A vehicle crash in Santa Cruz can leave you facing unexpected costs and confusion about what comes next. Property damage claims involve complex rules, and insurance companies don’t always offer fair settlements on the first try.

We at Schaar & Silva LLP help accident victims understand their rights and recover what they’ve lost. This guide walks you through valuing your damage, navigating insurance, and knowing when legal support makes a real difference.

What Happens to Your Vehicle After a Santa Cruz Crash

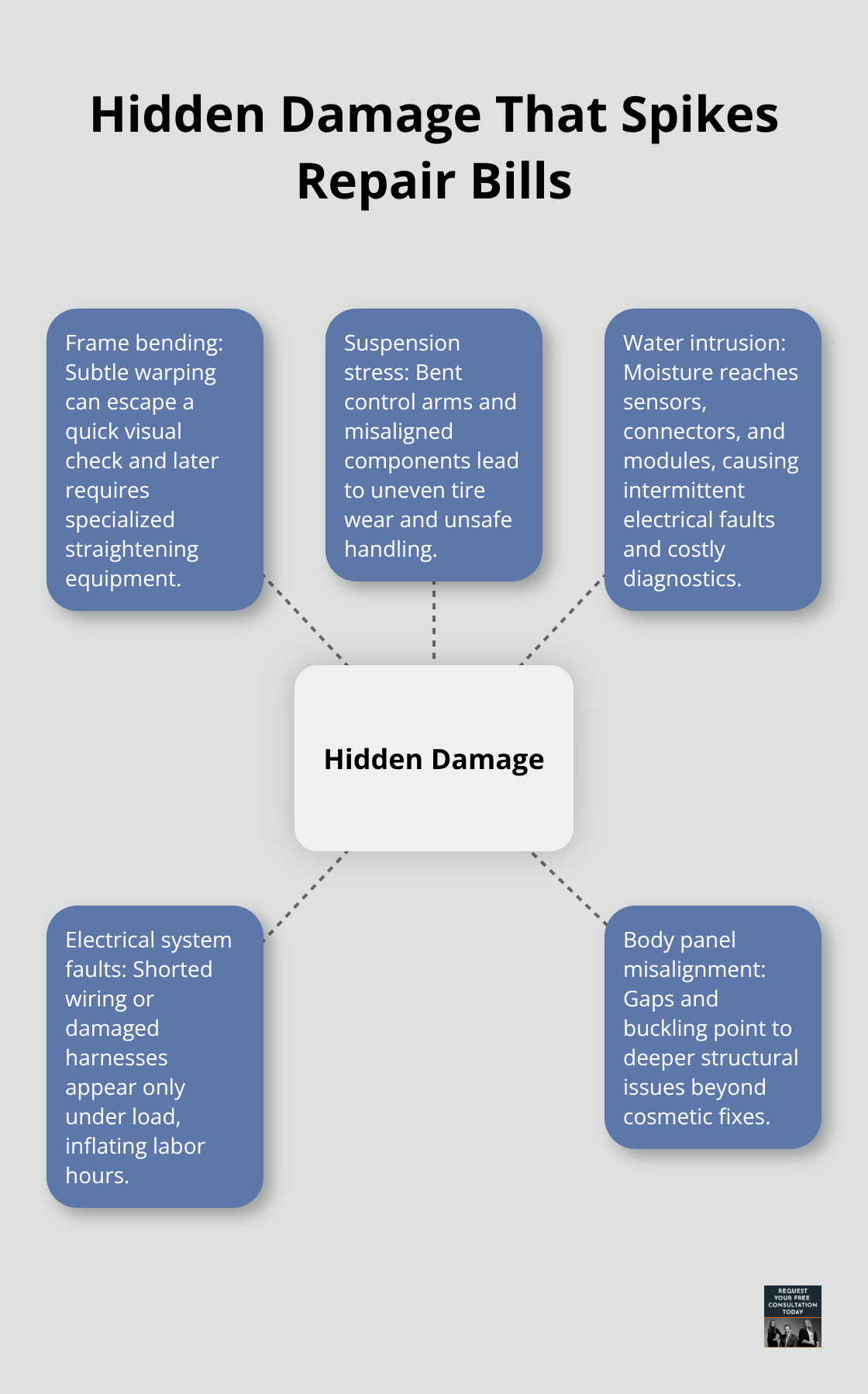

Vehicle damage in Santa Cruz crashes ranges from minor cosmetic harm to structural destruction that renders a car unsafe. The type and severity of damage determine whether repairs are economical or the vehicle should be declared a total loss. Common damage includes bent frames, crushed bumpers and doors, broken glass, suspension misalignment, and paint damage. Hidden damage-frame bending, suspension component stress, water intrusion into electrical systems-often remains undetected during a quick adjuster inspection and can add $5,000 to $10,000 to repair bills later. A full pre-repair mechanical assessment costs $200 to $400 but frequently saves thousands by identifying problems before work begins.

