A car accident in California can leave you facing medical bills, lost wages, and property damage that far exceed what insurance will cover. Most drivers carry only the state’s minimum coverage limits, which often aren’t enough to fully compensate accident victims.

At Schaar & Silva LLP, we help people in Santa Cruz County, Sacramento, and Oakland understand how California car accident limits work and what options exist to recover the full amount they’re owed. This guide walks you through the coverage limits, the gaps they create, and proven strategies to maximize your recovery.

What Are California’s Minimum Insurance Limits?

State-Mandated Coverage and the 2025 Changes

California requires every driver to carry a minimum of $30,000 in bodily injury coverage per person and $60,000 per accident, plus $15,000 for property damage. These limits took effect on January 1, 2025, when California SB 1107 raised the previous minimums. The state set these amounts as the bare floor for legal driving, not adequate protection. If a driver hits you while carrying only these minimums, you’ll quickly discover how inadequate they are.

Why Medical Costs Outpace Coverage

A single hospitalization from a moderate car accident costs $50,000 to $150,000, which immediately exhausts the bodily injury limit. Property damage coverage at $15,000 barely covers repair costs for a newer vehicle. When a victim’s medical bills alone reach $80,000 but the at-fault driver’s policy maxes out at $60,000 total, the victim absorbs the remaining $20,000 out of pocket unless other recovery sources exist.

