A car accident in Santa Cruz County can leave you facing medical bills, lost wages, and pain that won’t go away. You deserve compensation for what happened to you.

At Schaar & Silva LLP, we help accident victims understand exactly what they’re entitled to receive. This guide walks you through calculating damages, navigating insurance companies, and meeting California’s strict deadlines.

How Injury Severity Drives Your Settlement Value

Types of Injuries and Their Impact on Compensation

The type of injury you sustain directly determines how much your case is worth. Brain injuries, spinal cord damage, and fractures that require surgery command significantly higher settlements than soft tissue injuries like whiplash. In Santa Cruz, ER costs alone range from $1,200 to $3,500, and serious injuries often lead to ongoing care that multiplies your total damages. The Insurance Information Institute reported that the average property damage claim in 2018 exceeded $3,800, but that figure doesn’t capture the full picture for injury cases. When you have documented treatment spanning months-physical therapy at $60 to $150 per session, MRI scans costing $1,000 to $3,000, and follow-up visits at $150 to $500 each-you build a medical record that justifies higher compensation.

How Adjusters Calculate Your Settlement

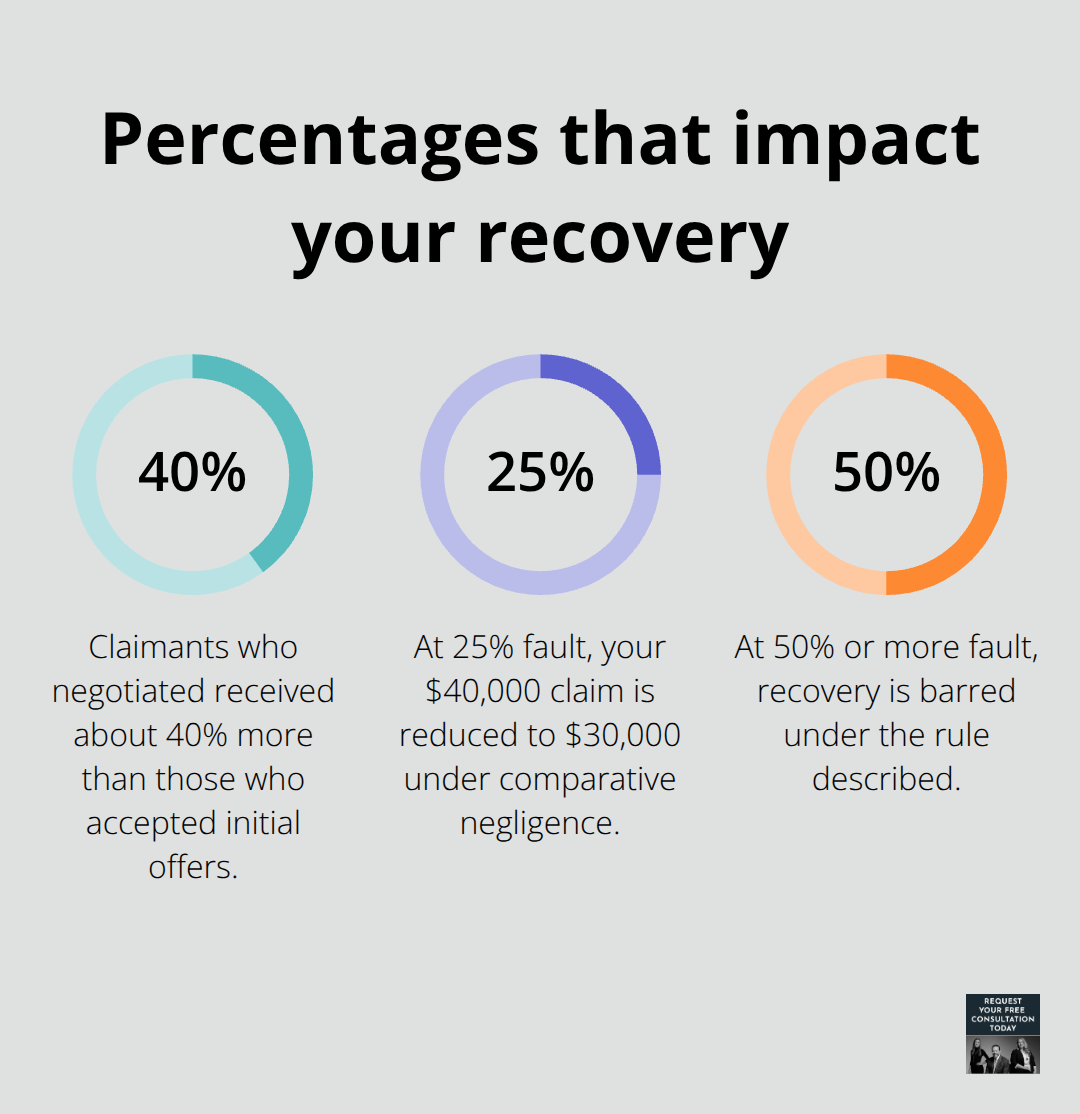

Insurance adjusters use a multiplier method, typically between 1.5 and 5 times your medical expenses, then add lost wages and property damage. Most people make a critical mistake by accepting the first offer without negotiation. A study by the Insurance Information Institute found that claimants who negotiated settlements received about 40 percent more than those who accepted initial offers, so pushing back with documented evidence pays off.

