After a car accident in California, insurance companies often lowball damage valuations. We at Schaar & Silva LLP have seen countless claims where drivers accepted initial offers that fell far short of actual repair costs.

Vehicle damage valuation in California depends on how insurers calculate your payout and what documentation you provide. Understanding these methods helps you fight back against unfair settlements.

How Insurance Companies Value Your Damaged Vehicle

California insurers rely on Actual Cash Value (ACV) to determine payouts on physical damage claims, which means you receive the lesser of repair costs or your vehicle’s fair market value according to the California Department of Insurance. This is where most drivers run into trouble-insurers use automated valuation tools that frequently miss California-specific market conditions, local pricing variations, and the unique characteristics of your vehicle. The ACV represents what a knowledgeable buyer and seller would agree on, but those valuations often undervalue your car by applying excessive depreciation adjustments, selecting comparable vehicles with higher mileage or worse condition, or ignoring recent upgrades and maintenance work you completed. Silicon Valley luxury cars and Central Valley work trucks operate in completely different markets, yet many insurers apply a one-size-fits-all approach that doesn’t reflect regional demand or pricing. Your documentation becomes critical here-repair shops, dealers, and independent appraisers in your area can provide evidence that contradicts the insurer’s automated estimate. Don’t accept the initial valuation without pushing back; the California Appraisal Clause gives you the right to hire an independent appraiser when you dispute the insurer’s ACV, which often uncovers thousands of dollars in additional settlement value that the insurer’s system overlooked.

