A car accident can leave you dealing with significant vehicle damage and the stress of navigating insurance claims. The path to getting your car repaired and receiving fair reimbursement involves several important steps that many people overlook.

We at Schaar & Silva LLP have helped countless accident victims in Santa Cruz County, Sacramento, and Oakland understand their options and recover what they’re owed. This guide walks you through the process from damage assessment to final reimbursement.

Assessing Your Vehicle Damage

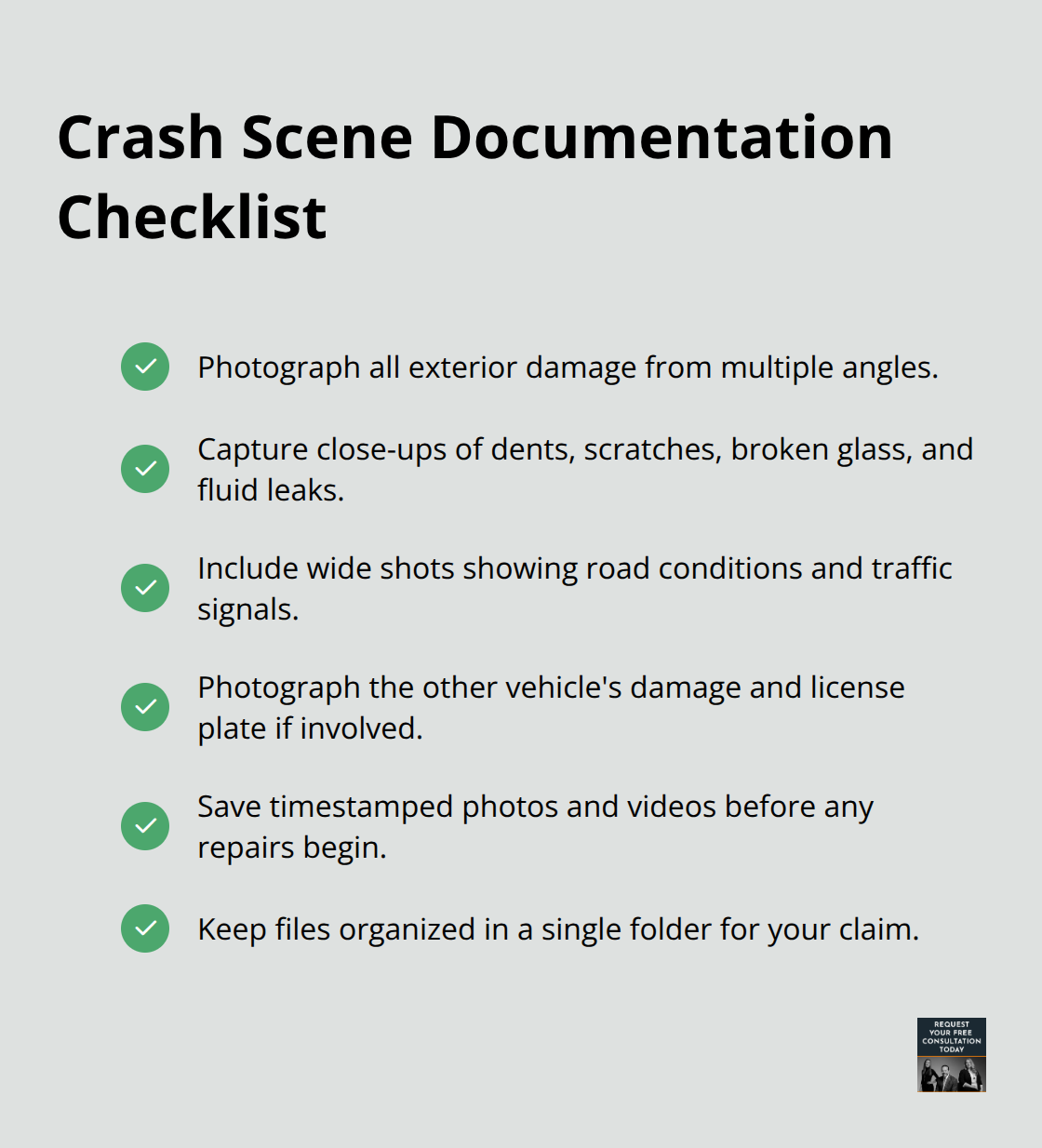

The first hours after an accident are critical for protecting your property damage claim. Most people rush to move their vehicle or call their insurance company before documenting anything, which is a mistake. You need photographic evidence of the damage before repairs begin, and you need a police report that establishes the facts of the accident. Insurance adjusters will question claims that lack proper documentation, and without clear evidence, you’ll struggle to negotiate fair compensation.

Document the Scene with Photos and Videos

Take photos and videos from multiple angles while the vehicle remains at the accident scene. Capture close-ups of all visible damage, including dents, scratches, broken glass, and fluid leaks. If the accident involved another vehicle, photograph the damage to that vehicle as well, plus the license plate and the accident scene itself (including road conditions and traffic signals). This visual record becomes your strongest tool when negotiating with insurance companies.

Obtain a Police Report for Your Records

Request the police report from the law enforcement agency that responded to your accident. The report number and officer details should appear on any citation or accident report you received at the scene. Request the full report, not just a summary, because adjusters will review it carefully when evaluating liability. This document establishes the officer’s assessment of fault and the accident circumstances.

Get a Professional Damage Assessment from a Mechanic

