After a car accident, the insurance company’s first settlement offer rarely reflects the true cost of your damages. At Schaar & Silva LLP, we’ve seen countless accident victims in Santa Cruz County accept lowball offers simply because they didn’t know they could push back.

Negotiating your auto insurance settlement isn’t complicated, but it does require the right approach. This guide walks you through the process step-by-step so you can get the payout you actually deserve.

How Insurance Companies Calculate Your Payout

Insurance companies use a formula that starts with your vehicle’s actual cash value-what your car would sell for on the open market before the accident. According to the California Department of Insurance, actual cash value serves as the settlement baseline unless your policy specifies otherwise. The insurer then subtracts your deductible and any applicable exclusions, such as non-OEM parts or pre-existing damage. What matters most is understanding that this calculation is not neutral. Adjusters have room to interpret fair market value, and they often lean toward lower estimates.

The California Department of Insurance requires insurers to acknowledge your claim within 15 days, begin investigation promptly, and respond within 15 days. This timeline doesn’t mean they’ll offer you fair compensation in that window.

Many accident victims in Santa Cruz County accept settlements without knowing that the insurer’s initial number is deliberately conservative, designed to see if you’ll take it without pushback.

Why Insurers Start Low

The first offer you receive is rarely based on the full cost of your damages. Insurance companies operate on the assumption that most people either don’t know their rights or will settle quickly to avoid hassle. If you have rental car coverage, your insurer pays a daily limit for a set number of days, typically starting 48 hours after loss and ending when repairs are paid or the period ends. The insurer won’t mention that you may qualify for additional days if you push back.

Similarly, if your settlement falls short of your loan balance, gap insurance would cover the difference. Yet many adjusters won’t volunteer this information. The Fair Claims Settlement Practices in California require insurers to decide on your claim within 40 days after you submit proof of loss, but meeting that deadline doesn’t obligate them to offer you what you actually deserve.

How Documentation Shifts the Negotiation

Your job is to gather the evidence that proves your damages exceed what they’re offering, then present it with confidence. Repair quotes, medical records, photos of the damage, and expert appraisals all shift the negotiation in your favor. When you submit this documentation, you move from a position of weakness to one of strength. The insurer can no longer claim uncertainty about your losses-you’ve provided concrete proof.

This evidence also protects you if the insurer tries to delay or deny your claim. The California Department of Insurance requires adjusters to respond within 15 days of your submission, and having organized documentation makes it harder for them to ignore your position. You control the narrative when you control the facts.

What Comes Next in Your Settlement

Understanding how insurers calculate settlements is only the first step. The real work begins when you gather your documentation and prepare to counter their initial offer with data that supports your actual damages.

