After a car accident, you face a critical decision: settle your claim or take it to court. Each path has different timelines, costs, and outcomes that directly affect your recovery.

At Schaar & Silva LLP, we help accident victims in Santa Cruz County, Sacramento, and Oakland understand their auto accident settlement options so they can make informed decisions about their future.

Settlement or Trial: Which Path Makes Sense for Your Situation

Most accident victims settle their claims without going to trial, and for good reason. Roughly 95 percent of personal injury cases resolve through negotiation rather than courtroom litigation. A negotiated settlement gives you control over the outcome, predictable timing, and the ability to move forward with your life on your own terms. You know exactly what you’ll receive and when you’ll receive it.

Trial, by contrast, introduces uncertainty. A jury decides your fate, and while verdicts can exceed settlement offers, they can also fall short of your expectations.

When Settlement Makes the Most Sense

Settlement typically resolves faster than trial, often within months rather than years. Insurance companies prefer settlements because they avoid the publicity and unpredictability of court. When you negotiate directly with an insurer through a demand letter and counteroffers, you maintain leverage without the expense of expert witnesses, depositions, and trial preparation. This approach works especially well when liability is clear and your damages are well-documented. If a police report shows the other driver caused the accident, your medical records support your injuries, and your lost wages are straightforward to calculate, settlement negotiations can move quickly.

The costs are significantly lower too. Trial expenses in California can reach tens of thousands of dollars when you factor in court filing fees, expert testimony, and attorney time. Settlement typically costs a fraction of that amount. Most accident victims in Sacramento, Oakland, and Santa Cruz County find that settling within six to twelve months allows them to access compensation faster and avoid prolonged stress.

When Trial Becomes the Right Choice

Trial makes sense when the insurance offer falls dramatically short of what your case is worth. If an insurer’s settlement proposal ignores your future medical needs, undervalues your pain and suffering, or fails to account for your lost earning capacity, going to court may yield substantially higher compensation. Insurance companies use valuation software like Colossus to calculate claim values, and these tools frequently underestimate non-economic damages like loss of companionship or emotional distress.

A skilled attorney can challenge these low offers by presenting compelling evidence that demonstrates the full scope of your losses. Trial also becomes necessary when liability itself is disputed. If the other driver claims you were partially at fault, or if multiple parties share responsibility, a jury determination may be the only way to establish clear liability and recover damages. Additionally, cases involving severe injuries, permanent disabilities, or wrongful death often warrant trial preparation because the stakes are high enough to justify the time and expense.

Building Pressure Through Trial Readiness

Going to trial signals to insurers that you take your claim seriously, which frequently leads to better settlement offers even before trial begins. Many cases settle during trial preparation when insurers realize you have solid evidence and genuine trial readiness. Your attorney’s willingness to invest in expert witnesses, medical documentation, and courtroom strategy demonstrates that you won’t accept inadequate compensation. This preparation phase often proves more valuable than the trial itself, as insurers recognize the strength of your position and adjust their offers accordingly. The decision between settlement and trial ultimately depends on your specific circumstances, the strength of your case, and how much time and emotional energy you’re willing to invest. Understanding how insurance claims actually work in California will help you evaluate which path aligns with your situation.

How Insurance Claims Work in California

California’s pure comparative negligence rule allows you to recover damages even if you share fault, but your compensation reduces by your percentage of responsibility. If you’re 20 percent at fault for a collision, you recover 80 percent of your total damages. This differs sharply from states with contributory negligence rules that bar recovery entirely if you share any fault. The police report establishes initial liability, but insurers conduct their own investigations using accident reconstruction, medical records, and witness statements.

Fault Determination and Liability

Fault determination directly affects your settlement value because insurers won’t offer full compensation if they believe liability is split. Dashcam footage and eyewitness testimony become critical evidence here. If you have clear proof the other driver violated traffic laws or caused the accident through negligence, your negotiating position strengthens immediately. Strong documentation from the accident scene-photos of vehicle damage, road conditions, and weather-supports your liability claim. The other driver’s insurance company will scrutinize every detail, so thorough evidence collection at the scene matters enormously.

