A car accident in California can leave you facing medical bills, vehicle repairs, and lost wages. Understanding vehicle liability in California is the first step toward recovering what you’re owed.

At Schaar & Silva LLP, we help accident victims navigate California’s negligence laws and build strong claims. This guide covers the facts you need to know about liability, damages, and the process ahead.

How California Determines Fault in Auto Accidents

The Fault-Based System and Negligence

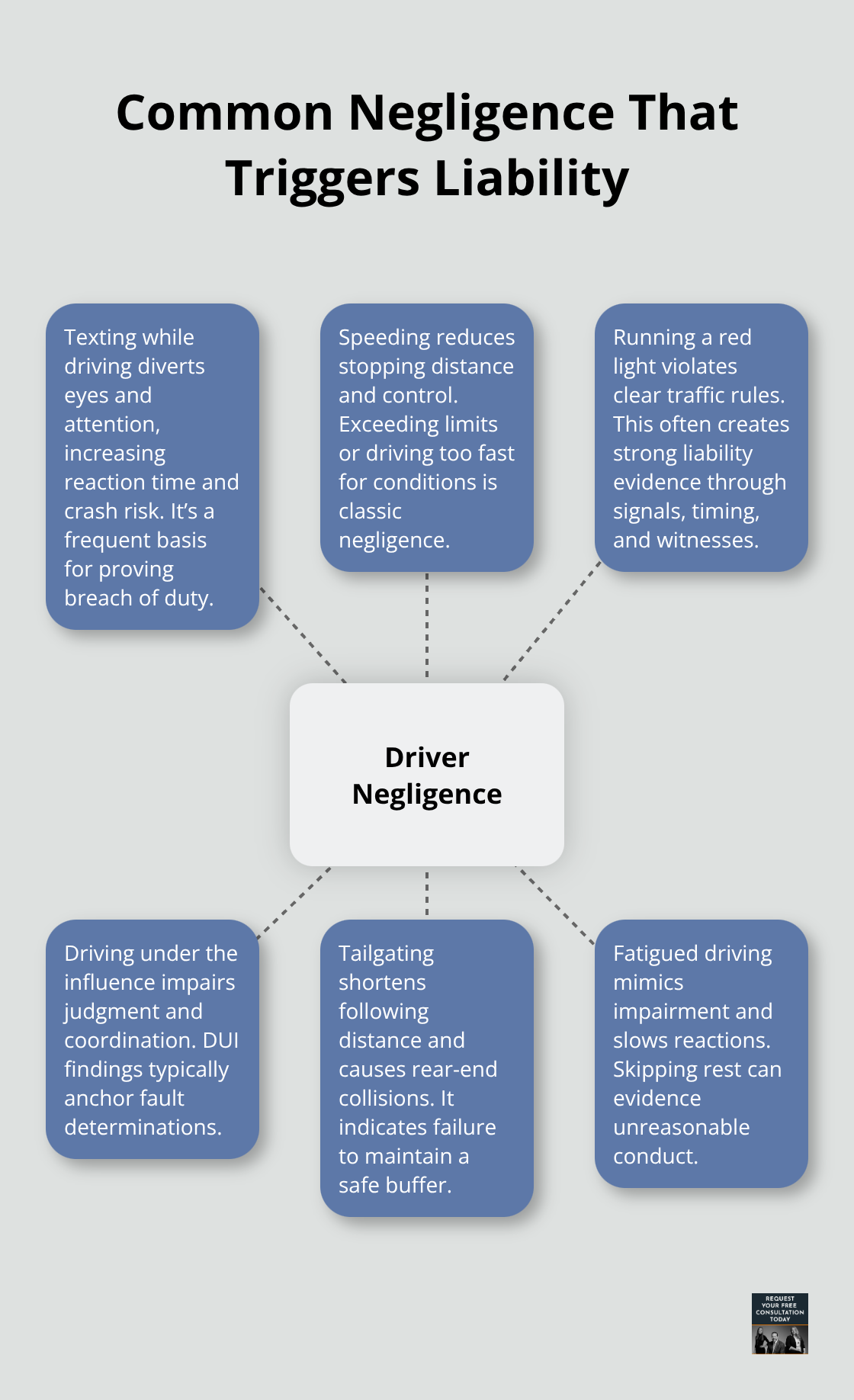

California operates under a fault-based system, meaning you must prove the at-fault driver’s negligence to recover compensation. Negligence occurs when a driver fails to act reasonably under the circumstances. That failure takes many forms: texting while driving, speeding, running a red light, driving under the influence, tailgating, fatigued driving, or skipping vehicle maintenance. The at-fault driver’s insurer becomes liable for your damages up to the policy limits.

