A truck crash in Santa Cruz can leave you facing overwhelming financial and physical consequences. Medical bills pile up, your vehicle needs repairs, and you might miss work while recovering.

We at Schaar & Silva LLP understand that calculating truck crash damages Santa Cruz residents are entitled to receive isn’t straightforward. This guide walks you through the types of damages available, how to document your losses, and the real obstacles you’ll face when fighting for fair compensation.

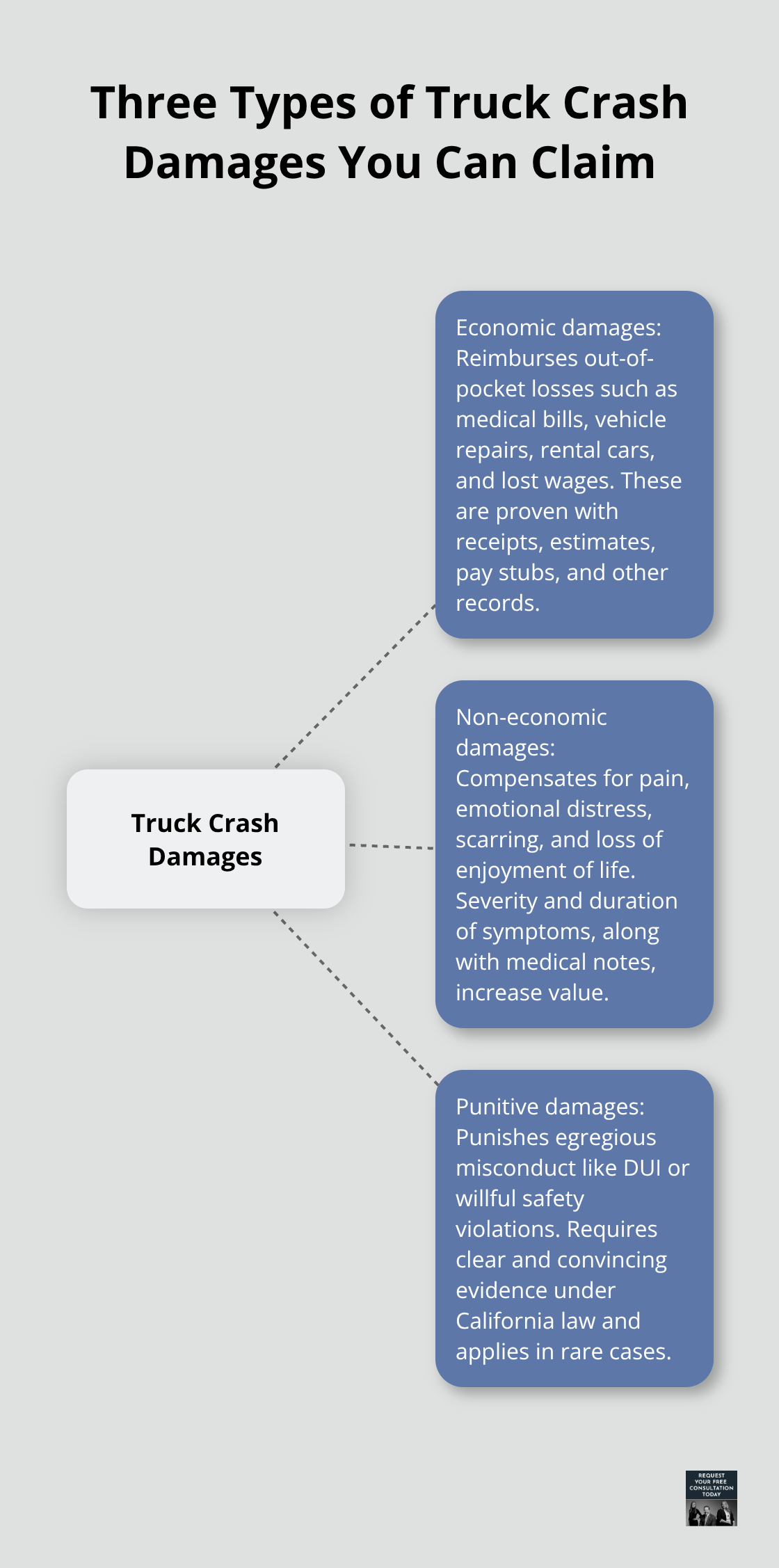

What Damages Can You Recover After a Truck Crash

When a truck crashes into your vehicle in Santa Cruz, the financial fallout extends far beyond the obvious repair bills. The law recognizes three distinct categories of damages you can pursue, and understanding each one is essential to building a strong claim. Economic damages cover your actual out-of-pocket losses, non-economic damages compensate for pain and suffering, and punitive damages punish the truck driver or company for egregious behavior. Most truck crash victims focus heavily on medical bills and car repairs, but they miss significant recovery opportunities in the other categories. This chapter explains what each damage type covers and why accuracy matters for your case.