Document the Scene Before Moving the Vehicle

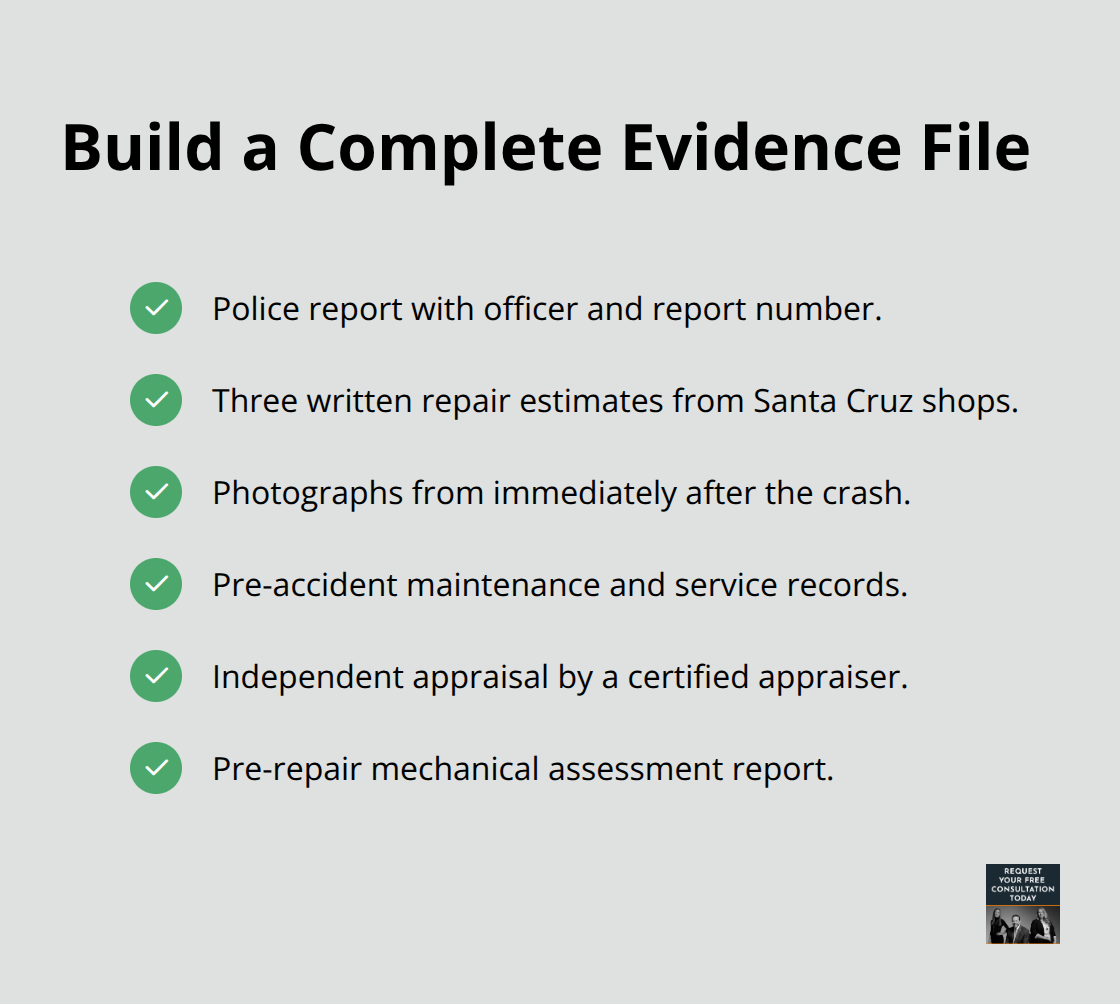

Photograph your vehicle immediately after the crash from multiple angles, capturing both wide shots and close-ups of all damaged areas. Take 15 to 20 images in daylight if possible; if the crash occurred at night, return the next morning to photograph road conditions and vehicle position. Include the interior if safe to do so, showing any damage to seats, dashboard, or personal items. Obtain the police report within 48 hours and record the officer’s name, badge number, and report number. Collect independent witness statements and contact information. These steps create a factual record that insurers cannot easily dismiss and establish a baseline for what your vehicle looked like before damage.

Three Repair Estimates Outperform One Adjuster’s Offer

Insurance companies in Santa Cruz rely heavily on NADA Guides, which systematically underestimate local labor rates and parts costs by roughly $2,000 to $5,000 compared with actual shop pricing. Obtain three written repair estimates from licensed Santa Cruz shops with no financial ties to your insurer. Kraft’s Body Shop and similar local operations provide itemized estimates that break down labor, parts, and paint separately. Present these estimates to the adjuster at the inspection. The gap between the adjuster’s initial offer and your three local estimates reveals the true Santa Cruz market price for repairs. This documentation shifts negotiations away from generic national databases toward concrete local evidence.

