After a car accident in Santa Cruz, the insurance claim process can feel overwhelming. You’ll face repair valuations, adjuster assessments, and negotiations that directly impact what you receive.

We at Schaar & Silva LLP help accident victims navigate vehicle repairs in Santa Cruz and understand their claims. This guide walks you through how property damage claims work, how fair market value gets determined, and how to push back against lowball offers.

How Insurance Claims Get Processed After an Accident

After a Santa Cruz car accident, your insurance claim enters a structured process governed by California law. The California Department of Insurance requires insurers to acknowledge your claim within 15 days, begin investigation within 15 days, and make a decision within 40 days after you submit proof of loss. Most insurers miss these deadlines, which weakens their negotiating position. Contact your insurance company within 24 hours of the crash and provide the police report, scene photos, initial medical records, and witness information within two weeks.

This speed matters because delays erode your leverage and allow adjusters to construct narratives that minimize your damages. When you call your insurer, document the date, time, and name of the person you speak with. Request written confirmation of your claim number and coverage limits. Do not provide a recorded statement without having an attorney present, especially in serious injury cases.

What the Adjuster Actually Does

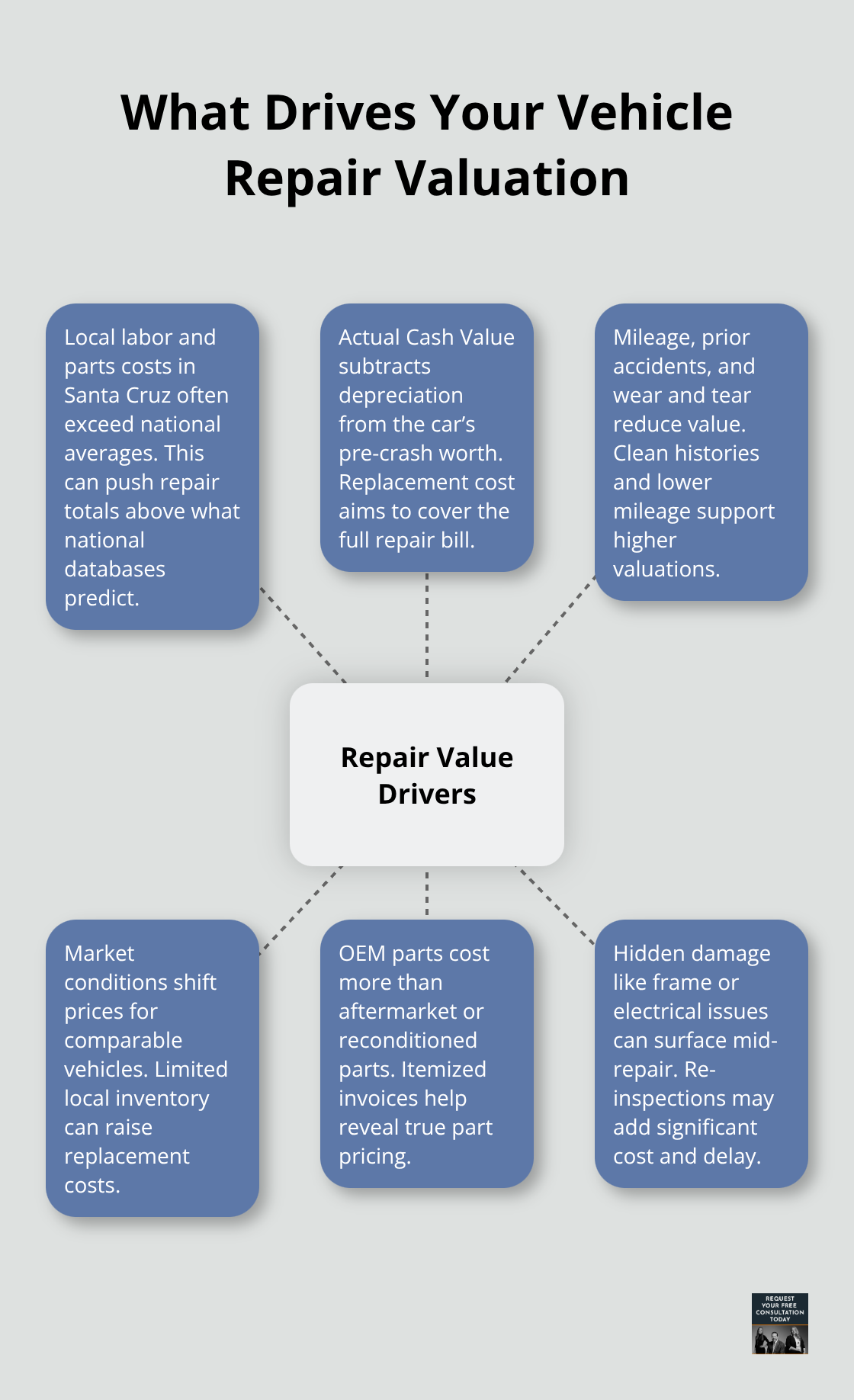

The insurance adjuster inspects your vehicle, estimates repair costs, and determines whether it qualifies as a total loss. In Santa Cruz County, repair costs run 15 to 25 percent higher than national averages because local labor rates and parts availability drive up expenses. This means national valuation databases like NADA Guides consistently underestimate what your repairs actually cost. The adjuster will use one of two valuation methods: actual cash value, which is what your car was worth immediately before the accident, or replacement cost, which covers the full repair bill. Santa Cruz adjusters typically default to actual cash value, the lowest option. Adjusters also look for frame damage, suspension problems, electrical issues, and hidden damage like water intrusion or rust that can add 5,000 to 10,000 dollars to the final repair bill. If additional damage surfaces during repairs, insurers may re-inspect and require approval for extra costs. This is why obtaining three independent repair estimates from certified shops before accepting any settlement offer protects you. Request itemized invoices showing whether parts are OEM, aftermarket, rebuilt, or reconditioned. California law requires shops to disclose part type on repair invoices, and OEM parts cost significantly more than aftermarket alternatives.

