Insurance companies often undervalue vehicles in Santa Cruz property damage claims. They rely on formulas and databases that don’t account for your car’s actual condition or local market realities.

At Schaar & Silva LLP, we’ve seen countless settlement offers that fall short of what vehicles are truly worth. The good news is you have concrete tools to fight back-independent appraisals, documentation, and comparative market data that prove your case.

How Insurance Companies Value Your Vehicle

Insurance companies rely on three primary valuation methods, and understanding each one reveals why their initial offers often undervalue your Santa Cruz vehicle. They pull data from NADA Guides, which provides wholesale and retail values based on year, make, model, mileage, and condition. However, NADA Guides frequently undervalue local repair costs. A vehicle valued at $15,000 on NADA might cost $18,000 or more to repair in Santa Cruz due to local labor rates and parts availability.

Adjusters typically inspect your vehicle once, usually for less than an hour, and rely heavily on these database values without accounting for hidden damage. They assess visible condition and mileage but rarely uncover structural frame damage, suspension issues, water intrusion, or electrical system problems that add $5,000 to $10,000 to actual repair costs. Depreciation calculations also work against you because insurers apply standard depreciation tables that don’t reflect your specific vehicle’s market position in Santa Cruz County right now.

The NADA Trap and Local Market Reality

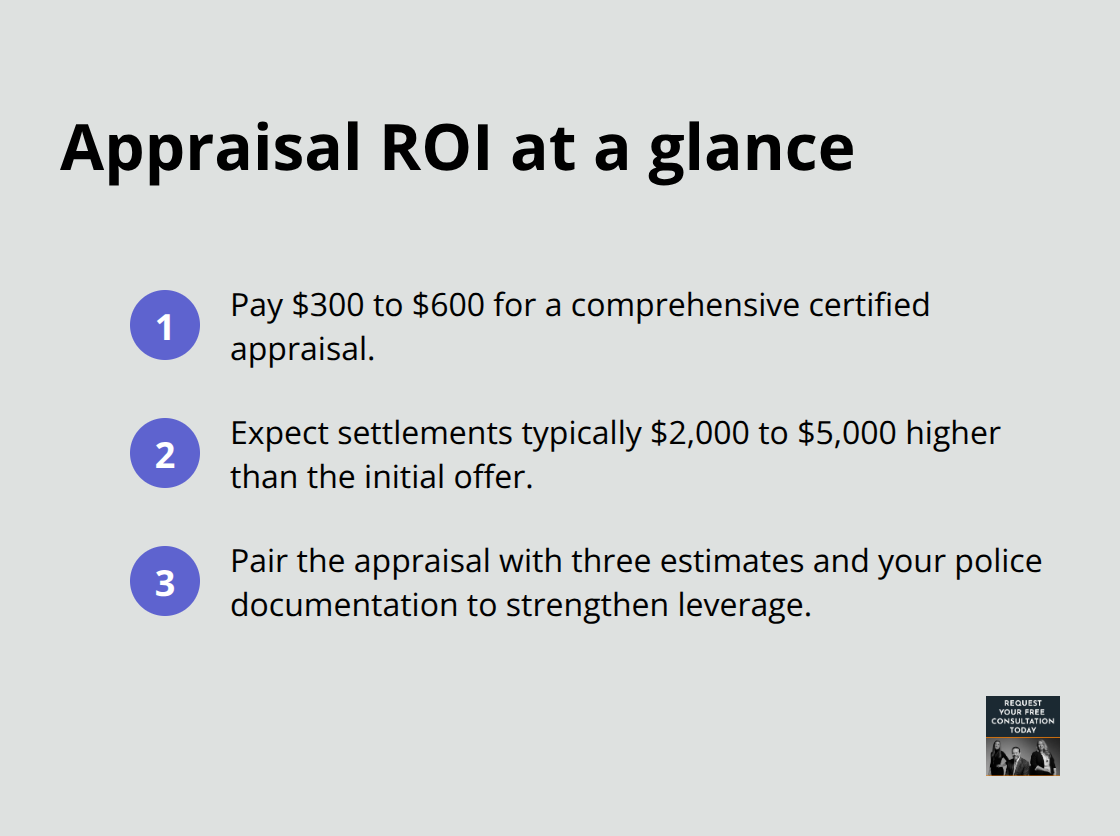

California law does not require insurers to use NADA exclusively, yet most do because it keeps payouts lower. This is a critical distinction. You are not bound by their valuation method. Obtain repair estimates from at least three independent Santa Cruz shops-not the insurer’s preferred vendors-to reveal the gap between NADA values and actual local costs. This comparison typically uncovers discrepancies of $2,000 to $5,000 or more. Hire an independent certified appraiser to counter NADA valuations; the cost runs $300 to $600 and often justifies settlements $2,000 to $5,000 higher. California law supports your right to an independent valuation, and appraisers familiar with Santa Cruz’s repair ecosystem understand local pricing pressures that national databases miss.

