After a crash, figuring out what your vehicle is actually worth becomes one of your biggest concerns. Insurance companies use specific methods to calculate damage, and understanding how they work puts you in a stronger position.

We at Schaar & Silva LLP have helped countless people in Santa Cruz County, Sacramento, and Oakland navigate this process. This vehicle damage valuation guide walks you through exactly what happens when adjusters assess your claim, what documentation you need, and the mistakes that cost people money.

How Insurance Companies Calculate What Your Vehicle Is Worth

Three Valuation Methods Adjusters Use

Insurance adjusters apply three primary valuation methods when assessing vehicle damage: the comparative market analysis approach, the cost-of-repair method, and automated valuation models like CCC reports. The comparative market analysis examines what similar vehicles in your local area sell for, accounting for mileage, condition, and trim level.

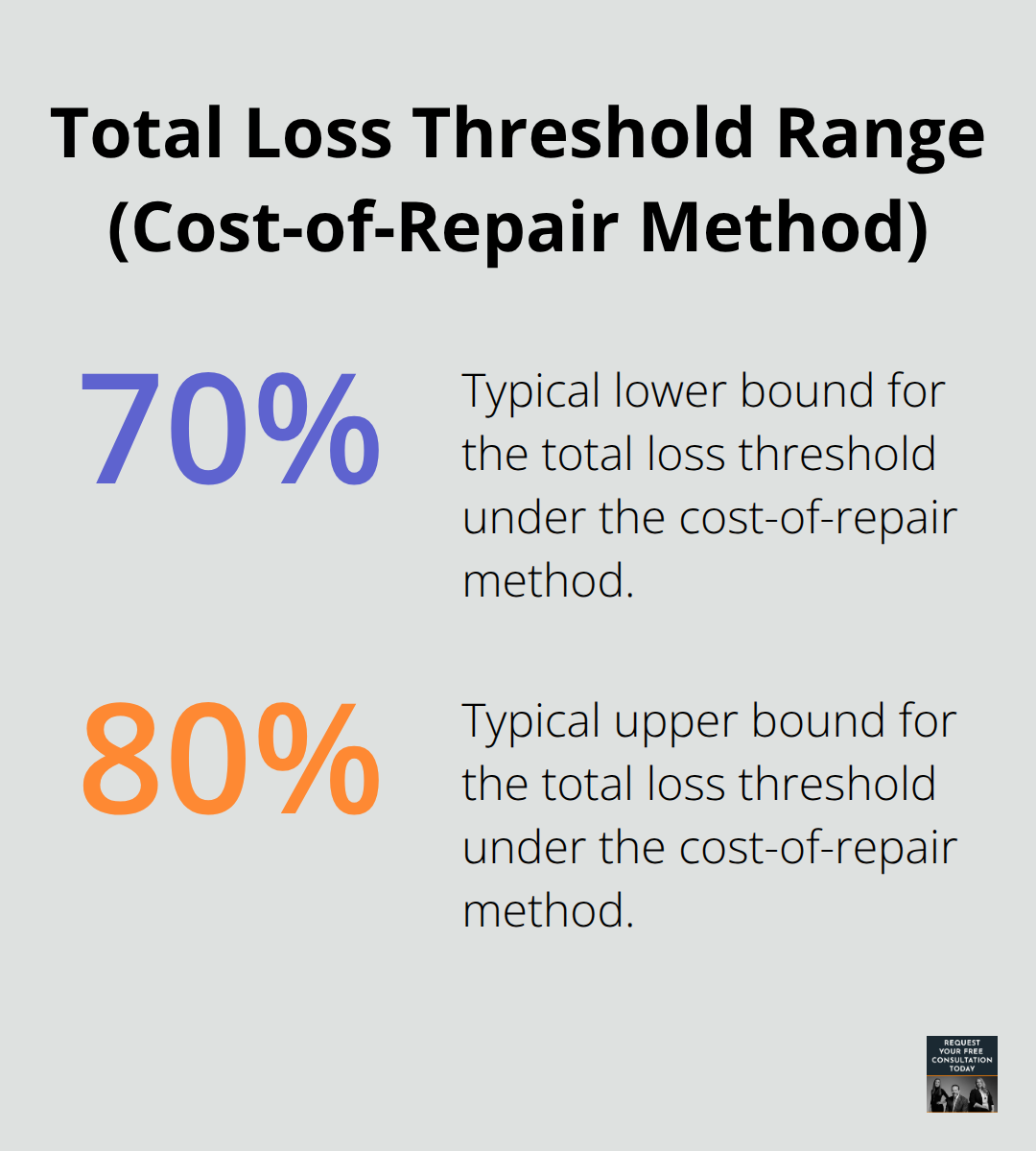

The cost-of-repair method totals all necessary repairs and uses that figure to determine if the vehicle qualifies as a total loss, typically when repair costs exceed 70 to 80 percent of the vehicle’s actual cash value. Automated reports like those from CCC compile data on comparable vehicles nationwide, but they often miss local market conditions specific to Santa Cruz County, Sacramento, or Oakland.

Why Local Market Data Matters More Than National Reports

This is where your involvement becomes essential. Adjusters are trained to minimize payouts, and their initial valuations frequently underestimate what your vehicle is truly worth. The adjuster assigned to your claim will physically inspect the damage, photograph the vehicle, and review repair estimates. However, adjusters work for the insurance company, not for you-they have financial incentives to settle claims quickly and at lower amounts. You should never assume the adjuster’s assessment is accurate or complete. Request a detailed written explanation of how they calculated the actual cash value, including which comparable vehicles they used and what adjustments they made for mileage and condition.

Building Your Documentation Package

Documentation serves as your strongest defense against lowball offers. Gather your vehicle’s maintenance records, service history, and any recent upgrades or repairs you completed before the accident (these items add value that adjusters frequently overlook). Collect photographs of your vehicle before the crash if you have them, along with photos taken immediately after the accident that show the full extent of damage. Obtain at least two independent repair estimates from registered auto body repair shops in your area, as California law gives you the right to choose any repair shop regardless of the insurer’s preferred network.

Creating a Complete Communication Record

Keep copies of the police report, all medical bills if you sustained injuries, and a detailed log of every phone call and email exchange with the insurance company, including dates and names of adjusters you spoke with. If the insurer’s valuation seems incorrect, request an independent appraisal from a certified vehicle appraiser. Services like Appraisal Engine Inc. provide second opinions on total loss valuations and can identify errors in the insurer’s calculations. The cost of an independent appraisal typically ranges from $300 to $500, but this investment often results in settlements thousands of dollars higher than the initial offer.

When you’ve assembled this documentation and understand how adjusters calculate value, you’re ready to move forward with confidence. The next step involves taking action to document and report your damage properly-a process that directly impacts what you ultimately receive.

