After a car accident in Santa Cruz County, insurance companies often undervalue property damage claims. We at Schaar & Silva LLP created this property damage valuation guide to help you understand what your vehicle damage is actually worth.

Getting the right payout requires knowing how insurers calculate damage, what documentation matters, and when to push back on low offers. This guide walks you through each step.

What Damage Does Your Claim Actually Cover

Understanding What Insurers Will Pay For

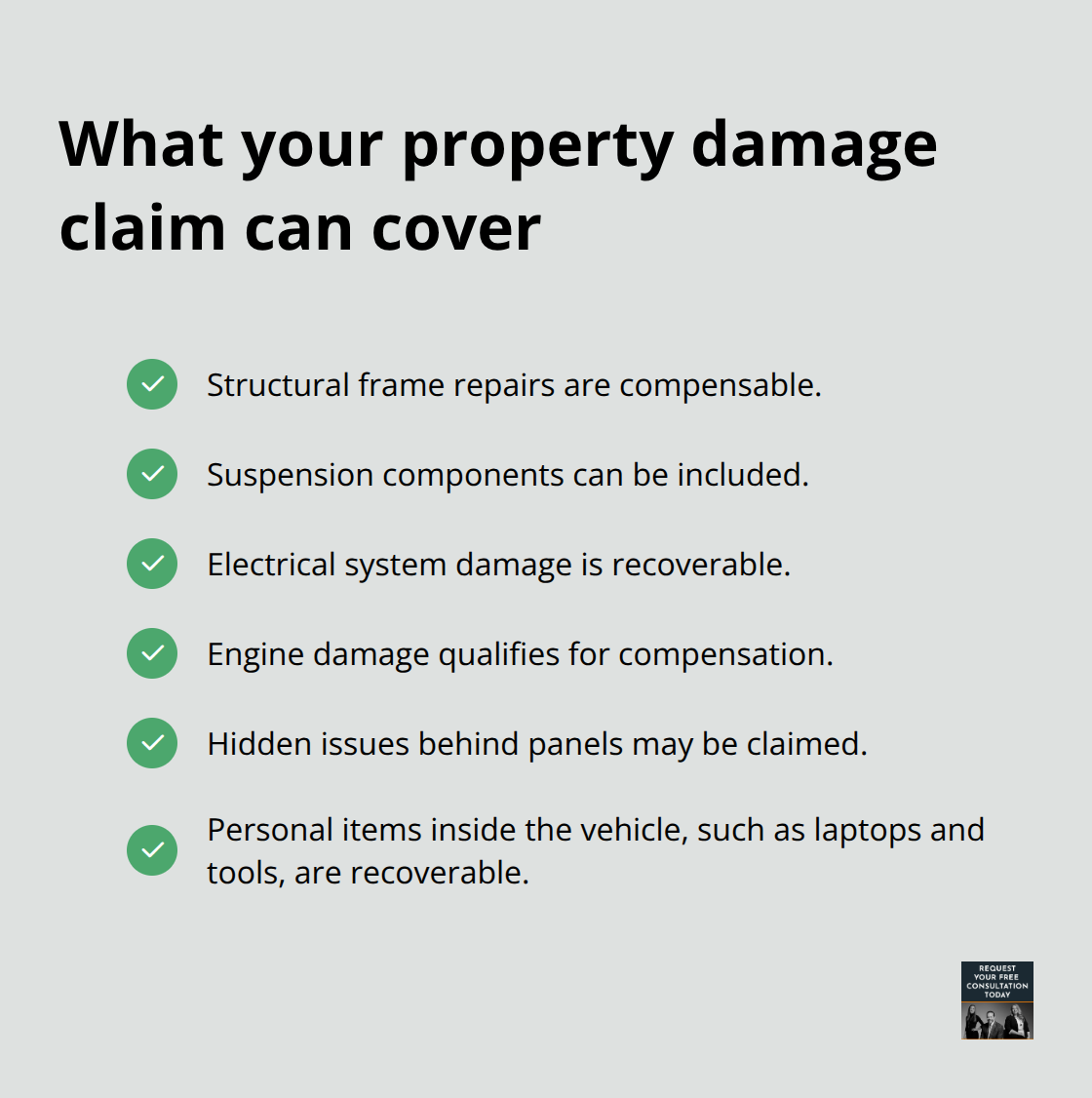

After a crash in Santa Cruz County, understanding what insurers will pay for is the first step toward protecting your recovery. Property damage claims cover far more than dents and broken glass. Your vehicle’s structural frame, suspension system, electrical components, engine damage, and hidden issues behind panels all qualify for compensation. Many claimants in Santa Cruz discover after settlement that they missed thousands in recoverable damage because they didn’t know what to claim.

Personal items inside your vehicle at the time of the accident-laptops, glasses, clothing, tools-are also recoverable losses. You should document these items with photos and receipts to include them in your claim.

