After a car accident in Santa Cruz County, one of your first questions is likely about timing. How long will your settlement timeline take? The answer depends on several factors unique to your case.

At Schaar & Silva LLP, we’ve guided many accident victims through this process. Understanding what to expect helps you plan ahead and avoid unnecessary stress.

Timeline Reality for Santa Cruz Auto Settlements

Most California car accident settlements wrap up between three to nine months after the crash, but Santa Cruz County cases vary widely based on what happened and how badly someone was hurt. Soft tissue injuries like whiplash settle in two to four months because medical treatment finishes quickly and damages are straightforward to calculate. Brain injuries, spinal cord damage, or cases requiring multiple surgeries stretch timelines to a year or longer because you cannot settle until your medical team declares maximum medical improvement, or MMI. Settling before MMI costs victims tens of thousands of dollars by underestimating future medical bills and ongoing care needs. The severity of your injuries directly controls how long you wait, not insurance company goodwill or legal pressure.

What Actually Moves Your Case Forward

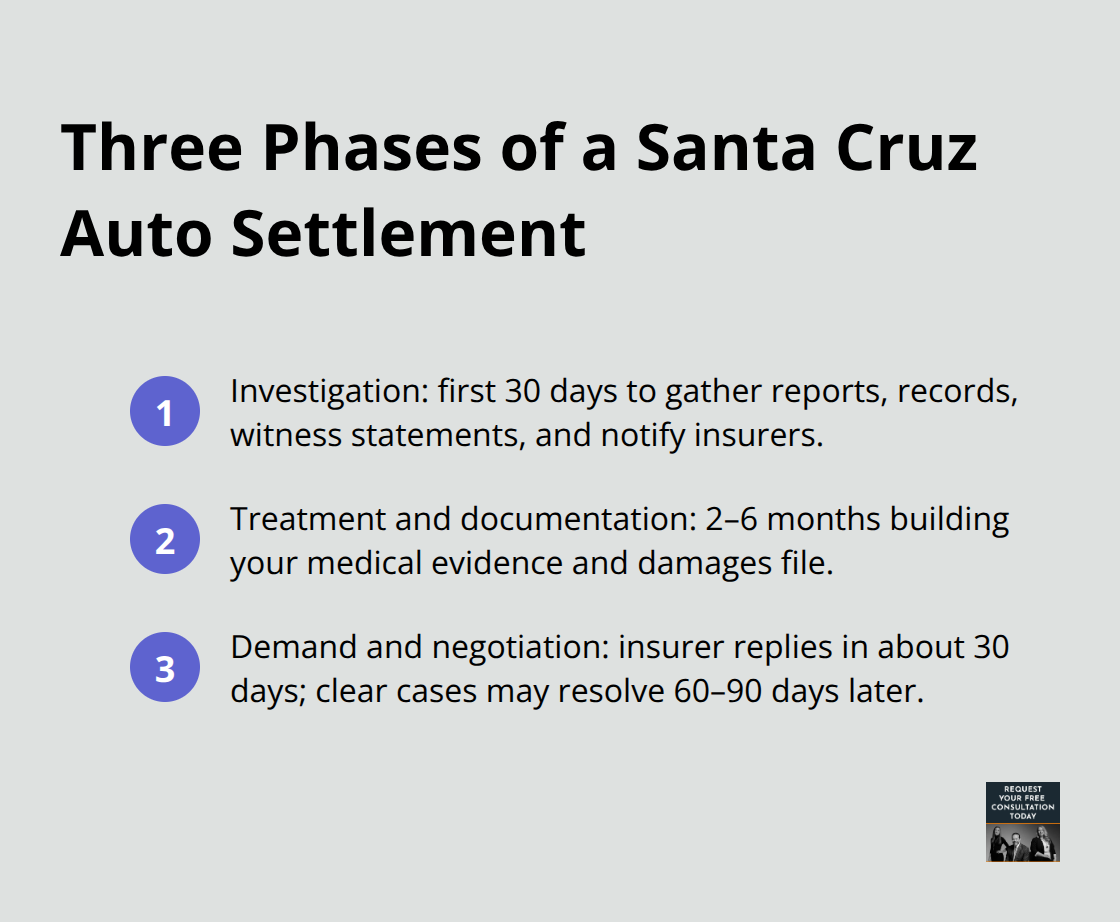

The process breaks into three distinct phases. First comes investigation during the first 30 days after your crash-police reports are gathered, medical records are collected, witness statements are documented, and representation letters go to the insurance company. Next is treatment and documentation spanning two to six months while you receive ongoing medical care that builds your damages file.

