After a car accident in Santa Cruz County, insurance settlement negotiations can feel overwhelming. Insurance companies often start with offers far below what your claim is actually worth, and they count on you not pushing back.

We at Schaar & Silva LLP have seen how quickly people accept these low initial offers out of stress or confusion. This guide walks you through the tactics insurers use, the strategies that actually work, and the red flags you need to recognize.

How Insurance Companies Calculate Your Settlement

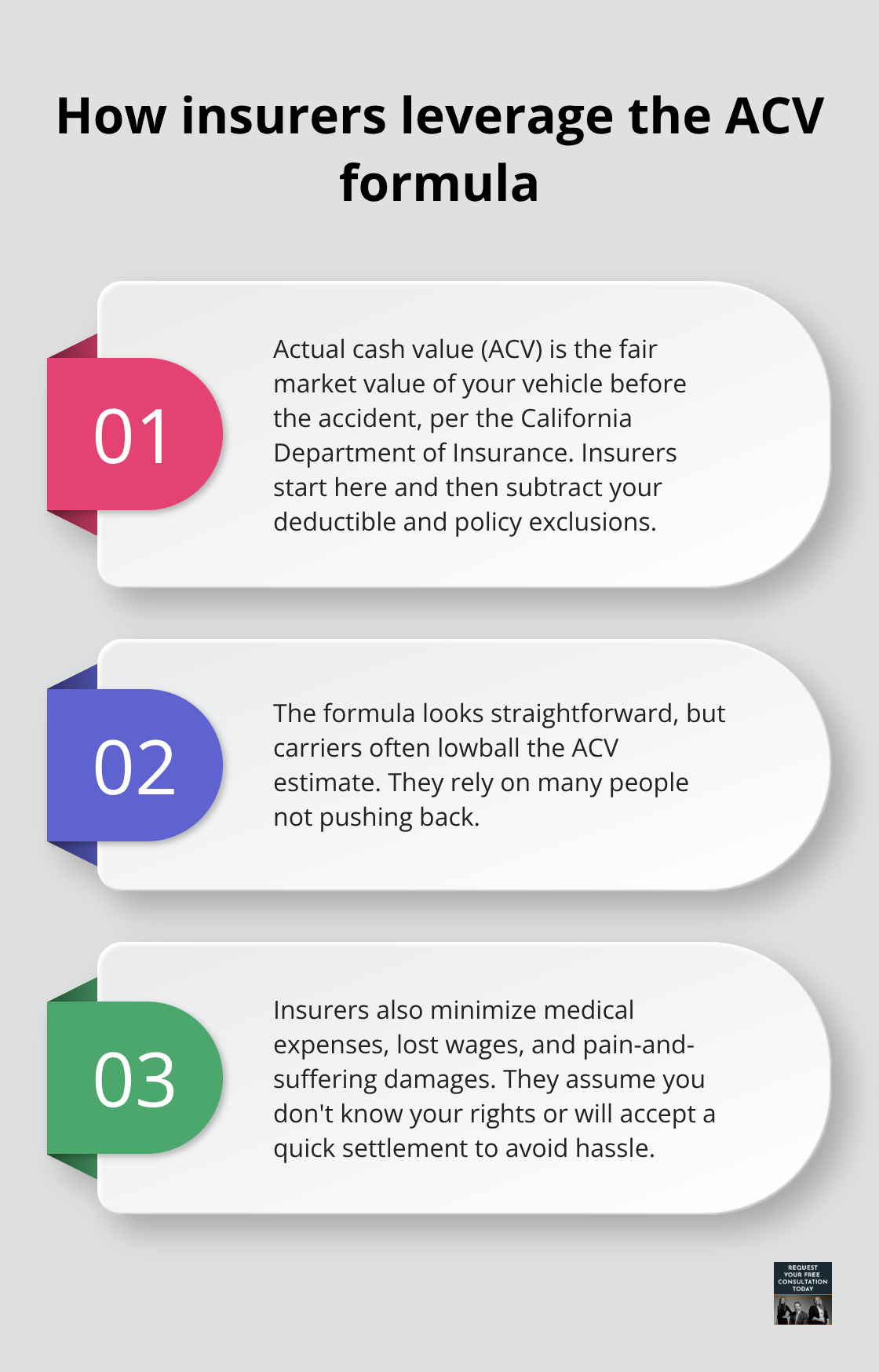

The ACV Formula and How Insurers Exploit It

Insurance companies start with your vehicle’s actual cash value, or ACV, which the California Department of Insurance defines as the fair market value of your vehicle before the accident. They subtract your deductible and any exclusions listed in your policy. The formula appears straightforward, but insurers deliberately lowball the ACV estimate, knowing most people won’t push back. They also minimize medical expenses, lost wages, and pain-and-suffering damages because they assume you either don’t know your rights or will accept a quick settlement to avoid hassle.