Why NADA Guides Underestimate Local Repair Costs

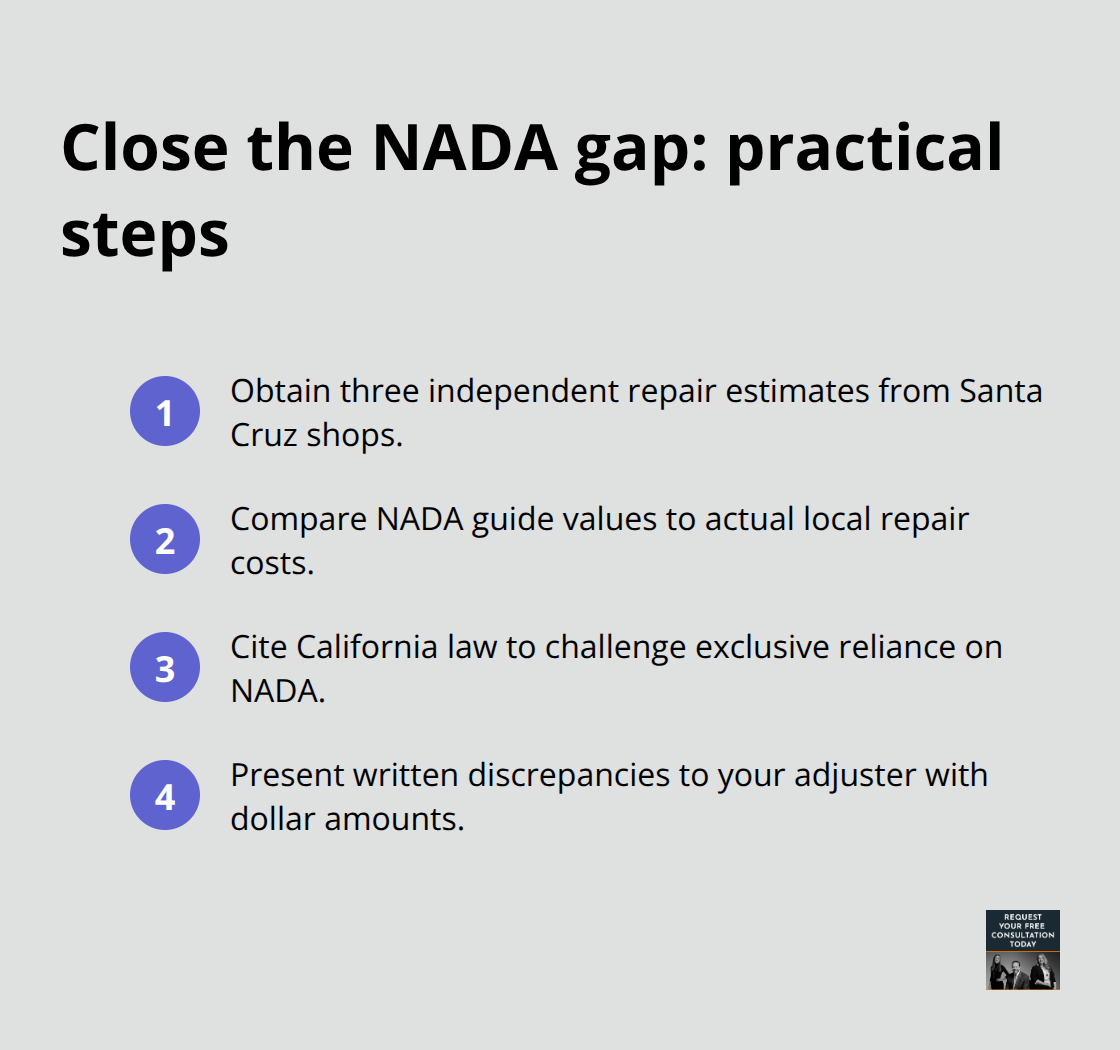

Insurance companies rely on National Automotive Dealers Association (NADA) Guides to assign values, but these guides frequently underestimate actual repair costs in our region. A vehicle valued at $15,000 on NADA might cost $18,000 or more to repair at Santa Cruz shops due to local labor rates and parts availability. This gap between the guide value and real costs is where claimants lose money.

California law does not require insurers to use NADA Guides exclusively, yet most do anyway because it keeps payouts lower. You gain significant leverage when you obtain at least three independent repair estimates from different Santa Cruz shops before accepting any settlement offer.

How Adjusters Miss Hidden Damage

Insurance adjusters assess damage using a standardized process, but the process itself creates room for underpayment. Adjusters typically inspect the vehicle once, often spending less than an hour on site, and then reference NADA values rather than obtaining multiple independent repair estimates from local shops.

The real problem surfaces when hidden damage emerges during repairs-frame misalignment, water intrusion, suspension component failure-which can add $5,000 to $10,000 or more to the final repair bill. Insurers often deny these additional costs because the damage wasn’t visible during the initial inspection. You should insist on a full pre-repair mechanical inspection from a licensed Santa Cruz technician before you settle. Request that the inspection specifically check for frame straightness, suspension integrity, and electrical system damage.

Building Your Negotiating Position

The difference between a low initial offer and estimates from local shops frequently reaches $2,000 to $5,000. You create leverage for negotiation when you present multiple written estimates to your adjuster. This documentation becomes your foundation for the next phase of your claim-negotiating with the insurance company to close the gap between their offer and what your vehicle actually costs to repair.

Building Your Valuation Case

Hire an Independent Appraiser to Counter NADA Valuations

