A car accident can leave you facing medical bills that quickly spiral out of control. Your insurance policy’s bodily injury limits in California determine how much your insurer will pay toward those expenses.

We at Schaar & Silva LLP have seen countless clients discover their coverage falls short when they need it most. This guide walks you through what these limits mean for your claim and how to protect yourself.

What Bodily Injury Limits Actually Mean

Understanding the Basics

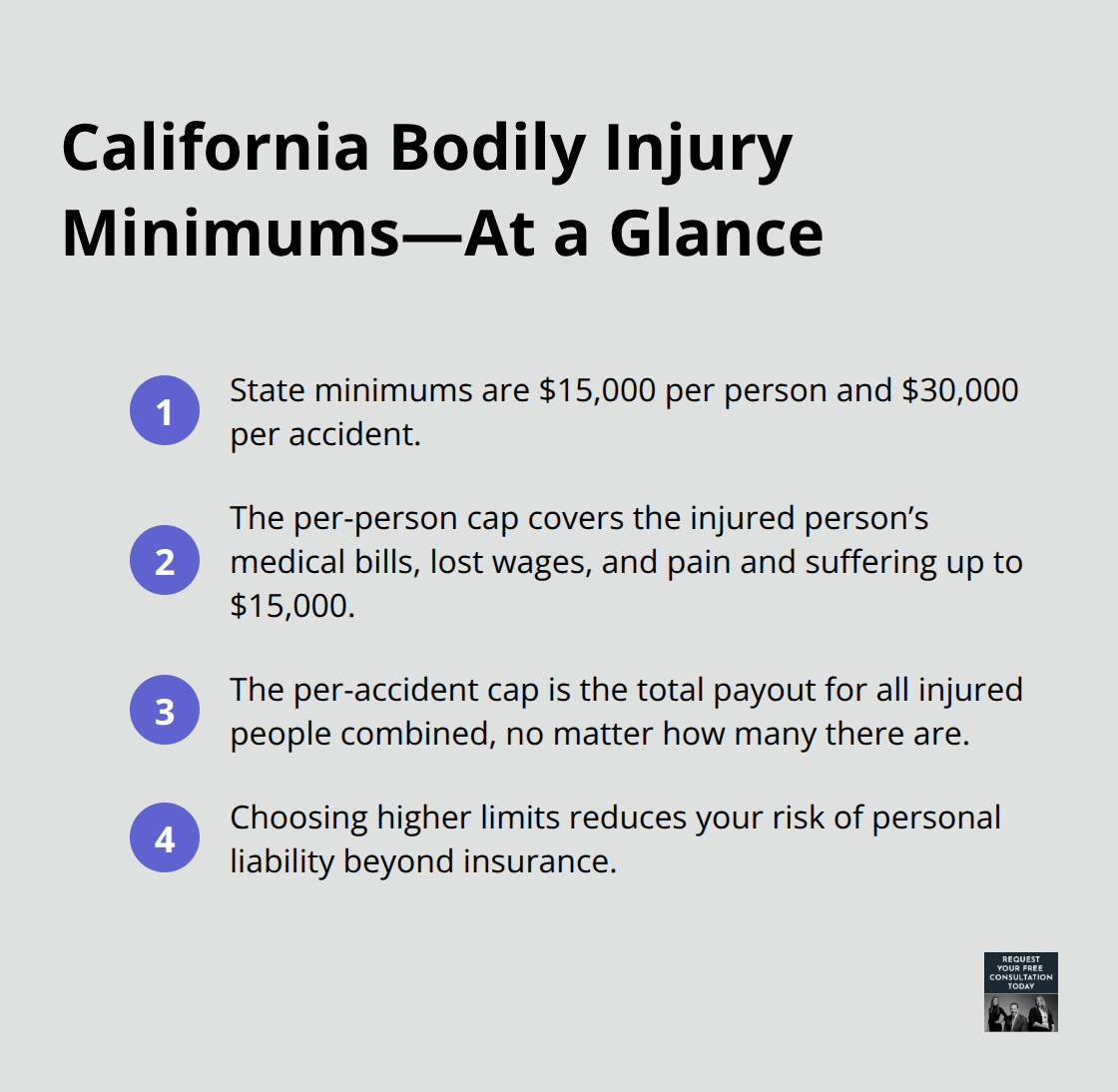

Bodily injury limits set a ceiling on what your auto insurance will pay for injuries you cause to other people in an accident. California law requires every driver to carry a minimum of $15,000 per person and $30,000 per accident, according to California Vehicle Code Section 16020. If you injure one person, your policy covers up to $15,000 of their medical bills, lost wages, and pain and suffering. If multiple people are hurt, the total payout cannot exceed $30,000 no matter how many victims exist.