Challenge Total Loss Valuations with Independent Appraisals

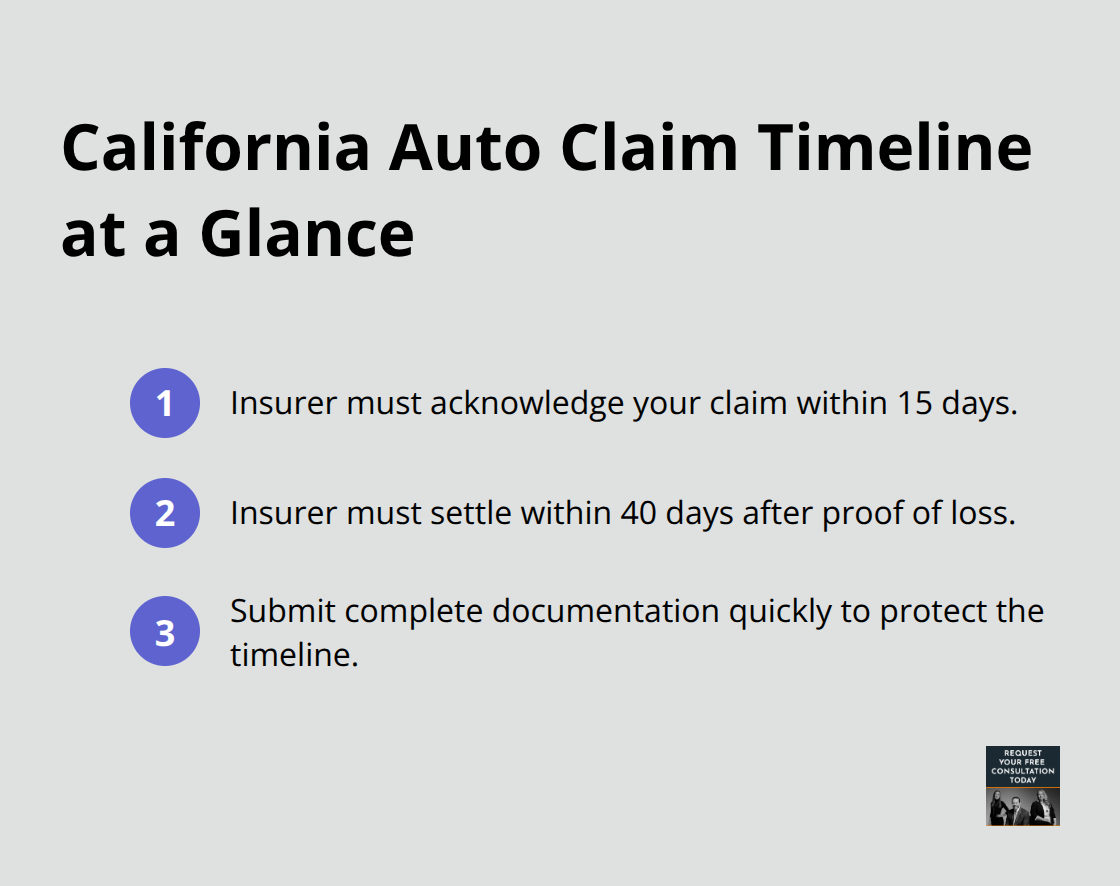

If your vehicle is declared a total loss, insurers pay depreciated value minus salvage. Challenge this valuation with an independent appraisal costing $300 to $600. A certified appraiser documents pre-accident condition, assesses frame straightness and electrical systems, and compares your vehicle to local market comps. This appraisal often justifies a $2,000 to $5,000 increase in the payout. California Department of Insurance rules require insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, so timely, thorough documentation keeps pressure on the timeline.

Negotiation Requires Multiple Rounds and Strong Evidence

The initial offer is almost never final-it functions as an opening position. Negotiation requires multiple rounds, and pushback grounded in three estimates and an appraisal yields measurably better results than passive acceptance. Insurance adjusters expect early settlement; the first offer often leaves $2,000 to $5,000 on the table. Build your negotiation strategy around concrete evidence. A comprehensive written submission that includes the three estimates, mechanical inspection report, independent appraisal, and pre-accident records creates leverage to shift the adjuster’s position higher. When negotiations stall or the insurer remains far from fair value, consulting a law firm becomes the next logical step to evaluate your options for recovering the full property damage loss.

How Insurance Companies Value Your Vehicle After a Crash

The Adjuster’s One-Hour Inspection Sets Your Valuation

Insurance adjusters in Santa Cruz follow a mechanical process that often undervalues what your vehicle is actually worth. They conduct a one-hour inspection of structural, paint, and mechanical damage, then enter your vehicle’s details into NADA Guides or Kelley Blue Book to generate a baseline valuation. The problem is that these national databases don’t account for Santa Cruz’s higher labor rates and parts costs. According to NADA Guides themselves, local market variations create gaps of $2,000 to $5,000 between what the database suggests and what Santa Cruz shops actually charge. The adjuster’s inspection report drives everything that follows, so if the initial assessment misses hidden damage or mischaracterizes your vehicle’s condition, the entire valuation suffers.

