After a car accident, one of your first questions is probably how long an auto claim takes. The answer depends on several factors, from the severity of your injuries to how quickly your insurance company responds.

At Schaar & Silva LLP, we’ve helped accident victims in Santa Cruz County, Sacramento, and Oakland navigate this process. We know the timeline matters because you need compensation to cover medical bills, lost wages, and vehicle repairs.

What Actually Happens During an Auto Claim

The timeline for your auto claim breaks down into three distinct phases, and understanding what happens in each one helps you know what to expect. From the moment you file to the day you receive payment, the process typically takes three to six months for straightforward cases, according to the Insurance Information Institute. Complex cases with severe injuries or disputed liability stretch well beyond a year, but most people don’t realize that how you handle the early stages directly impacts speed.

File Your Claim Within Days, Not Weeks

After your accident, you have a narrow window to act. California law requires insurance companies to acknowledge your claim within 15 days and issue a decision within 40 days of receiving all required documentation. The clock starts the moment you report the accident, so filing immediately matters more than you might think. When you contact your insurer, provide the police report number, photos of vehicle damage, and contact information for any witnesses. The National Highway Traffic Safety Administration reported 5.8 million police-reported crashes in 2022, which means insurance companies manage enormous caseloads. Delays often stem from incomplete initial documentation, so submit everything requested the first time rather than trickling information in gradually. Many people wait weeks before gathering photos or obtaining medical records, and this hesitation alone adds months to your timeline.

Investigation Takes Longer Than You’d Think

Once you file, the insurance company launches its investigation into liability and damages. This phase typically lasts several weeks to several months depending on case complexity. If liability is clear, this moves quickly. If the other driver contests fault or multiple vehicles are involved, the investigation deepens. Medical records also matter significantly here, which is why delaying treatment hurts your timeline. Don’t settle before you reach Maximum Medical Improvement, meaning you finish treatment or your condition stabilizes. Settling too early leaves you vulnerable to unexpected medical costs later.

Stay Connected With Your Adjuster

During the investigation phase, stay in regular contact with your adjuster and request written updates to document progress. If you cannot reach the adjuster, ask to speak with a supervisor. This direct communication keeps your case moving and prevents your file from sitting idle in a backlog. Written updates create a paper trail that protects you if disputes arise later.

Negotiate and Finalize Your Settlement

The negotiation phase follows investigation, and this is where settlement amounts get hammered out. Back-and-forth offers between your attorney and the insurance company can take weeks or months, especially if significant disagreement exists over damages. Once both sides agree and any liens are resolved, payment typically arrives within 30 days of signing the release. The speed of this final phase depends heavily on how organized your documentation is and whether medical providers have filed liens against your settlement. Understanding what happens next-and how legal representation can accelerate the process-becomes important if your claim stalls or the insurer’s offer falls short of your actual losses.

