Car accidents in Santa Cruz County leave victims facing mounting medical bills and lost income while dealing with insurance companies. Understanding the auto accident settlement formula helps you calculate what your case is truly worth.

We at Schaar & Silva LLP see too many accident victims accept lowball offers because they don’t know how to value their damages properly. This guide breaks down each component of settlement calculations so you can protect your financial recovery.

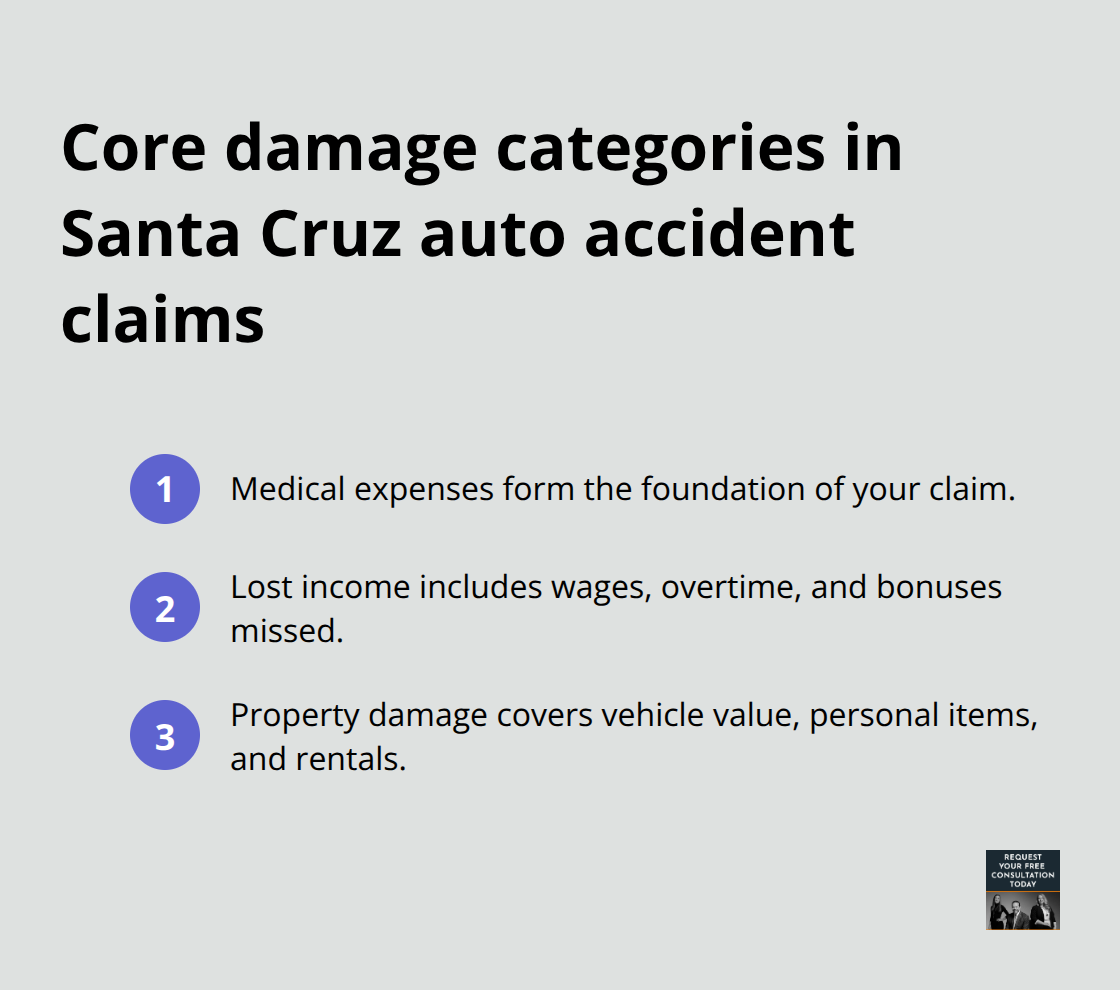

What Damages Can You Actually Claim

Your settlement calculation starts with three concrete damage categories that insurance companies must address. Medical expenses form the foundation of your claim and include every dollar you spend on emergency room visits, diagnostic tests, physical therapy sessions, and prescription medications. In Santa Cruz County, emergency room visits average $3,200 per incident according to California Hospital Association data, while physical therapy sessions typically cost $150 each. Future medical treatment costs require careful documentation from your doctors who must provide detailed prognosis reports and estimated treatment timelines.

Lost Income and Career Impact

Lost wage calculations go beyond your immediate time off work. Document your regular hourly rate or salary, overtime opportunities you missed, and any bonuses or commissions you lost due to your absence. California Labor Commissioner data shows the average Santa Cruz County worker earns $28.50 per hour, which makes even short-term disabilities financially significant. Diminished capacity becomes relevant when injuries affect your ability to perform job duties long-term. Construction workers with back injuries, for example, may need career transitions that result in permanent income reduction. Your employer’s HR department can provide documentation including pay stubs, missed promotion opportunities, and accommodation limitations.

Vehicle and Property Replacement Values

Property damage calculations require current market values, not what you originally paid for your vehicle. Kelly Blue Book and Edmunds provide baseline valuations, but actual cash value includes your vehicle’s specific condition, mileage, and optional equipment. Personal property inside your vehicle (laptops, phones, or tools) also qualifies for compensation. Rental car expenses during repairs add to your property damage claim, with Santa Cruz County rental rates that average $45 daily for economy vehicles.

