A car accident in Santa Cruz County leaves you with more than just physical injuries-you’re facing vehicle damage, repair bills, and questions about your vehicle’s future value.

We at Schaar & Silva LLP understand that navigating damage assessments, insurance coverage, and diminution claims feels overwhelming. This guide walks you through what happens after an accident, from how adjusters evaluate damage to what you can actually recover.

How Adjusters Assess Damage and What You Should Document

The Adjuster’s Role After Your Accident

After an accident in Santa Cruz County, an insurance adjuster will examine your vehicle to determine repair costs and establish a baseline for your claim. Adjusters assess structural damage, paint condition, mechanical systems, and whether parts can be repaired or must be replaced. They photograph the damage from multiple angles and document everything in a report that becomes the foundation of your claim. The adjuster’s job is to estimate repair expenses, but their valuation often falls short of what your vehicle actually loses in market value.

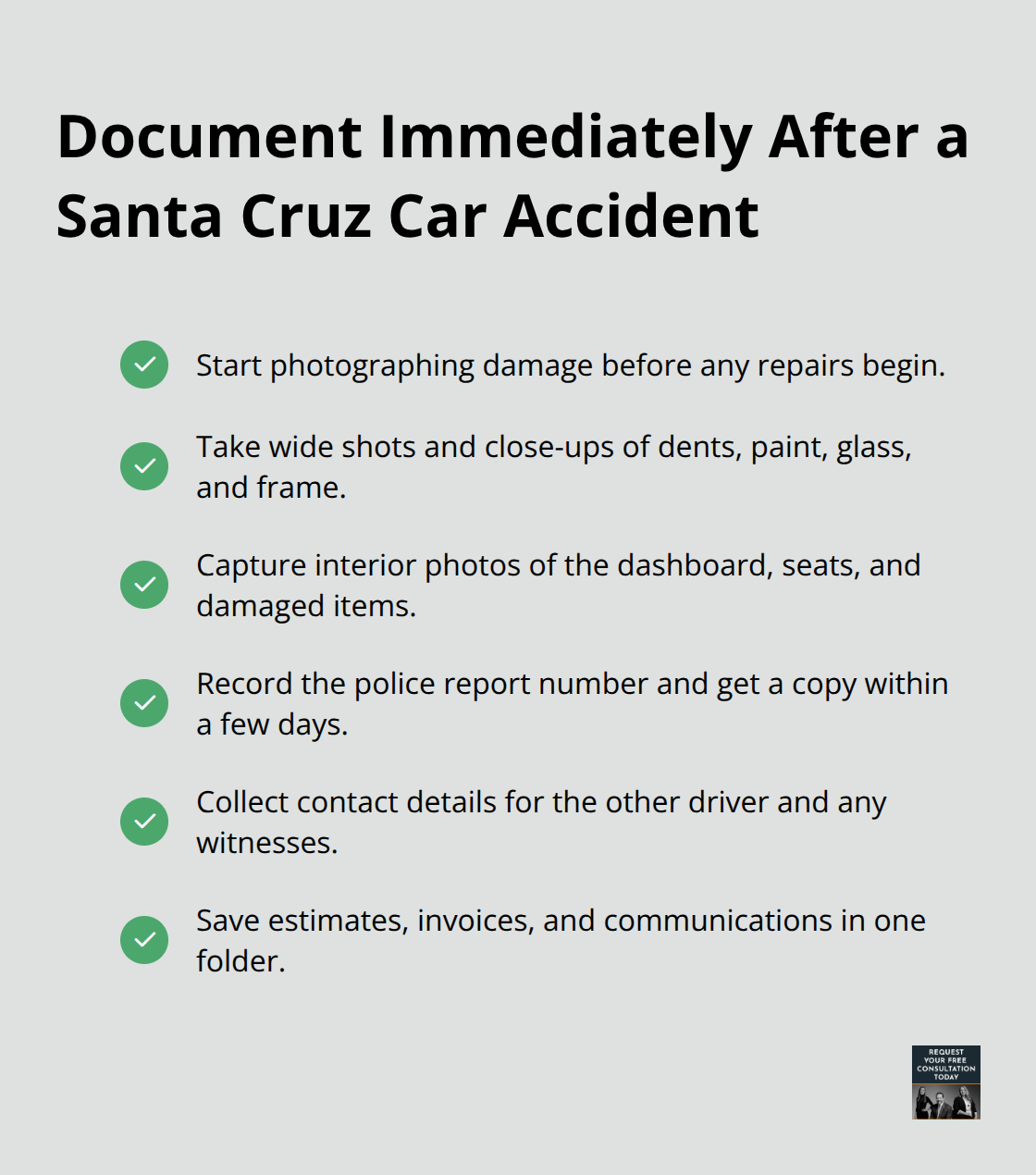

Photograph and Document Immediately

Your own documentation matters significantly after an accident. Start photographing damage immediately, before any repairs begin. Capture wide shots showing the overall damage and close-ups of specific areas like dents, paint scratches, broken glass, and frame damage. If you can safely access the vehicle’s interior, photograph the dashboard, seats, and any personal items damaged in the crash. Collect the police report number and obtain a copy within a few days-this report creates an official record of the accident and helps prove the incident occurred.

Request contact information from the other driver and any witnesses present at the scene.

Get a Detailed Repair Estimate

If you hire a body shop to assess repairs, ask them for a detailed written estimate that breaks down labor, parts, and paint costs separately. Shops in Santa Cruz like Kraft’s Body Shop provide free drive-in estimates and can explain exactly what repairs are needed and why. A thorough estimate from a reputable local shop strengthens your documentation and gives you concrete numbers to reference during negotiations.

