After a car accident in Santa Cruz County, dealing with property damage claims can feel overwhelming. Insurance companies often undervalue vehicles or deny legitimate repairs, leaving you with gaps in coverage.

We at Schaar & Silva LLP help accident victims navigate these claims and fight for fair reimbursement. This guide walks you through valuation methods, common settlement problems, and the steps to protect your rights.

How Property Damage Claims Work in Santa Cruz

The first 48 hours after your accident determine whether you’ll receive fair compensation or face a lowball settlement. Stop at the scene, call 911 if anyone is injured, and contact the police-the officer’s name, badge number, and report number become anchors for your credibility later. Exchange names, addresses, driver’s licenses, vehicle details, and VINs with the other driver. If they’re not present, leave a note with your contact information.

California law requires DMV reporting within 10 days if injuries or property damage exceeds $750.

Documenting Your Vehicle and the Scene

Photograph your vehicle from multiple angles in daylight, capturing the damage clearly. Document the accident scene, road conditions, and any visible injuries. Gather contact information from witnesses. Get repair estimates from three licensed Santa Cruz repair shops before contacting your insurer-these estimates reveal valuation gaps that insurers typically hide. Collect maintenance records and service receipts showing your vehicle was well-maintained, which prevents insurers from using condition as an excuse to reduce your settlement.

Understanding the Adjuster’s Role

Contact your insurer within days of the accident, not weeks. California’s Department of Insurance requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss. Your insurer will assign an adjuster who typically completes inspections in under an hour, relying heavily on NADA Guides to value repairs. This approach creates problems because NADA Guides underestimate Santa Cruz labor rates and parts costs by roughly $2,000 to $5,000. The adjuster’s quick inspection often misses hidden damage (frame misalignment, water intrusion, suspension issues, and electrical problems).

Building Your Case Against Lowball Offers

Do not accept the insurer’s initial offer. The typical gap between their first offer and actual repair costs runs $2,000 to $5,000. An independent appraisal costs $300 to $600 upfront but justifies settlement increases of $2,000 to $5,000 or more under California law. Use your three repair estimates to build a documentation package showing discrepancies between the insurer’s valuation and actual costs. Organize all documents chronologically in a single file to accelerate insurer responses and pressure timely action.

When Negotiations Stall

If negotiations stall, legal review helps evaluate your options and pursue additional compensation. The team at Schaar & Silva LLP can assist in evaluating the extent of property damage and help you receive a fair valuation for your loss. Understanding what happens next in the valuation process shapes your entire settlement strategy.

How Insurers Calculate Your Vehicle’s Value

Insurance companies use three methods to establish your vehicle’s value, and understanding each one protects you from accepting artificially low settlements. Kelley Blue Book anchors pre-accident value based on your vehicle’s make, model, year, and mileage, but the mileage brackets create significant swings in valuation. A 2022 Hyundai Kona with 85,000 miles versus 95,000 miles shifts the pre-accident value by approximately $1,500 to $3,000, which means the adjuster’s assessment of your odometer reading directly impacts your payout.

Why NADA Guides Underestimate Local Repair Costs

NADA Guides then estimate repair costs, but this is where most Santa Cruz accident victims lose money. NADA Guides consistently underestimate local labor rates and parts costs by roughly $2,000 to $5,000 compared to what licensed Santa Cruz repair shops actually charge. Your insurer’s adjuster, who typically spends less than an hour on your vehicle, relies on these guides without questioning whether they reflect real-world pricing in Santa Cruz County.