Independent Appraisals for High-Value Vehicles

Insurance companies often undervalue total loss vehicles, which makes independent appraisals worth the $400-600 cost when your vehicle’s value exceeds $15,000. These professional assessments provide leverage during negotiations and often reveal additional value that adjusters miss. The appraisal process typically takes 2-3 business days and includes detailed condition reports that support your claim.

Once you establish these economic damages, you can move forward to calculate the more complex non-economic damages that often represent the largest portion of your settlement.

How Do You Calculate Non-Economic Damages

Pain and suffering calculations rely on two primary methods that insurance companies accept in settlement negotiations. The multiplier method takes your total economic damages and multiplies them by a factor between 1.5 and 5, based on injury severity and recovery time. California insurance companies typically apply a 2x multiplier for minor injuries like whiplash, then increase to 4x or 5x for permanent disabilities or traumatic brain injuries. The per diem method assigns a daily rate to your pain (often your daily wage as the baseline), then multiplies by recovery days. A Santa Cruz County worker who earns $228 daily would receive that amount for each day of documented pain and suffering.

Factors That Drive Higher Multipliers

Permanent scarring, ongoing physical therapy requirements, and documented psychological trauma push multipliers toward the higher end of the range. Medical records that show chronic pain management, sleep disruption, or inability to participate in previous activities strengthen your case for increased compensation. Age also matters significantly – a 25-year-old with permanent back injuries faces decades of limitations, which justifies higher multipliers than similar injuries in a 65-year-old.

Insurance companies reduce multipliers when gaps exist in medical treatment, when you return to work quickly, or when pre-existing conditions complicate your injury claims. Clear medical documentation that connects your symptoms directly to the accident prevents these reductions.

Documentation That Maximizes Pain Awards

Pain journals that track daily symptoms, medication usage, and activity limitations provide concrete evidence for your suffering calculations. Physical therapy notes, prescription records, and specialist referrals create the medical foundation that supports higher settlement amounts. Photography of visible injuries, especially during the acute phase, adds visual proof that adjusters cannot dismiss easily.

Common Calculation Errors That Cost You Money

Many accident victims underestimate their pain and suffering damages because they focus only on current symptoms. Future pain considerations become vital when doctors predict ongoing complications or the need for additional surgeries. Insurance adjusters often exploit this gap by offering settlements before victims understand their long-term prognosis.

The calculation process requires careful attention to avoid mistakes that reduce your final settlement amount.

What Settlement Mistakes Cost You Money

Insurance companies profit when accident victims make calculation errors, and these costly mistakes appear repeatedly in Santa Cruz County cases. The biggest error involves acceptance of initial settlement offers within the first few weeks after an accident, often before victims understand their full injury scope. State Farm and Allstate typically present offers that fall 40-60% below fair settlement values, and they count on victims who make predictable errors that slash settlement values by 30-60%. These quick offers deliberately exclude future medical costs, treatment requirements, and long-term complications that may not surface for months.

Poor Documentation Destroys Settlement Value

Incomplete expense records kill settlement negotiations before they start. Every medical co-pay, prescription cost, transportation expense to appointments, and missed work hour must have documentation. California Department of Insurance data shows that claims with poor documentation receive settlements that average 35% lower than fully documented cases. Accident victims who fail to photograph their injuries immediately, skip follow-up appointments, or lose receipts hand insurance companies ammunition to reduce offers. Physical therapy sessions that cost $150 each in Santa Cruz County add up quickly, but lost receipts give adjusters reason to question your entire treatment plan. The gap between documented expenses and actual expenses often exceeds $5,000 in moderate injury cases.

Quick Settlement Acceptance Before Full Recovery

The most expensive mistake involves settlement before doctors can predict future complications or additional surgeries. Whiplash injuries that seem minor initially can develop into chronic pain that requires years of treatment, while concussions may cause cognitive issues that affect income capacity permanently. Medical research shows that 40% of accident victims experience symptom progression within six months of their initial injury.

Settlement for $15,000 when future medical costs will exceed $50,000 creates financial disasters that legal action cannot fix once settlement agreements are signed.

Failure to Account for Lost Future Income

Many victims calculate only immediate lost wages and ignore long-term income reduction from permanent disabilities. A construction worker with back injuries may need career transition that results in $20,000 annual income loss for decades. Insurance adjusters rarely volunteer information about diminished capacity claims (which can exceed $500,000 in severe cases), and they pressure victims to focus only on current medical bills and short-term wage loss.

Final Thoughts

Your auto accident settlement formula calculation provides the foundation for fair compensation, but you need strategic timing and professional guidance to maximize your settlement. Start by gathering complete documentation of all expenses, medical records, and income loss before you engage with insurance companies. Calculate your economic damages first, then apply appropriate multipliers for pain and suffering based on injury severity and recovery timeline.

Professional legal guidance becomes necessary when injuries involve permanent disabilities, disputed liability, or settlement offers below 70% of your calculated value. Insurance companies employ teams of adjusters and attorneys to minimize payouts, which makes legal representation valuable for cases that exceed $25,000 in damages. We at Schaar & Silva LLP help Santa Cruz County accident victims navigate complex settlement negotiations while we provide medical bill assistance and property damage claim support.

After you calculate your potential settlement, document any new symptoms or complications that develop and maintain consistent medical treatment. Avoid settlement agreements until you reach maximum medical improvement (the point where doctors expect no further recovery). Contact our legal team to review your calculation and protect your financial recovery from insurance company tactics that reduce your compensation.