Settlement Timelines and Your Options

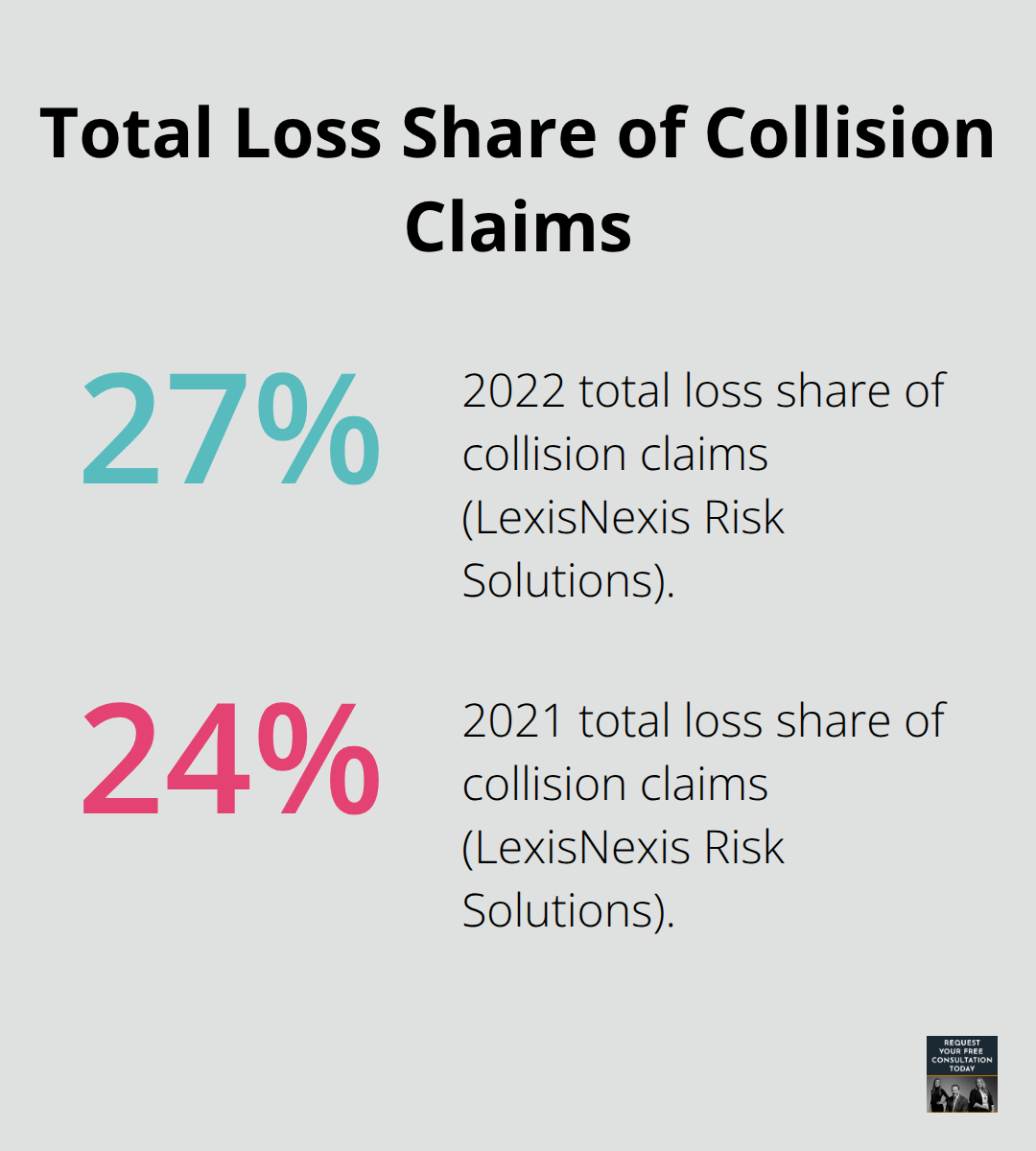

A typical total loss settlement takes a month or more, which is why rental car coverage matters. LexisNexis Risk Solutions found that total loss claims made up 27 percent of collision claims in 2022, up from 24 percent in 2021, and processing times have slowed. State Farm took about 10 weeks to total a 2023 Toyota Corolla XSE in one not-at-fault incident, illustrating real delays you may face.

Initial settlement offers are often 30 to 40 percent below actual repair costs. Counter with three independent local estimates and written explanations of how the pre-accident value and damage estimate were calculated. If the gap between the insurer’s offer and your estimates exceeds 2,000 dollars, California’s Appraisal Provision gives you a binding resolution path: two appraisers plus a neutral umpire determine fair value without litigation. Each party pays its own appraiser, and the umpire fee is split. This process typically costs 300 to 600 dollars and often justifies 2,000 to 5,000 dollars in additional recovery. If negotiations stall, file a complaint with the California Department of Insurance for bad-faith practices.

Moving Forward With Your Claim

The next step involves presenting your evidence to the insurer and preparing for potential negotiations. Understanding how to value your vehicle repair claim and what documentation strengthens your position will determine whether you settle quickly or pursue further action.

What Actually Determines Your Vehicle’s Repair Value

Santa Cruz repair shops charge 15 to 25 percent more than national averages, yet most insurers rely on databases that ignore local costs entirely. NADA Guides, the valuation tool adjusters default to, pulls national data that doesn’t reflect what a Santa Cruz body shop actually charges for labor and parts. This disconnect explains why your initial settlement offer feels low. Adjusters use actual cash value, which subtracts depreciation from what your vehicle was worth the moment before the crash. They factor in mileage, prior accidents, wear and tear, and market conditions. A 2020 Honda Civic with 80,000 miles and a previous fender repair receives a lower valuation than an identical vehicle with 40,000 miles and clean history.

