After a car accident in Santa Cruz County, Sacramento, or Oakland, you’ll quickly learn that bodily injury limits on an insurance policy aren’t just numbers on a document-they directly determine how much money you can recover for your injuries.

Many accident victims discover their medical bills far exceed what the at-fault driver’s bodily injury coverage will pay. We at Schaar & Silva LLP help people navigate these limits and fight for fair compensation when coverage falls short.

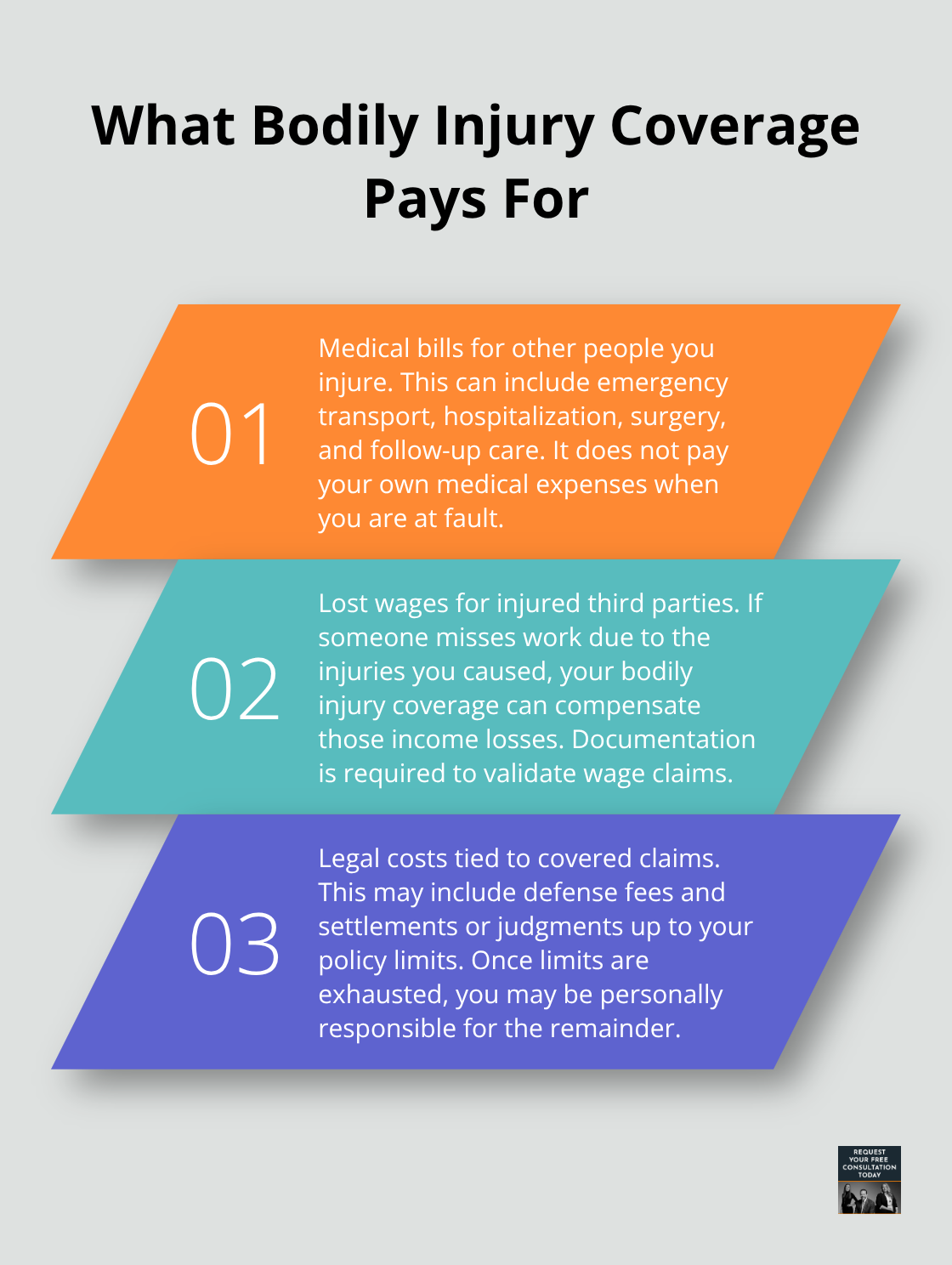

What Bodily Injury Coverage Actually Pays For

Bodily injury coverage pays the medical bills, lost wages, and legal costs of other people when you’re at fault in an accident. If you hit another vehicle and injure the driver or passengers, their medical expenses go to your bodily injury liability coverage, not to your own policy. This distinction confuses many accident victims in Santa Cruz County, Sacramento, and Oakland. Your bodily injury limits represent the maximum dollar amount your insurance company will pay on behalf of the other injured parties. Once those limits are exhausted, you become personally responsible for any remaining costs, which can mean wage garnishment, asset seizure, or ongoing legal judgments against you.