Hidden Damage Emerges After the Adjuster Leaves

A full pre-repair mechanical assessment before the adjuster leaves your property matters far more than most people realize. A licensed technician identifies frame straightness issues, suspension stress, and water intrusion that a 60-minute visual inspection will never catch. When hidden problems emerge later during repairs, you’re fighting with the insurer to cover costs they should have anticipated, and that fight costs time and money. The inspection costs $200 to $400 but frequently saves thousands by identifying problems before work begins.

Actual Cash Value Determines What You Receive

Insurance companies pay Actual Cash Value after a total loss-the depreciated value of your vehicle based on age, mileage, condition, and market comps, minus salvage value. The California Department of Insurance requires insurers to acknowledge your claim within 15 days and settle within 40 days after you provide proof of loss, but meeting that timeline depends entirely on how quickly you submit documentation. If you wait three weeks to gather estimates and photos, you’ve already burned half your settlement window.

Errors in Your Vehicle’s Details Tank Your Valuation

The insurer’s valuation report should list your exact VIN, mileage, year, trim, and options; errors in any of these fields artificially depress your value. Common mistakes include wrong mileage entries, incorrect model trim designation, or mischaracterization of your vehicle’s pre-accident condition. Challenging these errors requires concrete evidence-local market comps showing what similar vehicles actually sold for in Santa Cruz County, documentation of upgrades or aftermarket parts (new tires, leather seats), and service records proving your vehicle was well-maintained.