Settling during active treatment costs you money because your final medical costs remain unknown. The third phase starts after treatment ends: your attorney sends a demand package, insurers typically respond within 30 days, and straightforward cases with clear liability settle within 60 to 90 days after that demand arrives. Clear liability situations like rear-end collisions or red-light violations move faster than disputed fault cases or multi-vehicle crashes where blame gets tangled.

How Your Specific Situation Changes Everything

Cases with one defendant and damages under policy limits settle considerably faster than situations where damages exceed California’s minimum bodily injury coverage of fifteen thousand dollars per person. When damages exceed that threshold, you pursue underinsured motorist coverage or additional defendants, which adds months to resolution. Commercial vehicle crashes involving trucking companies or rideshare platforms layer in corporate insurance procedures and additional defendants, lengthening timelines but often increasing settlement amounts significantly. Policy limits and liability questions shape your timeline more than anything else, so understanding your insurance situation early matters tremendously.

What Happens Next in Your Case

Once you understand your settlement timeline, the actual negotiation process begins. Insurance companies follow predictable patterns when they respond to demand letters, and knowing what to expect helps you stay focused on recovery rather than worry.

How the Settlement Process Actually Works

Your settlement does not happen overnight, and the path from accident to payment follows a predictable sequence that you need to understand. The first thirty days matter most because your attorney gathers the police report, collects initial medical records, documents witness statements, and sends a representation letter to the insurance company. During this phase, the insurer knows you have legal representation, which stops them from contacting you directly or pressuring you into a quick statement. Talking to the other driver’s insurance adjuster without an attorney present can tank your case, so having representation from day one protects your rights and prevents costly mistakes.

Building Your Damages File Takes Time

Once the initial investigation wraps up, months two through six are dedicated to ongoing medical treatment and documentation. This is where victims make their biggest mistake by rushing to settle before treatment finishes. Your damages file grows with each medical appointment, each test result, each therapy session, and each specialist visit. If you settle during active treatment, you guess at future costs, and that guess almost always underestimates what you’ll actually need. After your medical team declares maximum medical improvement, your attorney compiles everything into a formal demand package that outlines your injuries, treatment costs, lost wages, and pain and suffering damages.