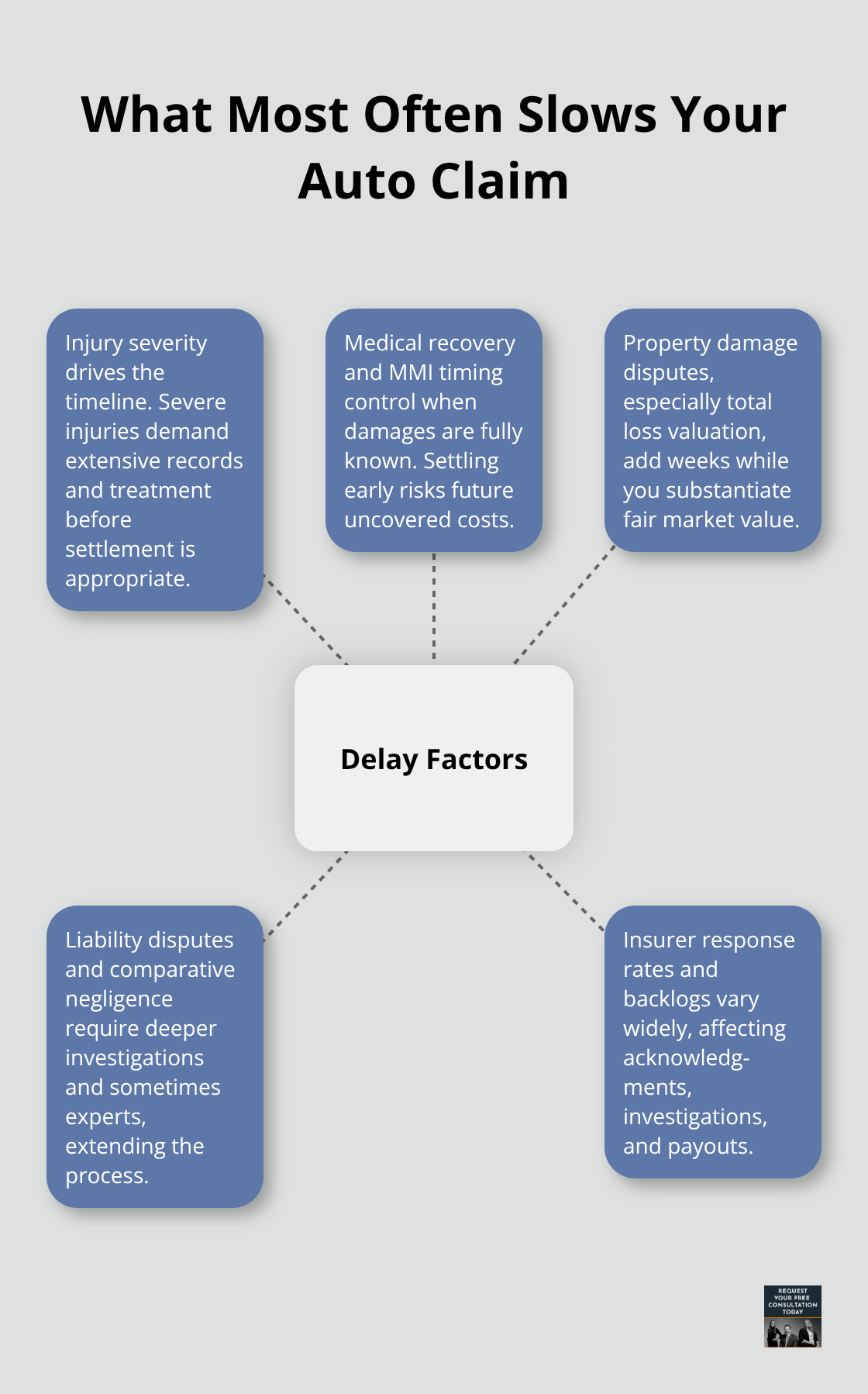

What Slows Down Your Auto Claim

Injury severity stands as the single biggest factor determining how long your claim takes. Minor injuries with clear medical documentation settle in three to six months, while severe injuries involving hospitalization, surgery, or ongoing therapy extend timelines to twelve months or beyond. The Insurance Information Institute confirms that straightforward claims with minor injuries typically resolve in three to six months, but catastrophic injuries require extensive medical records, specialist reports, and damage calculations that take considerably longer. You cannot rush this phase without harming your case.

Medical Recovery and Settlement Timing

Settling before you reach Maximum Medical Improvement means accepting compensation based on incomplete information about your long-term medical needs. If you have a spinal cord injury or traumatic brain injury, medical recovery takes time, and your settlement must account for future treatment, rehabilitation, and potential disabilities. Your medical records drive the timeline forward, so completing treatment or reaching stability matters more than speed.

Property Damage Complications

Vehicle repair estimates are straightforward, but if your car is totaled and disputes arise over its actual cash value, this disagreement alone adds weeks to your timeline. The insurer may undervalue your vehicle, forcing you to provide additional documentation or expert appraisals to justify fair market value. This back-and-forth extends the overall claim duration significantly.

Liability Disputes and Fault Determination

Liability disputes create the most significant delays. When the other driver denies fault or comparative negligence applies, the investigation deepens dramatically. California uses a fault-based system, meaning you must prove the other driver caused the accident. If both drivers share responsibility, California’s comparative negligence rules allow you to recover damages even if you’re partially at fault, but determining exact percentages requires extensive evidence gathering and sometimes expert testimony. This process is not quick.