Why Minimums Leave You Exposed

These minimums are dangerously low. A single hospital visit for a serious injury can exceed $15,000 in days. An overnight stay in intensive care, surgery, and follow-up treatment will blow past these limits quickly. Many drivers in Santa Cruz County, Sacramento, and Oakland operate with only these minimum limits, which means they face personal liability if damages exceed the policy cap.

How Your Own Coverage Works

Your own bodily injury coverage works differently than you might think. If you purchase higher limits like $100,000 per person and $300,000 per accident, those numbers protect you when someone else’s insurance is insufficient or they have no insurance at all. This is where uninsured and underinsured motorist coverage becomes critical. If an at-fault driver has only the $15,000 minimum and your injuries total $50,000 in medical bills, your own underinsured motorist coverage can bridge that gap up to your policy limits.

Medical Payments Coverage vs. Bodily Injury Liability

Many people confuse bodily injury liability with medical payments coverage. Medical payments coverage on your own policy pays your medical expenses regardless of who caused the accident, up to limits like $2,000 on basic plans or $5,000 on standard plans. Bodily injury liability, by contrast, is what you owe to others for injuries you cause. These are separate coverages with separate limits, and both matter for different reasons.

When your injuries exceed what the at-fault driver’s bodily injury limits will cover, your next step involves understanding whether your own policy can fill the gap-and that’s where the claim process becomes more complex.