Building Your Medical Record

Medical records serve as your strongest negotiating tool, and gaps in treatment represent your biggest vulnerability. Start medical care within days of the accident-delays between the crash and your first visit give insurers ammunition to argue your injuries weren’t serious. Obtain complete records from every provider, including diagnoses, treatment dates, prescriptions, and imaging results. Long-term costs extend far beyond what you initially see. Physical therapy might continue for three to six months, and specialist consultations add up quickly. Request written cost projections from your doctors to include in your settlement demand if you need ongoing treatment.

Tracking Expenses and Building Your Claim

Track every expense: copays ($10 to $50), medical equipment ($50 to $300), transportation costs, and lost wages. Most Santa Cruz providers accept medical liens, which means they defer payment until your settlement resolves, allowing you to receive care without upfront costs. Document your daily impact through a personal injury journal detailing pain levels, limitations, and how injuries affect your work and daily life. This narrative evidence strengthens non-economic damages claims for pain and suffering, which often represent the largest portion of your recovery but are frequently undervalued by insurers.

Moving Forward With Your Claim

With your medical documentation in place and expenses tracked, you now understand what your injuries are actually worth. The next step involves calculating the full scope of damages you’re entitled to receive under California law-both the tangible costs and the compensation for pain that extends beyond medical bills.