Economic Losses You Can Quantify

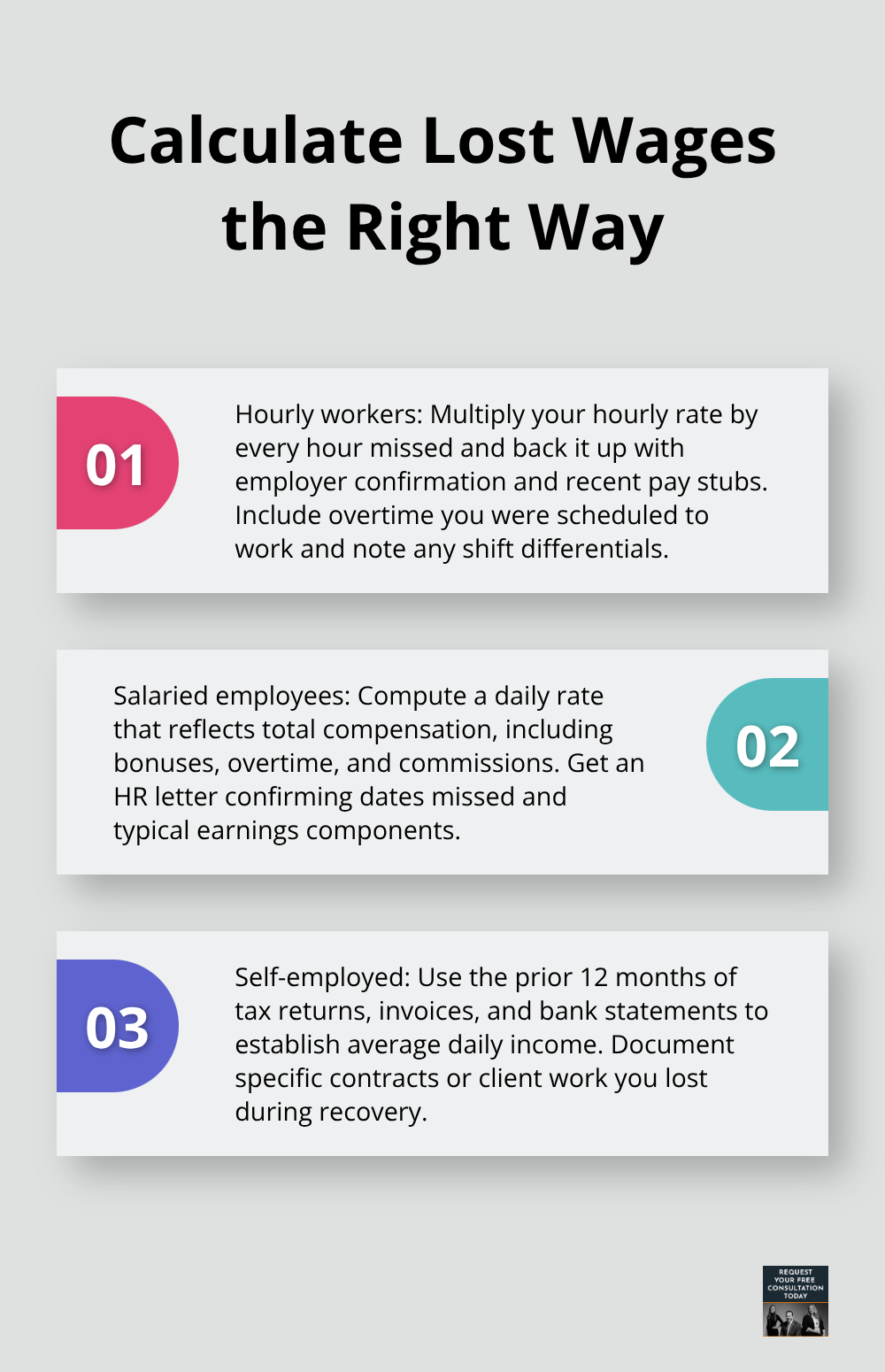

Economic damages are the straightforward financial losses you can prove with receipts, invoices, and statements. Medical expenses form the largest component for most truck crash victims-hospital bills, emergency room visits, surgery costs, physical therapy, and ongoing treatment all qualify. If the truck driver was at fault, their liability insurer should cover these bills through your claim. Lost wages represent the second major category, and this is where many people underestimate their recovery. If you missed work due to injuries, you can claim every hour or salary day you lost. For hourly workers, multiply your hourly rate by the hours missed; for salaried employees, calculate your daily rate and multiply by days away from work. Self-employed individuals can claim lost income using tax returns, invoices, and bank statements showing earnings during the recovery period. Property damage to your vehicle is straightforward-obtain repair estimates from at least two shops and submit them to the insurance adjuster. If your vehicle is totaled, the insurer must pay the fair market value minus salvage. Other economic losses include rental car costs while your vehicle is being repaired, transportation expenses, childcare costs you incurred because you couldn’t work, and medical equipment like crutches or wheelchairs. Keep every receipt and invoice related to the accident because these documents prove your economic damages.

Pain, Suffering, and Long-Term Impact

Non-economic damages compensate you for the intangible harm the truck crash caused-pain, emotional distress, lost enjoyment of life, and permanent scarring or disfigurement. Unlike medical bills, these damages lack a receipt, which makes them harder to prove but absolutely recoverable. California courts recognize that a serious truck crash can cause chronic pain, anxiety, depression, and reduced quality of life. If you required ongoing pain management, mental health treatment, or physical therapy for months after the crash, document this thoroughly with medical records and provider notes. The more severe your injuries and the longer your recovery period, the higher your non-economic damages claim. Insurance adjusters