When Your Medical Bills Exceed What Insurance Will Pay

The Gap Between Damages and Coverage

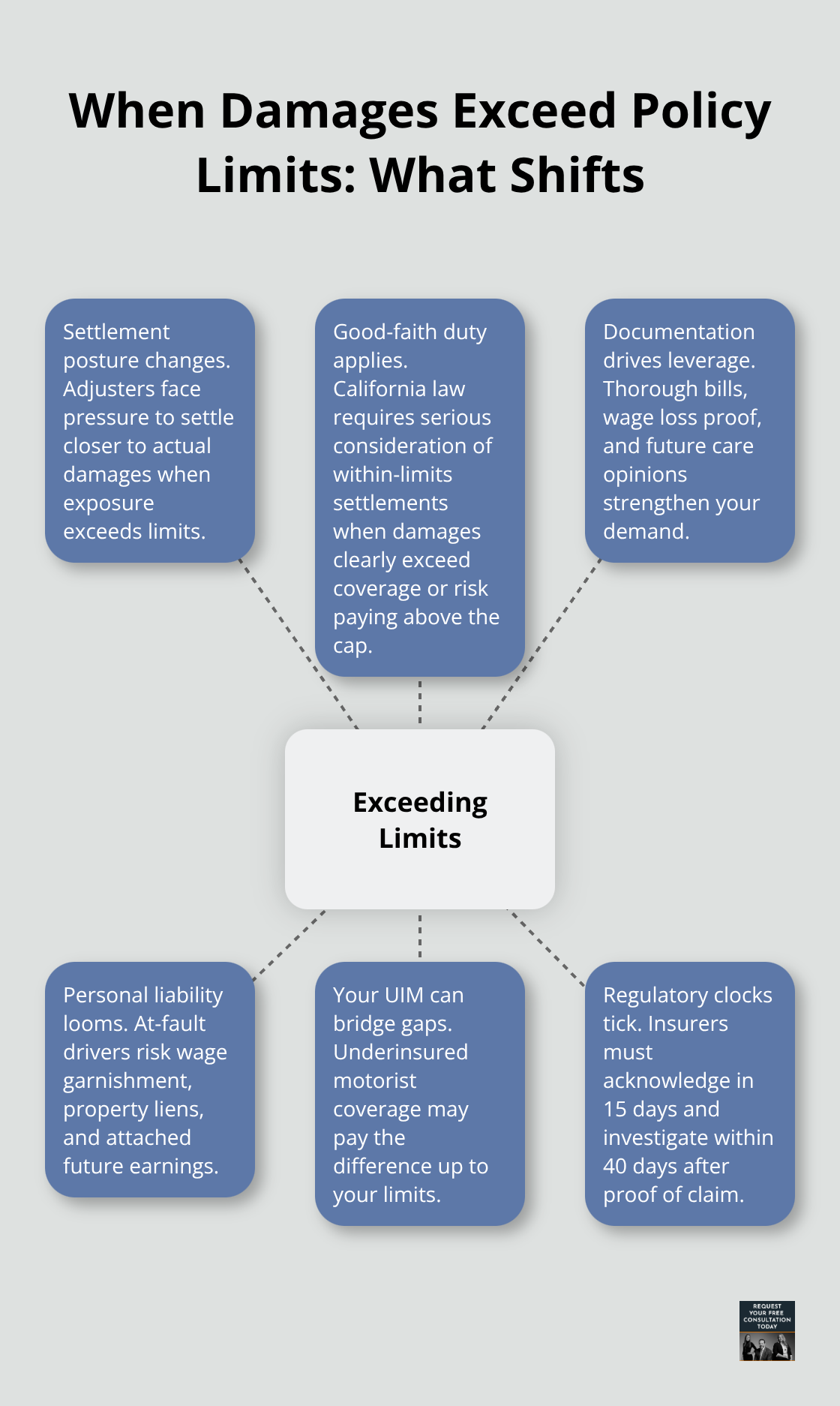

Once medical expenses climb above the at-fault driver’s bodily injury limits, your claim enters dangerous territory. A serious injury requiring surgery, hospitalization, and months of physical therapy can easily reach $75,000 or $100,000 in medical costs alone. If the at-fault driver carries only California’s $15,000 minimum per person, you face a $60,000 to $85,000 gap that someone must cover. The at-fault driver becomes personally liable for that difference, which means a judgment could attach their wages, home, and future earnings.

How Insurers Respond to Excess Damages

This reality changes how insurance companies approach settlement negotiations. When an adjuster realizes the potential judgment far exceeds the policy limit, they face pressure to settle closer to your actual damages rather than hide behind the minimum coverage.

Insurers handling claims in Santa Cruz County, Sacramento, and Oakland often shift their settlement posture once they understand the plaintiff’s damages documentation is thorough and the at-fault driver’s personal assets are at risk.

The insurer’s duty of good faith and fair dealing, established in California case law including Crisci v. Security Ins. Co., requires them to seriously consider settlements within policy limits when damages clearly exceed those limits. Refusing a reasonable settlement offer can expose the insurer to paying a judgment that goes beyond the policy cap. This means your settlement leverage increases substantially when you can demonstrate medical bills, lost wages, and pain and suffering totaling more than the available coverage.

Documentation as Your Strongest Tool

Documentation becomes your most powerful tool in these negotiations. Medical records from every treatment provider, itemized bills showing the actual charges, pay stubs proving lost income, and expert opinions on future medical needs all strengthen your position. An insurer reviewing a demand letter with $80,000 in documented medical expenses against a $15,000 policy limit cannot reasonably deny the claim or lowball the offer without risking a bad faith finding.

Real settlements in your region reflect this dynamic. A pedestrian struck in Sacramento with $50,000 in orthopedic surgery and rehabilitation costs against a $30,000 minimum policy typically settles for the full policy limit plus negotiated amounts from the at-fault driver’s other assets or payment plans. A multi-car collision in Santa Cruz involving three injured parties and a total of $120,000 in medical expenses against a $30,000 per-accident limit forces difficult allocation decisions, but the insurer must address each claim fairly or face litigation.

