A car crash leaves you stressed, injured, and facing mounting bills. Insurance companies often offer settlements that don’t cover your actual losses.

We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland navigate this process. Learning how to negotiate insurance claims puts you in control and protects your financial recovery.

What to Document Right After a Crash

The moments immediately after a crash are chaotic, but what you document then determines your negotiating power later. Insurance adjusters rely on incomplete information to justify low offers, so your documentation becomes the evidence that forces them to pay fairly.

Capture the Scene with Photos and Videos

Start with photos and videos before anyone moves vehicles or clears debris. Capture wide shots of the accident scene showing road conditions, traffic signals, and vehicle positions, then close-ups of all vehicle damage from multiple angles. Document weather conditions, time of day, and any visible road hazards. These details matter because adjusters use them to argue liability or minimize injury severity.

If you’re injured, take photos of visible injuries immediately and continue documenting them over the following weeks as bruising or swelling develops. Medical records alone won’t show an adjuster the full impact of your injuries the way visual documentation can.

Gather Information from the Other Driver and Witnesses

Get the other driver’s name, phone number, address, driver’s license number, and license plate. Write down their insurance company and policy number directly from their insurance card, not from what they tell you. Ask for their vehicle identification number and the year, make, and model of their vehicle.

If witnesses are present, collect their full names, phone numbers, and email addresses before they leave. Witnesses often become unavailable later, and their statements carry significant weight in negotiations. Request the police report number from the officer at the scene and note the officer’s name and badge number. The police report creates an official record of fault determination that insurers must acknowledge during settlement discussions.

If you’re too injured to gather this information yourself, ask a passenger, bystander, or call a friend to help you collect these details while you’re still at the scene.

Create a Documentation System That Protects Your Claim

File your insurance claim within the timeframe specified in your policy, typically within 30 days of the accident. Provide your insurer with the police report number and all documentation you’ve gathered. Keep copies of everything you submit and maintain a detailed log of every communication with your insurance company, including dates, times, names of adjusters, and summaries of conversations.

Written follow-ups matter more than phone calls because they create a record adjusters cannot dispute later. When you follow up in writing, adjusters move slower but justify their decisions more carefully. After a crash, the first settlement offer typically falls 30 to 50 percent below what your claim is actually worth, according to settlement data from personal injury cases. This happens because adjusters test your response to see if you’ll accept lowball figures without pushback. Your documentation gives you the foundation to reject those offers with confidence and move into active negotiation with the insurance company.

Know Your Policy Before You Negotiate

Your insurance policy is a contract, and most people never read it until they need to file a claim. This mistake costs accident victims thousands of dollars because they don’t understand your policy completely.