often use a multiplier method-they take your economic damages and multiply by a factor ranging from 1.5 to 5, depending on injury severity. A minor soft-tissue injury might warrant a 1.5 multiplier, while a serious broken bone requiring surgery could justify a 3 to 5 multiplier. However, this is just an insurance company calculation, not a legal requirement. In litigation, a jury can award substantially more if your injuries are severe and well-documented. Permanent scarring, loss of limb function, or chronic pain that affects your career prospects all justify higher non-economic damages.

When Punitive Damages Apply

Punitive damages are rare and only apply when the truck driver or company acted with gross negligence or intentional misconduct. These damages exist to punish the wrongdoer and deter similar behavior in the future, not to compensate you for losses. If a truck driver operated under the influence, texted while driving, or deliberately ignored mechanical failures in the truck, punitive damages might apply. California law requires clear and convincing evidence of oppression, fraud, or malice-a simple mistake or even ordinary negligence does not meet this threshold. Punitive damages are capped in California; for non-government defendants, they cannot exceed the greater of $10 million or the amount of compensatory damages multiplied by a specific factor. Most truck crash cases will not reach the punitive damages stage unless the conduct was egregious. However, if you suspect the truck driver or company engaged in reckless behavior, this conversation matters for your claim strategy and recovery potential.

Building Your Documentation Foundation

Medical records form the backbone of your truck crash claim, and you must start this process immediately after the accident. Visit your doctor within days of the crash, not weeks later, because insurance adjusters scrutinize delays and use gaps in treatment to argue your injuries weren’t serious. You should obtain copies of every medical report, test result, imaging scan, and provider note from your treatment. The California Department of Insurance requires insurers to acknowledge your claim within 15 days and respond within 15 days of receiving your proof, so completeness matters from day one.