Documentation That Shifts the Balance

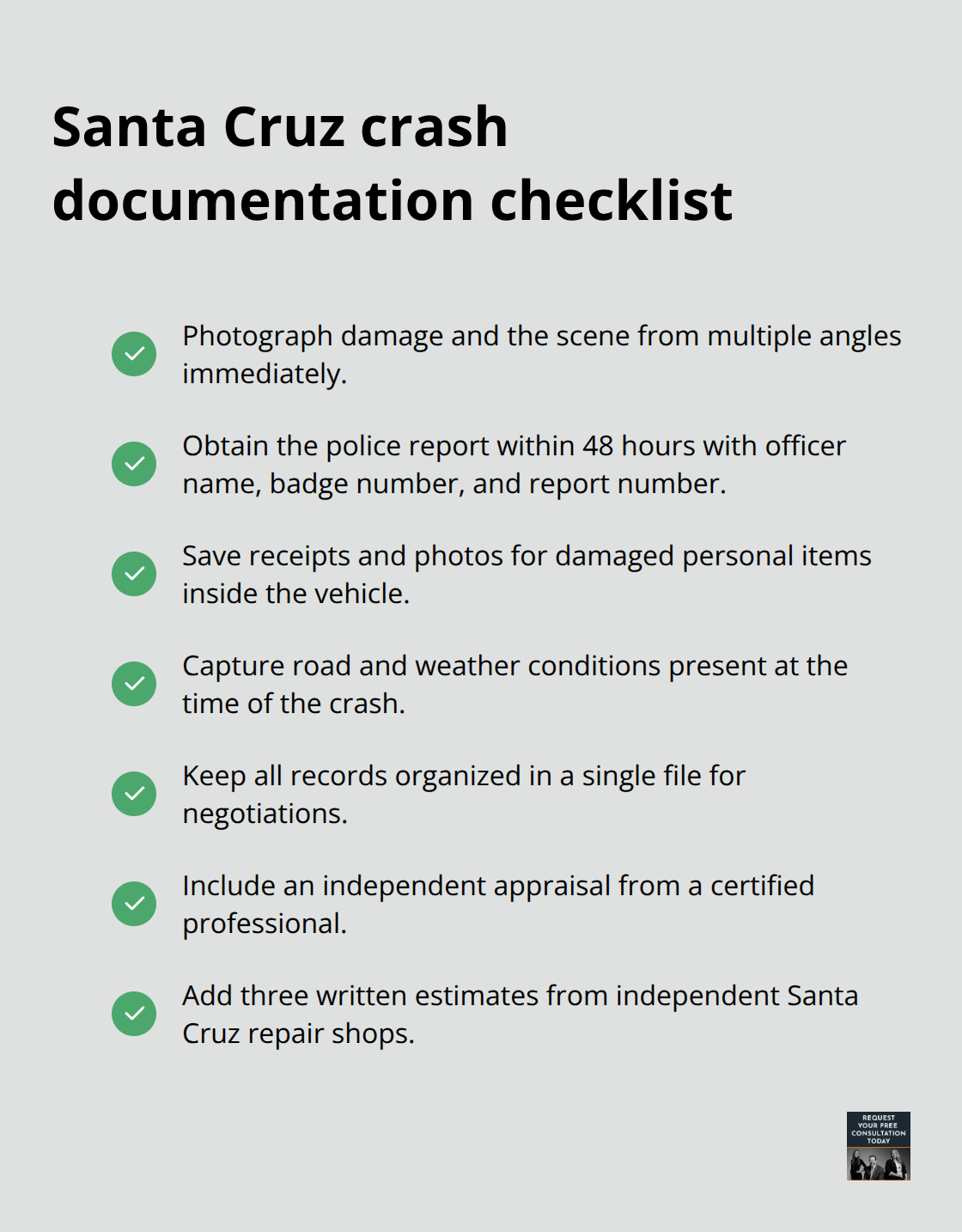

Photograph your vehicle from multiple angles immediately after the crash, capturing the scene and road conditions. Obtain the police report within 48 hours, including the officer’s name, badge number, and report number. Document any personal items damaged inside the car (laptops, glasses, clothing, tools) with receipts and photos; these are recoverable under California law. Organize all records in a single file and maintain them throughout negotiations, since California’s three-year statute of limitations for property damage claims means documentation matters for the full timeline. Present a complete file to the insurer: independent appraisal, three independent shop estimates, police report, and organized records. This defensible position shifts negotiations in your favor and forces insurers to justify why they’re rejecting documented evidence of your vehicle’s actual value.

What Comes Next in Your Claim

The gap between what insurers offer and what your vehicle is actually worth typically ranges from $2,000 to $5,000 or more. Most Santa Cruz claimants accept the first settlement without documentation, leaving money on the table. The next section shows you how to negotiate your auto insurance settlement with local appraisers who understand Santa Cruz’s market conditions and can provide the professional validation your claim needs to move forward.

How to Fight Back Against Undervalued Settlements

Insurance adjusters count on you accepting their first offer without question. The initial settlement they propose typically sits $2,000 to $5,000 below what your vehicle is actually worth in Santa Cruz’s repair market. You have three concrete tools to shift this dynamic: independent appraisals from certified professionals, photographic documentation from immediately after the accident, and comparative repair estimates that expose the gap between national databases and local reality.