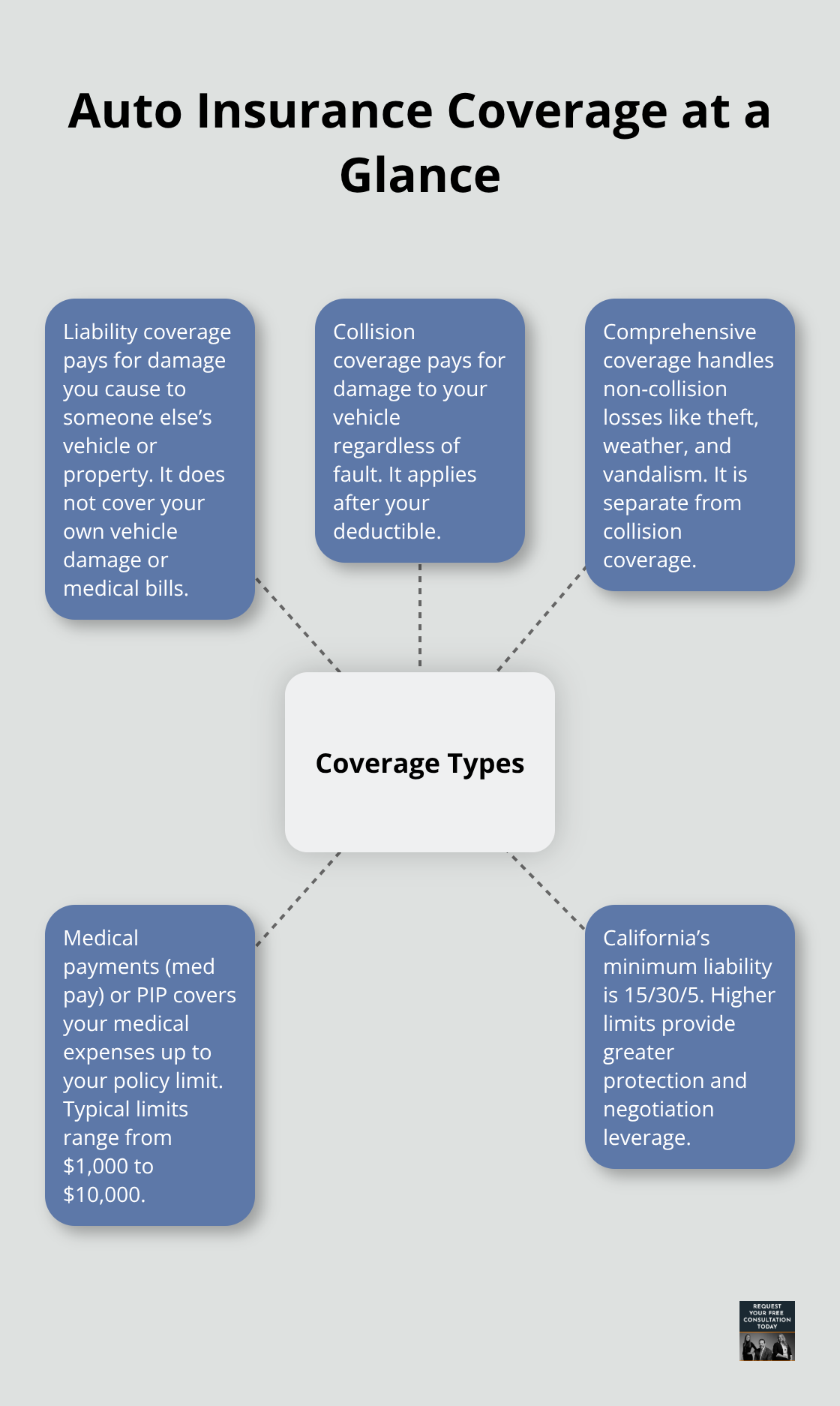

Understand Your Coverage Types and Limits

Liability coverage pays for damage you cause to someone else’s vehicle or property, but it doesn’t cover your own vehicle damage or medical bills. Collision coverage pays for damage to your vehicle regardless of fault, while comprehensive coverage handles theft, weather, and vandalism. Medical payments coverage (med pay) or personal injury protection (PIP) covers your medical expenses up to your policy limit, typically ranging from $1,000 to $10,000.

California requires minimum liability coverage of 15/30/5, meaning $15,000 per person for bodily injury, $30,000 total per accident, and $5,000 for property damage, but most accident victims carry higher limits. Your policy document lists these limits clearly, and you need to know yours before talking to an adjuster because they’ll use your limits to cap what they offer you. Understanding bodily injury limits is critical-if you have a $100,000 medical payments limit but only $15,000 in liability coverage, that’s the number the other driver’s insurer will use to justify their settlement offer to you.

Review Your Declaration Page and Deductibles

Check your declaration page right now-it shows your coverage types, limits, and deductibles in one place. Your deductible is what you pay out of pocket before insurance kicks in, typically $500 to $1,000 per claim, and this reduces what you receive in a settlement. If your vehicle is worth $20,000 and repair costs are $12,000 with a $1,000 deductible, you’ll receive $11,000, not $12,000.

Meet Filing Deadlines to Protect Your Claim

File your claim within the timeframe your policy specifies, almost always within 30 days of the accident, because missing this deadline gives insurers grounds to deny your entire claim. Most policies require notice of the accident within 30 to 60 days, and failure to report timely can result in claim denial under what’s called the late-notice clause.

Document All Communications in Writing

Track every conversation with your insurer in writing by following up phone calls with emails summarizing what was discussed, who you spoke with, and when. This paper trail prevents adjusters from claiming you said something you didn’t, and it documents delays on their end if they stall your claim. Adjusters move slower when you communicate in writing, but they justify their decisions more carefully-and that careful justification becomes your leverage when you negotiate the actual settlement amount.

How to Push Back Against Low Settlement Offers

Your documentation is now organized and your policy is understood. The actual negotiation begins when the insurance adjuster contacts you with an offer. This is where most accident victims make critical mistakes by accepting the first number without question.

Recognize That First Offers Are Deliberately Low

The adjuster’s opening offer is deliberately low, not because they lack information but because they test whether you’ll push back. Settlement data shows that first offers typically run 30 to 50 percent below actual claim value, which means accepting that initial number costs you thousands of dollars. The adjuster knows this gap exists, and they bet you’ll take the offer rather than fight for what you actually deserve.

Your job is to prove them wrong by presenting a counter that’s grounded in real numbers, not emotion. When you respond in writing with documented evidence, adjusters move slower but justify their decisions more carefully. That careful justification becomes your leverage when you negotiate the actual settlement amount.