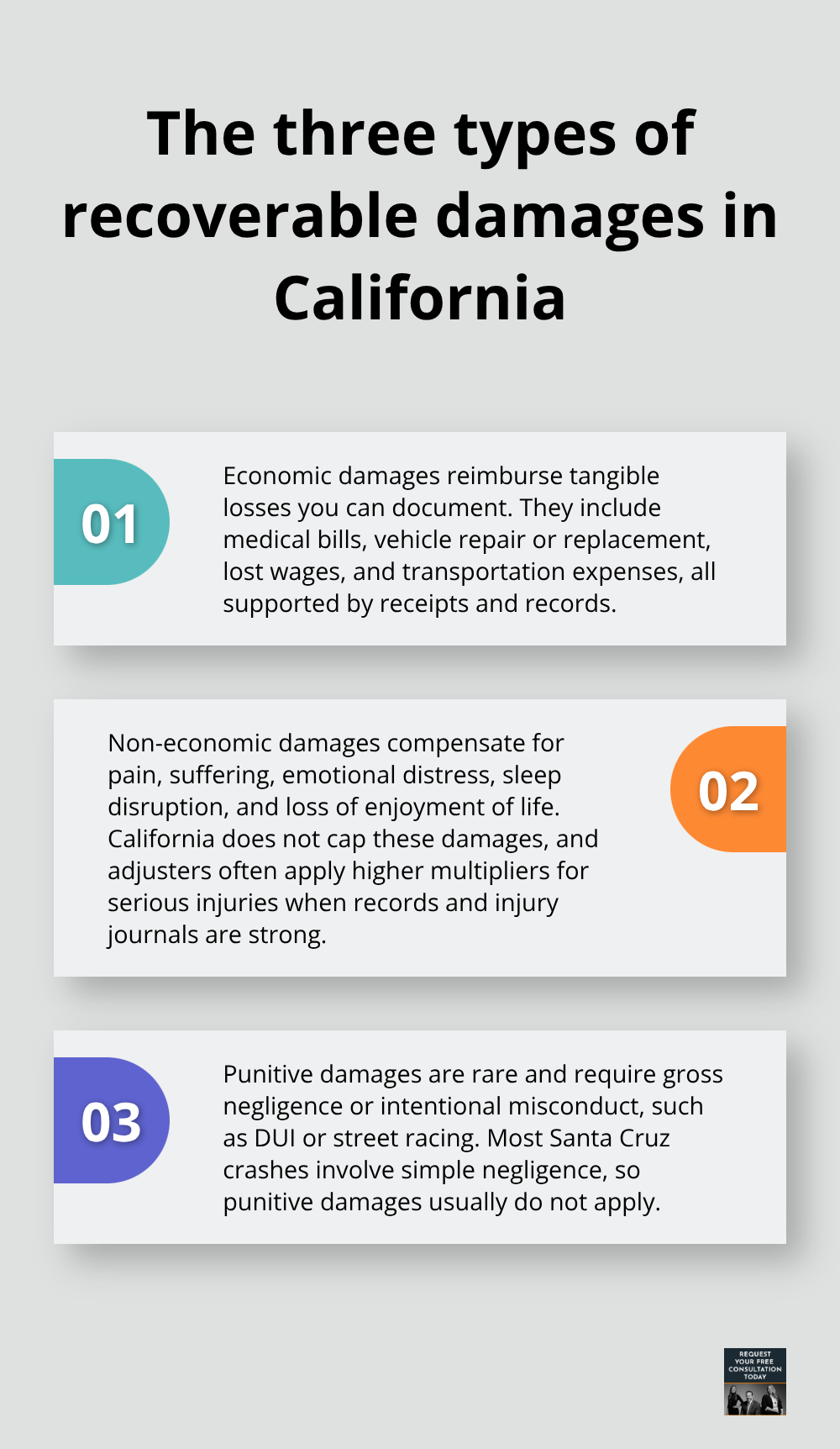

What You’re Actually Entitled To Recover

California law recognizes three distinct categories of damages after a car accident, and understanding each one prevents you from leaving money on the table. Economic damages cover tangible losses with receipts: medical bills, vehicle repair or replacement costs, lost wages, and transportation expenses. These are straightforward to calculate because documentation exists. If you spent $2,500 on ER care, $800 on follow-up visits, $1,200 on physical therapy sessions, and missed two weeks of work earning $1,500 per week, you have $5,800 in economic damages before even factoring in vehicle costs.

Non-Economic Damages: Pain, Suffering, and Lost Life

Non-economic damages compensate for pain and suffering, emotional distress, sleep disruption, and loss of enjoyment of life-the aspects insurers most aggressively undervalue. California does not cap non-economic damages, which means the severity and duration of your injury directly determine this portion. An adjuster using the multiplier method applies 1.5 times your medical expenses for minor soft tissue injuries but 4 or 5 times for serious fractures or spinal damage. Your daily injury journal becomes critical here: detailed entries about pain levels, activities you cannot perform, work interruptions, and how the injury affects your relationships create the narrative foundation for higher non-economic awards.

Punitive Damages: When They Apply

Punitive damages are rare and apply only when the at-fault driver engaged in gross negligence or intentional misconduct-DUI, street racing, or reckless behavior that endangered lives. Most Santa Cruz accidents involve simple negligence, so punitive damages typically do not apply to your case.

How Your Fault Percentage Reduces Recovery

Your percentage of fault directly reduces what you receive under California’s comparative negligence rule. If you are 25 percent at fault in a $40,000 claim, you recover $30,000. This rule applies as long as you are less than 50 percent responsible; being equally or more at fault bars recovery entirely.