Understanding Insurance Coverage Limits

Insurance coverage limits cap what you receive from the at-fault driver’s policy. A typical California bodily injury limit might be $15,000 per person and $30,000 per accident, though many drivers carry $50,000 or $100,000 limits. These limits create a hard ceiling on recovery from that insurer. If your damages exceed the policy limit, you pursue underinsured motorist coverage through your own policy or file against the at-fault driver’s personal assets, which rarely produces results.

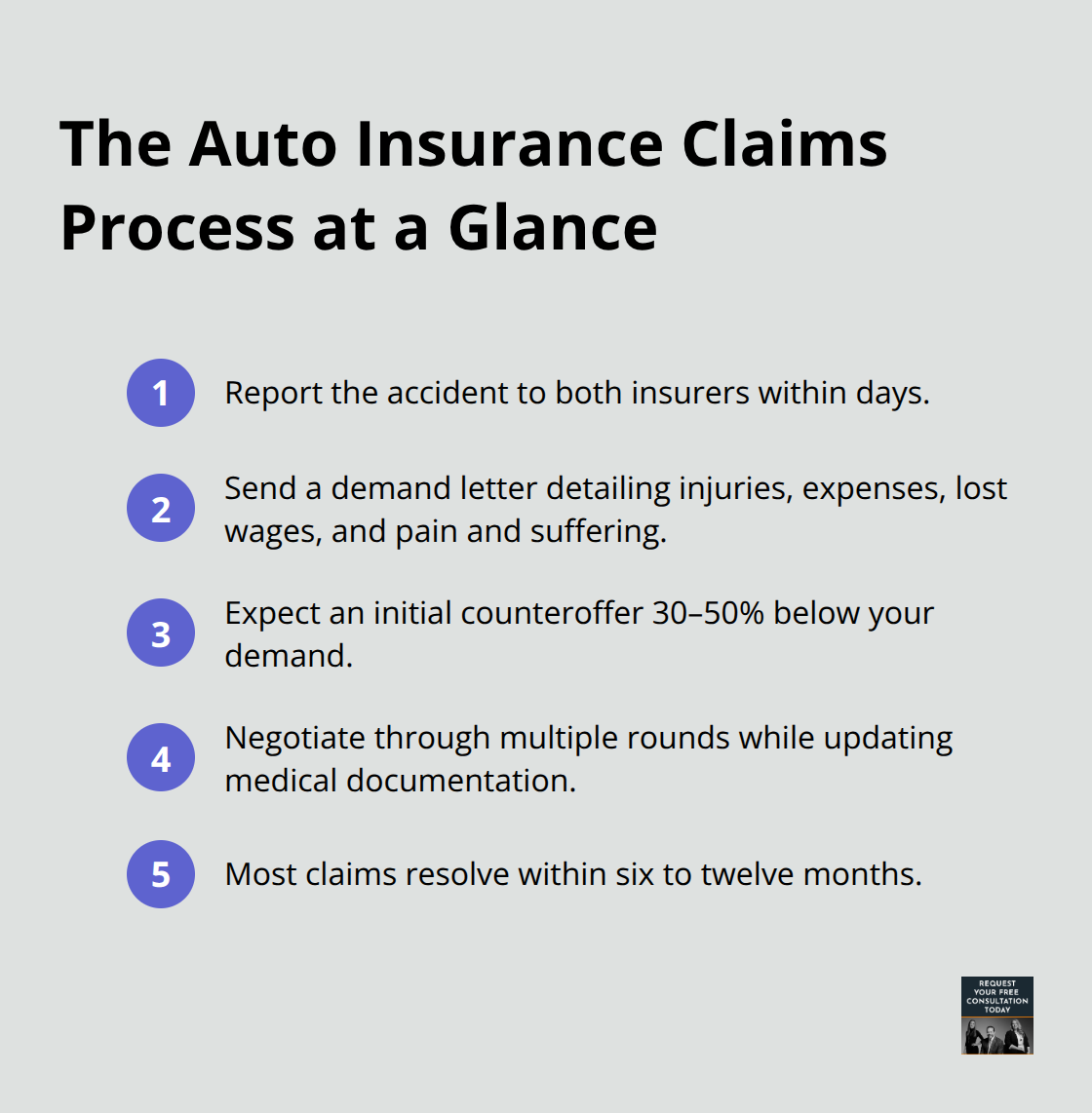

The Claims Process from Start to Finish

The claims process begins when you report the accident to your insurer and the other driver’s insurer within days of the incident. Your attorney sends a demand letter outlining your injuries, medical expenses, lost wages, and pain and suffering damages. The insurer responds with a counteroffer, typically 30 to 50 percent below your demand. Multiple rounds of negotiation follow as you provide updated medical records and documentation of ongoing treatment.