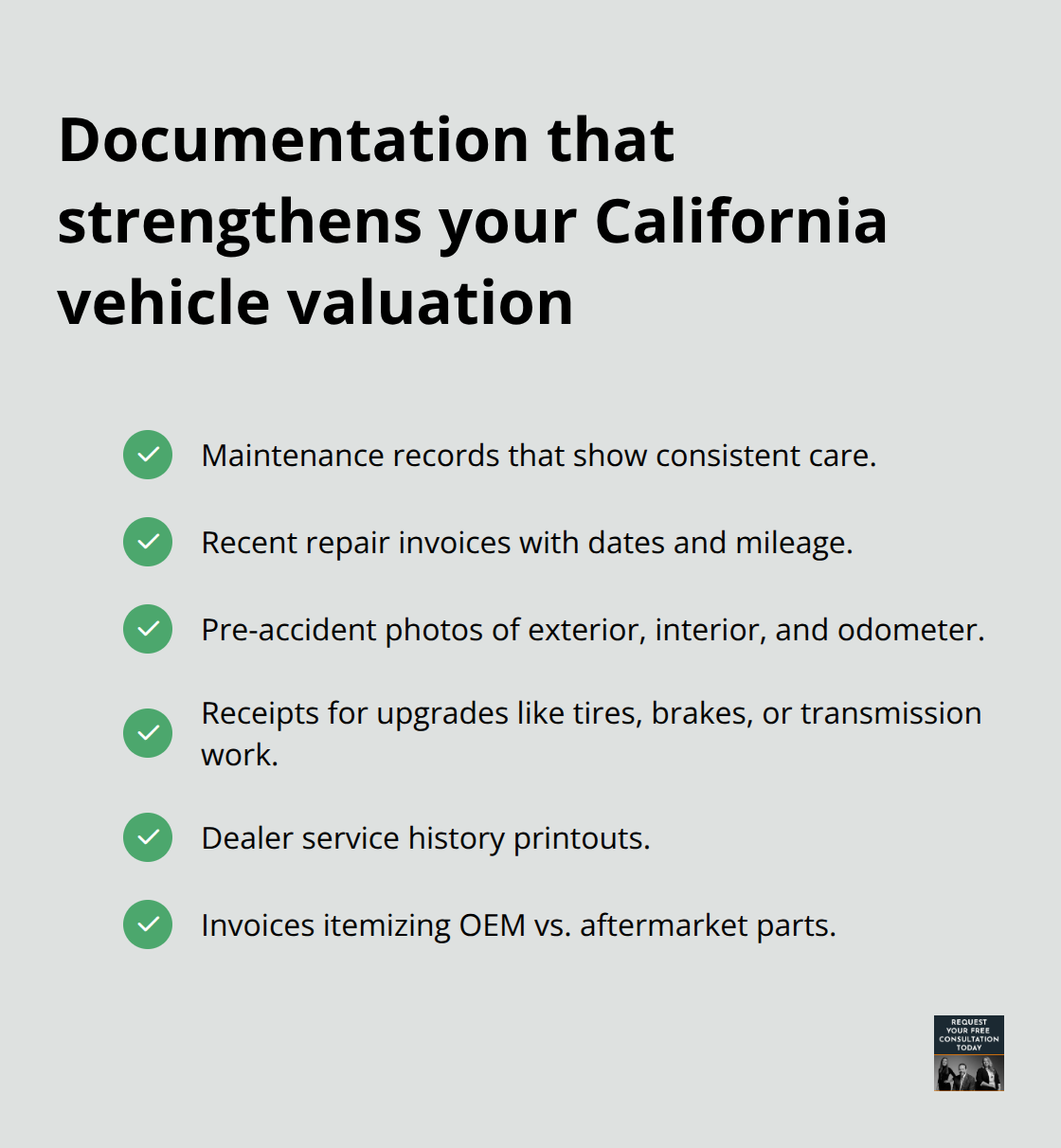

What Documentation Actually Matters

Collect your vehicle’s maintenance records, recent repair invoices, photos from before the accident, and any dealer service history that demonstrates pre-accident condition. Upgrade documentation proves especially valuable-new tires, recent brake work, or a newer transmission directly impact fair market value but are frequently ignored by automated systems. Pre-accident photos showing your vehicle’s actual condition, mileage, and any wear patterns help counter inflated condition adjustments that insurers sometimes apply. When repairs begin, request that the body shop itemize whether replacement parts are original equipment manufacturer (OEM) or aftermarket; California law requires this distinction on invoices, and OEM parts typically support higher valuations than aftermarket alternatives.

Why Independent Appraisals Win Negotiations

An independent appraisal analyzes California sales data, dealer inventories, and your vehicle’s specific pre-accident condition rather than relying on generic market reports. Professional appraisers document local pricing nuances that automated tools miss and calculate accurate valuations before you sign anything or cash any settlement check. Request a second opinion on the insurer’s total loss offer before accepting; this step alone frequently generates substantially higher payouts because it forces insurers to justify their valuation against documented market evidence. The appraisal process (which typically involves comparing recent sale prices of similar vehicles with and without accident history) provides the strongest foundation for negotiating a fair settlement.

Moving Forward with Your Claim

Once you have solid documentation and an independent appraisal in hand, you’re positioned to challenge the insurer’s initial offer with concrete evidence. The next section covers the common mistakes that reduce payouts and how to avoid them-mistakes that often stem from accepting valuations without proper support or failing to understand your policy’s coverage limits.

Why Your First Settlement Offer Falls Short

Insurers count on drivers accepting initial damage valuations without question, and this mistake costs accident victims thousands of dollars annually. The California Department of Insurance reports that claims typically settle within 40 days after proof of loss is provided, but this timeline pressures you into quick decisions before you’ve gathered proper evidence. Accepting the first offer without independent verification means you forfeit your right to challenge the valuation later, and most insurers structure their opening bids 20 to 40 percent below what fair market data actually supports. Your vehicle’s true value requires local market analysis that accounts for California’s regional pricing variations, your car’s maintenance history, and recent upgrades-not an automated system that generates a number in days. Once you cash that settlement check, the claim closes and you cannot return asking for more money if repair costs exceed the payout or if you discover the valuation missed critical details about your vehicle’s condition.

What Happens When Documentation Is Incomplete

Repair shops and body shops handle hundreds of claims annually and follow standard procedures that don’t always capture information relevant to your damage valuation. When the body shop completes repairs, you receive an invoice showing labor and parts, but this document alone rarely proves what your vehicle’s pre-accident value actually was. Insurers exploit this gap by claiming they cannot verify your car’s condition before the crash, which gives them justification to apply conservative depreciation adjustments and condition deductions that lower your payout. Missing documentation about recent maintenance work, upgrade installations, or dealer service records means the insurer’s valuation tool defaults to assuming average wear and average condition, even if your vehicle was meticulously maintained. Photographs taken immediately after the accident and before repairs begin serve as critical evidence that disputes the insurer’s damage assessment, yet most drivers never take these photos because they’re focused on safety and shock rather than claim preparation. Without pre-accident photos, repair invoices showing part types, maintenance records demonstrating care, and dealer service history, you’re arguing against the insurer’s automated estimate using only your word.

Why Independent Appraisals Force Fair Settlements

An independent appraiser hired directly by you or obtained through the California Appraisal Clause creates a second valuation that the insurer cannot ignore during settlement negotiations. The appraiser analyzes comparable vehicle sales in your specific region, examines your vehicle’s actual condition based on photographs and inspection, and documents how recent repairs or upgrades impact fair market value. This report provides concrete evidence that contradicts the insurer’s estimate, and when two valuations disagree significantly, the appraisal process requires both parties to select an umpire whose decision becomes binding on the ACV dispute. Drivers who skip this step and negotiate directly with the insurer’s adjuster are essentially arguing against a computer algorithm using only conversation and hope. Professional appraisals typically cost between $300 and $600, but they frequently recover $2,000 to $5,000 or more in additional settlement funds because they force the insurer to justify why their automated valuation should prevail over documented market evidence. The appraisal becomes your leverage point in negotiations because it shifts the burden of proof onto the insurer to explain why comparable vehicles in your market sold for higher prices than their estimate suggests your car was worth.