The Gap Between Minimums and Reality

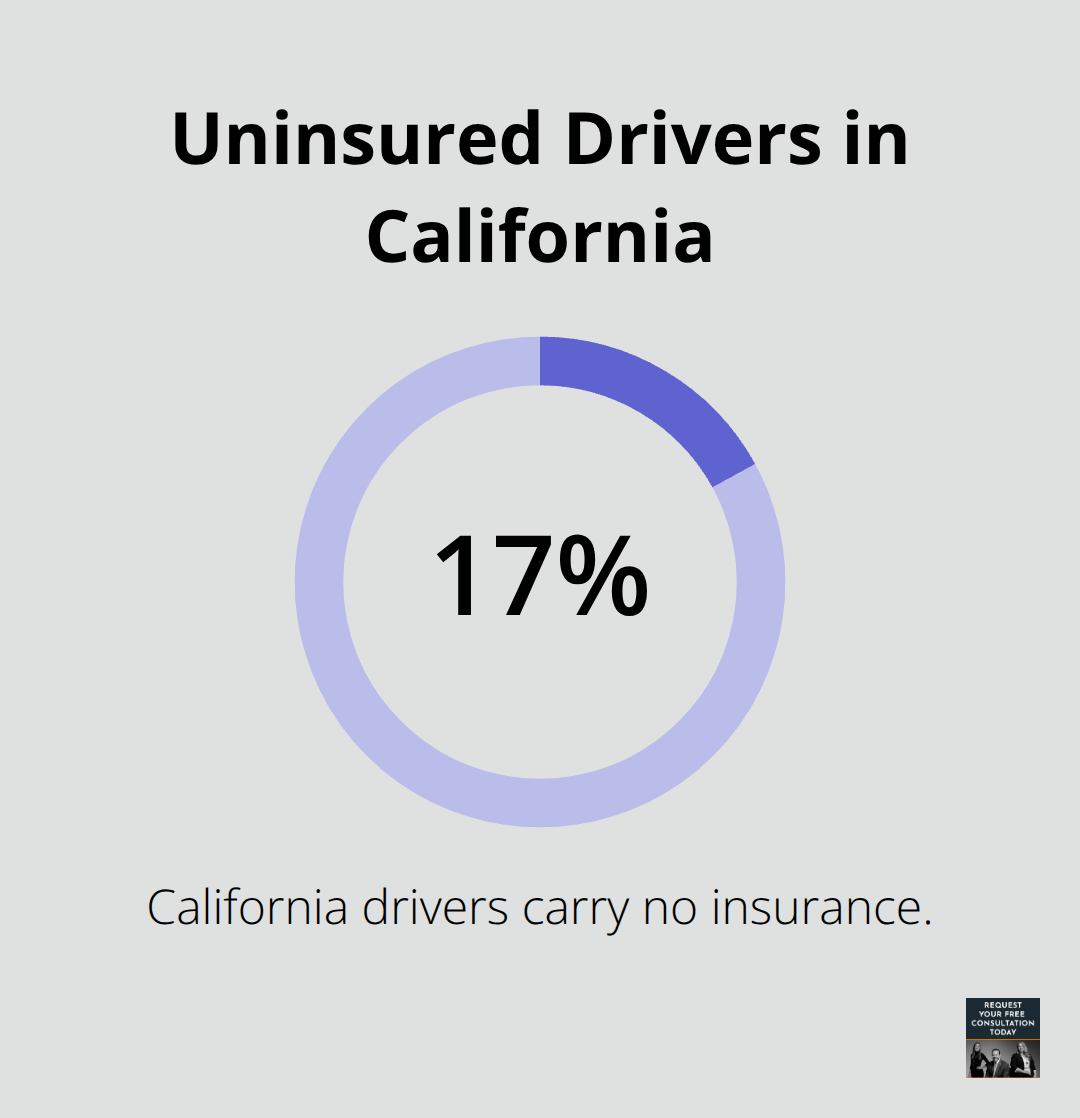

The real problem isn’t that California’s minimums are low-it’s that most drivers never upgrade beyond them. About 16.6% of California drivers carry no insurance at all, and those who do carry insurance typically stick with state minimums to keep premiums down. This creates a mismatch between what accidents actually cost and what insurance will pay.

A broken bone with surgery runs $100,000 to $500,000 in total medical expenses and lost wages. Soft tissue injuries from whiplash settle in the $15,000 to $75,000 range once pain and suffering are factored in. Traumatic brain injuries routinely exceed $250,000 in total value. If the at-fault driver carries only the $30,000 per-person minimum, you’re left fighting for recovery through underinsured motorist coverage on your own policy, claims against the driver’s personal assets, or identification of other liable parties.

Multiple Paths to Recovery

Your own insurance choices and understanding California’s fault-based system become critical to your outcome. This is where the next section-how accident limits affect your compensation-shows you the specific strategies that can bridge the gap between what you’re owed and what the at-fault driver’s policy will cover.

How Insurance Limits Leave You Short

When the at-fault driver’s bodily injury limit sits at $30,000 per person and your medical bills hit $80,000, that $50,000 gap doesn’t disappear-it becomes your problem. California’s minimum coverage limits create a direct shortfall between what accidents actually cost and what insurance will pay. A moderate car accident with hospitalization, surgery, and ongoing physical therapy easily reaches $100,000 to $150,000 in economic damages alone. Add pain and suffering, lost wages, and reduced earning capacity, and the total value climbs to $200,000 or more. The at-fault driver’s $60,000 per-accident limit covers only a fraction of this amount. State minimums were designed for the insurance company’s benefit, not yours.

Your Own Insurance Becomes Your Safety Net

Underinsured motorist coverage on your own policy exists specifically to bridge this gap. If you carry UIM coverage and the at-fault driver’s limits run out, your UIM kicks in to cover the difference up to your policy limit. For example, if your total damages reach $200,000 and the at-fault driver carries only $60,000 in bodily injury coverage, your UIM coverage can pay up to your limit-potentially $100,000 or $250,000 depending on what you selected. Most drivers never add UIM or carry minimal amounts to save on premiums, which significantly limits recovery options. California law requires insurers to offer UIM, but you must request it and pay for it. Carrying UIM limits that match or exceed your bodily injury limits protects you when the at-fault driver’s policy falls short.