How Your Limits Are Structured

Insurance policies display bodily injury limits as three numbers, typically shown as 25/50/25 or similar ratios. The first number is the per-person limit, the second is the per-accident limit, and the third is property damage coverage. California’s minimum required limits are 15,000 per person and 30,000 per accident for bodily injury, according to the California Department of Insurance. A 25/50/25 policy means the insurance company pays up to 25,000 for one injured person, but no more than 50,000 total for all injured people in that single accident.

When Limits Create Real Problems

If three people are injured and each has 30,000 in medical bills, the 50,000 per-accident limit creates a massive shortfall. Many accident victims in these regions fail to check whether the at-fault driver carries adequate coverage until after the accident occurs, leaving them unable to recover their full damages. The per-accident limit is what truly matters for your financial protection, since serious collisions often involve multiple injured parties.

What Happens When Coverage Falls Short

When medical bills exceed the at-fault driver’s bodily injury limits, you face a critical gap between your actual damages and what insurance will cover. This shortfall forces you to pursue additional recovery options, which we at Schaar & Silva LLP help clients navigate in Santa Cruz County. Understanding how to identify this gap early and take action determines whether you recover fair compensation or absorb the loss yourself.

How Bodily Injury Limits Control Your Recovery

The Ceiling on Your Compensation

Your bodily injury limits set the maximum amount you receive. If the at-fault driver carries 25/50/25 coverage and your medical bills total 40,000, you recover only 25,000 per-person limit-assuming you’re the only injured party. The Insurance Information Institute found that claimants who negotiated settlements typically received about 40% more than those who accepted the initial offer, which means accepting the insurer’s first proposal often leaves money on the table when limits create a cap on recovery. In Santa Cruz County, Sacramento, and Oakland, many accident victims don’t realize their damages far exceed what the other driver’s policy will pay until they’ve already incurred those bills.

The Gap Between Your Losses and Available Coverage

The gap between your actual losses and the at-fault driver’s coverage directly determines whether you absorb the financial burden yourself or pursue additional recovery through your own uninsured/underinsured motorist coverage, a personal injury claim, or both. California’s comparative negligence rule allows you to recover even if you’re partially at fault, as long as you’re under 50% responsible, but this recovery still faces a cap from the at-fault driver’s bodily injury limits unless you have other avenues. A serious accident with multiple injuries exposes the inadequacy of minimum coverage quickly.

Why Minimum Coverage Falls Short

California’s minimum required limits are 15,000 per person and 30,000 per accident, according to the California Department of Insurance, yet a single hospitalization and surgery can exceed 50,000 in costs alone. If three people suffer injuries in one crash, a 30,000 per-accident limit means each person receives only 10,000 on average-far below actual medical expenses. When limits fall short, you must determine whether you have uninsured/underinsured motorist coverage in your own policy to bridge that gap, or whether you need to pursue a personal injury lawsuit against the at-fault driver personally.

Acting Within Your Legal Window

The strongest position for a claim exists within the first 3–6 months while evidence remains fresh, and California generally allows a two-year window to file a personal injury lawsuit under California Code of Civil Procedure §335.1. Acting quickly protects both your legal rights and your financial recovery. We at Schaar & Silva LLP can help direct you to medical lien services that facilitate the payment of your bills until your case is resolved, allowing you to focus on healing while your claim develops.

Understanding how limits constrain your recovery is only half the battle. The next section examines the specific steps you should take when you discover the at-fault driver’s coverage won’t cover your damages.