The problem intensifies in Santa Cruz because local repair costs exceed the depreciated value that NADA calculates.

How Local Costs Create Valuation Gaps

When an adjuster tells you your car is worth $12,000 but repairs cost $15,000, the gap exists because the valuation software doesn’t account for regional labor rates and parts availability. You counter this by obtaining three independent repair estimates from certified shops within Santa Cruz County, not the insurer’s preferred vendors. Request itemized breakdowns showing labor rates per hour, which typically run $85 to $125 in Santa Cruz versus $65 to $85 nationally, and parts costs with OEM versus aftermarket pricing clearly separated. California law requires repair invoices to disclose part type, so shops cannot hide cost differences. These local estimates carry significant negotiation weight because California law does not require insurers to rely solely on NADA.

Hidden Damage That Adds Thousands

Hidden damage surfaces in roughly 15 to 25 percent of accident repairs in Santa Cruz, adding $5,000 to $10,000 to the final bill. Inspectors look for frame damage, suspension integrity, electrical system corrosion, water intrusion, and rust that wasn’t visible during the initial adjuster inspection. When additional damage emerges during repair, the insurer may demand re-inspection and approval before proceeding. This delay tactic pressures you to accept lower settlements. Photographs taken immediately after the accident from multiple angles plus maintenance records counter claims of pre-existing damage. If you kept service records showing your vehicle was in good condition before the crash, the adjuster cannot attribute wear or rust to your accident.