An independent certified appraiser documents your vehicle’s pre-crash condition and compares it to current market data, directly countering the insurer’s reliance on NADA Guides. Most claimants skip the appraisal step entirely, costing themselves thousands in lost recovery. The upfront cost of a professional appraisal-typically $300 to $600-pays for itself when the appraisal justifies a settlement increase of $2,000 to $5,000 or more. California law supports your right to an independent valuation, and presenting this professional assessment shifts the negotiation dynamic away from the insurer’s one-sided estimate toward a documented, defensible position.

Photograph Everything Immediately After the Accident

Photograph your vehicle from multiple angles immediately after the crash, capturing all visible damage, the accident scene, and any road conditions that contributed to the collision. Obtain the police report within 48 hours and request the officer’s name, badge number, and report number for your records. These photographs and the police report form the foundation of your claim and establish the accident’s circumstances before memory fades or conditions change.

Collect Repair Estimates from Three Independent Santa Cruz Shops

Collect repair estimates from at least three different licensed Santa Cruz shops-not the insurer’s preferred vendor. These independent estimates reveal what local shops actually charge for labor and parts, exposing the gap between NADA valuations and real costs. Present written repair estimates to your adjuster and include a brief statement highlighting discrepancies between the insurer’s valuation and the independent shop estimates.

Document Personal Items and Maintain Organized Records

Keep receipts and invoices for any personal items damaged in the vehicle, along with photos showing these items inside the car at the time of the accident. Organize all documentation in a single file with dates clearly marked; California’s three-year statute of limitations for property damage claims means you must maintain these records throughout any negotiation or potential legal process. This written record protects you if disputes arise and demonstrates that you approached the claim methodically rather than emotionally.