Schedule an appointment with a qualified mechanic for a professional damage assessment. Do not rely on insurance company estimates alone. A mechanic you trust can identify hidden damage that may not be visible during an initial inspection, such as frame damage, alignment issues, or internal mechanical problems that only surface during repair work. Many repair shops offer free estimates and will document their findings in writing.

Obtain at least two estimates from different shops so you have multiple professional opinions on repair costs. Insurance adjusters often lowball their initial estimates, and having competing quotes gives you leverage during negotiations. Keep all estimates, photos, police reports, and repair receipts organized in a single folder or file. This documentation proves both the extent of your damage and the cost of repairs-the two elements adjusters must verify before paying your claim.

With your damage assessment complete and documentation in hand, you’re ready to move forward with your insurance claim. The next step involves understanding your coverage options and submitting everything to your insurance company for review.

Filing Your Insurance Claim

Now that you have documented your damage and gathered your evidence, you need to file your insurance claim with your insurance company. Your coverage options determine what you can recover, and understanding these options before you file makes a significant difference in your final reimbursement.

Understanding Your Coverage Options

Most California drivers carry collision coverage, which pays for repairs to your vehicle regardless of who caused the accident, though you pay your deductible out of pocket. If the other driver was at fault, you can file a claim against their liability insurance instead, which means their company pays for repairs without you paying a deductible. However, this approach takes longer because you deal with another company’s claims process. Some drivers also carry comprehensive coverage, which covers damage from events like theft, weather, or vandalism. Review your policy documents carefully before filing to understand exactly what your coverage includes and what your deductible is.