Securing Property Damage Documentation

For property damage, you need repair estimates from at least two independent body shops before accepting any insurance offer. Many shops in Santa Cruz underestimate costs on the initial quote, so multiple estimates protect you from accepting lowball settlements. If your vehicle is totaled, the insurer must pay fair market value minus salvage; you should verify this calculation using resources like the National Automobile Dealers Association or Kelley Blue Book to challenge undervaluation. You must photograph your vehicle from multiple angles immediately after the accident, capture the accident scene with time stamps, and collect contact information and insurance details from the other driver. The Santa Cruz County Sheriff’s Office maintains a Motor Vehicle Accidents portal where you can access raw crash data and official reports, which strengthens your claim with objective third-party documentation.

Closing Documentation Gaps That Cost You Money

Documentation gaps are where insurance companies exploit truck crash victims. Self-employed individuals must gather invoices, 1099 forms, and bank statements showing lost income during recovery, not just a rough estimate of missed earnings. Salaried workers need employer confirmation letters documenting the exact days missed and an official pay stub showing your daily rate. For hourly workers, you should obtain a written statement from your employer confirming hours missed multiplied by your hourly wage. Medical Examiner data from Santa Cruz County can support claims involving severe injuries or fatalities by providing objective injury severity information.

Organizing Expenses and Creating Your Damage Record

You must keep all receipts for rental cars, transportation, childcare costs incurred because you couldn’t work, and medical equipment purchases. Create a single spreadsheet listing every expense with the date, vendor, amount, and what it covers. Insurance adjusters evaluate claims by cross-referencing documentation against medical records and treatment timelines, so inconsistencies invite lower settlement offers. You should preserve the accident scene evidence by keeping the police report, photos of vehicle damage, and diagrams showing vehicle positions at impact. Write down your account of the accident while details are fresh, including time of day, weather conditions, and what the other driver was doing before impact. This contemporaneous narrative strengthens your credibility if the case goes to litigation.

Moving From Documentation to Damage Valuation

Once you have compiled your medical records, repair estimates, lost wage documentation, and expense receipts, you face the next critical step: determining what your damages actually worth. Insurance adjusters use formulas and multipliers to calculate settlement offers, but these calculations often undervalue your claim significantly. Understanding how adjusters arrive at their numbers-and where they frequently make mistakes-positions you to challenge lowball offers and pursue fair compensation.