Present Your Documentation to Strengthen Negotiations

When you submit your complete file to the adjuster, the combination of independent appraisal, multiple repair estimates, police report, and organized documentation creates a position the insurer cannot easily dismiss. The gap between what you can prove and what the insurer initially offered becomes the starting point for serious negotiation rather than a take-it-or-leave-it scenario. Your next move involves using these materials strategically to challenge lowball offers and push for fair settlement.

Negotiating Settlement When Insurers Undervalue Your Claim

Present Your Complete Documentation in Writing

Your documentation is now complete, but the initial settlement offer sitting in your inbox is almost certainly too low. Insurance companies set their opening position as a negotiating floor, not a final number. The gap between their first offer and what you can prove with independent repair estimates typically ranges from $2,000 to $5,000, sometimes more. This is where your preparation converts into actual money.

Submit your complete file to the adjuster in writing, including the independent appraisal, three repair estimates from Santa Cruz shops, the police report, and a clear statement highlighting each discrepancy between the insurer’s valuation and your documented costs. Insurers respond to organized, documented pressure far more readily than to phone calls or emotional appeals.

Leverage Your Repair Shop Estimates

Your repair shop estimates carry particular weight because California law requires insurers to stand behind repairs performed at your chosen shop if those repairs meet accepted trade standards. This means the insurer cannot dismiss your local shop’s estimate as inflated when that shop holds proper licensing and maintains industry standards.

Do not accept a counteroffer immediately. Take time to review whether it covers all documented damages, and if the number still falls short of your estimates, submit a written response with specific dollar amounts and supporting evidence for each disputed item. The combination of multiple independent estimates and California’s repair shop protection law shifts the negotiation dynamic in your favor.

Use the California Appraisal Provision to Resolve Disputes

If negotiations stall after you have presented strong documentation, the California appraisal provision offers a formal pathway forward without immediately filing a lawsuit. Under this provision, you and the insurer each select an appraiser, and those two appraisers select a neutral umpire to resolve the valuation dispute. The umpire’s decision becomes binding, giving you a clear mechanism to challenge unreasonable valuations.

This formal process removes the insurer’s ability to simply ignore your evidence and forces a third-party evaluation of the actual damage costs. Many claimants find that the threat of appraisal alone motivates insurers to increase their settlement offers rather than face a binding decision.

