A car accident is stressful enough without discovering the other driver has no insurance. Thousands of drivers in Santa Cruz County, Sacramento, and Oakland operate vehicles without coverage, leaving accident victims facing serious financial hardship.

Uninsured motorist claims exist to bridge this gap, but the process is complex and many people don’t understand their options. We at Schaar & Silva LLP help accident victims recover the compensation they deserve when facing this situation.

Who Counts as an Uninsured Motorist in California

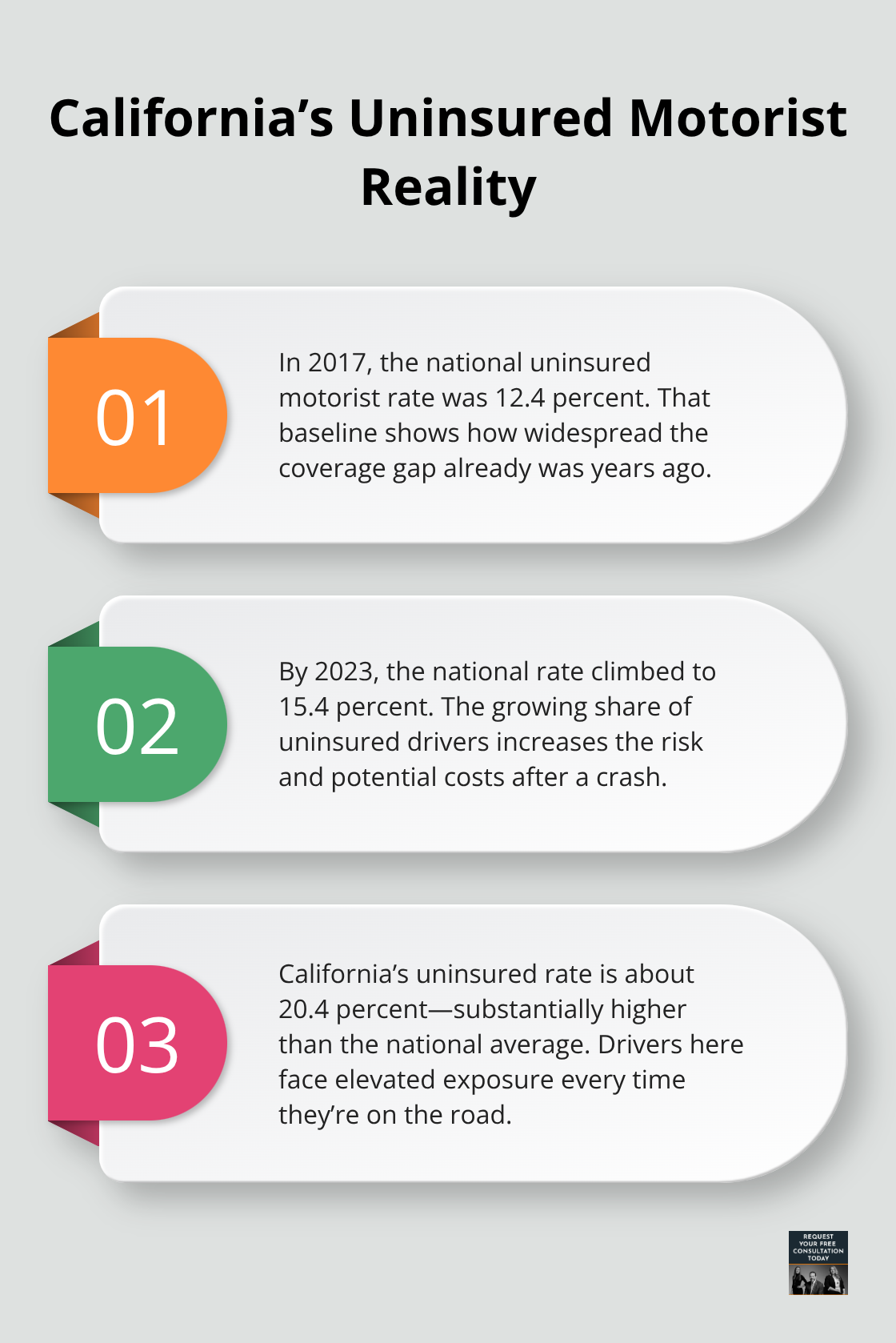

An uninsured motorist is any driver operating a vehicle without active auto insurance coverage. In California, state law requires all drivers to carry minimum liability insurance, yet thousands ignore this requirement. According to the Insurance Research Council, approximately 16 to 17 percent of drivers in the Santa Cruz, Sacramento, and Oakland metro areas operate without insurance. This means roughly one in six vehicles you encounter on the road carries no coverage whatsoever.