Why Insurance Adjusters Undervalue Your Truck Crash Claim

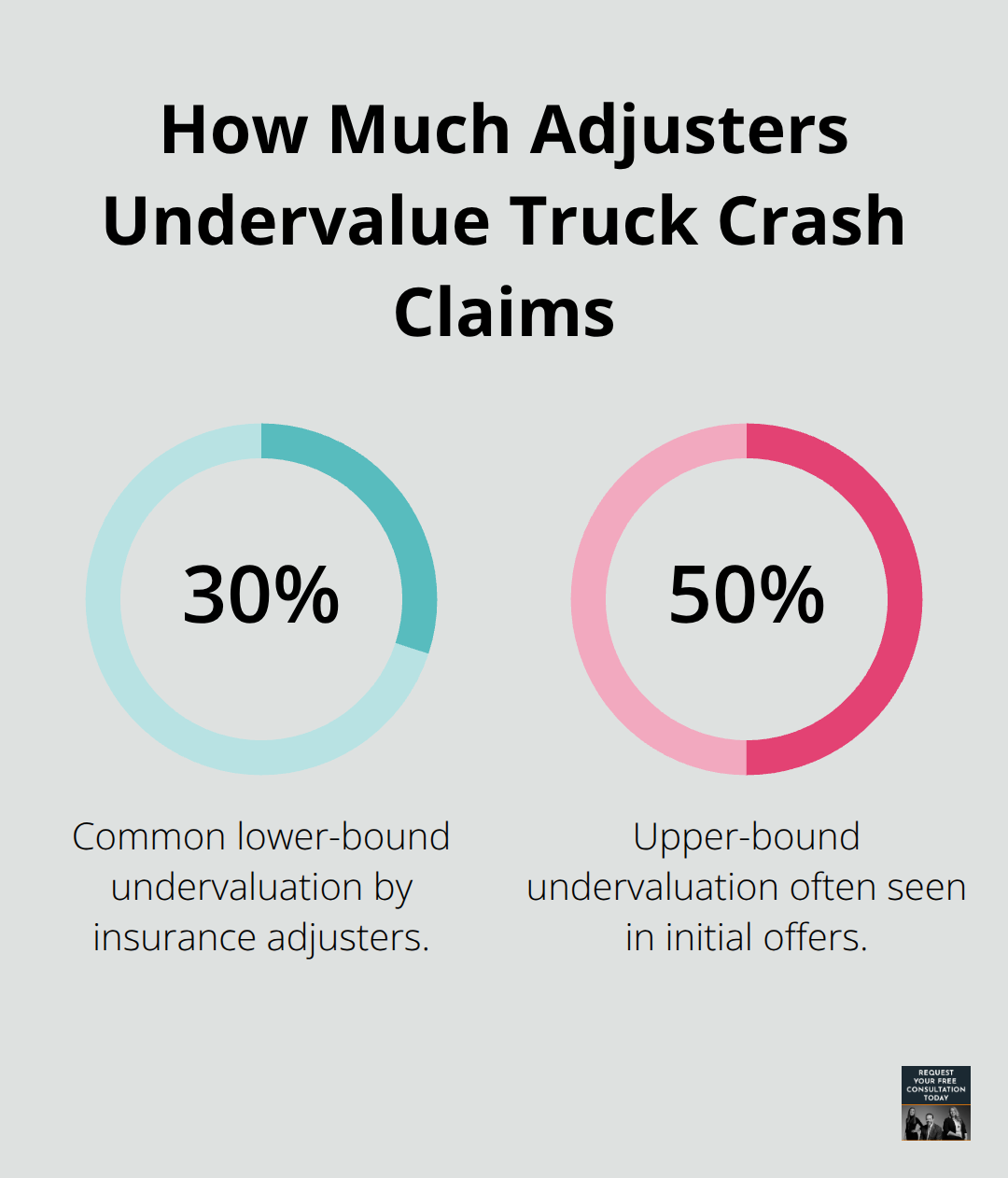

Insurance adjusters in Santa Cruz routinely settle truck crash claims for 30 to 50 percent below what victims actually deserve, and the reason is straightforward: their job is to minimize payouts, not maximize fairness. Adjusters use hidden formulas and multiplier methods that systematically undercount non-economic damages, ignore future medical costs, and suppress lost wage calculations. When you submit documentation showing $8,000 in medical bills, an adjuster might multiply by 1.5 to calculate non-economic damages as $12,000, arriving at a total offer of $20,000. However, if your injuries caused chronic pain lasting two years, required ongoing physical therapy, and reduced your earning capacity permanently, that $12,000 figure is grossly inadequate. Adjusters also exploit documentation gaps aggressively-if your medical records show a three-week gap between the crash and your first doctor visit, they argue the injuries were minor and use that gap to justify lower settlement offers. They know most truck crash victims lack legal guidance and will accept the first offer rather than fight for fair compensation. The Santa Cruz County Sheriff’s Office Motor Vehicle Accidents portal contains raw crash data that can support your claim’s severity, but adjusters rarely volunteer this information or acknowledge how objective data contradicts their low offers.

Adjusters also discount lost wages by claiming you could have returned to work sooner or that you exaggerate missed days. They request employer letters confirming time off, then argue the number is inflated because you might have worked part-time or from home during recovery. For self-employed individuals, adjusters scrutinize tax returns and bank statements looking for inconsistencies, then claim your normal income does not reflect actual earnings during the accident period.

Future Medical Treatment Costs Multiply Over Time

Long-term medical costs after a truck crash frequently exceed initial treatment expenses by 200 to 400 percent, yet adjusters settle claims based only on bills paid through the accident date. If you required six weeks of physical therapy immediately after the crash, you might face another six to twelve months of treatment for residual pain, joint stiffness, or nerve damage that emerges weeks later. Adjusters exclude these future costs from settlement offers because you cannot produce invoices for treatment that has not occurred yet. However, you can obtain a medical provider’s statement projecting future treatment needs and associated costs, then include this projection in your damage calculation. A surgeon or physical therapist can document that ongoing care will likely continue for six months at $150 per session, twice weekly, totaling $7,800 in future expenses. Adjusters will resist including this figure, claiming it is speculative, but California courts recognize future medical damages as legitimate and recoverable. Chronic pain conditions like complex regional pain syndrome or post-traumatic stress disorder often require long-term management that extends years beyond the initial injury. If imaging shows permanent structural damage to your spine or joints, future degenerative changes and treatment costs become foreseeable and compensable. The California Department of Insurance Fair Claims Settlement Practices Regulations require insurers to decide claims within 40 days after you provide proof of loss, but this timeline pressure often forces adjusters to lowball offers rather than conduct thorough analysis of future costs.