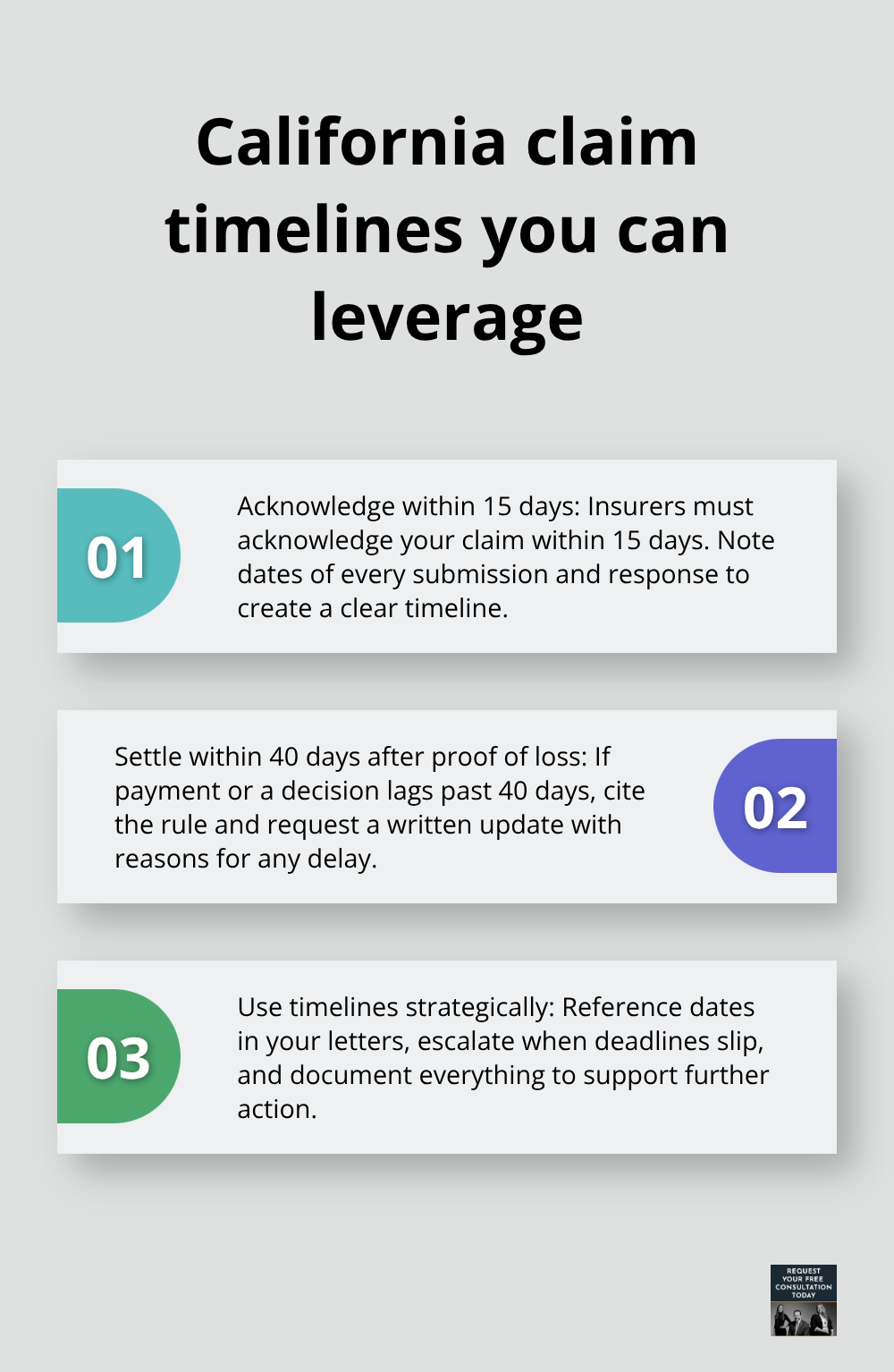

Understand California’s Settlement Timeline Requirements

The timeline for settlement matters significantly in California. The state Department of Insurance requires insurers to acknowledge your claim within 15 days and settle within 40 days after you submit proof of loss. This does not mean the insurer will meet these timelines in practice, but knowing these requirements gives you a legitimate basis to escalate pressure if your claim drags beyond 40 days without fair resolution.

Track all communications with dates and reference these regulatory timelines when the insurer delays. A written reminder that California law sets specific settlement deadlines often accelerates the negotiation process.

Pursue Legal Representation When Negotiations Fail

If the insurer continues to underpay despite your documentation and formal appraisal request, legal representation becomes the practical next step. We at Schaar & Silva LLP evaluate property damage claims and can assess whether pursuing litigation makes financial sense for your specific situation. Do not leave money on the table by accepting a settlement that falls short of what your vehicle damage actually costs to repair.

Final Thoughts

Most claimants in Santa Cruz County accept the first settlement offer without documentation or pushback, leaving thousands of dollars on the table. The gap between what insurers initially offer and what your vehicle actually costs to repair frequently reaches $2,000 to $5,000 or more. This property damage valuation guide equips you with the tools to close that gap through organized documentation, independent repair estimates, and strategic negotiation.

When negotiations reach an impasse or the insurer refuses to adjust despite strong evidence, professional guidance becomes the practical choice. We at Schaar & Silva LLP evaluate property damage claims and help claimants in Santa Cruz County understand whether pursuing legal action makes financial sense for their situation. Our team can review your documentation, assess your claim’s value, and guide you through the next steps if settlement negotiations fail.

Contact us to discuss your claim and determine the best path forward for your recovery. We can help you understand your property damage claim and maximize what you receive from your insurance company.