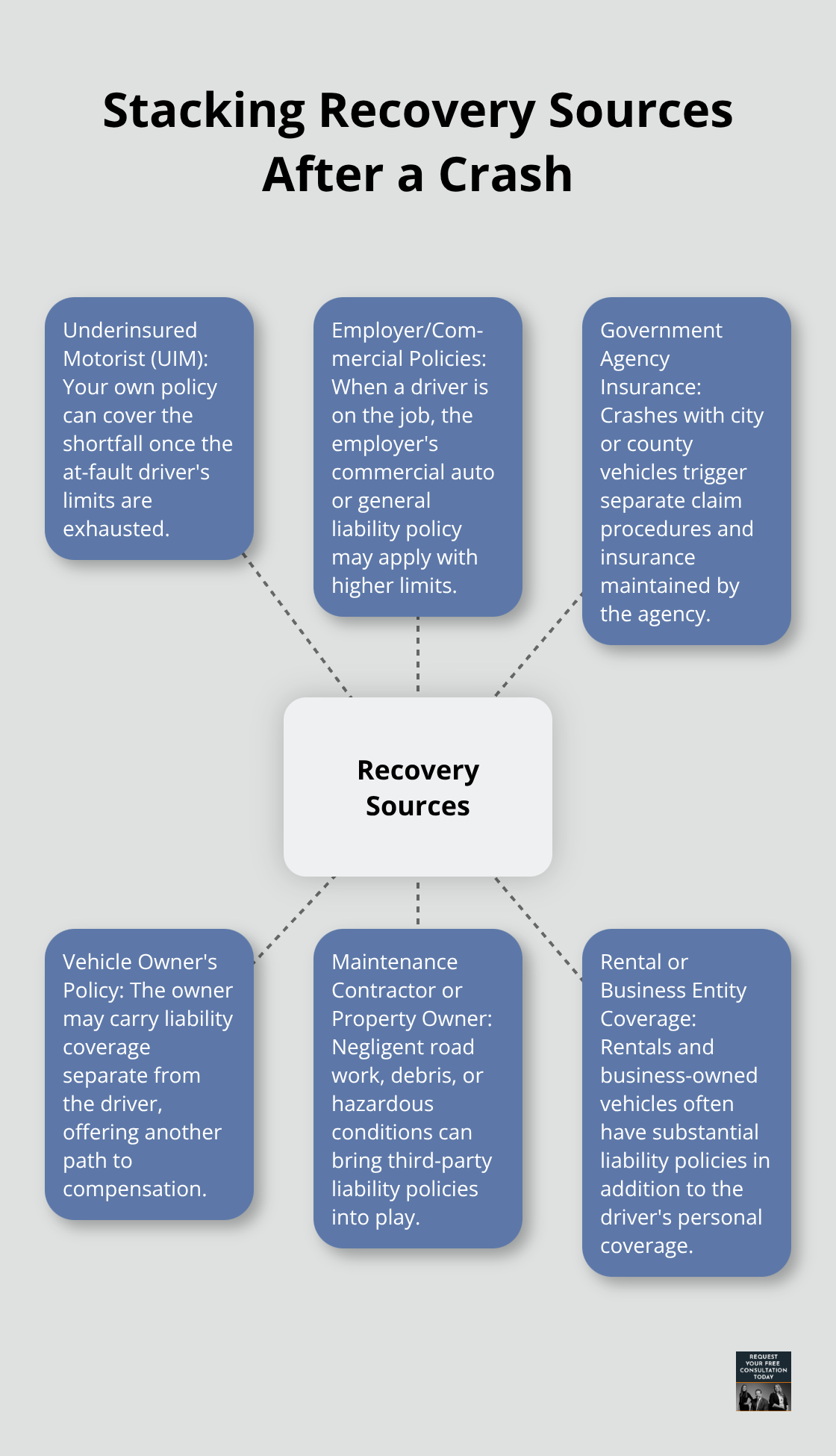

Finding Recovery Beyond the At-Fault Driver’s Policy

When one insurance policy isn’t enough, multiple liable parties and stacked coverage become your lifeline. If a business vehicle, government vehicle, or contractor caused your accident, their employer’s liability insurance may carry higher limits than the driver’s personal auto policy. A delivery driver working for a major retailer involved in your crash might trigger both the driver’s personal auto policy and the retailer’s commercial liability coverage. These policies can stack, meaning you recover from one, then pursue the other for remaining damages. Government vehicles operated by city or county agencies follow different rules and timelines, but they carry their own insurance.

Identifying every potentially liable party-including the vehicle owner, employer, maintenance contractor, or property owner if road conditions contributed to the crash-expands your recovery sources dramatically.