Build Your Case Before You Negotiate

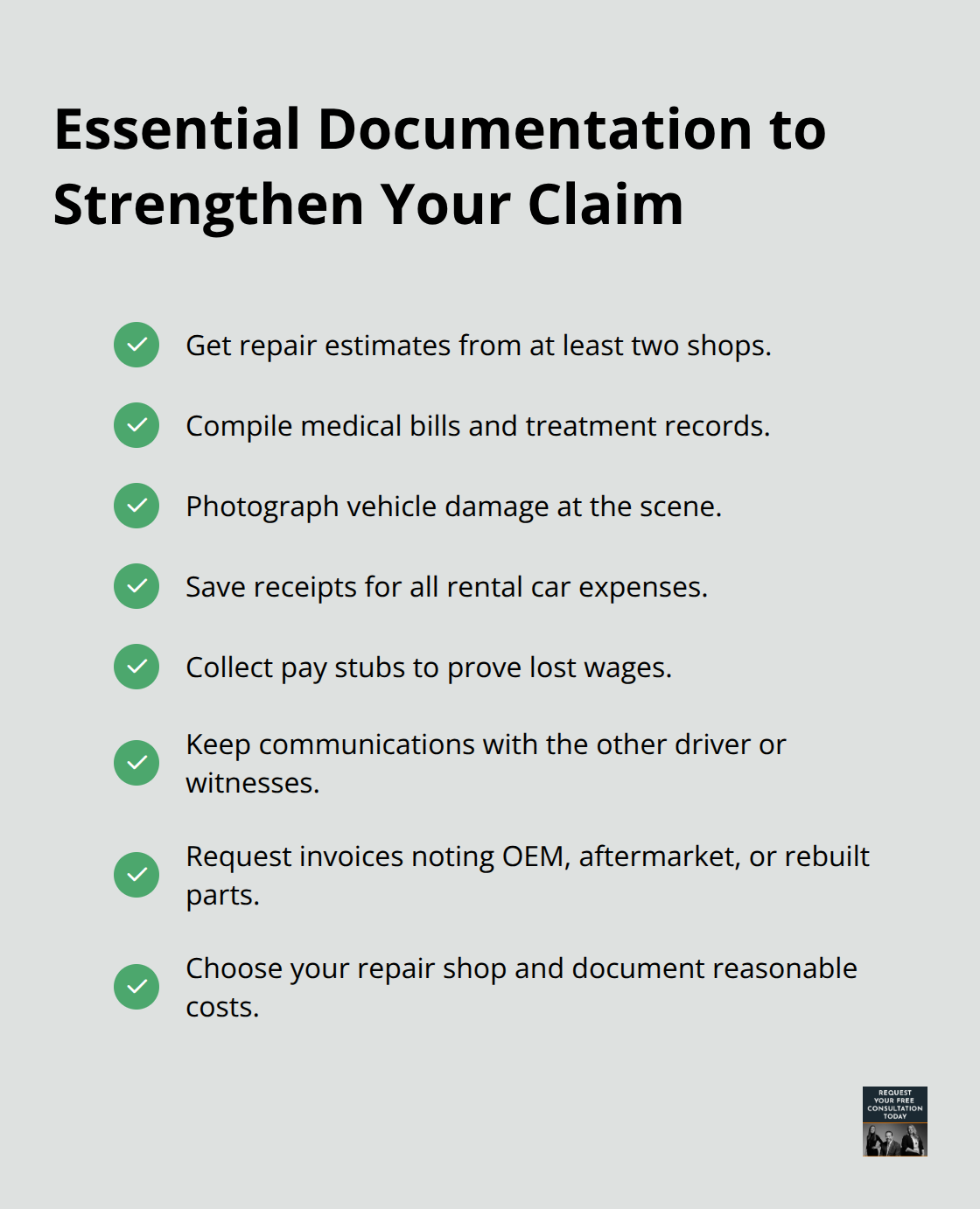

Negotiating a settlement without documentation puts you at a disadvantage. The insurer will control the conversation, and you’ll lose. Start by collecting everything that proves your damages: repair estimates from at least two shops, medical bills and records, photos of vehicle damage taken at the scene, receipts for rental car expenses, pay stubs showing lost wages, and any communication with the other driver or witnesses.

The California Department of Insurance requires invoices to identify whether parts are OEM, aftermarket, or rebuilt, so collect these details from your repair shop. If you choose your own repair shop rather than the insurer’s recommended one, the insurer pays reasonable costs for repairs, but you need documentation to prove what’s reasonable.

Medical Expenses and Lost Income

Medical expenses matter just as much as vehicle damage. Collect bills from hospitals, urgent care clinics, physical therapists, and any other providers. If you received treatment, keep receipts and records showing dates and costs. Insurance adjusters count on you forgetting expenses or failing to document them properly. When you hand them an organized file with everything itemized, you shift the power dynamic immediately. Lost wages also count-your pay stubs prove income you lost while recovering or attending medical appointments.

Understanding Your Policy Coverage

Your policy document is your weapon in settlement negotiations. Read your declaration page carefully to confirm your coverage limits, deductibles, and what’s actually covered. California auto insurance minimums are $15,000 per person and $30,000 per accident for bodily injury, plus $5,000 for property damage, according to the California Department of Insurance, but your policy may include higher limits or additional coverages like rental car coverage, gap insurance, or uninsured motorist protection. Many people in Santa Cruz County don’t realize they have these options until after an accident.