Location Matters More Than Insurers Admit

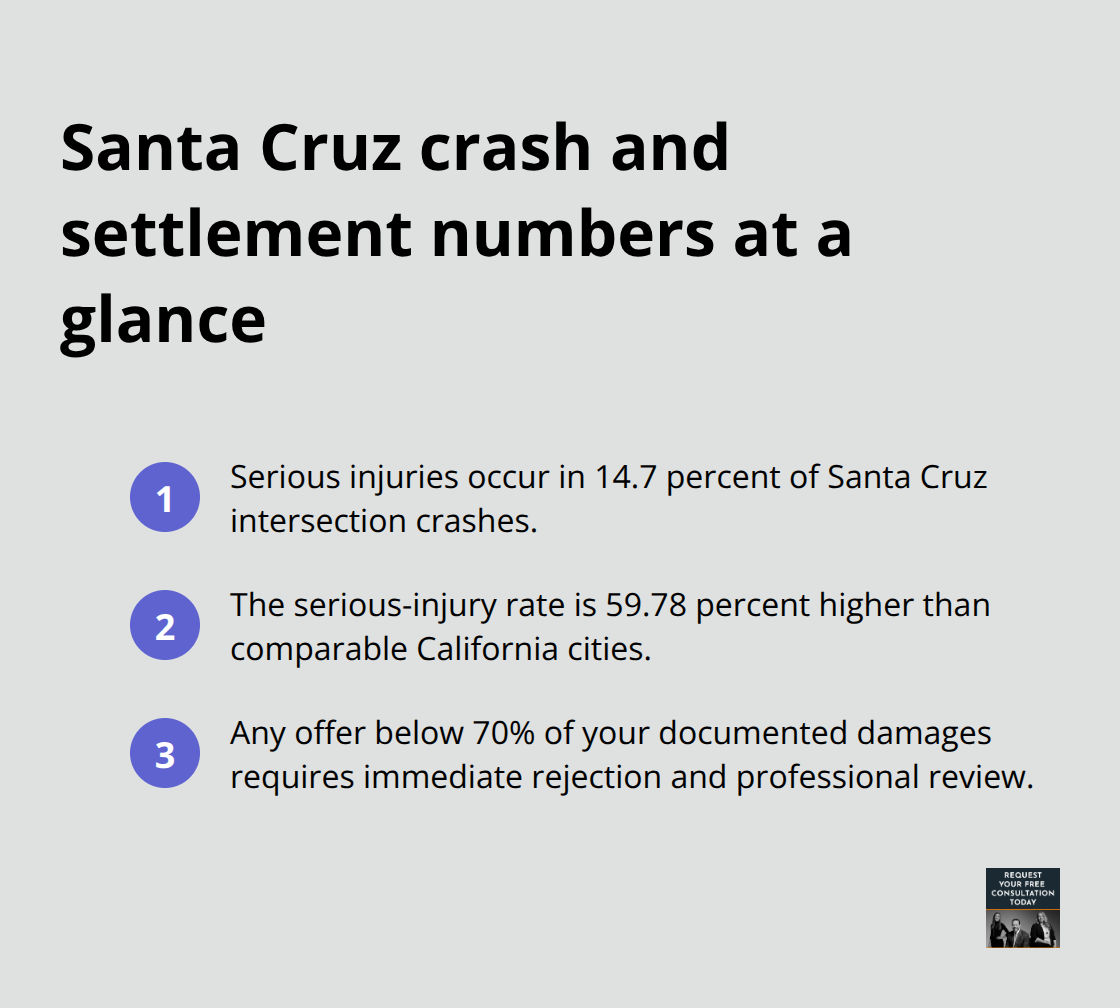

At intersections like Highway 1 and Highway 9 in Santa Cruz, where 11 crashes occurred between 2020 and 2024, or Pacific Avenue and Beach Street with 8 crashes in that same period, serious injuries happen far more often than state averages. The Statewide Integrated Traffic Records System data shows Santa Cruz intersection crashes result in serious injuries 59.78 percent more often than comparable California cities. Yet insurers often treat injury claims from these high-risk areas the same way they treat minor fender-benders. They count on you not having documentation that proves your damages are severe.

Why Initial Offers Function as Tests, Not Starting Points

Your initial settlement offer isn’t a starting point for negotiation-it’s a test. Insurers deliberately start low because they know roughly half of claimants accept without question. The California Department of Insurance requires insurers to acknowledge your claim within 15 days and respond within 15 days, but meeting those deadlines doesn’t mean you’ve received fair compensation. A decision within 40 days after you submit proof of loss is also required, yet this timeline protects the insurer’s schedule, not your payout.