Insurance Company Response Rates and Backlogs

Insurance company response time varies wildly depending on their caseload and internal processes. The National Highway Traffic Safety Administration reported 5.8 million police-reported crashes in 2022, creating massive backlogs at many insurers. Some companies acknowledge claims within days; others take the full 15 days allowed by California law. Once they issue a decision, they have 30 days to pay if the claim is approved, but investigations can extend well beyond this timeframe for complex cases.

Identifying and Addressing Delays

If your insurer requests additional documentation, ask specifically what they need and when they need it. Vague requests for more information are often delay tactics. Document every communication in writing, and if the insurer seems to be stalling without valid reason, they may be acting in bad faith. When delays become unreasonable, legal representation becomes essential to escalate the matter and push for faster resolution. An attorney can identify whether the insurer is using legitimate investigative procedures or employing stalling tactics to pressure you into accepting a lower settlement.

How to Speed Up Your Auto Claim

Photograph everything at the scene before you leave, including vehicle positions, damage to both vehicles, road conditions, and any visible injuries. These photos become critical evidence that insurers use to assess liability and damage severity, and they cost you nothing but a few minutes of your time. Police reports matter equally, so obtain the report number immediately and request a copy within days, not weeks. Many people delay this step, then struggle to locate the report later when the insurance company asks for it. Witness statements also carry significant weight, so collect names and phone numbers from anyone who saw the accident happen, even if they seem reluctant to get involved. The Insurance Information Institute notes that straightforward claims with clear evidence typically settle in three to six months, while cases lacking solid documentation stretch well beyond a year. Your evidence collection phase determines whether your claim moves quickly or stalls in investigation limbo.

Organize Your Documentation Before Your Insurer Asks

Create a single folder or digital file containing your police report, accident photos, witness contact information, and the other driver’s insurance details. Add to this folder every medical bill, prescription receipt, and treatment record as you receive them, along with documentation of lost wages from your employer. When your adjuster requests information, you can respond within hours instead of scrambling for documents over several days. Insurance companies process thousands of claims simultaneously, and claimants who submit complete documentation on the first request move to the front of the queue while those trickling information in gradually fall behind. Maintain a log of every communication with your insurer, including dates, times, names of people you spoke with, and what was discussed. This written record protects you if disputes arise later about what was promised or what deadlines were set. Request written confirmation of important conversations via email, and save every message your adjuster sends. This documentation becomes invaluable if the insurer later claims they never received information you clearly submitted, or if their response times become unreasonably slow.

Request Written Updates and Set Clear Deadlines

Contact your adjuster every two weeks during the investigation phase and ask for a specific status update in writing. Do not accept vague responses about things being in progress. Request concrete information such as when medical records were received, whether liability has been determined, and when you can expect a settlement offer. If your adjuster does not respond within three business days, escalate to their supervisor and document that escalation. California law requires insurers to acknowledge claims within 15 days and issue decisions within 40 days of receiving complete documentation, so you have a legal baseline for what constitutes reasonable speed. When these timelines slip without explanation, the insurer may be acting in bad faith, which gives you grounds to pursue legal action or file a complaint with the California Department of Insurance. An attorney can identify whether delays stem from legitimate investigative needs or deliberate stalling tactics designed to wear you down into accepting a lower settlement.

Final Thoughts

Your auto claim timeline depends on how organized you are and whether legal support pushes the process forward. Straightforward cases with clear liability and minor injuries typically resolve in three to six months, while severe injuries or disputed fault extend timelines well beyond a year. The speed of your claim rests largely in your hands during the early stages, when you gather evidence, file promptly, and maintain organized documentation that directly impacts how quickly your insurer moves.

Legal representation becomes valuable when your claim stalls, the insurer’s offer falls short of your actual losses, or liability disputes emerge. An attorney identifies whether delays stem from legitimate investigation or bad faith tactics designed to pressure you into accepting less than you deserve. We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland understand their rights and navigate the claims process efficiently (our team handles medical bill assistance, property damage evaluation, and the legal complexities that slow many claims).

If your claim has been pending longer than expected or you’re unsure whether an insurer’s offer is fair, contact us for a free consultation. We can review your situation, identify what’s causing delays, and determine whether legal action will accelerate your path to fair compensation.