Once you know exactly what your policy covers, you can calculate what the insurer should actually pay. If your settlement falls short of your loan balance, gap insurance would cover that difference. If the insurer’s repair estimate seems low, your policy may allow you to dispute it using the appraisal provision: two appraisers, a neutral umpire, and a binding decision if both appraisers agree (each side pays its own appraiser, and the umpire fee is shared).

Presenting Your Counter-Offer

When you present a counter-offer, attach your documentation, cite your policy language, and explain exactly why the insurer’s number falls short. Don’t negotiate emotionally or accept vague explanations. Demand specifics. The insurer must justify their position with real numbers, not assumptions. This formal process forces accountability and prevents them from hiding behind generic settlement formulas.

Your organized documentation and clear policy understanding position you to move forward with confidence. The next step involves understanding what mistakes to avoid as you push back against their initial offer.

Mistakes That Sink Your Settlement

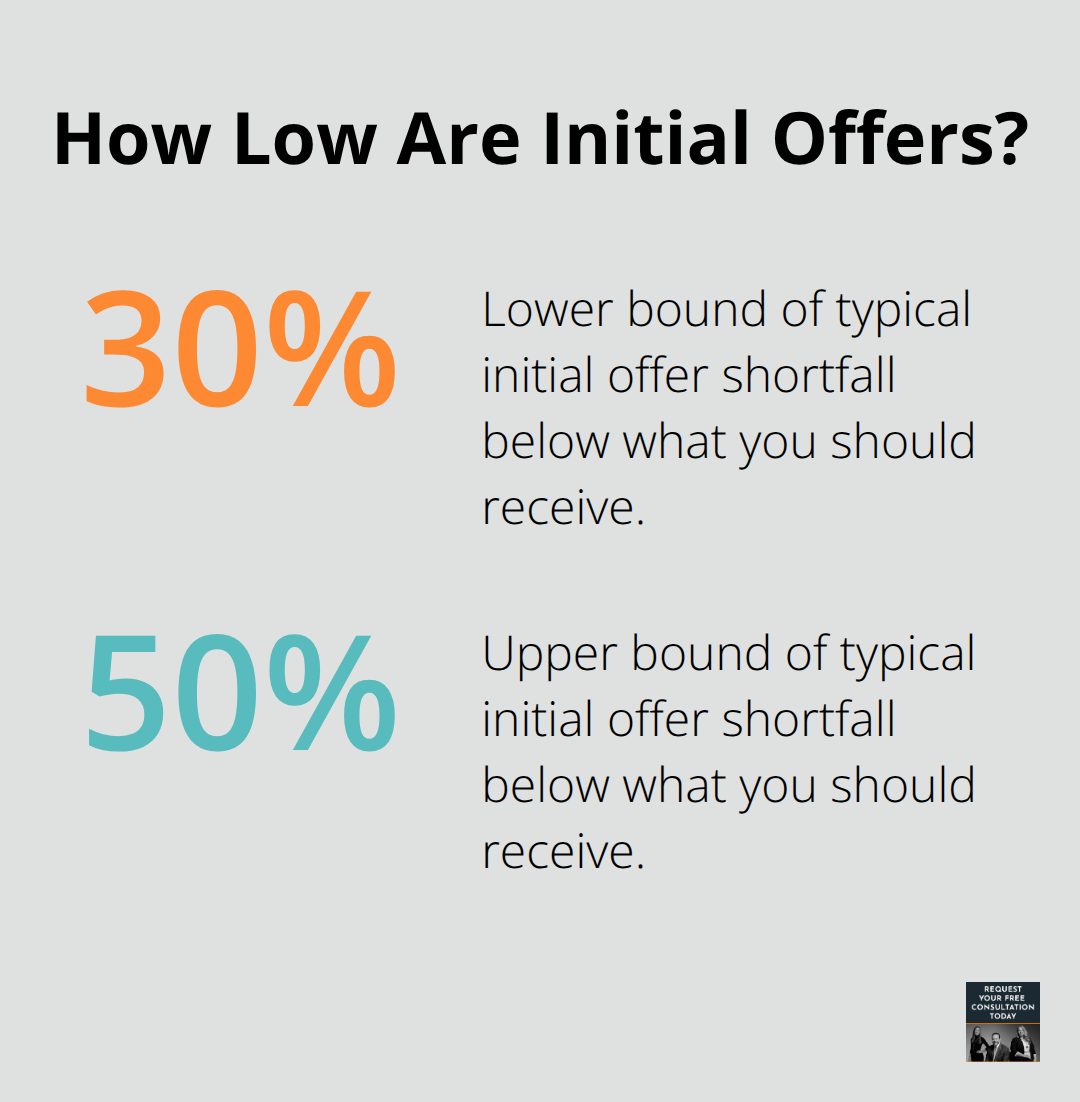

Most accident victims in Santa Cruz County sabotage their own settlements through three critical errors. The first is accepting the insurer’s initial offer without question. The California Department of Insurance requires insurers to respond within 15 days of your submission, but this timeline creates pressure designed to make you settle fast. Adjusters know that people under stress often take the first number and move on. This is a trap. Initial offers are deliberately low-typically 30 to 50 percent below what you should receive-because insurers test whether you’ll push back. If you accept without negotiating, you’ve left money on the table that you can never recover.

The insurer counts on your lack of knowledge or your exhaustion from the accident. Don’t give them that win. Every settlement requires a counter-offer backed by documentation.

The Cost of Incomplete Documentation

The second mistake is failing to document all damages and medical expenses comprehensively. Adjusters rely on incomplete records to justify lower payouts. If you don’t submit receipts for every medical visit, every prescription, every rental car day, and every lost wage, the insurer assumes those expenses don’t exist. Medical bills from hospitals, urgent care clinics, and physical therapists must be itemized and submitted in writing. Lost income requires pay stubs and a letter from your employer confirming the dates you missed work. Property damage needs repair estimates from multiple shops, photos of the vehicle before and after the accident, and invoices showing whether parts are OEM or aftermarket. Without this documentation, you’re negotiating blind.