Updated Liability Minimums in California

Under SB 1107, policies issued or renewed after January 1, 2025 must carry minimum liability of $30 per person and $60 per accident for bodily injury, plus $15 for property damage. These higher minimums expand the available coverage, but only for newly issued or renewed policies. If you were partly at fault, California’s pure comparative negligence rule still allows you to recover, but your award gets reduced by your percentage of fault. For example, if damages total $100,000 and you’re found 25 percent at fault, you recover $75,000.

How Evidence Determines Liability

Police reports, witness statements, dashcam footage, and physical evidence at the scene all establish fault. Insurance companies often dispute liability to minimize their payouts-they may argue the other driver wasn’t negligent, question injury severity, or claim you contributed to the accident. Gathering strong evidence immediately after the crash strengthens your position. Photograph the scene from multiple angles, collect witness contact information, request the police report number, and obtain medical evaluation the same day.

Building Your Evidence Trail

Medical documentation proves your injuries occurred as a direct result of the accident. Do not admit fault, speculate about speeds or positions, or provide recorded statements to the insurer without legal guidance. These mistakes can undermine your claim significantly. Insurance adjusters use tactics to undervalue claims, including quick settlement offers and social media monitoring, so protecting your evidence and statements matters from day one.

Protecting Your Claim From the Start

Early professional involvement preserves evidence and prevents costly errors. We at Schaar & Silva LLP help clients in Santa Cruz County, Sacramento, and Oakland coordinate with medical providers, reconstruct accident scenes, and negotiate with insurers who attempt to minimize liability. With proper documentation and legal support in place, you’re positioned to move forward with confidence toward settlement negotiations.