Regulatory Timelines and Your Advantage

The Fair Claims Settlement Practices Regulations require insurers to acknowledge your claim within 15 days and complete their investigation within 40 days after you provide proof of claim, according to the California Department of Insurance. Meeting these deadlines keeps pressure on the insurer to move toward settlement rather than delay.

Your own underinsured motorist coverage becomes critical in these scenarios. If you purchased $100,000 per person limits on your policy, that coverage can pay you the difference between what the at-fault driver’s policy covers and your actual damages, up to your UIM limit. Without that coverage, you must pursue the at-fault driver personally, which is often costly and time-consuming. The choice to carry higher bodily injury limits on your own policy is not about protecting others-it protects you when someone underinsured or uninsured causes your injury. Understanding how your own coverage interacts with the at-fault driver’s limits determines whether you recover fully or face significant out-of-pocket losses.

Why Higher Coverage Limits Matter More Than You Think

The Real Cost of Minimum Coverage

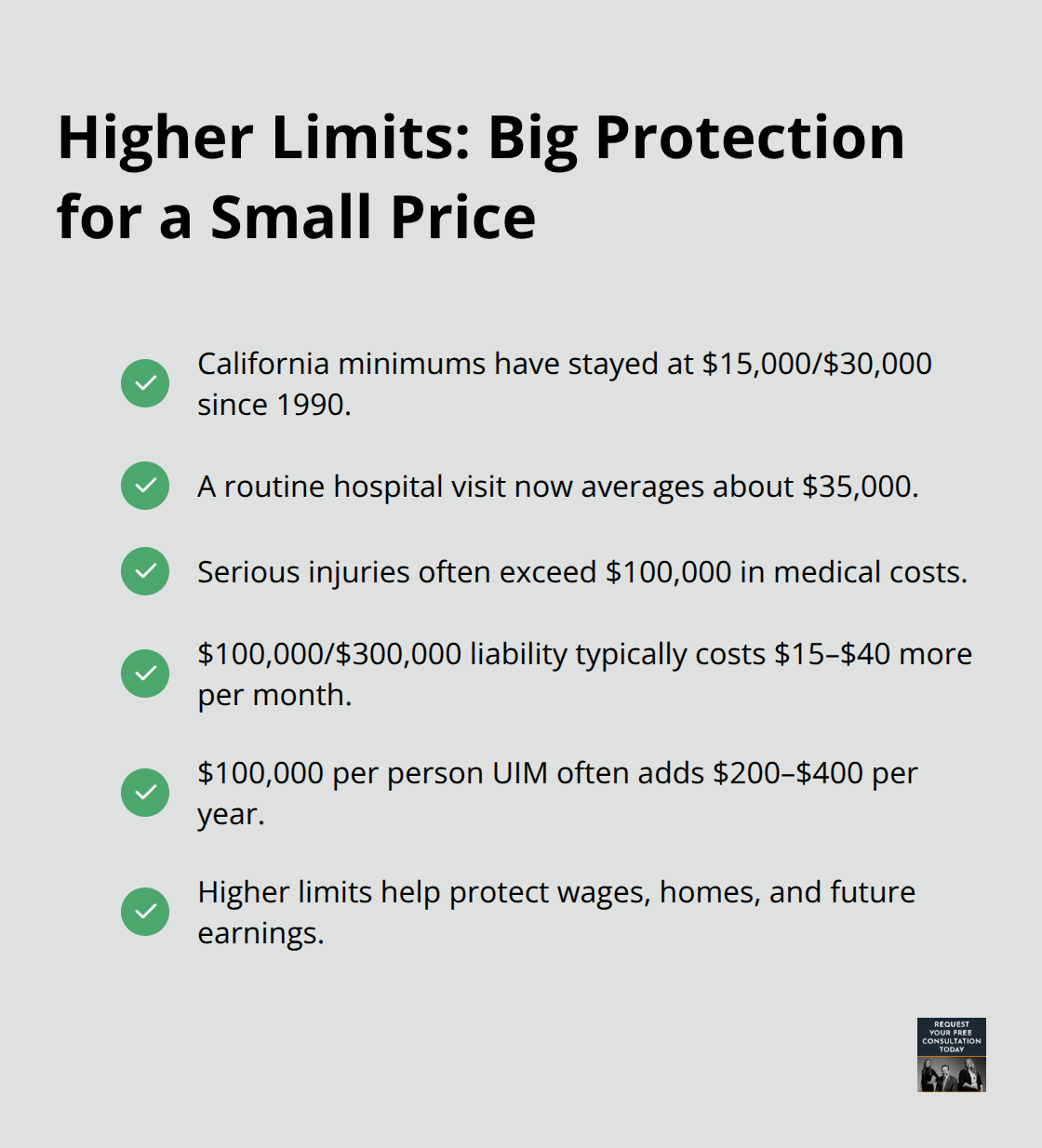

California’s minimum bodily injury limits of $15,000 per person and $30,000 per accident have remained unchanged since 1990, according to state law. Medical costs have skyrocketed in that time. A routine hospital visit now averages $35,000, and serious injuries requiring surgery or extended care push well beyond $100,000. Carrying minimum limits in 2026 leaves you essentially unprotected. If you cause an accident and injure someone seriously, your personal assets become vulnerable to judgment once your policy limit runs out. The at-fault driver’s wages face garnishment, their home can face a lien, and their future earnings can be attached for years.

Affordable Protection Through Higher Limits

Standard coverage limits of $100,000 per person and $300,000 per accident cost only marginally more in premiums than minimums-typically $15 to $40 more per month depending on your age, driving record, and location. For someone in Sacramento, Oakland, or Santa Cruz County, this difference is negligible compared to the protection it provides. Higher limits also improve your negotiating position in settlement talks because insurers know the realistic damages and cannot hide behind inadequate coverage.

Protecting Yourself as an Injured Party

Your own bodily injury coverage decisions matter equally when you are the injured party. If you carry only $15,000 in uninsured or underinsured motorist coverage and an at-fault driver with minimum limits injures you, you absorb the gap yourself. Purchasing $100,000 per person limits on your own policy costs approximately $200 to $400 annually more than minimums but protects you against underinsured drivers (a significant portion of accidents in California). Without that coverage, you must pursue the at-fault driver personally, which is often costly and time-consuming.