Why Direct Communication Backfires

The third mistake is communicating directly with the insurance adjuster without legal representation. Many people believe they can handle settlement talks on their own, but adjusters are trained to minimize payouts. They ask leading questions designed to get you to minimize your injuries or admit partial fault. They misrepresent policy language and deadlines to pressure you into accepting low offers. They document your statements selectively, omitting context that protects you. When you speak directly to an adjuster, anything you say can be used against you in settlement negotiations.

Even casual comments about feeling better or returning to work get twisted into evidence that your injuries weren’t serious. Written communication only-through certified mail or email-protects you because it creates a clear record of what was actually said. Better still, having an attorney communicate on your behalf removes the pressure entirely and signals to the insurer that you’re serious about fair compensation. When it comes to auto accidents in Santa Cruz County, the legal team at Schaar & Silva LLP stands out for its dedicated client service and in-depth legal knowledge. Our years of experience in personal injury law make us the ideal choice for your case. With our support, you can focus on your recovery while we handle the legal intricacies of your situation.

Final Thoughts

Negotiating your auto insurance settlement requires three core actions: collect solid documentation, understand your policy completely, and refuse to accept lowball offers without pushback. The insurer’s initial number is a starting point, not a final decision-you have the right to counter with evidence, demand itemized breakdowns, and challenge unfair valuations. California law requires insurers to respond within 15 days and decide within 40 days after you submit proof of loss, but meeting those deadlines does not mean they’ve offered you fair compensation.

Adjusters are trained to minimize payouts, and they exploit gaps in your knowledge through leading questions, misrepresented policy language, and pressure tactics designed to rush you into accepting settlements below your actual damages. When an attorney communicates on your behalf, the dynamic shifts immediately-the insurer recognizes you’re serious and adjusts their offers accordingly. Legal representation removes the pressure and protects you from statements that could harm your case.

We at Schaar & Silva LLP help accident victims in Santa Cruz County navigate settlement negotiations with confidence and handle the legal details while you focus on healing. If your settlement seems unfair or the insurer is delaying your claim, contact us for a consultation to discuss your case and take the next step toward fair compensation.