Submitting Your Documentation to Insurance

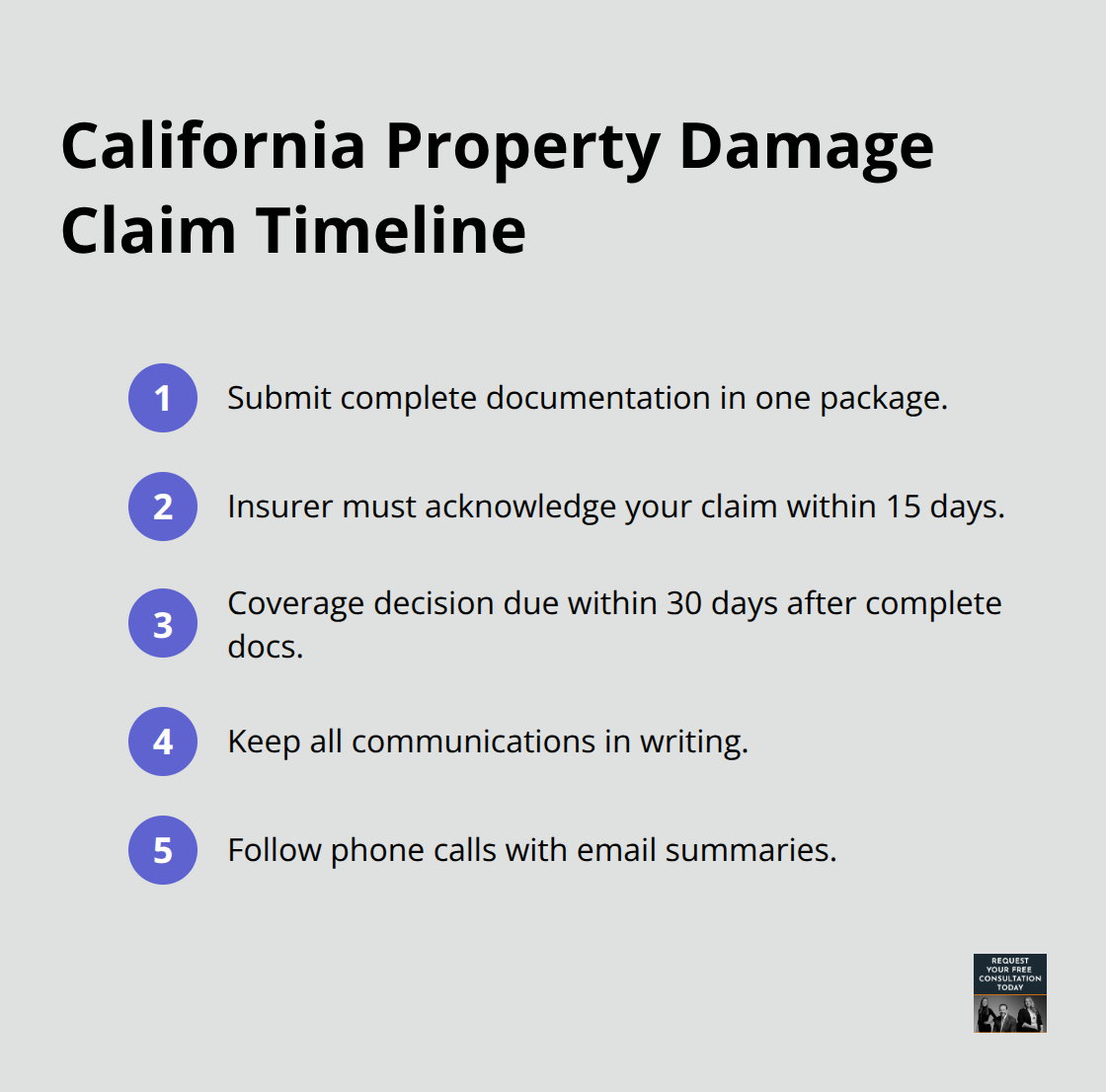

When you submit your claim, provide everything at once: your photos, the police report, all repair estimates, and proof of any expenses you’ve already incurred. Insurance companies in California must acknowledge your claim within 15 days and make a coverage decision within 30 days after you submit complete documentation, according to state regulations. Document every communication with your adjuster in writing, whether through email or by following up phone calls with written summaries.