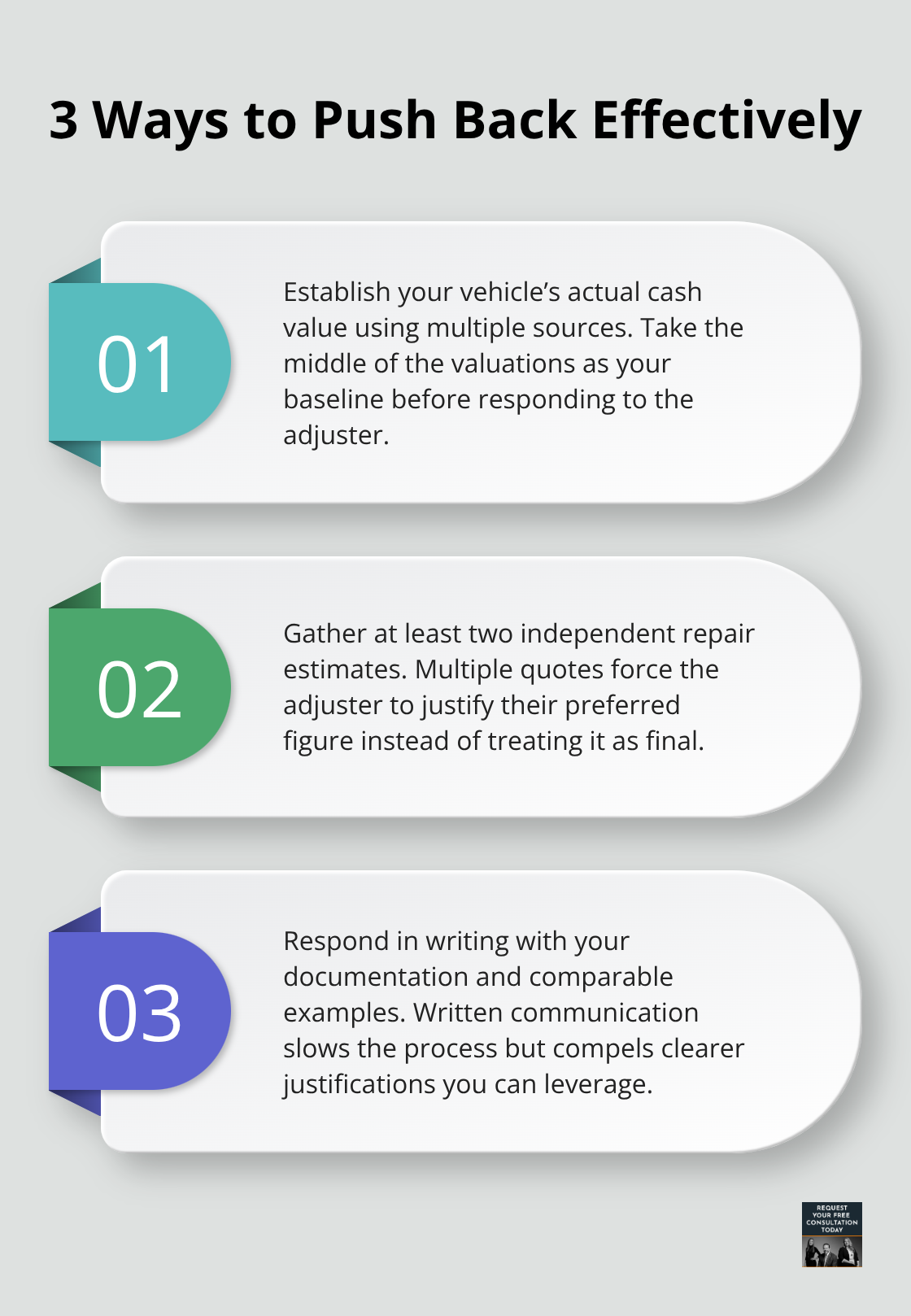

Establish Your Vehicle’s Actual Cash Value

Start by establishing the actual cash value of your vehicle using multiple sources rather than relying on the adjuster’s valuation. Check the NADA Guides, Kelley Blue Book, and local used car listings in your area to see what similar vehicles sell for in Santa Cruz County, Sacramento, or Oakland markets. These three sources often produce different valuations, so pull all three and take the middle figure as your baseline.

If the adjuster’s valuation falls below that middle figure, respond in writing with your documentation showing comparable vehicles and their prices. Adjusters will often adjust their number upward rather than spend time justifying why local market data doesn’t apply to your claim.

Present Multiple Repair Estimates

Include repair estimates from at least two independent body shops in your response, not just the one the adjuster selected. Body shop estimates vary significantly based on shop overhead and labor rates, and presenting multiple estimates forces the adjuster to justify which one is correct instead of simply accepting their chosen figure. When you respond to their low offer, never accept their valuation without documented pushback, and never let them frame the negotiation as final when you have evidence showing otherwise.

Final Thoughts

Some claims become too complex for solo negotiation, particularly when brain and spinal injuries from car crashes require life care plans that project decades of future medical costs or when wrongful death claims involve emotional and financial losses extending far beyond vehicle damage. Attempting to negotiate insurance alone in these situations typically costs you more than professional guidance would have saved. We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland navigate these complex claims and connect you with the support you need during recovery.

Your recovery matters more than the settlement timeline, and the insurance company has adjusters and attorneys working against your interests. You deserve the same level of support working for yours. Contact us to discuss your specific situation and determine whether your claim requires professional representation.

The foundation you build at the accident scene determines your negotiating power months later when settlement discussions begin. Your photos, witness statements, and police report number become the evidence that forces adjusters to justify their numbers instead of simply accepting their initial lowball offers. These actions shift control from the insurance company back to you.