When the Insurance Company Responds

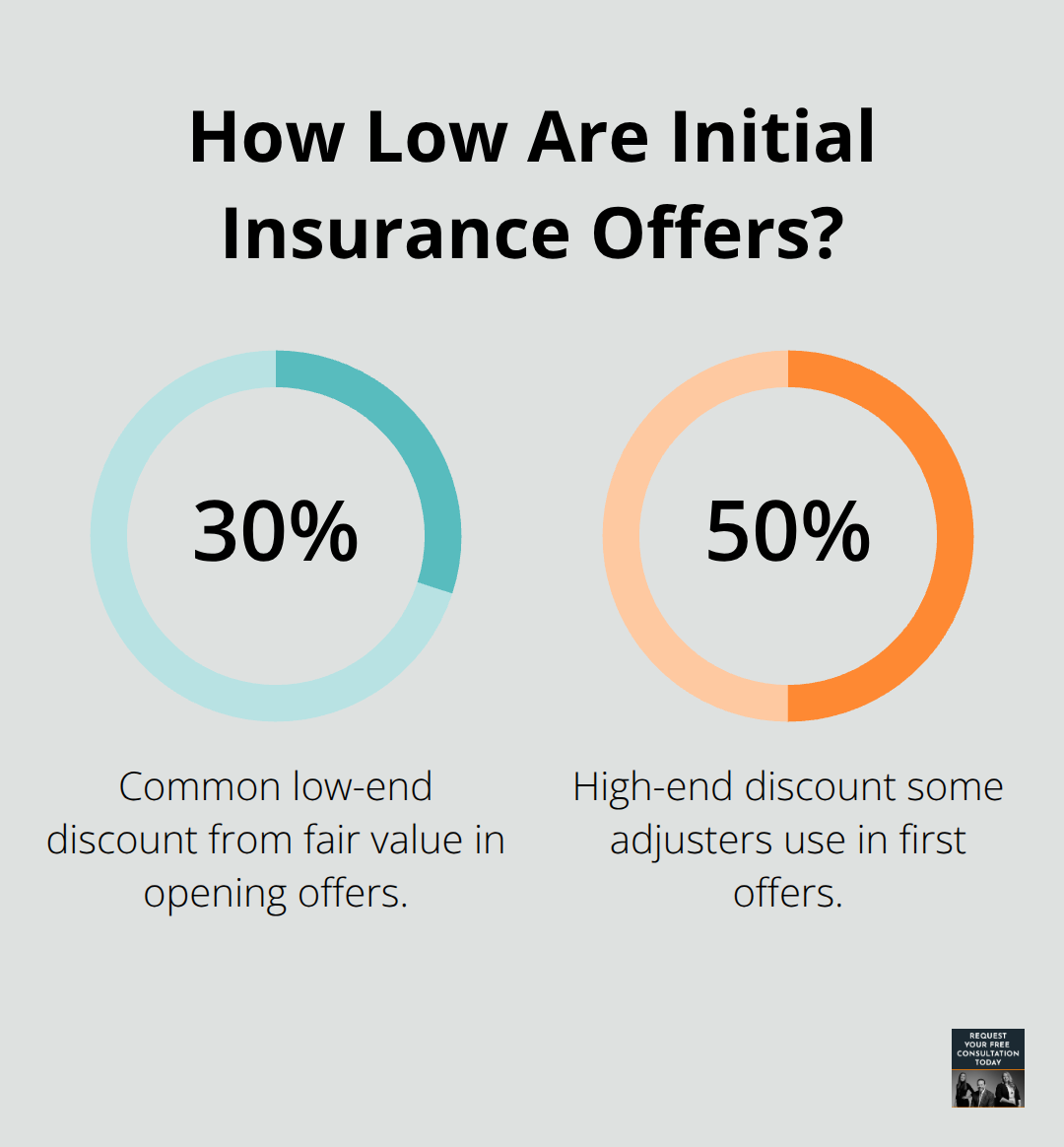

The insurance company typically responds within thirty days of receiving your demand package, and this is when real negotiation begins. Straightforward cases where liability is crystal clear settle within sixty to ninety days after the demand arrives. The insurer knows they’re liable, your damages are documented, and both sides want resolution. But if liability is disputed or multiple vehicles were involved, this negotiation phase stretches longer because the insurer questions who caused the crash and what injuries actually resulted from it. The adjuster’s opening offer is deliberately low-typically 30 to 50 percent below what your claim is actually worth.

Speeding Up Settlement Through Organization

Insurance companies delay when they sense confusion or desperation, so organized documentation, clear evidence of fault, and patient professional representation speed everything forward. Mediation sometimes becomes necessary when initial settlement offers are far apart, and having an attorney who understands Santa Cruz County’s court system and local insurance practices matters significantly in reaching fair agreements. Once both sides agree on a settlement amount, you sign a release document that closes your claim, and payment typically arrives within two to six weeks as the check processes and clears.