How to Document Damage After an Accident

Photograph and Film Your Vehicle Immediately

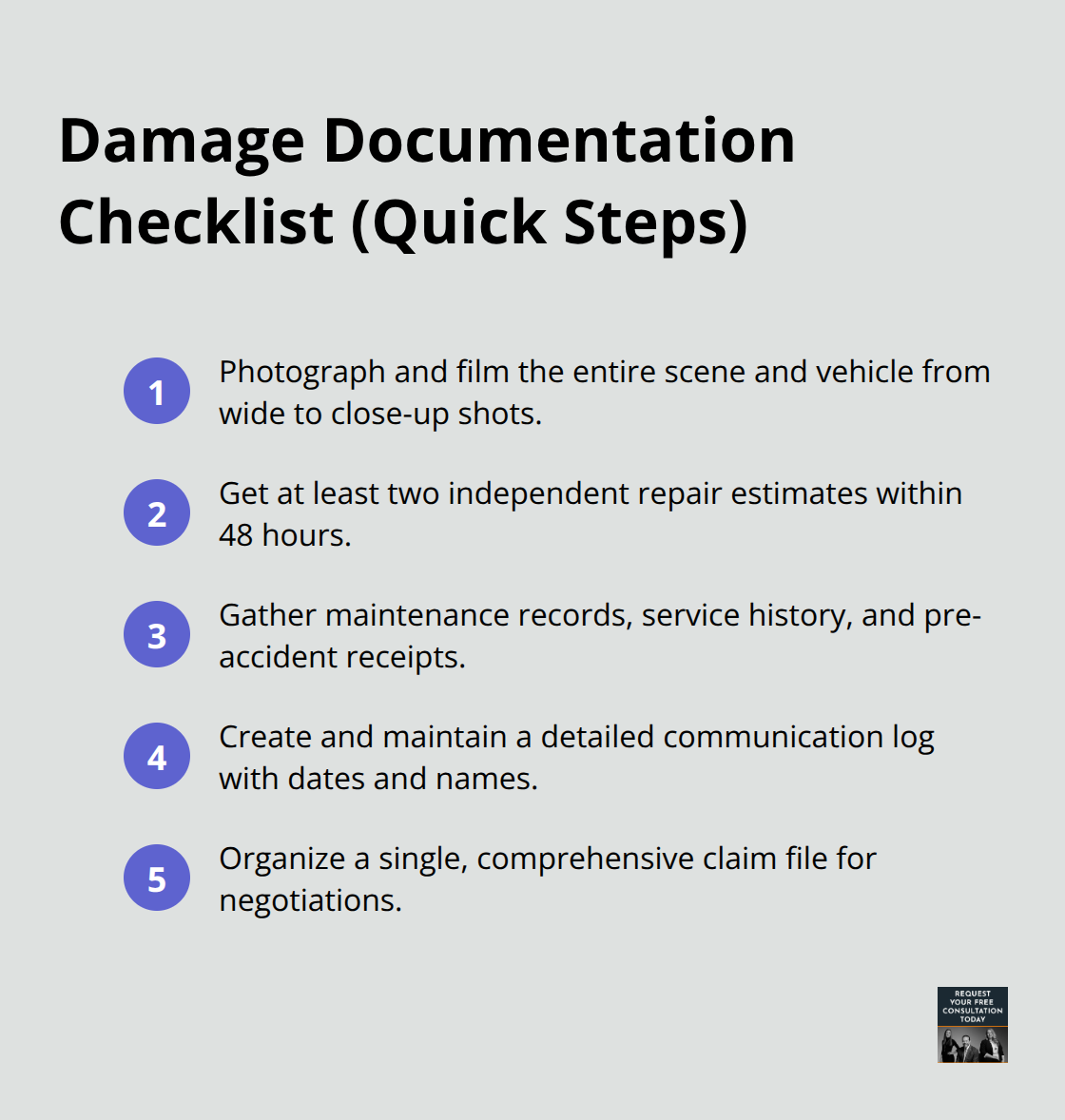

Start photographing and filming immediately after the accident, before you move your vehicle or clean up debris. Take wide shots showing the accident scene, surrounding area, and traffic patterns, then move to medium shots of your vehicle from all angles, and finally close-ups of each damaged section. Include photos of the vehicle’s odometer, dashboard, and interior condition to establish pre-accident state. Shoot video while walking around the entire vehicle, narrating what you see so the timestamp and continuous footage prove you captured the damage in its original state.

Obtain Independent Repair Estimates Within 48 Hours

California law gives you the right to obtain independent repair estimates from registered auto body repair shops, so contact at least two shops within 48 hours of the accident and request written estimates that itemize labor, parts, and specific damage locations. These estimates serve two critical purposes: they provide baseline numbers to compare against the insurer’s valuation, and they demonstrate you took prompt action to minimize loss, which strengthens your credibility with the adjuster.

Do not accept the first estimate as gospel or assume the insurer’s chosen shop will provide the most accurate assessment. Request estimates that specify whether they recommend new original equipment parts, aftermarket parts, or used parts, since this distinction affects repair costs and your vehicle’s post-repair value.

Gather Pre-Accident Documentation

Document your vehicle’s condition before the accident by gathering maintenance records, service history, and receipts for any repairs or upgrades completed in the year before the crash. If you lack pre-accident photos, ask family members or friends if they have any pictures of your vehicle, and compile these into a folder organized by date. This documentation establishes the vehicle’s baseline condition and value before impact.