Calculating Your Coverage Needs

To evaluate the right coverage amount, calculate your household income, assets, and potential liability exposure. If you own a home or have substantial savings, your exposure is higher and justifies $250,000 to $500,000 in bodily injury limits. If you have minimal assets, $100,000 per person still makes financial sense given the low premium cost.

Making Changes to Your Policy

Adjusting your policy takes minutes. Contact your insurance agent or log into your online account, locate the bodily injury liability section, and increase the per-person and per-accident limits. Most insurers allow changes effective immediately or within a few days. Do not wait for renewal; coverage gaps exist the moment you drive without adequate protection. Document the changes in writing and keep confirmation emails for your records. If you have questions about how limits interact with your specific situation, we at Schaar & Silva LLP can review your policy and help you understand your protection level.

Final Thoughts

Bodily injury limits in California set the boundary between adequate protection and financial devastation after an accident. The state’s minimum of $15,000 per person and $30,000 per accident has not changed since 1990, while medical costs have tripled, leaving drivers who carry only minimums exposed to personal liability judgments. Standard coverage at $100,000 per person and $300,000 per accident costs just $15 to $40 more monthly and shields your wages, home, and future earnings from attachment.

When medical expenses exceed the at-fault driver’s bodily injury limits, settlement negotiations shift in your favor because insurers face pressure to settle closer to your documented damages rather than hide behind insufficient coverage. Documentation of medical bills, lost wages, and expert opinions on future care becomes your strongest negotiating tool, and California’s good faith requirements apply pressure on insurers to move quickly toward fair resolution. Your own uninsured and underinsured motorist coverage matters equally when an underinsured driver injures you, as it bridges the gap between their inadequate limits and your actual damages.

We at Schaar & Silva LLP help clients navigate these coverage complexities every day in Santa Cruz County, Sacramento, and Oakland. If you have been injured in an accident and face questions about coverage, settlement negotiations, or whether you can recover beyond policy caps, contact us for a free evaluation. Do not wait until after an accident to address these gaps.