Lost Wages Require Precise Documentation and Calculation

Lost wages represent one of the largest damages in truck crash cases, but calculating this amount correctly requires precision that adjusters deliberately avoid. For hourly workers, the math is simple: multiply your hourly rate by hours missed, but adjusters often challenge the number of hours you claim by requesting employer documentation and then arguing you could have worked partial shifts or that your employer inflated the figure. Salaried employees face a different problem-adjusters calculate daily wages by dividing annual salary by 260 work days, but this ignores bonuses, overtime, and commissions that constitute your actual earnings. If you earn a $50,000 base salary plus $15,000 in annual bonuses, your true daily earning rate is $250, not $192.

Adjusters use the lower figure to suppress lost wage claims. Self-employed individuals encounter the strongest resistance because adjusters claim business income fluctuates and you cannot prove what you would have earned during the recovery period. However, you can establish your normal earnings using the prior twelve months of tax returns, invoices, and bank statements, then calculate the average daily income. If you earned $120,000 over the past year, your daily rate is approximately $328, and missing thirty work days equals $9,840 in lost wages. Adjusters will argue your business would have slowed during the recovery period anyway, but you can counter with evidence showing consistent earnings patterns and client commitments that suffered because of your absence. Future earning capacity losses are even more contentious-if your injuries prevent you from returning to your previous occupation, you can hire a forensic economist to calculate lifetime earnings losses. A 35-year-old earning $60,000 annually who can no longer work has potential future losses exceeding $1.2 million over thirty years, yet adjusters routinely deny these claims entirely without obtaining expert analysis.

How Adjusters Suppress Non-Economic Damages

Adjusters systematically undervalue pain and suffering by applying rigid multiplier formulas that fail to account for injury severity or long-term impact. The multiplier method takes your economic damages and multiplies by a factor (typically 1.5 to 5), but adjusters consistently apply the lowest multiplier regardless of circumstances. A serious truck crash that caused permanent scarring, nerve damage, or chronic pain justifies a 4 to 5 multiplier, yet adjusters apply 1.5 or 2 to suppress the final offer. They also argue that non-economic damages are subjective and therefore not “real” losses, even though California law explicitly recognizes these damages as compensable. Adjusters will claim your pain and suffering is exaggerated if you miss a physical therapy appointment or if medical records show improvement between visits. They use any gap in treatment as evidence that your injuries were not serious, ignoring the reality that financial constraints or work obligations often prevent consistent therapy attendance. They also discount psychological injuries like anxiety or depression unless you have extensive mental health treatment records, which many truck crash victims cannot afford to obtain. Adjusters know that most victims will accept lowball offers rather than litigate, so they structure initial offers to be just high enough to seem reasonable but far below what a jury would award.

Final Thoughts

Truck crash damages in Santa Cruz require careful documentation, realistic valuation, and an understanding of how insurance adjusters systematically undervalue claims. Economic damages cover medical bills, lost wages, and property damage, while non-economic damages compensate for pain, suffering, and permanent impacts on your quality of life. Insurance adjusters will exploit gaps in your documentation and apply rigid multiplier formulas that suppress your settlement offer by 30 to 50 percent.

Fighting for fair compensation requires challenging adjuster calculations with evidence from the Santa Cruz County Sheriff’s Office Motor Vehicle Accidents portal, medical providers who project future treatment costs, and forensic economists who calculate lifetime earning capacity losses. The California Department of Insurance Fair Claims Settlement Practices Regulations require insurers to acknowledge your claim within 15 days and decide within 40 days, but this timeline pressure often forces adjusters to lowball offers rather than conduct thorough analysis. You can obtain raw crash data to support your claim’s severity and counter undervaluation tactics with objective documentation.

We at Schaar & Silva LLP understand the financial and emotional burden truck crashes create, and we help you pursue the compensation you deserve. Contact us to discuss your case and learn how our team can handle the legal intricacies while you focus on recovery.