Challenge the 17c Method with Real Market Data

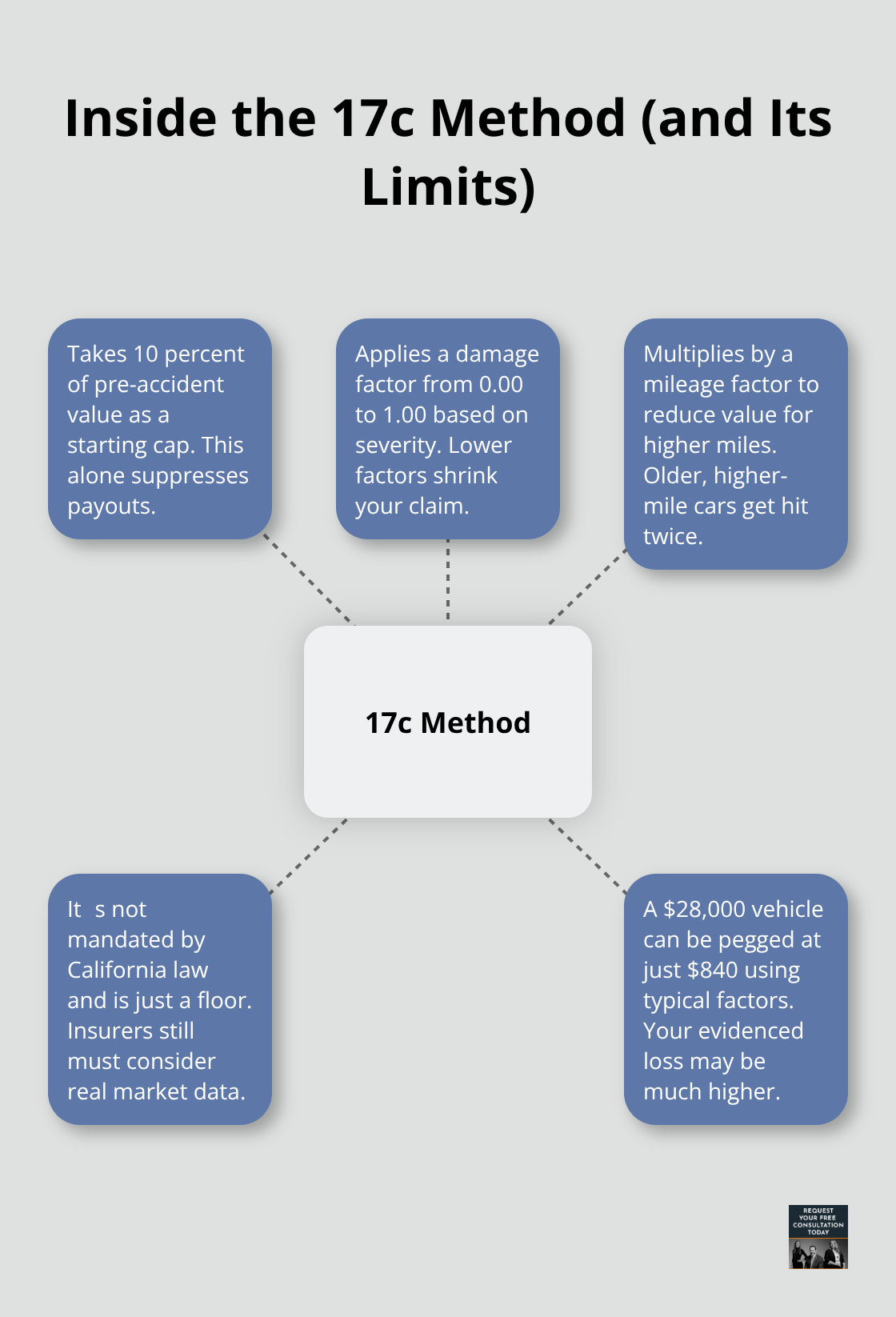

The adjuster’s initial assessment often uses shortcuts to minimize payouts. Many insurers apply what’s called the 17c method as a starting point, which takes 10 percent of your vehicle’s pre-accident value, applies a damage factor between 0.00 and 1.00, and multiplies by a mileage factor. For example, if your vehicle was worth $28,000 before the crash, the 17c method might calculate diminished value at $840 using standard factors. This method is not California law and represents only a floor, not a ceiling. Your actual diminished value claim can be far higher when backed by real market data.

Gather evidence showing what comparable vehicles with clean accident histories sell for in Santa Cruz County. Check local listings on platforms where you’d normally buy or sell a vehicle and note the price range for your exact year, trim level, and mileage. Then compare those prices to what similar vehicles with disclosed accident histories are selling for in your area. The price gap between clean and accident-disclosed vehicles is your strongest proof.

Build Your Evidence Package

Consider obtaining a written offer from a local dealership or wholesaler for your vehicle post-repair. Dealerships routinely adjust their offers downward for vehicles with accident history, and that written offer provides concrete evidence of diminished value. An independent appraisal from a local appraiser carries significant weight in negotiations. Request a report that includes comparable vehicles, a detailed review of the repairs completed, and photographs showing the vehicle’s current condition.

When you present your claim to the at-fault driver’s insurer, include your repair invoices, vehicle history report showing the accident, local comparable listings, and any appraisals or dealer offers. Start this documentation process immediately after the accident. Delaying weakens your leverage and makes it harder to gather accurate market data later. The evidence you collect now determines how much you can recover for the loss in your vehicle’s value-a loss that extends far beyond the repair bill itself.