Insurance Limits and Coverage Gaps

Insurance limits create a hard ceiling on recovery regardless of actual damages. California’s minimum liability coverage is $15,000 per person and $30,000 per accident for bodily injury, leaving a significant gap if your injuries exceed these thresholds. Verifying the at-fault driver’s coverage limits immediately after the accident matters: if they carry only minimum coverage and your damages total $50,000, you can only recover $30,000 from their liability policy unless your own uninsured or underinsured motorist coverage applies. Check your policy right now-most Santa Cruz drivers carry inadequate limits. Medical lien services amplify your recovery by deferring provider payments until settlement, preventing early bill collection that would reduce your settlement demand. When calculating your final net recovery, subtract medical lien payouts, health insurance subrogation claims, and any outstanding liens before comparing settlement offers to your actual injury costs.

With your damages calculated and your recovery potential clear, the next step involves navigating the actual claims process and understanding the strict timelines California imposes on your case.

How to Navigate Your Claim and Insurance Negotiations

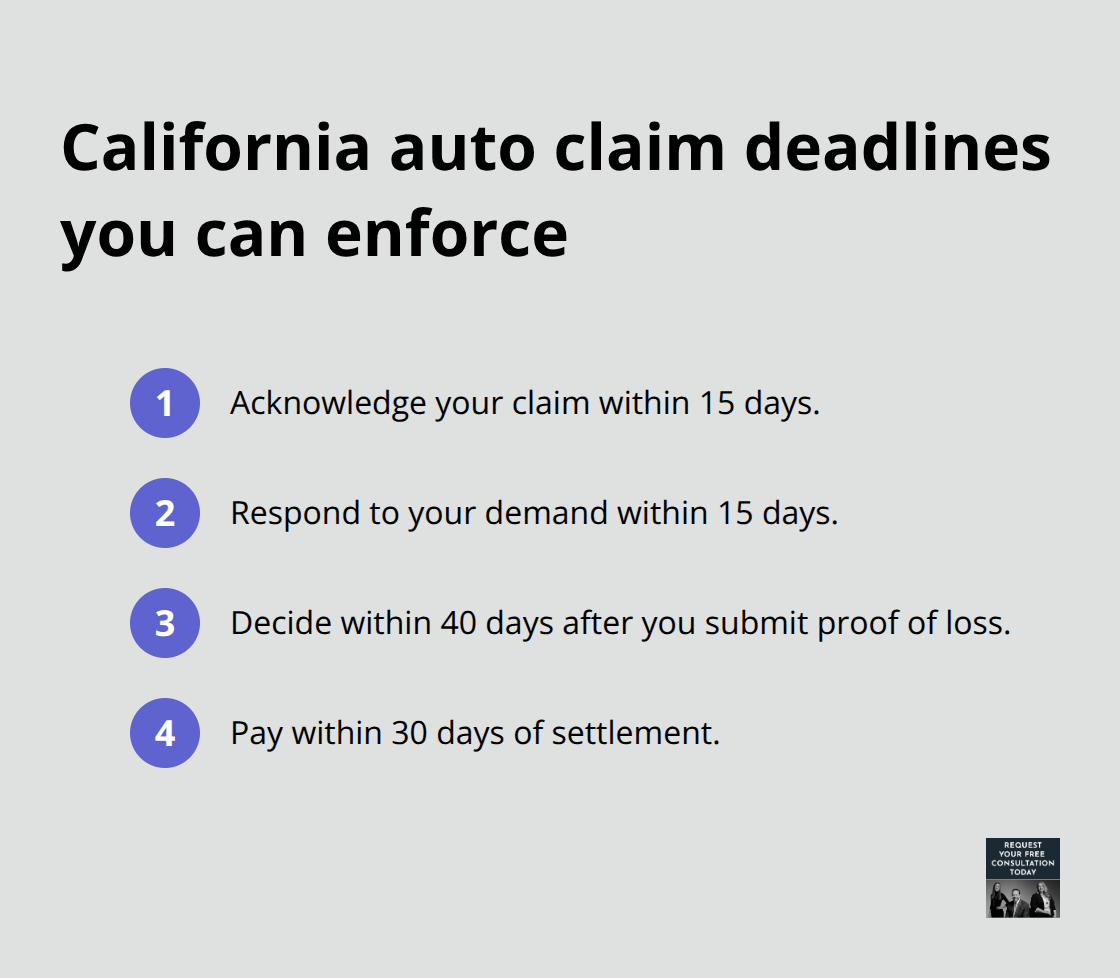

California’s Fair Claims Settlement Practices Regulations impose strict timelines that work in your favor if you understand them. Your insurer must acknowledge your claim within 15 days, respond to your demand within 15 days, make a decision within 40 days after you submit proof of loss, and pay within 30 days of settlement. Most Santa Cruz accident victims don’t realize these deadlines exist, which means they accept delays as normal when they should be pushing back.

File Your Claim Promptly

File your claim within 30 days of the accident. Contact your insurer with the police report number, accident date, location, and a brief description of what happened. Provide your claim number in writing and keep copies of everything you send. When the adjuster contacts you, never give a recorded statement without consulting an attorney first. California regulations don’t prevent insurers from using recorded statements against you, so declining or requesting written questions instead protects your position. Document every communication with dates, times, names, and what was discussed.

Understand Adjuster Tactics

Insurance adjusters negotiate settlements daily and know exactly how to pressure you into accepting less than your claim is worth, especially if you’re unfamiliar with the process. They typically counter with 40 to 60 percent of your opening demand, so anticipate negotiation rounds. A study by the Insurance Information Institute found that claimants who negotiated settlements received about 40 percent more than those who accepted initial offers, so rejecting lowball offers and countering with documented evidence is standard practice.

Build Your Demand Package