The Growing Problem in Your Region

The problem has worsened significantly since 2017, when the national uninsured rate stood at 12.4 percent. The Insurance Research Council reported that by 2023, this number climbed to 15.4 percent nationally, with California’s uninsured rate sitting substantially higher than the national average at around 20.4 percent. In practical terms, if you’re in an accident tomorrow, there’s a meaningful chance the other driver has zero insurance protection.

What UM Coverage Actually Pays For

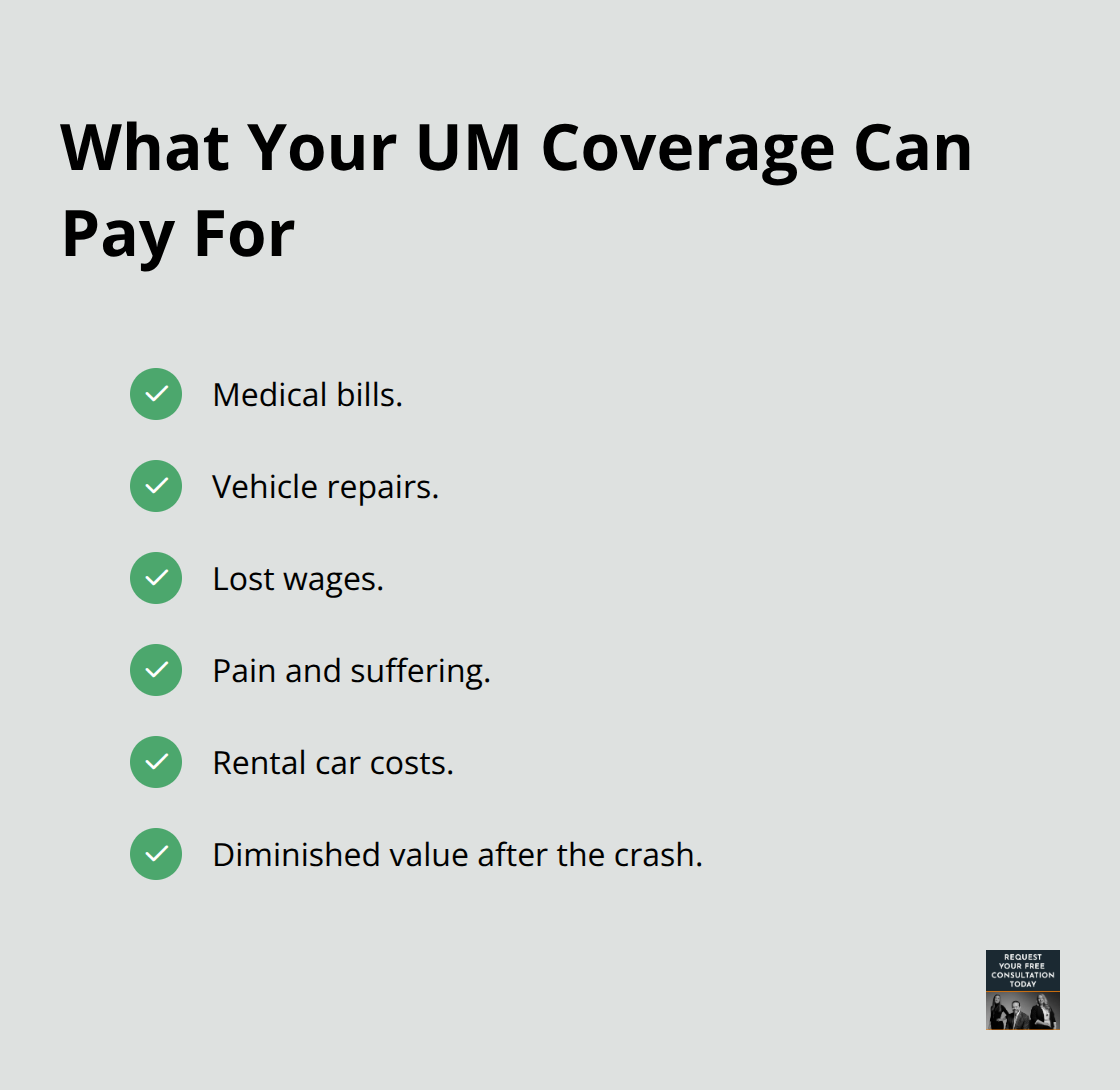

When an uninsured motorist causes your accident, your own uninsured motorist coverage becomes your lifeline. This coverage pays for your medical bills, vehicle repairs, lost wages, pain and suffering, and rental car costs when the at-fault driver lacks insurance or cannot be identified in hit-and-run situations. Without UM coverage, you absorb these expenses yourself.

The Financial Reality of Skipping UM Coverage

Many accident victims in your area skip UM coverage to save roughly twenty dollars monthly, then face catastrophic financial gaps after a serious crash. The California Department of Insurance and the Insurance Research Council both emphasize that UM coverage operates separately from your collision insurance, typically carrying a lower deductible of around $250 compared to collision deductibles that often exceed $1,000. This distinction matters significantly when managing recovery costs.

What Happens Without UM Protection

If you were hit by an uninsured driver and lack UM coverage, you’d need to pursue the at-fault driver directly through small claims court or civil litigation-a lengthy, uncertain process that frequently yields nothing if that driver has no assets or income to recover from. UM coverage bypasses this frustration entirely, allowing you to file a claim against your own policy and recover damages promptly. Understanding how your own policy protects you sets the foundation for navigating the claims process itself.

How Your UM Coverage Actually Works

Your uninsured motorist coverage operates through your own insurance policy, not the other driver’s. When an uninsured motorist causes your accident, you file a claim with your own insurer, who then investigates liability and compensates you for damages up to your policy limits. This direct relationship with your own insurance company differs fundamentally from pursuing the at-fault driver. California Insurance Code Section 11580.2 governs how insurers must handle these claims, including investigation timelines and your right to arbitration if disputes arise about fault or the value of your damages.

Notify Your Insurer Immediately