What Insurance Actually Pays for After Your Accident

Coverage Types and What They Cover

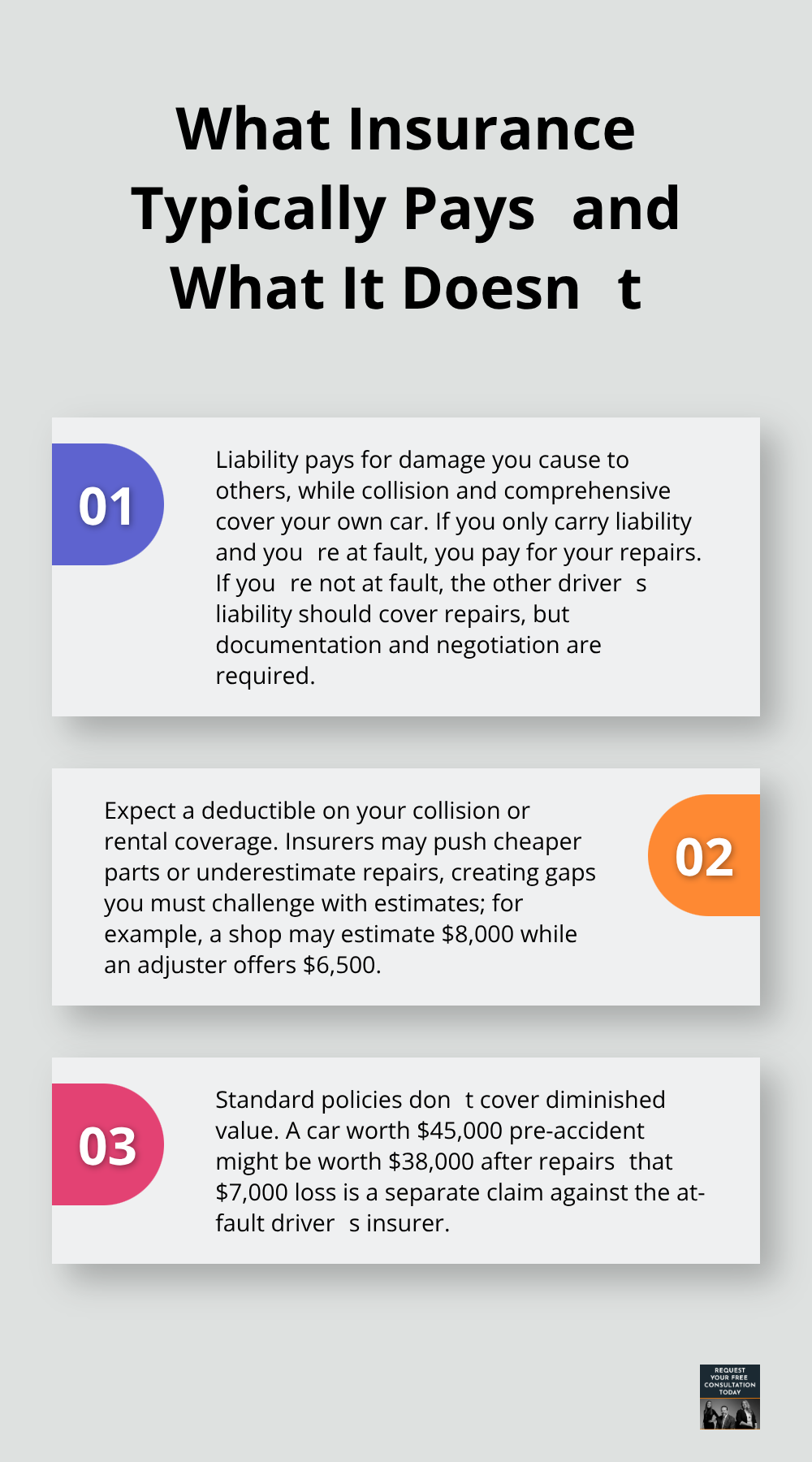

After an accident in Santa Cruz County, your insurance coverage determines what gets paid and what comes out of your pocket. Most California drivers carry liability coverage, which pays for damage you cause to someone else’s vehicle but does nothing for your own repairs unless you have collision or comprehensive coverage. If you’re the at-fault driver and only carry liability, you pay every repair dollar. If you’re not at fault, the other driver’s liability insurance should cover your repairs in full, but getting there requires documentation and negotiation. Collision coverage on your own policy pays for repairs regardless of fault, though you’ll owe your deductible first-typically ranging from $250 to $1,000 in Santa Cruz County. Comprehensive coverage handles non-collision damage like theft, weather, or vandalism.

The Gap Between What Insurers Pay and What You Actually Lose

Most people assume insurance covers everything. It doesn’t. Your insurer pays only for repairs that restore your vehicle to pre-accident condition, not improvements.

They’ll also push to use aftermarket or refurbished parts instead of original manufacturer parts, which can affect your vehicle’s resale value and repair quality. Kraft’s Body Shop in Santa Cruz works directly with most major insurance companies and can explain exactly what your coverage allows, helping you avoid surprises when the bill arrives.

Your out-of-pocket costs depend on your deductible, the coverage limits of the at-fault driver’s insurance, and whether your repairs exceed what the insurer considers reasonable. If the repair estimate from a reputable local shop is $8,000 but the at-fault insurer’s adjuster estimates only $6,500, you face a gap that the insurer won’t cover unless you push back with competing estimates and documentation.

Diminished Value: The Loss Insurers Won’t Cover

Many Santa Cruz drivers don’t realize that diminished value isn’t covered by standard insurance policies. The repair bill might be fully covered, but the loss in your vehicle’s market value after repairs is a separate claim you must file against the at-fault driver’s insurer. This is where most people lose money. A vehicle worth $45,000 before an accident might be worth only $38,000 after repairs, even with perfect body shop work. That $7,000 gap is real economic loss, and insurers count on drivers not knowing they can claim it.