Your settlement demand should arrive in writing and itemize every cost with supporting documentation. Include your medical bills organized by provider and date, pay stubs showing lost wages, repair estimates and invoices for vehicle damage, photographs of the accident scene and your injuries, witness statements with contact information, and the police report. For non-economic damages, reference your injury journal entries that describe specific pain levels, activities you cannot perform, sleep disruption, and work interruptions. Request a 30-day response deadline in your demand letter.

Assess When to Pursue Legal Action

If negotiations stall after three to four exchanges, assess whether the adjuster is negotiating in good faith or whether litigation makes financial sense for your claim size. Most Santa Cruz personal injury claims settle within 3 to 9 months, so plan for delays and ongoing medical costs during this period. Serious injuries like brain or spinal cord damage, cases involving multiple defendants, or claims exceeding your at-fault driver’s insurance limits often require legal representation to maximize recovery. The legal team at Schaar & Silva LLP can review your case, evaluate settlement offers against your actual damages, and handle negotiations or litigation if the insurer refuses fair compensation.

Final Thoughts

You now understand how Santa Cruz auto compensation works from injury assessment through settlement negotiation. Economic damages cover your medical bills, lost wages, and vehicle repair costs with straightforward documentation, while non-economic damages compensate for pain, suffering, and lost life quality-often representing your largest recovery but requiring solid evidence through medical records and injury journals. Your fault percentage directly reduces what you receive under California’s comparative negligence rule, and insurance limits create a hard ceiling regardless of actual damages.

The claims process follows strict timelines that work in your favor if you act promptly: file your claim within 30 days of the accident, never give a recorded statement without legal guidance, and build a comprehensive demand package with itemized medical bills, pay stubs, repair estimates, photographs, and witness statements. Claimants who negotiated settlements received about 40 percent more than those who accepted first offers, so reject lowball initial offers and counter with documented evidence. Most Santa Cruz personal injury claims settle within 3 to 9 months, so plan for ongoing medical costs and delays during recovery.

Serious injuries, multiple defendants, or claims exceeding insurance limits often require legal representation to maximize recovery. The team at Schaar & Silva LLP can review your case, evaluate settlement offers, and handle negotiations or litigation if the insurer refuses fair compensation. Contact us to discuss your specific situation and understand what your Santa Cruz auto compensation claim is actually worth.