Building Documentation That Changes the Adjuster’s Mind

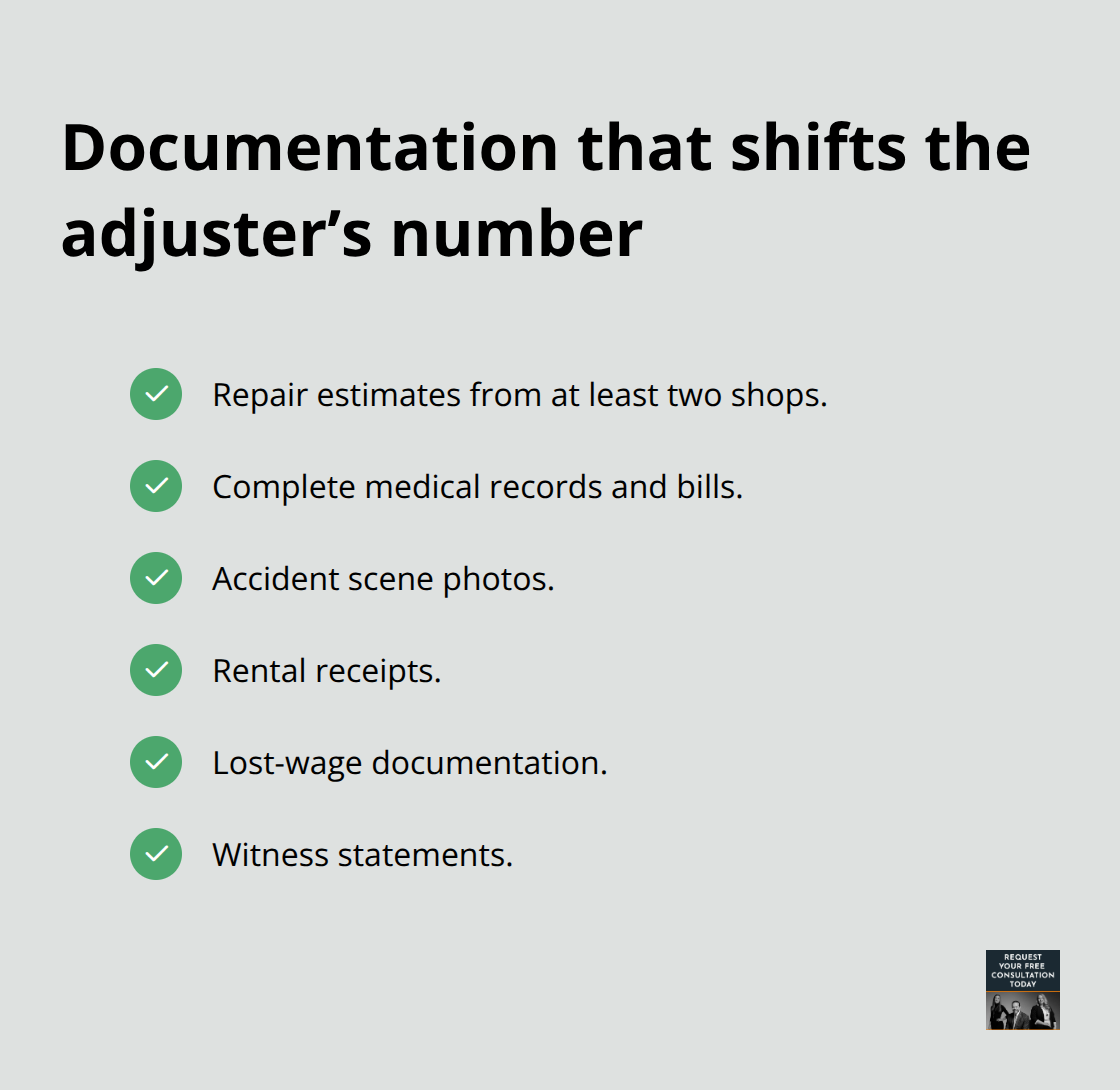

The insurer’s adjuster has already decided what they’re willing to pay before they contact you. Your job is to change that number by building an airtight case with repair estimates from at least two shops, complete medical records and bills, photos from the accident scene, rental receipts, lost-wage documentation, and witness statements. If your accident happened at one of Santa Cruz’s most dangerous intersections, use that location data to argue why your injuries and damages exceed the insurer’s initial offer.

The concentration of crashes and serious injuries at these specific locations strengthens your position and justifies higher settlement demands backed by official data.

Understanding how insurers calculate settlements reveals their strategy-but recognizing their tactics is only half the battle. The real power comes from what you do next.

What Documentation Actually Wins Negotiations

Gather Repair Estimates That Challenge Lowball Offers

Build your file the moment you reject the insurer’s initial offer. Obtain repair estimates from at least two independent shops, not the insurer’s preferred vendors, because competition between shops produces realistic pricing that challenges inflated ACV calculations. Request itemized invoices that identify whether parts are original equipment manufacturer (OEM), aftermarket, or reconditioned-the California Department of Insurance requires this distinction, and insurers often use cheap aftermarket parts to suppress settlement amounts. When the adjuster claims repair costs are excessive, your second estimate serves as proof of market rate and forces them to justify their position.