Rental Coverage and Additional Out-of-Pocket Expenses

Rental car coverage is another area where gaps appear. Your policy might cover a rental for 30 days, but if repairs take longer, you pay the difference. Deductibles apply to rental coverage too, meaning you might owe $500 out of pocket for the rental on top of your collision deductible.

Building Your Repair Documentation

Start gathering repair estimates from multiple Santa Cruz shops immediately after the accident. Compare what each shop recommends and get their reasoning in writing. This gives you leverage when the insurer’s adjuster underestimates repair costs or tries to use cheaper alternatives that compromise your vehicle’s integrity or value. The estimates you collect now become your foundation for negotiating with the at-fault insurer and, if necessary, pursuing a diminished value claim that extends far beyond the repair bill itself.

How Diminished Value Actually Works in Santa Cruz

Diminished value is the real loss in your vehicle’s market worth after an accident, separate from repair costs. A vehicle worth $45,000 before a crash might sell for only $38,000 afterward, even with flawless repairs. That $7,000 gap is diminished value, and it’s yours to claim against the at-fault driver’s insurer. Most Santa Cruz drivers never pursue this because they don’t realize it exists or they assume insurance covers it automatically. Insurance doesn’t. The repair bill gets paid, but the loss in resale value is a distinct property damage claim you must file separately.

The Market Reality in Santa Cruz County

Buyers in Santa Cruz County actively avoid vehicles with accident history. When you list a repaired vehicle for sale, local buyers check the Carfax or AutoCheck report and immediately offer less. The price difference between a clean-history vehicle and one with disclosed accident history is your proof of diminished value. Pull local listings right now for your exact year, trim, and mileage on platforms where people actually buy and sell vehicles in Santa Cruz. Note the asking prices for clean-history cars, then search for identical vehicles with disclosed accident history. The gap between those two price ranges is concrete evidence. A 2019 Honda Civic with 60,000 miles and no accidents might list for $18,500 in Santa Cruz, while the same model with accident history sells for $16,200. That $2,300 difference is your baseline. This market data beats any formula the insurer uses.

Collect Evidence That Proves Your Loss

Start immediately after repairs finish. Obtain a written offer from a local Santa Cruz dealership or wholesaler for your repaired vehicle. Dealerships routinely reduce their trade-in offers for accident-history vehicles, and that written offer gives you hard evidence. Hire an independent appraiser in Santa Cruz County to evaluate your vehicle post-repair and request a detailed report showing comparable vehicles, repair quality assessment, and current market value. This appraisal carries significant weight because it comes from a neutral third party with no stake in the outcome. Gather your repair invoices, parts lists, and completion photos showing the quality of work. Compile your vehicle history report and attach it to your claim submission.

Present Your Claim to the At-Fault Insurer

When you file with the at-fault driver’s insurer, present everything together: repair documentation, local comparable listings showing price gaps, the dealership offer, and the independent appraisal. The insurer will likely respond with a low initial offer using the 17c method or similar shortcuts (taking 10 percent of pre-accident value, applying damage and mileage factors). Reject it. Your market data and appraisal prove the actual loss is higher.

Push back with your evidence. If the insurer refuses to move significantly, contact Schaar & Silva LLP to evaluate whether your case warrants legal action to recover the full diminished value you deserve.

Final Thoughts

After an accident in Santa Cruz County, you now understand what happens when adjusters assess vehicle damage, how insurance coverage actually works, and why diminished value claims matter far more than most drivers realize. The repair bill covers only part of your recovery-your vehicle loses market value the moment the accident occurs, and that loss is yours to claim against the at-fault driver’s insurer. Document everything immediately: photographs, police reports, repair estimates from local shops, and comparable vehicle listings showing what clean-history cars sell for in your area.

Gather market data before filing your diminished value claim, obtain a dealership offer and an independent appraisal, and present all this evidence together when you submit your claim. The at-fault insurer will likely respond with a low initial offer using formulas like the 17c method, but your real market data proves the actual loss is higher. Push back with your evidence and reject offers that don’t reflect what your vehicle actually lost in value.

If negotiations stall or the insurer refuses to move significantly, you don’t have to accept their offer. Contact Schaar & Silva LLP to discuss your vehicle damage Santa Cruz claim and learn what you can actually recover-we help Santa Cruz County residents evaluate property damage claims and pursue the full compensation they deserve.