Appraisal Provisions Offer a Path Forward When Negotiations Stall

If negotiations stall after you’ve submitted three independent repair estimates and an independent appraisal, California’s Appraisal Provision allows you to demand binding appraisal with a neutral third party. This process costs hundreds of dollars and extends your timeline by weeks, but it shifts control away from the adjuster’s initial position toward an independent assessment. Understanding how insurers construct their valuations-and where those valuations fail to reflect Santa Cruz’s actual market-positions you to challenge lowball offers with evidence rather than emotion. The next section examines the specific documentation and evidence you need to build that challenge.

Building Your Case with Documentation and Support

Organize Your Evidence Into a Single Chronological File

The gap between what an insurance adjuster offers and what your vehicle damage actually costs to repair widens when you lack organized, credible documentation. Create a single chronological file that contains the police report, all three repair estimates from Santa Cruz shops, photographs from immediately after the crash, pre-accident maintenance records, and any independent appraisal. This file becomes your negotiating foundation. The California Department of Insurance requires insurers to acknowledge your claim within 15 days and settle within 40 days after you provide proof of loss, so submitting a complete package early keeps pressure on the timeline. Many people lose thousands by submitting incomplete documentation piecemeal over weeks, which extends negotiations and weakens their position.

Submit Written Documentation, Not Verbal Explanations

Write everything down and demand written justifications from adjusters for any valuation discrepancies rather than accepting verbal explanations. When you present three independent estimates alongside your mechanical inspection report, the adjuster shifts from relying on NADA Guides toward defending their position against concrete local evidence. This forces them to justify why your Santa Cruz shop charges $3,000 more than the national database predicted. The written submission creates accountability and a traceable record that protects you if negotiations escalate.

Schedule Your Inspection After You Gather All Documentation

Working with adjusters requires persistence and specificity rather than confrontation. Schedule the inspection only after you obtain your three repair estimates and the mechanical assessment, then present all documentation at that meeting. If hidden damage emerges during repairs that the adjuster missed, photograph it immediately and submit a written supplemental claim with the new repair estimate and photos. The insurer often covers these additions once confronted with evidence rather than fighting over what should have been caught initially.

Invoke the Appraisal Provision When Negotiations Stall

If negotiations stall after multiple rounds and the adjuster refuses to move significantly closer to your three estimates and appraisal, California’s Appraisal Provision allows you to demand binding appraisal with a neutral third party. This costs hundreds of dollars and extends your timeline by weeks, but it removes the adjuster from the equation. When the insurer’s position remains far from fair value despite your documentation, consulting a law firm allows you to evaluate whether pursuing additional compensation makes financial sense.

Evaluate Your Options With Legal Support

When property damage claims involve significant losses or the insurer refuses fair settlement, legal review helps you understand your next steps. We at Schaar & Silva LLP assist in evaluating the extent of property damage and work with you to recover what you’ve actually lost rather than settling for an initial lowball offer.

Final Thoughts

Property damage Santa Cruz claims succeed when you act quickly, document thoroughly, and refuse to accept lowball offers without pushback. The three-step approach outlined in this guide-gathering independent repair estimates, obtaining a mechanical inspection, and building a comprehensive evidence file-shifts control from the adjuster’s initial position toward concrete local market data. Most people leave thousands of dollars on the table by accepting the first offer or submitting incomplete documentation, and the gap between what insurers initially offer and what your vehicle damage actually costs to repair typically ranges from $2,000 to $5,000 or more.

Moving forward after a crash means understanding that the California Department of Insurance requires insurers to acknowledge your claim within 15 days and settle within 40 days after proof of loss. Photograph damage immediately, obtain the police report within 48 hours, collect three repair estimates from Santa Cruz shops, and schedule a pre-repair mechanical assessment before the adjuster leaves your property (these steps take days, not weeks). This organized approach forms the foundation of every successful negotiation and creates real pressure on the insurer’s timeline.

When property damage claims involve significant losses or the insurer refuses fair settlement despite your documentation, legal support helps you evaluate your options. We at Schaar & Silva LLP assist in evaluating the extent of property damage and work with you to recover what you’ve actually lost. Santa Cruz County residents facing property damage claims have concrete tools and local support available-use them.