Create a Detailed Communication Log

Create a communication log starting immediately after the accident and maintain it throughout the claims process. Record the date, time, name of the insurance adjuster or representative, phone number called, and a summary of what was discussed, including any promises made about coverage or timelines. Save every email from the insurance company and take screenshots of text messages if communication occurs through apps. Request written confirmation from the insurer for any verbal statements about your claim, especially regarding repair shop selection, coverage limits, or valuation methodology. The California Department of Insurance requires insurers to act in good faith and thoroughly investigate claims, meaning they must document their reasoning for valuations and settlement offers.

Organize Your Complete Documentation File

Store all documents in one organized location: police report, medical bills if applicable, repair estimates, photographs, maintenance records, communication logs, and any correspondence with the insurance company. If the adjuster’s initial offer arrives without a detailed written explanation of how they calculated actual cash value, immediately request this documentation in writing. This consolidated file becomes your negotiating toolkit when the insurer’s valuation falls short of fair market value for your specific vehicle and condition. With this evidence assembled, you’re positioned to identify and challenge common mistakes that adjusters make-mistakes that frequently result in reduced claim payouts.

Mistakes That Cost You Money in Your Claim

The gap between what insurers initially offer and what your vehicle is actually worth often comes down to three preventable errors that undermine your negotiating position.

Why Accepting the First Offer Destroys Your Leverage

Insurers submit lowball valuations in their opening offers, counting on accident victims to settle quickly without pushback. The California Department of Insurance reports that insurance companies routinely undervalue claims in initial offers, knowing most claimants want the process finished fast. If you accept within days of the accident, you forfeit your right to negotiate, and the difference between that first offer and fair market value can easily reach thousands of dollars. A 2024 Hyundai Tucson with moderate damage and 30,000 miles might receive an initial offer of $400 for diminished value when the actual calculated amount using damage and mileage multipliers reaches $1,000 or higher.

Never respond to an initial valuation offer for at least two weeks. Instead, request a detailed written explanation of how the adjuster calculated actual cash value, which comparable vehicles they used, and what adjustments they applied for mileage and condition. This written documentation forces the insurer to justify their numbers and gives you concrete information to challenge with your own evidence.