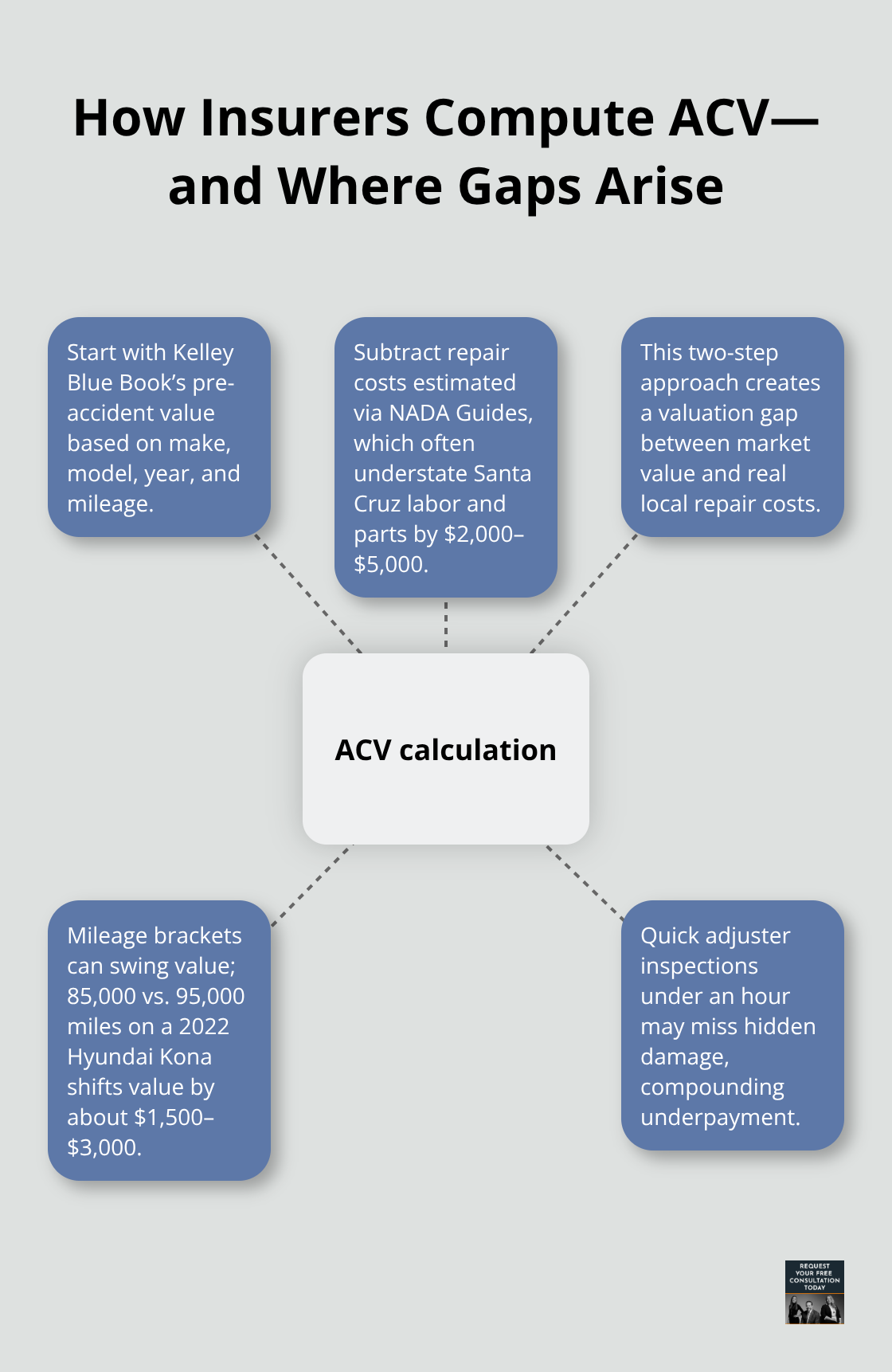

How Actual Cash Value Gets Calculated

Actual Cash Value (ACV) represents what insurers ultimately pay-the fair market price a knowledgeable buyer and seller would accept. Insurers calculate this by starting with Kelley Blue Book’s pre-accident value and then subtracting repair costs estimated through NADA Guides. This two-step process creates the valuation gap you’ve heard about, because Kelley Blue Book may overstate your vehicle’s condition or market value in Santa Cruz, while NADA Guides understate what repairs actually cost locally.

Using Repair Estimates to Challenge Lowball Valuations

Your three repair estimates from licensed Santa Cruz shops are your most powerful tool against this system. These estimates reveal the true labor costs and parts pricing your insurer ignored when relying on NADA Guides. When repair costs exceed your vehicle’s ACV, insurers declare a total loss and pay only the depreciated value minus salvage, meaning you lose money even when the other driver caused the accident. California law allows independent valuations to challenge this outcome. An independent appraiser costs $300 to $600 upfront but provides documentation that justifies settlement increases of $2,000 to $5,000 or more by proving the insurer’s valuation was incorrect.