Document the Accident Scene Immediately

Start with photography the moment the accident happens. Photograph your vehicle from multiple angles, capture the accident scene and road conditions, and secure the police report within 48 hours including the officer’s name, badge number, and report number. These records establish the baseline for your claim and prevent the insurer from rewriting the accident narrative later.

Document personal items damaged inside the vehicle-laptops, glasses, clothing, tools-with receipts and photos; California law makes these recoverable and insurers often overlook them in initial settlements.

Obtain Three Independent Repair Estimates

Contact three independent Santa Cruz repair shops (not the insurer’s preferred vendors) and request written estimates for full repairs. This step exposes what NADA Guides hide: a vehicle valued at $15,000 on NADA might require $18,000 or more to repair properly in Santa Cruz due to regional labor rates and parts availability. The three estimates create documented proof of the actual cost to restore your vehicle to pre-accident condition and reveal the gap between national databases and local market reality.

Hire a Certified Independent Appraiser

An independent certified appraiser costs $300 to $600 and typically justifies settlements $2,000 to $5,000 higher than the initial offer. California law supports your right to an independent valuation, and appraisers familiar with Santa Cruz’s repair ecosystem understand local pricing pressures that national databases miss. Insist the appraiser conduct a full pre-repair mechanical inspection that specifically checks frame straightness, suspension integrity, and electrical system damage. Hidden damage behind panels and within structural components adds $5,000 to $10,000 to repair costs, and a thorough inspection uncovers what a one-hour adjuster inspection will not.