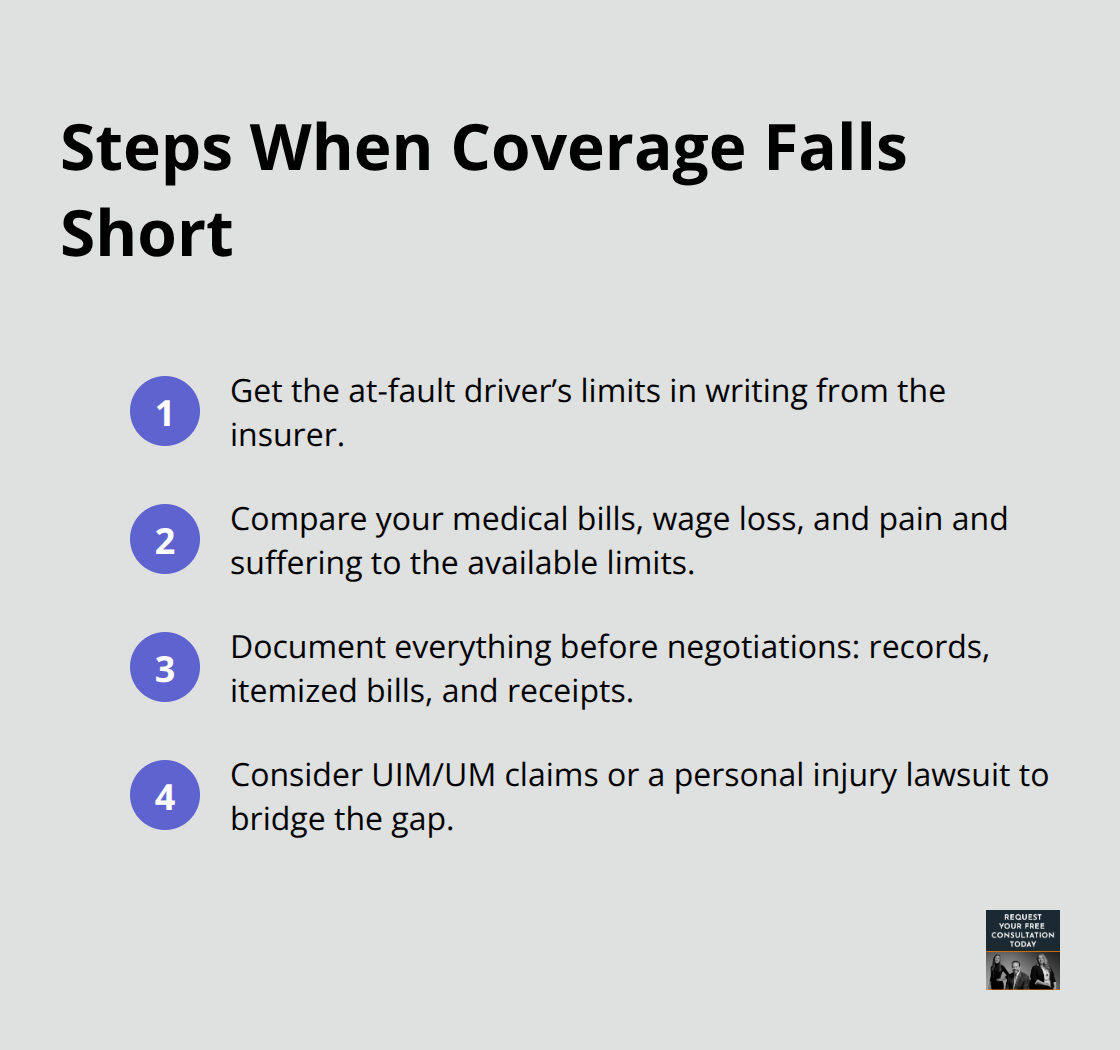

What to Do When Coverage Falls Short

Obtain the At-Fault Driver’s Insurance Information

After an accident, your first move should be obtaining the at-fault driver’s insurance information and policy details from the police report or directly from their insurer. Contact the at-fault driver’s insurance company and request their bodily injury limits in writing, not verbally. Many people accept verbal confirmations that turn out to be inaccurate when the actual policy arrives. California law requires insurers to acknowledge a claim within 15 days and respond to communications within 15 days according to Fair Claims Settlement Practices Regulations, so written requests create a documented timeline.

Compare Your Damages Against Available Coverage

Once you know the limits, compare them against your actual damages including medical bills, lost wages, and non-economic losses like pain and suffering. If the at-fault driver’s bodily injury limits fall short, immediately check your own insurance policy for uninsured or underinsured motorist coverage, which can bridge the gap up to your own policy limits.

This coverage is separate from the at-fault driver’s liability and often provides recovery when their limits prove inadequate. In Santa Cruz County, Sacramento, and Oakland, many accident victims overlook this option entirely, leaving money on the table.

Document Everything Before Settlement Discussions

When limits cannot cover your losses, document everything meticulously before settlement discussions begin. Gather complete medical records from all providers, obtain itemized bills from hospitals and clinics, and maintain receipts for all accident-related expenses. The Insurance Information Institute found that claimants who negotiated settlements received about 40% more than those accepting initial offers, which means your documentation directly influences settlement value. Never accept the insurance company’s first settlement proposal, especially when you know coverage is inadequate.

Pursue a Personal Injury Lawsuit if Necessary

If the at-fault driver’s policy limits will not cover your documented damages, you have the right to pursue a personal injury lawsuit against them individually under California law (though this requires filing within two years of the accident date per California Code of Civil Procedure §335.1). This legal action can hold the at-fault driver personally liable for damages that exceed their insurance limits. In Santa Cruz County, the legal team at Schaar & Silva LLP can help you evaluate coverage gaps, negotiate with insurers, and determine whether additional legal action is necessary to recover fair compensation.

Final Thoughts

Bodily injury limits directly control how much compensation you recover after a car accident in Santa Cruz County, Sacramento, or Oakland. California’s minimum required limits of $15,000 per person and $30,000 per accident often fall short when medical bills, lost wages, and pain and suffering mount up. Understanding these limits before an accident occurs helps you assess whether the at-fault driver carries adequate coverage and whether your own uninsured or underinsured motorist coverage can bridge any gaps.

The most important action you can take is documenting your damages thoroughly from the moment the accident happens. Gather medical records, obtain itemized bills, and maintain a timeline of your injuries and expenses. Research shows that claimants who negotiated settlements received about 40% more than those accepting initial offers, which means your documentation directly influences what you recover.

When bodily injury limits fall short of your actual losses, you have options beyond accepting what the insurance company offers. Your own uninsured or underinsured motorist coverage may provide additional recovery, or you may pursue a personal injury lawsuit against the at-fault driver personally to hold them liable for damages exceeding their policy limits. Contact us to discuss your case and learn how we can help you recover what you deserve.