What Damages Can You Recover After a California Auto Accident

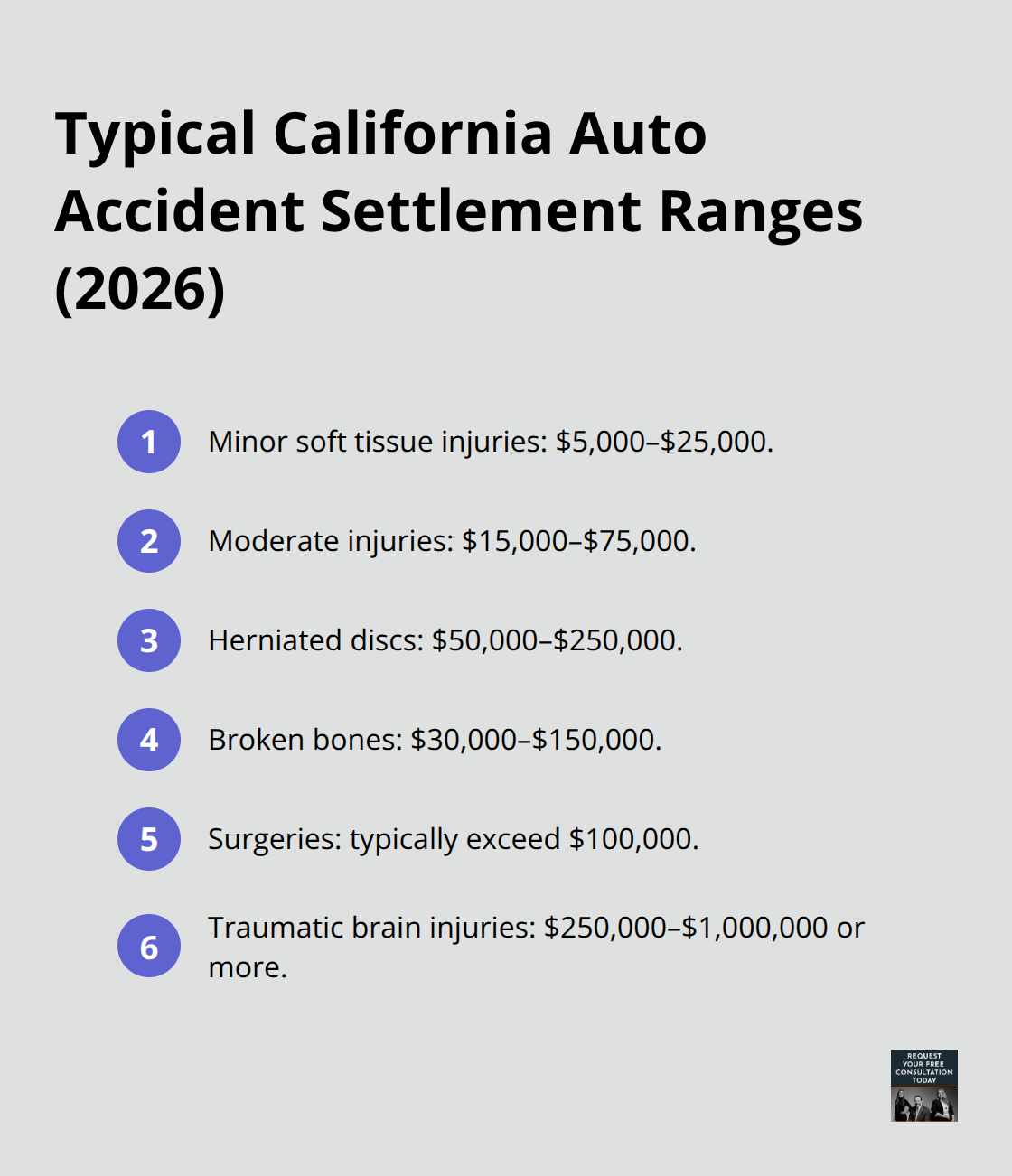

California law recognizes two main categories of damages: economic and non-economic. Economic damages cover tangible, measurable losses like medical bills, vehicle repairs, and lost wages. Non-economic damages compensate for pain, suffering, and reduced quality of life. A 2026 settlement analysis shows typical ranges by injury type: minor soft tissue injuries settle between $5,000 and $25,000, moderate injuries between $15,000 and $75,000, herniated discs between $50,000 and $250,000, broken bones between $30,000 and $150,000, and surgeries typically exceed $100,000.

Traumatic brain injuries often reach $250,000 to $1,000,000 or more.

How Medical Documentation Strengthens Your Claim

Objective medical evidence like MRI results, surgical reports, and specialist evaluations dramatically increases settlement value and makes it harder for insurers to minimize your claim. Gaps in medical care reduce claim value significantly, so you should seek timely, continuous treatment from the accident through maximum medical improvement. This approach maintains a strong paper trail that supports your recovery amount. Insurance companies scrutinize claims with inconsistent medical records, so consistent care demonstrates the severity of your injuries.

Understanding Property Damage and Vehicle Valuation

Property damage claims require understanding actual cash value, which represents the fair market price a knowledgeable buyer and seller would agree on in an arm’s-length transaction. For physical damage claims, insurers typically pay the lesser of repair cost or the vehicle’s actual cash value. If you chose your own repair shop rather than the insurer’s preferred facility, the insurer must still pay reasonable costs for repairs according to accepted trade standards and cannot artificially discount costs to pressure you into their network. Many policies include an appraisal provision to resolve total-loss disputes: two appraisers (one selected by each side) meet with a neutral umpire, and the agreed amount becomes binding.

Non-Economic Damages and Pain and Suffering

Non-economic damages like pain and suffering represent the largest component of most settlements in California, which has no cap on these damages. Settlement multipliers typically range from 1.5 to 5 times your economic damages, depending on injury severity and documentation quality. For catastrophic injuries, multipliers can exceed 5 times. Lost wages matter considerably-include time off work and reduced future earning potential, particularly if you’re self-employed or a high earner. Support these claims with tax returns, pay stubs, and employer letters. Permanency and long-term injuries like chronic pain or ongoing care dramatically boost settlement value; a life care plan projecting lifetime medical needs and associated costs strengthens your position.