How to Collect Evidence Before Accepting Any Offer

Collect your vehicle’s maintenance records, recent repair invoices, photos from before the accident, and any dealer service history that demonstrates pre-accident condition. Upgrade documentation proves especially valuable-new tires, recent brake work, or a newer transmission directly impact fair market value but are frequently ignored by automated systems. Pre-accident photos showing your vehicle’s actual condition, mileage, and any wear patterns help counter inflated condition adjustments that insurers sometimes apply. When repairs begin, request that the body shop itemize whether replacement parts are original equipment manufacturer (OEM) or aftermarket; California law requires this distinction on invoices, and OEM parts typically support higher valuations than aftermarket alternatives. Don’t sign or cash any settlement check until you review the insurer’s valuation for accuracy; settling early makes disputes harder to pursue later.

Moving Forward with Your Claim

Once you have solid documentation and an independent appraisal in hand, you’re positioned to challenge the insurer’s initial offer with concrete evidence. The next section covers the common mistakes that reduce payouts and how to avoid them-mistakes that often stem from accepting valuations without proper support or failing to understand your policy’s coverage limits.

Maximizing Your Vehicle Damage Claim

Request Multiple Repair Estimates

Multiple repair estimates reveal significant differences that a single insurer-preferred shop cannot show. Request at least two additional estimates from independent body shops in your area-shops that have no financial relationship with the insurance company. These estimates often differ substantially because repair shops assess damage differently, price labor at different rates, and may recommend OEM parts where the insurer’s shop defaults to aftermarket alternatives. A shop in Oakland may charge $85 per hour for labor while a Santa Cruz shop charges $65, and both are legitimate market rates. The key is ensuring each estimate includes the same scope of work: identical parts (OEM vs. aftermarket specified), same labor hours, and comparable paint quality standards. When your estimates show higher repair costs than the insurer’s initial valuation, you have concrete evidence that their ACV calculation undervalues your vehicle. California law requires insurers to pay reasonable costs per trade standards, and if your chosen shop’s estimate exceeds theirs, the insurer must justify why their figure is more accurate.

Work with Independent Claims Adjusters

Claims adjusters employed by insurance companies work for the insurer, not for you, despite what their friendly demeanor might suggest. Their job is to minimize payouts, and they’re trained to use settlement psychology to close claims quickly. Hire an independent claims adjuster who works on your behalf-these professionals typically charge between $400 and $800 but recover far more than their fee through detailed damage assessment and negotiation leverage. An independent adjuster will attend the insurer’s inspection, document discrepancies in their damage evaluation, and identify coverage issues that benefit your claim. They understand California’s Fair Claims Settlement Practices Regulations, which require insurers to respond to claims within 15 days and settle within 40 days after proof of loss-timelines that pressure you into accepting inadequate offers.

Understand Your Policy Coverage Limits

Your policy coverage limits determine the maximum payout available, but many drivers never review their declarations page to understand what they actually purchased. If you carry $250,000 in bodily injury coverage but only $50,000 in property damage coverage, your vehicle’s valuation is capped at $50,000 regardless of its actual value. Review your policy now before filing a claim, and if coverage seems insufficient, contact your agent about increasing limits-especially critical if you financed or leased your vehicle, since lenders often require higher coverage. The insurer will not voluntarily point out if their initial offer exceeds your policy limits; they’ll simply cap the payout and move forward. Sacramento and Oakland drivers should verify their coverage aligns with local vehicle values, as regional market differences can significantly impact whether your limits adequately protect your assets.

Final Thoughts

Vehicle damage valuation in California demands that you challenge the insurer’s initial offer with concrete evidence rather than accept their first number. Documentation, independent appraisals, and multiple repair estimates create the leverage you need to recover thousands of dollars that insurers would otherwise withhold from your settlement. The California Appraisal Clause protects your right to dispute valuations, and using this tool consistently produces higher payouts than negotiating alone.

When injuries accompany property damage, your situation requires legal guidance beyond valuation alone. Medical expenses, lost wages, and pain and suffering claims demand attention that extends past damage assessment, and an attorney protects your rights while you focus on recovery. We at Schaar & Silva LLP help accident victims throughout Santa Cruz County, Sacramento, and Oakland navigate property damage claims and injury recovery while ensuring you receive fair compensation for all losses.

After settlement closes, monitor your vehicle’s performance and document any issues that stem from the accident. Keep records of all correspondence, estimates, and appraisals for your files, and if you accepted a diminished value settlement, maintain documentation showing the accident history for future resale purposes. The accident itself is behind you, but your active participation in the recovery process determines whether you receive the full compensation you deserve.