What Happens to Your Money After Settlement

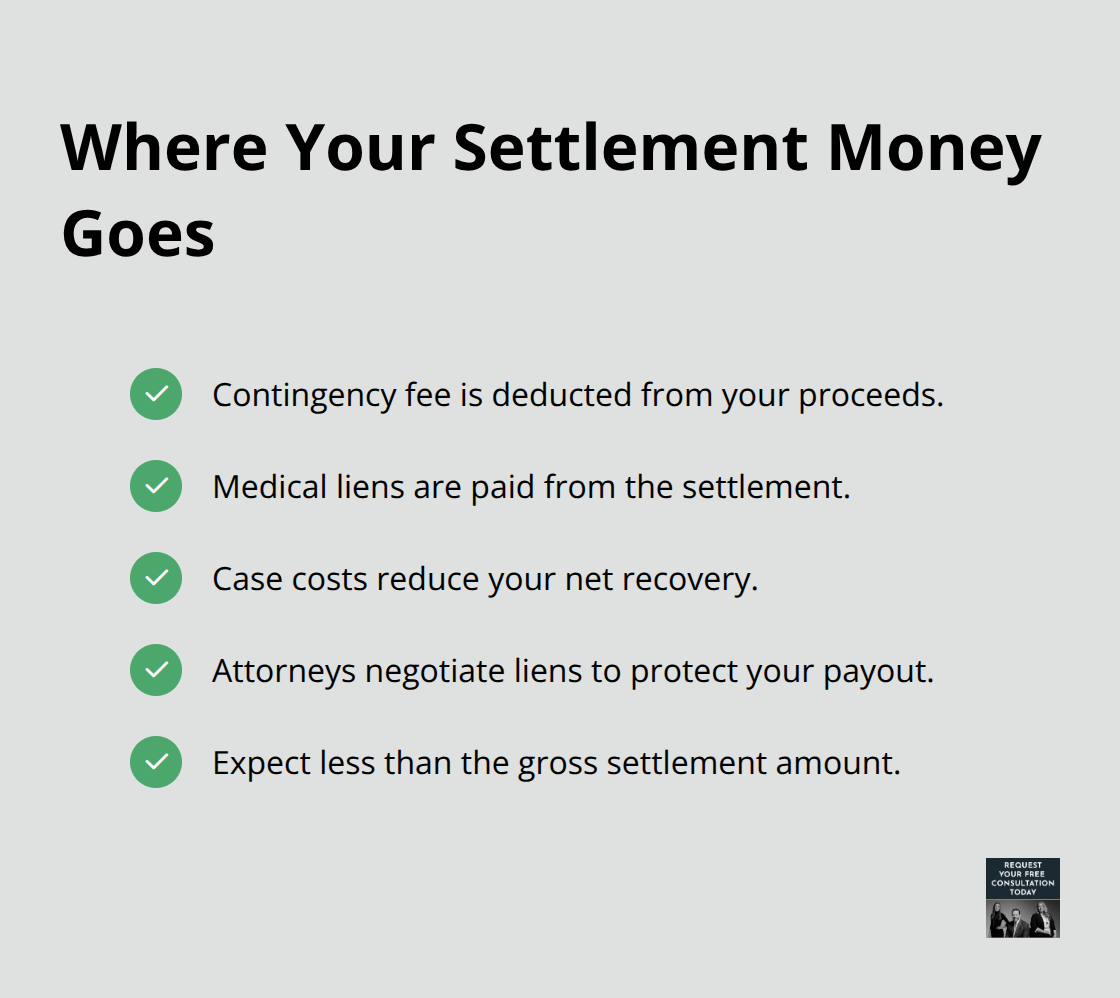

The settlement funds you receive are not the full amount agreed upon. Your attorney’s contingency fee (typically 33 to 40 percent of the settlement) comes from your proceeds, and medical liens and outstanding case costs reduce your final payment. Your attorney handles lien negotiations to protect your recovery, and understanding these deductions helps you plan for what you’ll actually receive.

After payment clears, you move forward with your recovery knowing the legal process is complete.

What Slows Down Your Settlement

Insurance Company Investigations Create Bottlenecks

Insurance company investigations stall settlements when adjusters request duplicate medical records, reassign your case to new adjusters who restart their review, or renew liability questions months into the process. A new adjuster frequently re-examines evidence already reviewed, costing you weeks or months of wasted time. California’s two-year statute of limitations gives insurers room to delay tactics without facing immediate consequences, though ethical practices still apply. The investigation phase typically takes 30 days initially, but if the insurer questions fault or injury causation, they extend this phase indefinitely through requests for additional statements, surveillance footage, or expert opinions on accident reconstruction.

Liability Disputes Extend Timelines Significantly

Santa Cruz County cases with unclear liability-where both drivers partially contributed to the crash-see investigations stretch to four or five months because the insurer calculates their exposure differently depending on fault percentages. Multi-vehicle crashes compound this problem exponentially. Determining which driver caused the initial impact, whether a third vehicle contributed, and how damages should be apportioned takes months of investigation and often requires expert testimony. The insurer’s opening settlement offer typically comes in at 30 to 50 percent below fair value, forcing multiple rounds of negotiation that extend timelines by 60 to 90 days.

Medical Treatment Controls When Settlement Happens

Your medical treatment timeline directly controls when settlement can actually happen because you cannot settle until your doctor declares maximum medical improvement. If you need surgery, physical therapy for three months, and follow-up specialist appointments, you’re looking at minimum five to seven months before settlement discussions become realistic. Settling before MMI creates a financial disaster, as hidden complications emerge months later and you’ve already signed away your rights to additional compensation.

Disputes Over Damages Create Extended Negotiations

Disputes over liability and damages create the longest delays because the insurer’s valuation of your pain and suffering, lost wages, or permanent disability differs dramatically from your actual losses. Cases where you missed work for six months face pushback from adjusters questioning whether your lost wages truly resulted from the accident or other factors. Commercial vehicle accidents involving delivery trucks or rideshare drivers add corporate insurance procedures and additional layers of investigation that routinely extend settlements by three to four months beyond typical timelines.

Final Thoughts

You control more of your settlement timeline auto crash than you might think. Organized documentation from day one speeds everything forward-keep medical records filed, maintain a log of lost wages, photograph injuries, and preserve all accident-related communications. Avoid posting about your case on social media, never give recorded statements to the other driver’s insurer without an attorney present, and maintain consistent medical treatment without gaps that adjusters will exploit.

Getting legal representation early matters far more than waiting until problems arise. An attorney stops the insurance company from contacting you directly, prevents you from making statements that undermine your case, and handles the complex negotiation process where adjusters deliberately lowball initial offers. We at Schaar & Silva LLP help Santa Cruz County accident victims navigate this process by managing medical bill assistance through lien services, evaluating property damage claims fairly, and connecting you with psychological support when emotional trauma complicates recovery.

After your settlement resolves and payment clears, your recovery continues beyond the courtroom. Understanding what you’ll actually receive after attorney fees and medical liens prevents financial surprises, and the release document your attorney reviews closes your claim while protecting you from losing rights to future medical complications. If you’re facing an auto accident settlement in Santa Cruz County, contact Schaar & Silva LLP for a free evaluation to understand your specific timeline and maximize your recovery.