Closing Coverage Gaps With Uninsured Motorist Protection

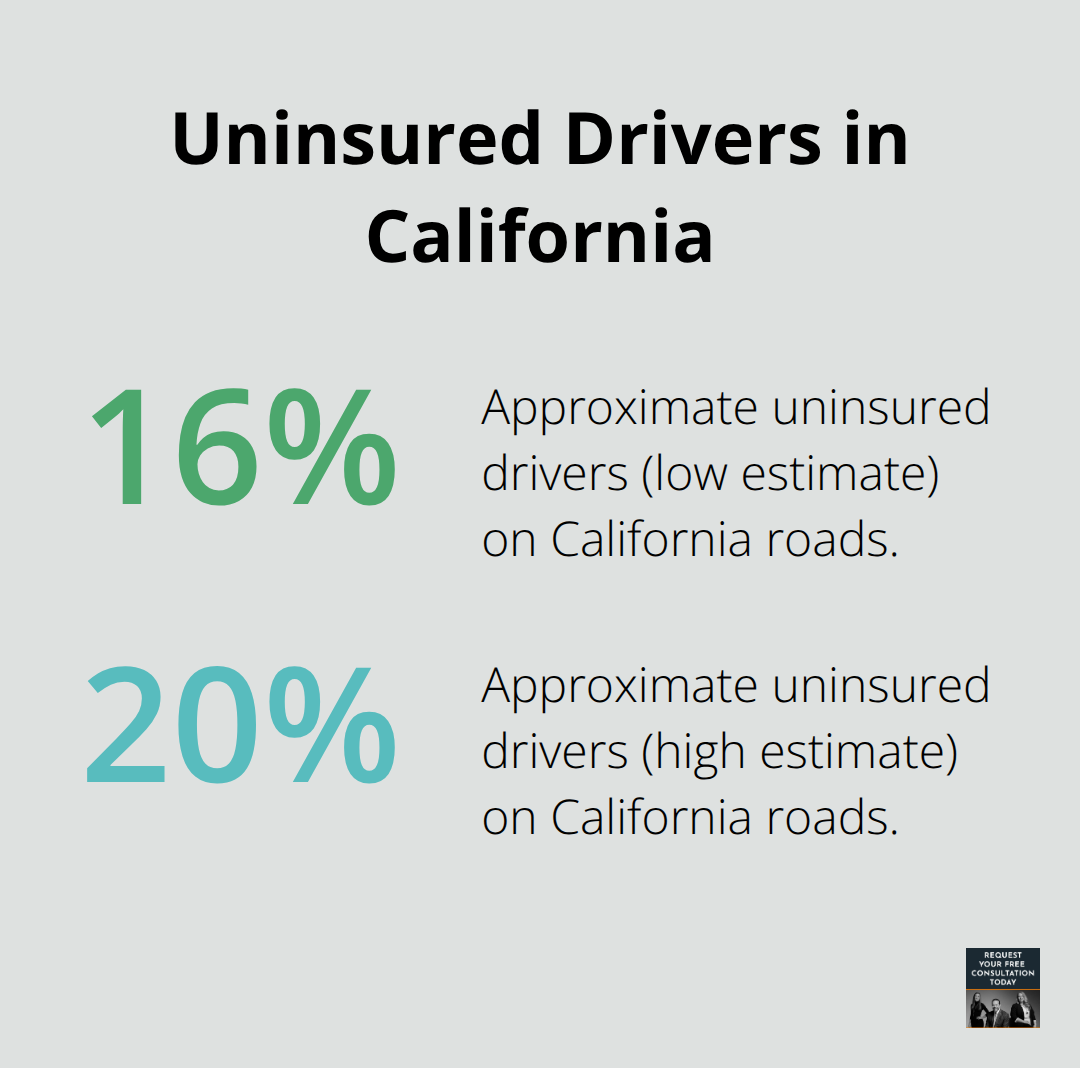

If the at-fault driver carries insufficient insurance, your uninsured or underinsured motorist coverage steps in to bridge the gap. California requires insurers to offer uninsured motorist coverage, and approximately 16 to 20 percent of drivers on California roads carry no insurance, making this protection vital. Fair Claims Settlement Practices require insurers to acknowledge claims within 15 days, respond within 15 days, decide within 40 days, and pay within 30 days after settlement.