Present a Complete Documentation Package

Organize all records in a single file: the independent appraisal, three repair estimates, police report, photographs, receipts for personal items, and your inspection documentation. Present this complete package to the insurer in writing. This defensible position forces adjusters to justify in writing why they’re rejecting documented evidence of your vehicle’s actual value. California’s repair shop protection law means insurers must stand behind repairs performed at your chosen shop if they meet industry standards, lending additional weight to estimates from reputable local shops. Most Santa Cruz claimants accept the first settlement without this documentation, leaving thousands on the table. The gap exists precisely because insurers know most people won’t push back. When the insurer receives your organized evidence, the negotiation shifts from their initial lowball offer to a conversation grounded in facts they cannot easily dismiss.

Local Santa Cruz Appraisers: Your Leverage in Negotiations

Finding the Right Certified Appraiser

The American Society of Appraisers maintains a directory of certified members that you can filter by location and specialty in automotive valuation. Look specifically for appraisers holding the AAA (Accredited Appraiser of Automobiles) credential, which requires extensive training in vehicle valuation methodology and adherence to the Uniform Standards of Professional Appraisal Practice. Many Santa Cruz body shops and independent repair facilities recommend appraisers they’ve worked with on complex damage assessments; these referrals often point you toward professionals who understand local market conditions and carry credibility with insurers. Avoid appraisers connected to the insurance company or the insurer’s preferred vendors, as their independence becomes questionable in negotiations. An appraiser working for you alone has no obligation to the insurance company and can advocate for your vehicle’s actual value without pressure to keep payouts low.

What the Appraisal Process Reveals

The appraisal process takes two to four hours and involves far more detail than the one-hour adjuster inspection you received from the insurer. A certified appraiser photographs your vehicle from multiple angles, documents visible damage, and performs a full mechanical inspection checking frame straightness with specialized equipment, suspension integrity, electrical system function, and hidden damage behind panels and within structural components. This thorough assessment uncovers the $5,000 to $10,000 in hidden costs that adjusters miss because they lack the time and incentive to investigate further. Once the appraisal is complete, you receive a detailed written report with photographs, component-by-component condition assessments, and a professional valuation backed by comparable market data specific to Santa Cruz County.

The Cost and Return on Your Investment

The cost ranges from $300 to $600 for a comprehensive appraisal, and this investment typically justifies settlements $2,000 to $5,000 higher than the insurer’s initial offer. When you present this report alongside your three independent repair estimates and police documentation, you shift from defending yourself against the insurer’s lowball offer to forcing them to defend why they’re rejecting a professional expert’s assessment.

Insurers understand that certified appraisals carry weight in disputes and in potential litigation, making them far more likely to increase their settlement offer rather than escalate to the California Appraisal Provision or court proceedings.

How Professional Appraisals Transform Your Position

The appraiser’s credibility and independence transform your negotiating position from weak to strong. Insurers know that a certified appraisal creates a documented record they cannot easily dismiss in settlement discussions or legal proceedings. The professional assessment validates your claim with objective data and shifts the burden of proof onto the insurance company to justify their lower valuation.

Final Thoughts

You now have the framework to fight back against undervalued settlements in Santa Cruz property damage claims. The three-step approach-independent appraisal, multiple repair estimates, and organized documentation-closes the gap between what insurers initially offer and what your vehicle is actually worth. Most claimants leave $2,000 to $5,000 on the table when they accept the first settlement without evidence.

Start with documentation immediately after the accident: photographs, police reports, and repair estimates from local shops create the foundation for your claim. Then hire a certified appraiser to validate your vehicle’s true value with professional expertise. Present everything together in writing, and the insurer must justify their position against documented facts rather than national databases that ignore Santa Cruz property damage realities and local market conditions.

If the insurer refuses to increase their offer despite your evidence, California’s Appraisal Provision gives you a formal dispute resolution process where both sides select appraisers and an umpire whose binding decision can push settlements higher. When negotiations stall or the gap remains unacceptable, contact Schaar & Silva LLP to evaluate your property damage claim and determine whether pursuing litigation makes financial sense for your situation. Your vehicle’s value is what the evidence proves, not what the insurer says it is.