Negotiating Fair Compensation for Repairs

The initial settlement offer from an insurance adjuster is rarely their best offer, so don’t accept the first number they propose without negotiation. Adjusters often employ tactics to minimize payouts, such as questioning the accuracy of repair estimates, pushing you toward cheaper aftermarket parts instead of original manufacturer parts, or suggesting that some damage existed before the accident. When the adjuster’s estimate falls short of your repair quotes, respond with specific documentation showing why their estimate is incomplete, such as frame alignment work, hidden structural damage, or safety system repairs that only appeared during initial teardown. If your vehicle needs original manufacturer parts for safety components, insist on them rather than accepting aftermarket alternatives, especially on newer vehicles where fit and performance matter.

Handling Total Loss and Fault Situations

For total loss situations, California insurers should pay fair market value based on vehicles comparable to yours in your local area, not just book value, so research current listings of similar vehicles to support your valuation. If you’re at fault for the accident, contact your own insurance company immediately, as your collision coverage will apply minus your deductible. If negotiations stall or the insurer denies your claim unfairly, you have the right to dispute their decision through the company’s formal appeals process or seek a free legal consultation with an attorney who can review your case and potentially recover more than you could alone.

Once your claim moves through the insurance process, you’ll need to decide how to handle the actual repairs and get your vehicle back on the road.

Getting Your Vehicle Repaired After Settlement

Choosing the Right Repair Shop

Once your insurance company approves your claim, you face a critical decision about where to repair your vehicle. You can choose any repair shop you want, not just the insurer’s preferred vendors, and this choice matters more than most people realize. Insurance companies push customers toward their network shops because those facilities often accept lower labor rates and use aftermarket parts without question, which reduces the insurer’s payout. Independent repair shops and dealerships typically charge fair market rates and stand behind their work with longer warranties.

If your vehicle is newer or has complex safety systems, choosing a dealership or certified shop prevents cheap repairs from masking underlying damage that surfaces months later. Most quality shops in Sacramento and the surrounding areas charge between $75 and $150 per hour for labor, so compare rates when selecting your facility. Ask whether the shop uses original manufacturer parts or aftermarket alternatives, and insist on original parts for safety-critical components like brakes, airbag sensors, or suspension systems where fit and performance directly affect your safety.