Understanding these timelines helps you track whether your insurer meets legal obligations. With proper documentation of your damages and clear knowledge of available coverage, you’re ready to move forward with building your claim and negotiating with insurance companies.

How to Protect Your Claim From Day One

Act Immediately at the Accident Scene

The first hours after an accident determine whether your claim succeeds or fails. At the scene, photograph the vehicle damage from multiple angles, the road conditions, traffic signals, and any visible injuries. Collect the names and phone numbers of all witnesses, not just their statements. Request the police incident number or report number on the spot-this becomes critical evidence later. If you’re injured, seek medical evaluation the same day, even if symptoms seem minor. Insurance adjusters scrutinize gaps in medical records, so immediate documentation creates a credible timeline that strengthens your claim.

Avoid Statements That Destroy Your Claim

Do not admit fault, speculate about speeds or positions, or provide recorded statements to the other driver’s insurer. These statements become permanent evidence that can destroy your settlement value. Many drivers make the mistake of saying things like “I’m sorry” or “I didn’t see you coming,” which insurers weaponize as admissions of negligence. Keep your statements factual and minimal at the scene and in all future communications.

Report to Your Insurer and Track Deadlines

Report the accident to your own insurer within the timeframe stated in your policy-typically within 24 to 72 hours. Provide only basic facts: date, time, location, vehicles involved, and the police report number. Do not speculate about injuries or liability. California law requires insurers to acknowledge claims within 15 days and respond within 15 days, so track these deadlines carefully. Insurance companies use delay tactics and surveillance to undervalue claims, including social media monitoring, so avoid posting about the accident or your injuries online.

Build a Medical Documentation Trail

Medical documentation proves causation and injury severity; obtain records from every provider who treats you, including ER visits, follow-up appointments, physical therapy, and specialist evaluations. Objective evidence like MRI results, surgical reports, and imaging studies makes claims substantially harder for insurers to minimize. If you miss appointments or delay treatment, adjusters will argue your injuries weren’t serious, reducing your settlement significantly. Consistent medical care from the accident through maximum medical improvement demonstrates injury severity and protects your recovery amount.

Understand Settlement Timelines and Avoid Premature Deals

Most soft-tissue claims settle within 3 to 6 months, but surgical or spinal injuries require 18 to 36 months for proper resolution. Settling prematurely costs you tens of thousands of dollars in uncompensated future medical care and lost earning capacity. Legal representation early in the process stops insurers from pressuring you into low settlement offers before maximum medical improvement is reached. We at Schaar & Silva LLP help clients in Santa Cruz County coordinate medical care, organize medical records, and communicate with insurers to prevent these costly errors.

Final Thoughts

Vehicle liability in California determines who pays for your medical bills, lost wages, and vehicle repairs after an accident. Understanding negligence, comparative fault, and damage categories protects your claim from day one, and California’s pure comparative negligence rule means you recover even if partly at fault-though your award gets reduced by your percentage of responsibility. The key is building a strong evidence trail immediately: photograph the scene, seek medical care the same day, collect witness information, and avoid statements that admit fault or speculate about the accident.

Settlement value depends on medical documentation, injury severity, and how well you preserve evidence (soft-tissue claims typically settle in 3 to 6 months, while surgical or spinal injuries require 18 to 36 months for proper resolution). Settling too early costs you thousands in uncompensated future care and lost earning capacity, and insurance companies use delay tactics, social media monitoring, and low initial offers to minimize what you receive. Professional guidance matters from the start to counter these tactics and protect your recovery.

We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland navigate vehicle liability California claims with medical bill support through lien services, property damage evaluation, and coordination with medical providers to build your strongest case. Contact us for a free case evaluation to understand your options and get realistic guidance on settlement value.