Most claims resolve within six to twelve months through this exchange.

California’s two-year statute of limitations for personal injury claims creates urgency-waiting longer than necessary weakens your position because evidence fades and witnesses become harder to locate. The strength of your documentation (medical records, wage statements, accident reports) directly influences how quickly insurers move toward fair offers. Understanding these mechanics helps you recognize when an insurer’s proposal falls short of what your case truly warrants, which brings us to the specific factors that determine your settlement amount.

Factors That Affect Your Settlement Amount

Your settlement amount depends on three concrete categories of damages, and understanding how insurers calculate each one reveals where you can strengthen your claim.

Medical Expenses and Future Care Costs

Medical expenses form the foundation of every settlement calculation. You must document every cost: emergency room visits, specialist consultations, imaging studies, physical therapy sessions, and prescribed medications. California courts recognize both past medical expenses and projected future care costs. If you suffered a spinal injury requiring ongoing physical therapy for two years, your settlement should include those anticipated treatment expenses with supporting documentation from your physician.

Request detailed medical records showing diagnoses, treatment plans, and provider recommendations for future care. Insurers frequently lowball medical damage estimates by ignoring long-term rehabilitation needs or assuming you will stop treatment sooner than medically necessary. Counter this by obtaining a life-care plan from a medical professional that itemizes all anticipated expenses, from surgeries to home modifications for mobility assistance.

Lost Wages and Income Loss

Lost wages and diminished earning capacity represent the second major damage category. You should gather recent pay stubs, tax returns, and employer statements confirming your income before the accident. If your injuries prevent you from returning to your previous job, calculate the difference between what you earned before and what you can reasonably earn now.

A construction worker who sustained a shoulder injury may never regain full strength, permanently reducing earning potential. Quantify this loss over your remaining working years with help from a vocational rehabilitation expert. Insurers resist these calculations because they represent substantial long-term costs, but solid documentation with expert support makes them difficult to dispute.

Pain and Suffering Damages

Pain and suffering damages compensate for physical pain, emotional distress, and lost quality of life. California imposes no statutory caps on non-economic damages in most personal injury claims, which means settlements can reflect genuine losses. The challenge lies in proving these subjective damages with objective evidence.

You should maintain a detailed injury journal documenting daily pain levels, activities you can no longer perform, sleep disruption, and relationship impacts. Medical records noting pain management prescriptions, therapy visits, and functional limitations strengthen these claims considerably. Insurance software like Colossus typically applies a multiplier to medical expenses, usually between 1.5 and 5 times the medical costs, but this formula frequently undervalues severe trauma cases.

Compelling narratives and testimony about how your injuries affected your life often persuade insurers and juries far more effectively than formulas alone. If you required hospitalization for an extended period before death in a wrongful death case, the decedent’s pre-death pain and suffering becomes recoverable, sometimes adding hundreds of thousands to settlements.

Final Thoughts

Your decision between settlement and trial shapes your recovery timeline, costs, and ultimate compensation. If liability is clear, your damages are well-documented, and the insurer’s offer reflects your actual losses, settlement provides faster resolution and lower expenses. Most accident victims in Santa Cruz County, Sacramento, and Oakland resolve their auto accident settlement options this way within six to twelve months. However, if the offer significantly undervalues your medical needs, lost earning capacity, or pain and suffering, trial preparation often pressures insurers into better settlements even before courtroom proceedings begin.

Insurance companies rely on software and formulas that frequently underestimate non-economic damages and long-term consequences. An attorney who understands California’s pure comparative negligence rules, coverage limits, and damage calculations identifies where insurers fall short and builds compelling evidence to support higher compensation. We at Schaar & Silva LLP help accident victims throughout Santa Cruz County evaluate their options and determine which path aligns with their specific circumstances.

Gather your accident documentation, medical records, and wage statements, then contact an attorney who can honestly assess your case value. Don’t accept the first settlement offer without understanding how it was calculated-request detailed breakdowns and provide updated medical costs to support higher demands. Contact Schaar & Silva LLP to discuss your situation and determine the best path forward for your recovery.