Understanding Repair Timelines and Costs

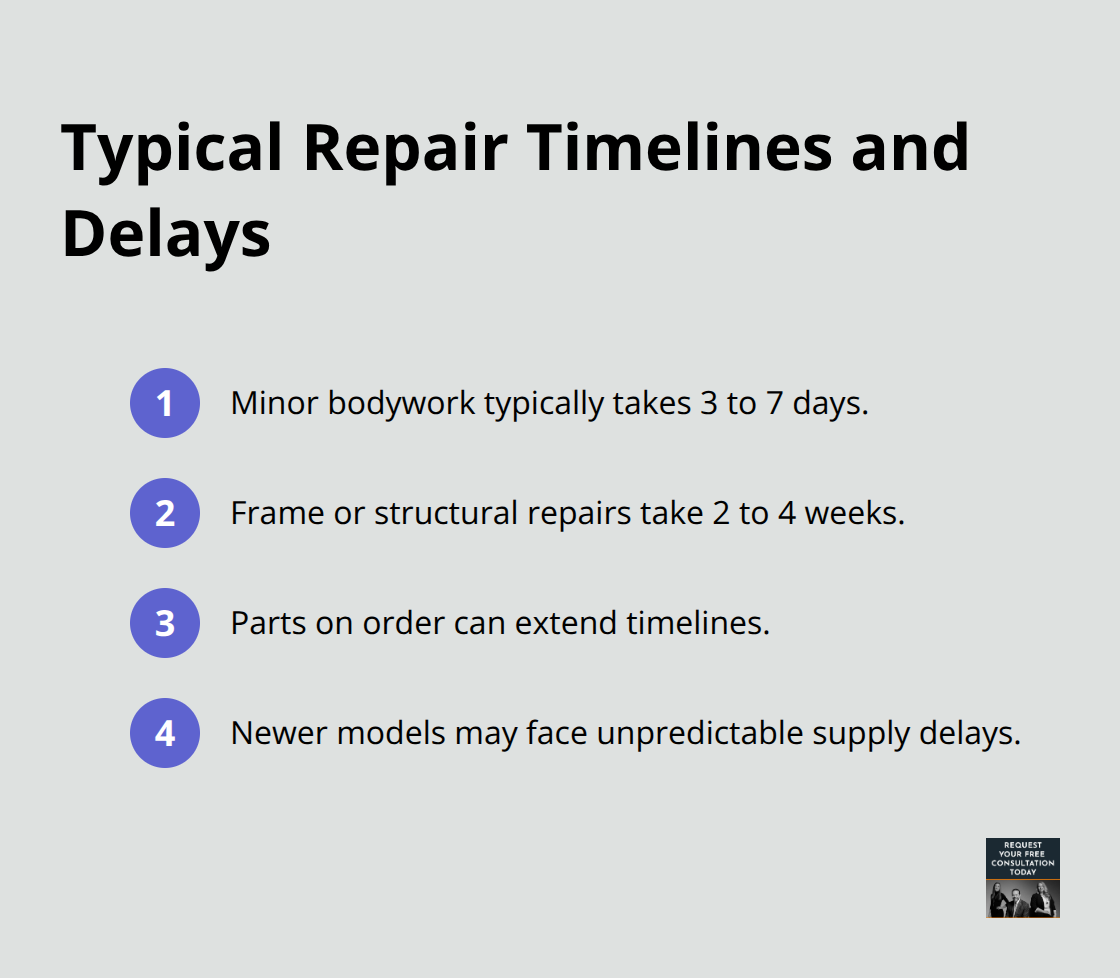

Repair timelines vary significantly based on damage severity and parts availability. Minor damage like dents and paint work typically takes three to seven days, while frame damage or structural repairs can stretch to two to four weeks. If your vehicle requires parts ordered from manufacturers, expect additional delays, especially for newer models where supply chains remain unpredictable.

Get your repair estimate in writing before work starts, and request that the shop contact you before starting any additional work beyond what the estimate covers. If the repair shop discovers additional hidden damage during teardown, they must obtain your written approval before proceeding, and your insurance adjuster will review the supplemental estimate. If repairs exceed the original estimate by more than 10 percent, ask the shop to explain the discrepancy in writing before authorizing additional work.

Managing Rental Vehicle Costs

During repairs, your insurance company should cover rental vehicle costs if your policy includes rental reimbursement, which typically caps at $30 to $50 per day depending on your coverage limits. Keep all rental receipts and submit them with your final claim documentation. Request daily updates from your repair shop on progress, and don’t accept vague timelines.

Inspecting Your Repaired Vehicle

Once repairs complete, inspect your vehicle thoroughly before paying the final bill, checking paint quality, alignment, and all repaired components to confirm work meets your standards. This final walkthrough protects you from accepting substandard work and ensures the shop addressed all damage properly. If you notice issues during inspection, document them with photos and request corrections before releasing payment.

Final Thoughts

Car accident property damage claims require organization, persistence, and knowledge of your rights. The steps outlined in this guide-documenting damage thoroughly, understanding your coverage, negotiating with adjusters, and selecting quality repair shops-form the foundation of a successful claim. Most people accept less than they deserve because they lack proper documentation or fail to push back against lowball offers from insurance companies.

Property damage claims often involve more complexity than drivers expect, especially when hidden damage surfaces during repairs or when insurers deny coverage unfairly. If your claim stalls, the insurer disputes liability, or you suspect you’re being offered less than fair value, legal guidance can make a significant difference. We at Schaar & Silva LLP help accident victims in Santa Cruz County, Sacramento, and Oakland evaluate the extent of their vehicle damage and work toward fair valuations for their losses.

Our team handles the legal details while you focus on moving forward, and we can review your case at no cost to determine whether pursuing additional compensation makes sense for your situation. Contact us to discuss your accident and learn what options are available to you.