Building a Documentation Package That Works

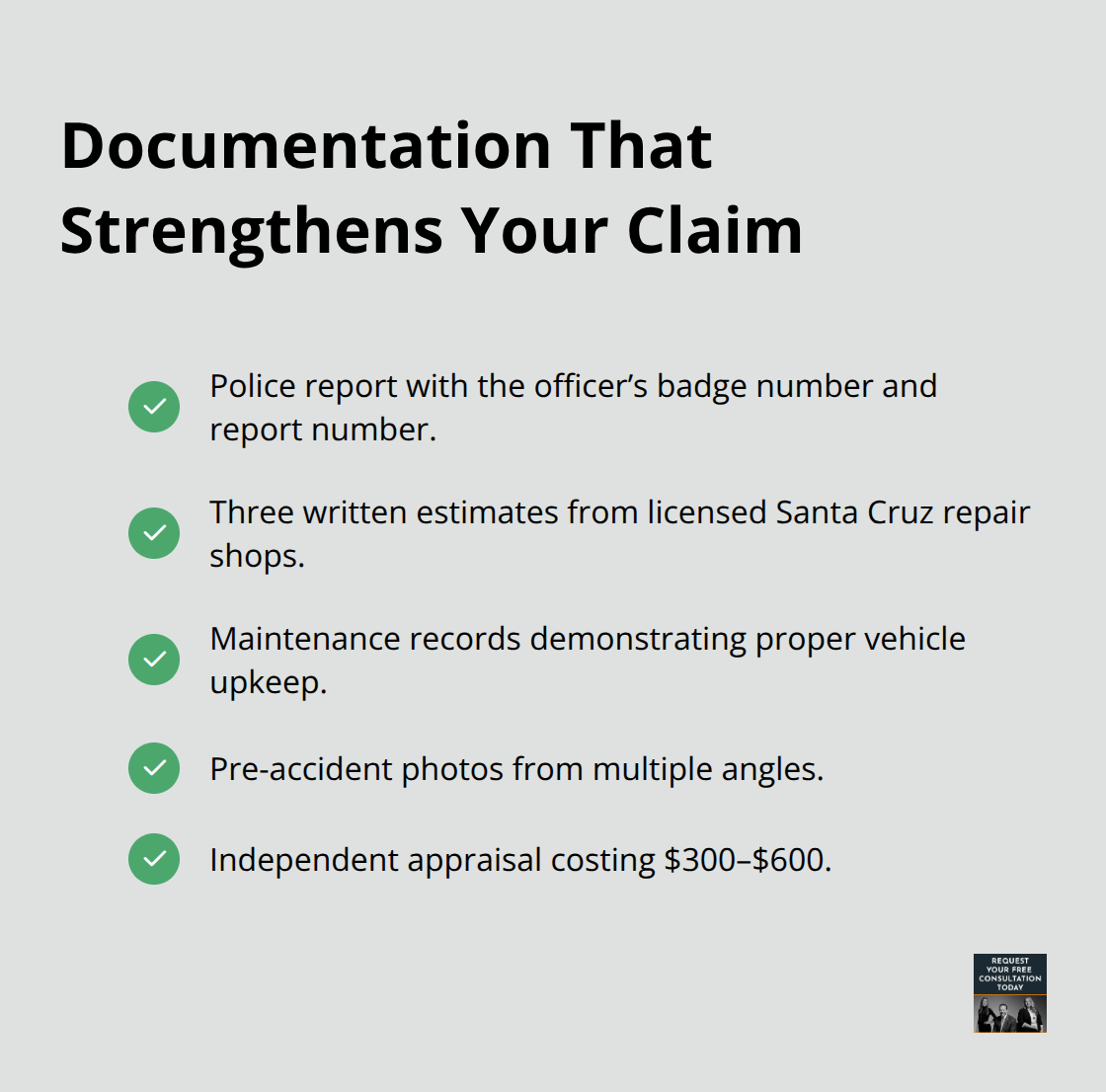

The appraiser examines your vehicle’s condition, verifies mileage, checks for prior accident history, and documents proper repairs-all factors that strengthen your negotiating position. Do not rely on the insurer’s preferred vendor network for repair estimates; independent Santa Cruz shops’ estimates carry more weight because they have no financial relationship with the insurance company. Organize your documentation chronologically: the police report, your three repair estimates, maintenance records, pre-accident photos, and the independent appraisal if you obtain one. This package demonstrates that the insurer’s initial offer diverges significantly from actual repair and replacement costs in Santa Cruz County, pressuring them toward a fair settlement. When disputes arise over what your vehicle is actually worth, knowing how to present this evidence becomes the difference between accepting a lowball offer and receiving compensation that matches your real losses.