Most policies require you to notify your insurer promptly after an accident, typically within days rather than weeks. Failing to give timely notice can jeopardize your coverage, so contact your insurance company before discussing details with anyone else. Request your full policy documents immediately, paying close attention to stacking provisions, exclusions, and how UM coverage interacts with collision and medical payments coverage. Your UM deductible typically runs $250, considerably lower than collision deductibles that often exceed $1,000, which means you’ll pay less out of pocket when filing a UM claim versus a collision claim for the same accident.

What UM Coverage Pays and What It Doesn’t

UM coverage pays for medical bills, vehicle repairs, lost wages, pain and suffering, rental car costs, and diminished value if your vehicle’s market value drops after the crash. The Insurance Research Council confirms that this coverage applies whether the at-fault driver has no insurance whatsoever or cannot be identified in hit-and-run situations where documented vehicle contact occurred.

However, UM coverage does not pay for traffic tickets, criminal fines, or punitive damages in most California policies. Many policies also exclude coverage if you operated a vehicle illegally or if the at-fault driver was a household member covered under your policy.

Review your specific policy language carefully, as exclusions vary between insurers. Set your UM limits high enough to cover your vehicle’s replacement cost plus anticipated medical expenses, since California’s minimum liability limits of $30,000 per person often fall short for serious injuries. You can typically increase UM coverage in $5,000 increments, and a practical rule of thumb suggests setting limits at least equal to your vehicle’s replacement value.

Understanding Arbitration in UM Claims

Arbitration is common in California UM claims when disputes arise about liability or damages. Your policy likely includes mandatory arbitration language requiring binding arbitration rather than court proceedings for disagreements between you and your insurer. This process typically moves faster than litigation but removes your right to a jury trial. If your insurer denies or significantly undervalues your claim, understanding arbitration provisions in your policy becomes critical.

The statute of limitations for UM claims is two years under California Code of Civil Procedure Section 335.1, though your policy’s arbitration deadlines may be shorter. Document everything meticulously from the moment of impact, as damages are heavily document-driven in UM claims. Maintain organized records of medical treatment, receipts, lost wages, and any communication with your insurer.