Building Your Case With Independent Evidence

A certified independent appraiser, costing $300 to $600, documents pre-crash condition and current market data using local comparables. This appraisal often justifies $2,000 to $5,000 in additional recovery. Keep all communications with the adjuster in writing and request written explanations of how pre-accident value and damage estimates were calculated. If the gap between the insurer’s offer and your independent estimates exceeds $2,000, the California Appraisal Provision provides a binding resolution without litigation. Two appraisers plus a neutral umpire determine fair value, with each party paying its own appraiser and splitting the umpire fee. This process typically costs $300 to $600 total and often justifies $2,000 to $5,000 in additional recovery.

Once you’ve gathered your repair estimates and documentation, the next step involves presenting this evidence to the insurer and preparing for negotiations that will determine whether you settle quickly or pursue further action.

How to Win Negotiations With Your Insurance Company

Organize and Present Your Evidence

Presenting your evidence correctly determines whether you settle for thousands less or receive fair compensation. Start by organizing everything into a single document: the police report, your three independent repair estimates with itemized breakdowns, photographs from multiple angles taken immediately after the crash, maintenance records proving pre-accident condition, and the adjuster’s written valuation. Request written explanations from the adjuster showing exactly how they calculated pre-accident value and damage estimates. Send all of this to the insurer via email so you have proof of delivery. The adjuster will likely counter with their preferred valuation tool, but California law does not require insurers to rely solely on NADA Guides, which means your local Santa Cruz estimates carry significant weight.

Expose the Local Cost Gap

If the insurer’s offer sits 30 to 40 percent below your independent estimates, that gap exists because national databases ignore local labor rates of $85 to $125 per hour versus the $65 to $85 national average. Make this explicit in your response: calculate the difference between what NADA shows and what Santa Cruz shops actually charge, then present that calculation alongside your itemized invoices. Adjusters often increase their offers once they see concrete local pricing because the math becomes undeniable. This approach transforms a vague dispute into a documented fact that the insurer cannot ignore.

Counter Lowball Offers With Firm Demands

Lowball offers require aggressive pushback, not politeness. If the insurer’s initial settlement offer falls short, do not accept it or negotiate incrementally upward. Instead, set a firm deadline of 30 days for their response and propose a number that accounts for 25 to 40 percent more than your documented economic losses to cover non-economic damages like inconvenience and time lost. If they reject this and the gap between their offer and your estimates exceeds $2,000, invoke California’s Appraisal Provision immediately.

Use the Appraisal Provision as Leverage

Two independent appraisers plus a neutral umpire determine binding fair value without litigation, costing roughly $300 to $600 total and often justifying $2,000 to $5,000 in additional recovery. This process carries real leverage because insurers know the umpire will likely side with your documented evidence. The appraisal provision removes the insurer’s ability to drag out negotiations indefinitely. Once you file for appraisal, the timeline accelerates and the stakes shift in your favor.

Escalate to Regulatory Complaints and Legal Action

If the insurer still refuses or delays beyond the 40-day California Department of Insurance deadline, file a complaint with the state regulator for bad-faith practices. Most insurers respond quickly once they receive a bad-faith notice. When negotiations stall despite your documentation and appraisal demand, contact Schaar & Silva LLP to evaluate whether your case warrants legal representation and potential litigation.

Final Thoughts

Vehicle repairs in Santa Cruz cost 15 to 25 percent more than national averages, which means your initial insurance settlement offer will likely fall short of actual repair expenses. The gap between what NADA Guides calculates and what local shops charge is real, measurable, and worth fighting for. Your three independent repair estimates from certified Santa Cruz shops carry significant legal weight because California law does not require insurers to rely solely on national databases.

The appraisal provision gives you a binding resolution path without litigation when the gap between offers exceeds $2,000. Two appraisers plus a neutral umpire determine fair value, typically costing $300 to $600 and often justifying $2,000 to $5,000 in additional recovery. This process removes the insurer’s ability to drag out negotiations indefinitely and shifts leverage in your favor.

If negotiations stall despite your documentation and appraisal demand, file a complaint with the California Department of Insurance for bad-faith practices. When further action becomes necessary, contact Schaar & Silva LLP to evaluate whether your case warrants representation and potential litigation.