers to acknowledge your claim and respond within 15 days, then decide within 40 days after you submit proof of loss. Your insurer will assign an adjuster who inspects your vehicle and prepares a damage estimate. This is where most people make critical mistakes. Do not accept the insurer’s first estimate without question.

Obtain independent repair estimates from two manufacturer-certified shops in your area, which typically cost nothing. Compare these estimates against the insurer’s valuation line by line. If significant discrepancies exist, the insurer must justify their lower figures. Insurers sometimes recommend cheaper repair facilities that use aftermarket parts instead of original equipment manufacturer parts, which can compromise safety and resale value.

Assert Your Right to Choose Your Repair Facility

You have the absolute right to choose your own repair facility and demand OEM parts. Document your vehicle’s condition before the accident with maintenance records, service receipts, and photos if available. This evidence supports claims for diminished value, which California law permits but insurers rarely volunteer. The appraisal clause in your policy allows you to dispute the settlement amount by hiring your own appraiser; if you and the insurer disagree, both appraisers select a neutral umpire whose decision becomes binding.

Consider consulting with an attorney if the insurer’s estimate seems substantially low or if they deny coverage. Legal representation often recovers amounts far exceeding attorney costs. When disputes over property damage arise in Santa Cruz County, the legal team at Schaar & Silva LLP can assist in evaluating the extent of property damage and help you receive a fair valuation for your loss. The next section addresses what happens when you challenge unfair settlement offers and how to navigate the depreciation calculations that insurers use to reduce your payout.

Fighting Back Against Lowball Settlement Offers

How Insurers Calculate Vehicle Depreciation

Insurance adjusters calculate damage settlements using depreciation formulas that systematically reduce what they owe you. The actual cash value method, which California insurers use, subtracts depreciation from the vehicle’s market value before the accident. A five-year-old vehicle with 80,000 miles loses 10 to 15 percent of its value annually, meaning your insurer’s initial estimate often reflects this depreciation rather than true replacement cost. When an adjuster values your 2020 sedan at $18,000 after an accident, they’ve already factored in age and mileage, even though you need that full amount to purchase a comparable replacement vehicle.

Challenge the Insurer’s Valuation With Evidence

Collect evidence of your vehicle’s pre-accident condition through maintenance records, service receipts, and photos showing mechanical condition and interior quality. Request the insurer’s valuation worksheet and challenge line items where repair costs seem artificially low. If the adjuster estimated $3,500 for a bumper replacement when local shops quote $5,200, the discrepancy matters. Obtain written estimates from at least two manufacturer-certified repair facilities in your area and submit them to your adjuster with a detailed explanation of why their estimate falls short. The California Department of Insurance requires insurers to respond to additional documentation within 15 days, and many will increase their offer when presented with competitive estimates from reputable shops.

Navigate Total Loss Disputes and Salvage Value

Depreciation disputes escalate quickly when your vehicle is declared a total loss. Insurers use either a percentage-based threshold or a total loss formula that subtracts salvage value from fair market value to determine total loss. If your vehicle’s repair cost reaches or exceeds its fair market value, the insurer declares it totaled and pays you the vehicle’s actual cash value minus your deductible and any salvage value they recover. This calculation often leaves you underwater, particularly if you financed the vehicle.

The appraisal clause in your policy gives you a powerful tool: hire your own independent appraiser to challenge the insurer’s valuation, and if disagreement persists, both appraisers select a neutral umpire whose decision becomes binding. This process costs $300 to $600 but frequently recovers thousands in additional compensation. If you’re facing a total loss settlement that leaves you owing money on a loan, gap insurance should have covered the difference, but if you didn’t purchase it, your options narrow significantly unless the insurer’s valuation was genuinely unreasonable.

When to Pursue Legal Action for Property Damage

For property damage disputes in Santa Cruz County, an attorney can evaluate whether the insurer’s valuation aligns with actual replacement costs and help you pursue fair compensation through negotiation or appraisal.

Final Thoughts

Vehicle damage repairs after an accident demand attention to detail and persistence. You now understand the coverage types protecting your vehicle, the documentation required to support your claim, and the tactics insurers use to minimize payouts. Collision and comprehensive coverage form the foundation of vehicle protection, but only if you understand your policy limits and deductibles.

The claims process rewards those who act quickly and gather evidence immediately. Photos from the accident scene, police reports, and independent repair estimates create a record that insurers cannot easily dismiss. When you contact your insurer within 24 hours and provide thorough documentation, you establish credibility and set expectations for fair treatment.

Depreciation calculations and total loss valuations often shortchange accident victims who accept initial offers without question. The appraisal clause in your policy gives you leverage to dispute unfair settlements through binding arbitration, and independent appraisers frequently recover thousands in additional compensation. If you’re facing a complex vehicle damage repairs claim or settlement disputes in Santa Cruz County, Sacramento, or Oakland, the team at Schaar & Silva LLP can evaluate your claim and help you pursue fair compensation.