Medical Records and Lost Wages Create Undeniable Proof

Collect every medical bill, treatment record, and receipt tied to your accident without delay. Obtain a letter from your employer documenting missed work days and lost wages, then attach recent pay stubs that confirm your income level. Medical expenses and lost income carry equal weight to vehicle damage in settlement calculations, yet many claimants overlook this documentation. Photos from the accident scene, damage progression, and your injuries create visual proof that undermines the adjuster’s attempt to minimize harm.

Location Data Transforms Routine Claims Into High-Value Cases

If your crash occurred at Highway 1 and Highway 9, Pacific Avenue and Beach Street, or another of Santa Cruz’s ten most dangerous intersections, pull the official crash data from the Statewide Integrated Traffic Records System showing injury severity rates 59.78 percent higher than state averages. This transforms your claim from a routine settlement into a location-specific injury case that justifies substantially higher compensation. The concentration of crashes and serious injuries at these specific locations strengthens your position and backs your settlement demands with official data.

Counter-Offers Require Written Communication and Formal Pressure

Rejection and counter-offers require written communication, never phone calls. Send your counter-offer via certified mail or email with all supporting documentation attached, then cite specific policy language explaining why the insurer’s number falls short. State your counter-amount clearly without vague language. Submit your counter-offer before the insurer’s 40-day decision window closes, because missing that deadline removes pressure and gives them reason to delay further.