Bad Faith Handling and Your Rights

If an insurer denies your claim or handles it in bad faith under California Insurance Code Section 790.03, you may recover damages beyond your policy limits and attorney fees. Early legal involvement matters significantly for protecting your rights and ensuring fair treatment throughout the process. When disputes over claim value or liability emerge, having someone review your policy language and deadlines can make the difference between a denied claim and full recovery. The next step involves understanding exactly how to file your claim and what documentation strengthens your position from day one.

Steps to File an Uninsured Motorist Claim

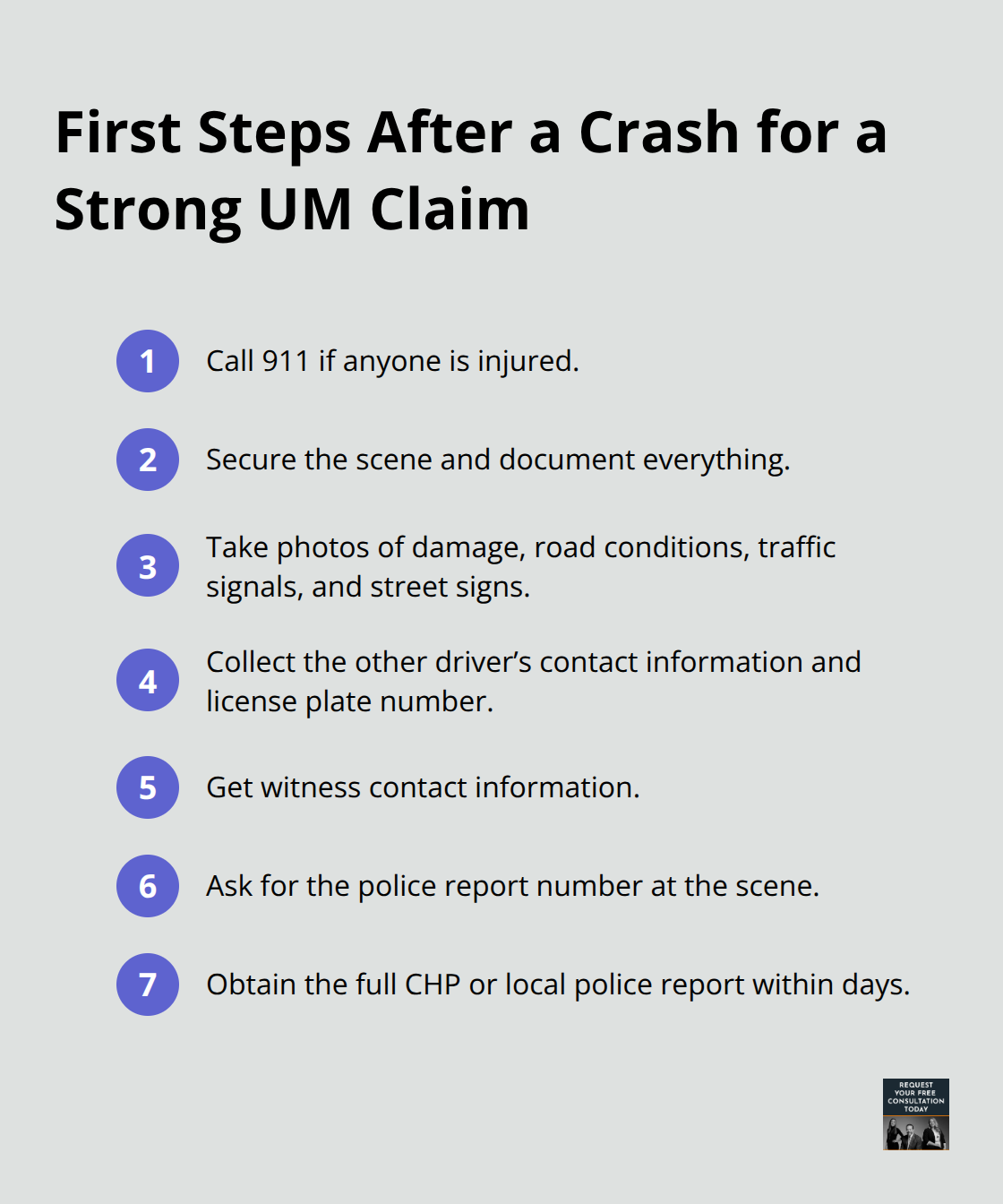

The moments immediately after an accident determine whether your UM claim succeeds or fails. Call 911 if anyone is injured, then secure the scene and document everything before leaving the accident location. Take photos of vehicle damage from multiple angles, road conditions, traffic signals, and street signs that show the intersection or location. Collect the other driver’s name, phone number, address, and license plate number. Get contact information from any witnesses who saw the collision, as their statements often carry significant weight in UM disputes. Request the police report number from the officer at the scene, then obtain the full report from the California Highway Patrol or local police department within days.