Strategies to Identify All Available Coverage

The path to full recovery requires systematic investigation of every possible insurance source. Start with the at-fault driver’s policy limits and coverage type. Then identify whether the vehicle belonged to an employer, rental company, or business entity. Check whether any government agency operated the vehicle or maintained the road where the accident occurred. Property owners, maintenance contractors, and other third parties may carry liability insurance that applies to your case. Each additional policy represents another potential source of compensation (up to your actual damages). Missing even one available policy means leaving money on the table that rightfully belongs to you.

Moving Forward With Your Recovery

Understanding where compensation can come from transforms your approach to settlement negotiations and claims. The next section covers specific strategies to maximize your recovery by identifying all available insurance policies and pursuing claims methodically rather than accepting the at-fault driver’s minimum limits.

How to Find Every Dollar Available for Your Recovery

Uncovering All Insurance Policies That Apply to Your Case

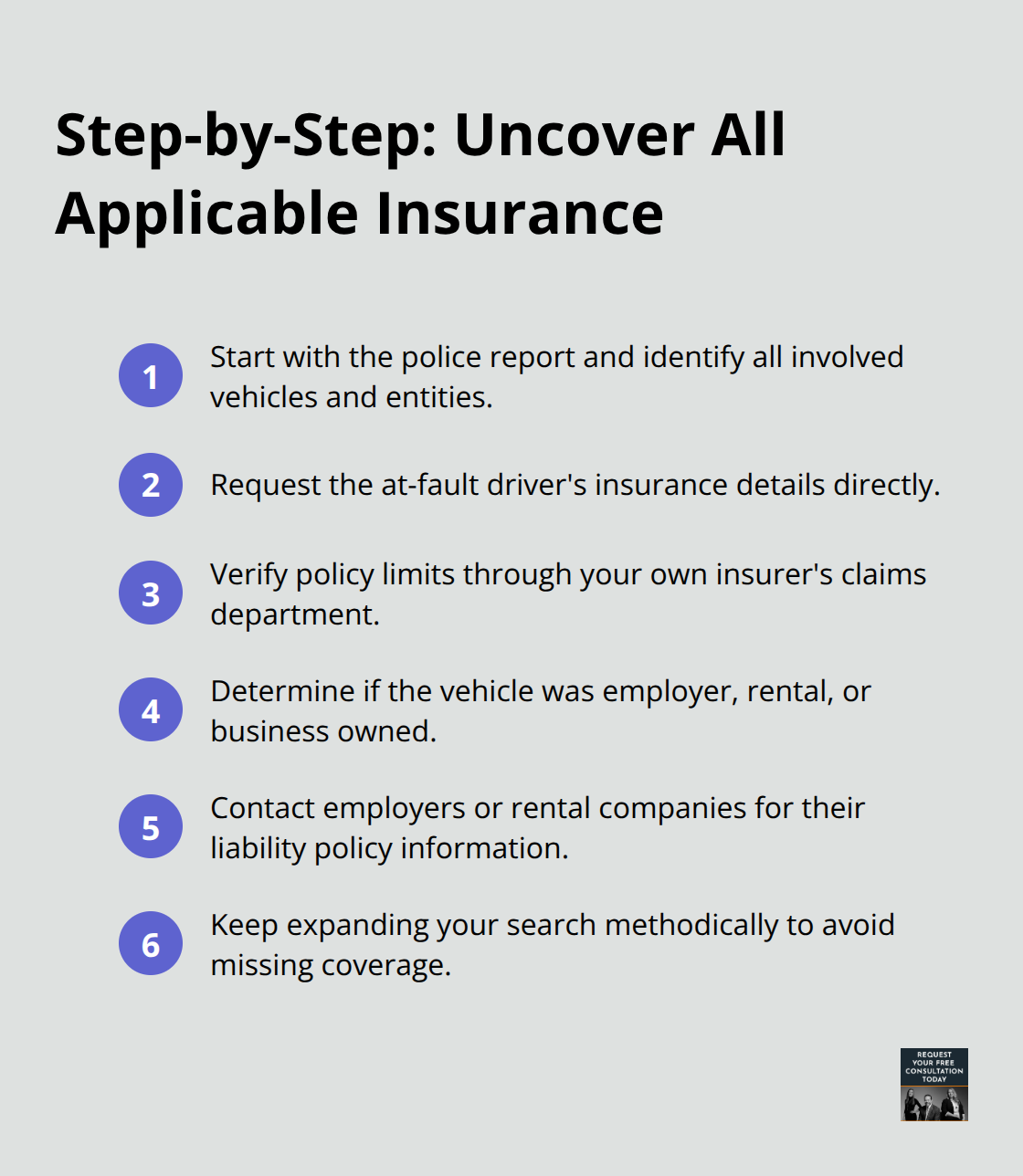

Insurance policies stack when multiple parties bear responsibility for your accident, and most victims never investigate beyond the at-fault driver’s primary coverage. Start with the police report, which names the at-fault driver and often identifies whether a commercial vehicle or government entity was involved. Request the at-fault driver’s insurance information directly and verify their policy limits through your own insurer’s claims department. Then expand your search systematically.

If the vehicle belonged to an employer, that company’s commercial liability policy typically carries higher limits than a personal auto policy-sometimes $500,000 to $1,000,000 or more. A rideshare driver, delivery worker, or contractor involved in your crash triggers both personal and commercial coverage. Contact the vehicle owner’s employer and request their insurance information; they’re legally required to provide it. Check whether a rental company owned the vehicle, as rental companies maintain substantial liability coverage separate from the driver’s personal policy.

Government Vehicles and Third-Party Liability

If a government vehicle caused the crash-a city bus, county maintenance truck, or police vehicle-the government agency carries its own insurance with different claim procedures and timelines. Property owners and maintenance contractors may also carry liability coverage if road conditions, debris, or negligent maintenance contributed to the accident. Each additional policy represents a distinct recovery source.

After identifying all available policies, file claims with each one, documenting how the accident caused your injuries and damages. Insurance companies won’t volunteer information about competing policies or higher limits; you must uncover them through investigation.