The Appraisal Process Signals You Will Not Capitulate

If medical damages remain disputed, request the appraisal process your policy likely includes, where each side selects an appraiser and a neutral umpire makes a binding decision if they agree. This formal step signals you will not accept their valuation and often prompts the insurer to settle rather than spend appraiser fees. Having an attorney communicate on your behalf shifts the dynamic immediately and prevents misstatements that undermine your case. Insurers count on claimants negotiating alone without representation, so this change in approach carries significant weight in settlement discussions.

Red Flags in Settlement Negotiations

Artificial Deadlines and Manufactured Urgency

Insurers know that stressed claimants make poor decisions, so they manufacture artificial urgency to push you into accepting inadequate settlements. The California Department of Insurance requires insurers to respond within 15 days of your claim and make a decision within 40 days after you submit proof of loss, but insurers weaponize these timelines by implying your claim will be denied if you miss informal deadlines they invent. They call repeatedly, mention that other claimants have already settled, or suggest that your case will be closed if you don’t sign within days. Watch for offers that lack supporting calculations or arrive with unrealistic deadlines-none of these pressures are legally binding. You control the timeline once you reject their initial offer and submit a counter-offer with documentation.

Selective Medical Records and Injury Minimization

Insurers minimize your injuries by requesting medical records selectively, focusing only on initial treatment while ignoring ongoing therapy, medication adjustments, or specialist visits that prove your damages extend beyond what their adjuster assumed. If your accident happened at Santa Cruz’s Highway 1 and Highway 9 intersection, where 11 crashes occurred between 2020 and 2024, or at Pacific Avenue and Beach Street with 8 crashes in that period, the injury severity data from the Statewide Integrated Traffic Records System contradicts any attempt to downplay your condition. Serious injuries occur in 14.7 percent of Santa Cruz intersection crashes, 59.78 percent higher than comparable California cities. Use this data directly when an adjuster claims your injuries seem minor or unrelated to the crash.

Pressure to Sign Away Your Rights

Insurers push claimants to sign settlement agreements that waive future claims, release subrogation rights, or surrender the ability to pursue additional damages before you fully understand the long-term costs of your injuries. Any offer below 70% of your documented damages requires immediate rejection and professional review. Never sign anything without reviewing your complete medical file and understanding what rights you’re surrendering. The moment an adjuster pressures you to sign quickly, that pressure itself signals the settlement is undervalued.

Regaining Control Through Written Communication

Written rejection via certified mail or email, paired with your counter-offer and supporting documentation, shifts control back to you and removes the urgency insurers artificially create. If pressure intensifies or deadlines feel coercive, legal representation becomes necessary to protect your position and prevent you from surrendering rights worth far more than the settlement they’re pushing.

Final Thoughts

Insurance settlement negotiations in Santa Cruz demand confidence backed by solid documentation and a willingness to reject inadequate offers. Your initial offer functions as a test, not a starting point, and you control the outcome by submitting written counter-offers with repair estimates, medical records, lost-wage documentation, and accident scene photos attached. If your crash occurred at one of Santa Cruz’s ten most dangerous intersections, the official data showing 59.78 percent higher injury rates than state averages transforms your claim into a location-specific case that justifies substantially higher compensation.

Legal representation becomes necessary when the insurer’s offer falls below 70 percent of your documented damages, when pressure to sign intensifies, or when medical expenses and lost wages remain disputed after your counter-offer. An attorney communicating on your behalf immediately shifts the dynamic and prevents misstatements that undermine your position. The moment an adjuster resists your documentation or claims your injuries seem unrelated to the crash, that resistance signals the settlement is undervalued and professional intervention is warranted.

We at Schaar & Silva LLP understand the stress that follows a car accident in Santa Cruz County and help you navigate insurance settlement Santa Cruz negotiations with confidence. Contact us to discuss your case and move forward with legal knowledge and dedicated client service backing your recovery.