How Missing Pre-Accident Documentation Weakens Your Position

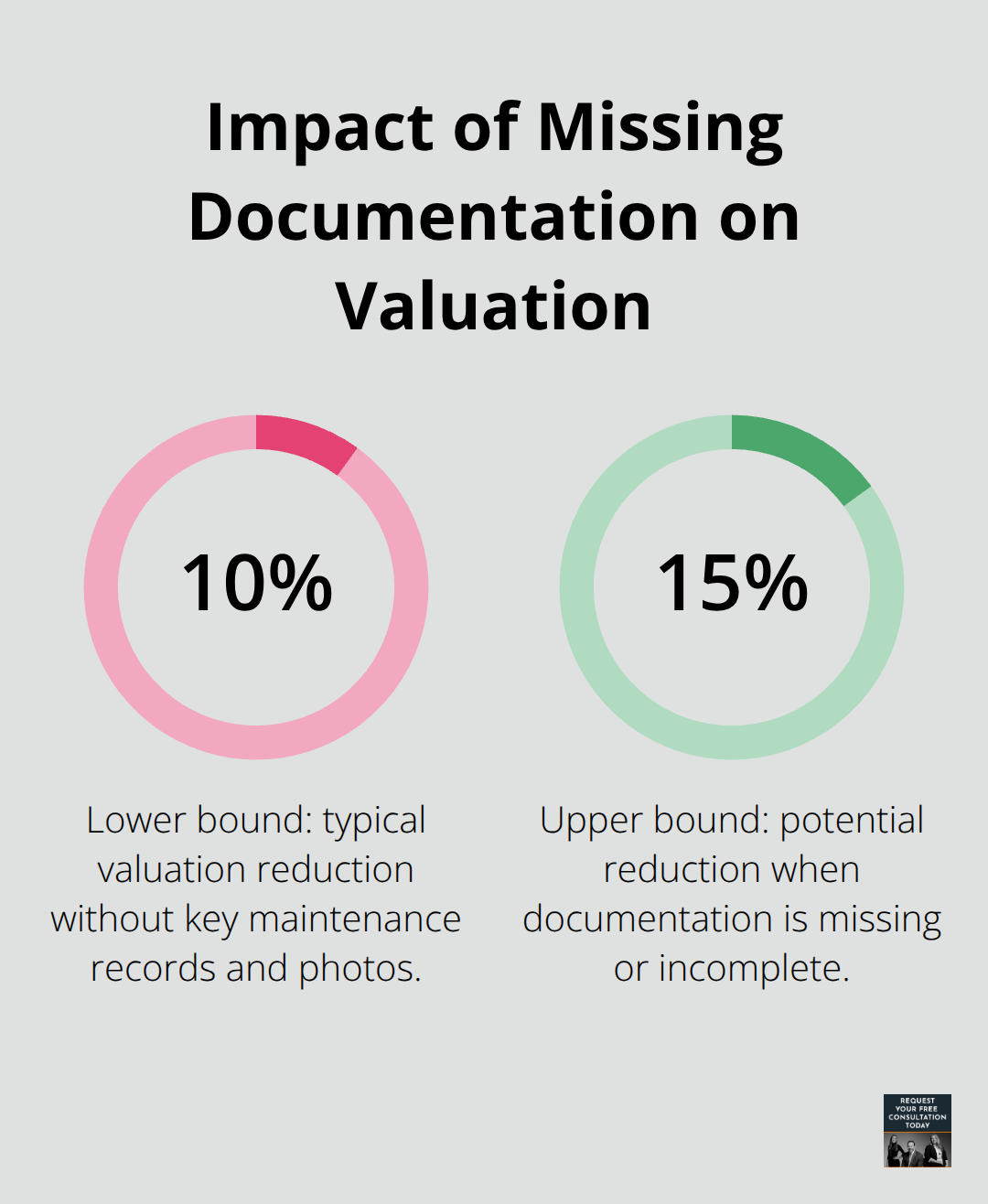

Failing to establish your vehicle’s pre-accident condition creates a documentation vacuum that adjusters fill in their favor. Without maintenance records, service history, or pre-accident photographs, you cannot prove your vehicle was in excellent condition before impact, which means the adjuster can claim it had existing wear or damage that reduces value.

Owners who cannot produce oil change receipts, repair invoices, or pre-accident photos routinely receive 10 to 15 percent lower valuations than those with complete documentation.

This documentation gap becomes especially damaging when negotiating diminished value claims. Adjusters exploit missing records to argue your vehicle’s condition was already compromised, justifying lower payouts across all claim categories.

Why Reporting Delays Undermine Your Credibility

Delaying your damage report costs you negotiating power and raises red flags with adjusters. Report the damage to your insurer within 24 hours of the accident and obtain written confirmation of the report date. Delays suggest you may have caused additional damage or inflated repair costs, which adjusters use as justification for lower payouts. The moment you file, your documentation timeline begins, and this creates a credibility advantage that serves you throughout negotiations.

Gather those independent repair estimates within 48 hours, maintain your communication log, and assemble your complete file before the adjuster’s initial offer arrives. This preparation transforms you from a reactive claimant into an informed participant ready to negotiate from evidence rather than emotion.

Final Thoughts

You now understand how insurance companies value vehicle damage and the specific steps that protect your claim from lowball offers. Never accept an initial valuation without requesting detailed written justification of how the adjuster calculated actual cash value. Assemble your documentation package before negotiations begin, including pre-accident photos, maintenance records, independent repair estimates, and a complete communication log.

Your vehicle’s true value depends on local market conditions in Santa Cruz County, Sacramento, or Oakland, not national automated reports that miss regional factors. When the insurer’s offer falls short of fair market value, you have the right to challenge it with evidence. The cost of an independent appraisal typically ranges from $300 to $500, but settlements often increase by thousands of dollars when you present professional valuations alongside your documentation.

If negotiations stall or the insurer denies your claim without reasonable justification, the team at Schaar & Silva LLP helps people throughout Santa Cruz County, Sacramento, and Oakland navigate property damage claims and ensures you receive fair valuation for your loss. We connect you with medical lien services if you sustained injuries requiring treatment, allowing your medical bills to be paid once your case resolves. Contact us to discuss your vehicle damage valuation guide and claim strategy today.