Managing Medical Bills Through Liens and Negotiation

Medical bills consume most settlement proceeds, which is why controlling those costs directly impacts your net recovery. Medical lien services allow providers to defer payment until your case settles, meaning you don’t pay bills out of pocket while waiting for compensation. Rather than paying $80,000 in medical expenses immediately, a medical lien allows your provider to wait for settlement funds, reducing your out-of-pocket burden during recovery.

When negotiating your final settlement, medical lien services often negotiate reduced rates with providers-sometimes recovering 10 to 25 percent in bill reductions. This means if your medical bills total $100,000, negotiated liens might reduce that to $75,000 to $85,000, leaving more of your settlement in your pocket. We at Schaar & Silva LLP can direct you to medical lien services that manage your bills strategically.

Documenting Economic Damages and Subrogation Rights

Document every medical expense meticulously: hospital bills, surgeon fees, physical therapy invoices, prescription costs, and transportation to appointments. These documents prove economic damages and support higher settlement demands. If the at-fault driver’s insurance limits won’t cover your full medical expenses, your own health insurance may cover treatment, and you can recover those payments from the settlement through subrogation rights.

The key is separating what you owe from what you actually pay-medical liens create that separation and protect your recovery.

Final Thoughts

California car accident limits create a system where most drivers carry inadequate coverage, leaving victims to bridge the gap between what insurance pays and what accidents actually cost. Understanding how these limits work and where additional recovery sources exist transforms your ability to obtain fair compensation. The state’s minimum requirements protect insurance companies more than accident victims, which is why investigating every available policy, identifying liable parties, and managing medical bills strategically becomes essential to your recovery.

We at Schaar & Silva LLP recognize that navigating California’s fault-based insurance system while recovering from injuries is overwhelming. You manage medical appointments, deal with pain and lost wages, and face pressure from insurance companies to settle quickly for amounts far below what you’re owed. Our team helps clients in Santa Cruz County, Sacramento, and Oakland understand their rights within California’s system, identify all available insurance sources, and pursue claims methodically rather than accept inadequate offers.

Contact us to discuss your accident, your injuries, and the coverage limits you’re facing. We investigate your case, identify every insurance policy that applies, and build a strategy to maximize your recovery within California car accident limits. You don’t pay unless we recover compensation for you, which means pursuing your claim carries no financial risk.