The CHP accident report provides critical corroboration of liability and timelines that your insurer will examine closely.

Notify Your Insurer Without Delay

Notify your insurance company within 24 to 48 hours of the accident, never weeks later. When you call, state only the basic facts: date, time, location, and that the other driver had no insurance or fled the scene. Do not provide a recorded statement or sign blanket medical authorization forms before consulting with someone who understands policy language and claim tactics. Insurance adjusters contact victims within hours with recorded statements specifically designed to lock you into statements that limit your recovery. Request your full policy documents immediately, including your UM endorsements, arbitration provisions, exclusions, and how UM interacts with collision and medical payments coverage. California Insurance Code Section 11580.2 requires insurers to provide these documents promptly.

Build Your Evidence File Immediately

Seek medical care immediately after the accident, even if you feel fine, since adrenaline masks injuries that emerge days or weeks later. Maintain meticulous records of every medical visit, test, prescription, and expense. The Insurance Research Council confirms that damages in UM claims are heavily document-driven, meaning your organized medical records directly determine your settlement value. Preserve all receipts for lost wages, transportation costs, and rental car expenses. Request CHP accident reports and California Department of Motor Vehicles records early, as these documents strengthen your evidence file significantly.

When Legal Representation Becomes Essential

Many accident victims in Santa Cruz County and surrounding areas attempt UM claims alone, then face insurer denials or significant undervaluations that force them to settle for pennies on the dollar. If your injuries are serious, if liability is disputed, or if the insurer delays payment beyond 30 days, legal representation becomes essential. Someone familiar with UM claims understands your insurer’s investigation tactics, knows which damages to document, and prevents you from making statements that reduce your recovery. If your insurer denies your claim or handles it in bad faith, you have two years under California Code of Civil Procedure Section 335.1 to file a claim, though policy arbitration deadlines may be shorter. Early legal involvement creates a record and prompts insurers to reconsider denials. The legal team at Schaar & Silva LLP handles the communication with your insurer, compiles documented losses, and protects your rights throughout the process. If disputes arise about liability or claim value, your policy likely includes mandatory arbitration rather than court proceedings, which moves faster but removes your jury trial right.

Managing Medical Costs While Your Claim Resolves

Medical expenses often accumulate faster than your claim resolves. Many medical facilities in the Oakland, Sacramento, and Santa Cruz areas participate in medical lien arrangements, allowing providers to defer payment until your case settles. Ask your healthcare provider directly whether they accept liens, then provide their contact information to your insurer. The California Victim Compensation Program can also cover medical expenses, lost wages, and counseling if you apply through your county’s victim services office. Maintain ongoing medical treatment throughout your claim, since gaps in care weaken the damages portion of your case. Document everything consistently: each visit, diagnosis, treatment plan, and cost. This documentation becomes your strongest evidence when your insurer calculates what your injuries are worth.

Final Thoughts

Uninsured motorist claims demand careful attention to detail and timely action from the moment of impact through settlement. Document the accident scene thoroughly, notify your insurer within 24 to 48 hours, and avoid recorded statements before understanding your policy. Set your UM limits high enough to cover vehicle replacement costs plus anticipated medical expenses, since California’s minimum liability limits often fall short for serious injuries.

The reality facing accident victims in Santa Cruz County, Sacramento, and Oakland is stark: roughly one in six drivers carries no insurance. Even with UM coverage, insurers sometimes deny claims or undervalue damages, leaving victims with far less than they deserve. Early legal involvement prevents these outcomes by ensuring your insurer handles your claim fairly and your rights remain protected throughout the process.

We at Schaar & Silva LLP help accident victims navigate uninsured motorist claims by handling communication with your insurer, compiling documented losses, and protecting your rights. Contact us today to discuss your situation and learn how we can help you recover the compensation you deserve.