Settlement Gaps That Cost You Money

Insurance companies in Santa Cruz County systematically lowball property damage claims because their initial offers rely on flawed valuation methods that ignore local repair costs. The typical gap between an insurer’s first offer and what Santa Cruz repair shops actually charge runs $2,000 to $5,000, and this gap widens when hidden damage surfaces after the quick adjuster inspection. Your vehicle’s condition assessment happens in under an hour, yet frame misalignment, water intrusion, suspension damage, and electrical problems often remain invisible during this rushed evaluation. When repair costs exceed your vehicle’s fair market value, insurers declare a total loss and pay only depreciated value minus salvage-meaning you absorb the financial loss even though the other driver caused the accident. California law allows independent valuations to challenge these outcomes, and an independent appraiser costs $300 to $600 upfront but typically justifies settlement increases of $2,000 to $5,000 or more through documentation of what the insurer’s valuation missed.

Why Insurers Miss Hidden Damage

The adjuster’s one-hour inspection creates blind spots that cost you money. Frame misalignment, water intrusion, suspension issues, and electrical problems require extended evaluation or specialized equipment to detect. Insurers rely on NADA Guides, which underestimate Santa Cruz labor rates and parts costs by roughly $2,000 to $5,000 compared to what licensed repair shops actually charge. This systematic underestimation means the insurer’s initial offer reflects neither the true repair costs nor the hidden damage your vehicle sustained.

How to Build Negotiating Power Before Settlement

Obtain three written estimates from licensed Santa Cruz repair shops before engaging with your insurer’s preferred vendors. Shops with no financial relationship to the insurance company provide estimates that carry genuine negotiating weight. Your documentation package should include the police report (with the officer’s badge number and report number), all three repair estimates itemized by labor and parts, maintenance records proving proper vehicle upkeep, and pre-accident photos from multiple angles. An independent appraisal ($300 to $600) strengthens your position further by documenting what the insurer’s valuation overlooked.

Organizing Evidence for Maximum Impact

Arrange these documents chronologically in a single file to accelerate insurer responses and demonstrate that their initial offer diverges significantly from actual repair costs in Santa Cruz County. This organized package pressures the insurer toward a fair settlement because it presents clear evidence of the valuation gap. When you present itemized repair estimates alongside the independent appraisal, the insurer faces documented proof that their NADA Guides-based offer falls short of reality.

When Negotiations Stall

If the insurer refuses to increase their offer after you present this evidence, legal review becomes necessary to evaluate whether additional compensation is justified. The legal team at Schaar & Silva LLP can assist in evaluating the extent of property damage and help you pursue fair valuation for your loss.

Final Thoughts

After an accident in Santa Cruz County, your immediate actions determine whether you receive fair compensation or accept a lowball settlement. File your claim within days, not weeks, and obtain three repair estimates from licensed local shops before your insurer’s adjuster completes their rushed inspection. Photograph your vehicle from multiple angles, collect the police report with the officer’s badge number, and organize maintenance records showing proper upkeep-this documentation package reveals the valuation gaps that insurers create through NADA Guides and quick inspections that miss hidden damage.

Property damage claims in Santa Cruz require you to challenge the insurer’s initial offer with independent evidence. An independent appraisal costs $300 to $600 upfront but justifies settlement increases of $2,000 to $5,000 or more by documenting what the insurer’s valuation overlooked. Present your three repair estimates alongside this appraisal to demonstrate that the insurer’s offer falls short of actual repair costs in Santa Cruz County.

We at Schaar & Silva LLP help you evaluate the extent of property damage and secure fair valuation for your loss. Contact our legal team to discuss your property damage claim and learn how we support accident victims throughout Santa Cruz County in obtaining the compensation they deserve.