Getting hit by an uninsured motorist in Santa Cruz County leaves you vulnerable and confused about what happens next. You’re facing medical bills, vehicle damage, and uncertainty about who pays for it all.

At Schaar & Silva LLP, we help accident victims navigate these situations and recover the compensation they deserve. This guide walks you through your rights, your coverage options, and how to move forward after a collision with an uninsured driver.

Who Are Uninsured Motorists and Why Do They Matter in Santa Cruz

Understanding Uninsured Motorists in California

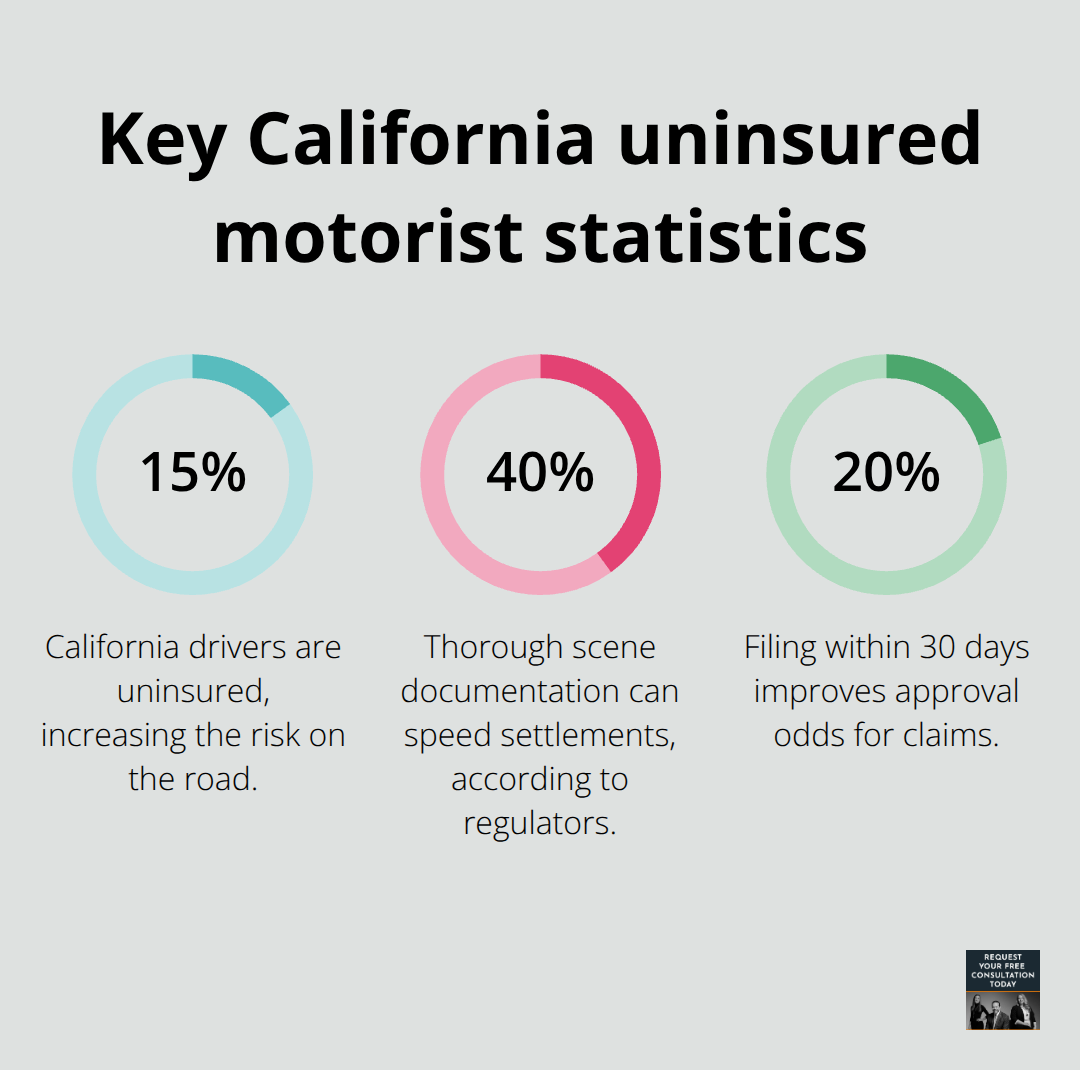

An uninsured motorist is a driver operating a vehicle without active liability insurance coverage, which is illegal in California. The California Department of Insurance reports that approximately 15% of California drivers are uninsured, and Santa Cruz County experiences higher rates of hit-and-run incidents and bicycle crashes, making this a serious local concern. California law requires all drivers to carry minimum liability coverage of $15,000 per person and $30,000 per accident for bodily injury, plus $5,000 for property damage. When a driver hits you without this required coverage, you face the financial burden unless you have uninsured motorist protection on your own policy.

Why Drivers Skip Insurance

Some drivers can’t afford premiums, while others lose coverage due to missed payments or policy lapses. A smaller group deliberately chooses to drive uninsured and accepts the legal risk. The California Department of Insurance reports that uninsured drivers cause a disproportionate number of accidents relative to their percentage of the driving population, meaning your odds of encountering one in Santa Cruz are higher than in many other regions.

How Uninsured Motorist Coverage Protects You

When an uninsured motorist hits you, uninsured motorist bodily injury coverage protects you for medical expenses, lost wages, pain and suffering, and vehicle damage up to your policy limits through your own insurance. California law requires insurers to offer this coverage; you can decline it only in writing. This coverage works differently from normal liability claims because you file through your own insurer rather than pursuing the at-fault driver directly, which simplifies the process but requires thorough documentation of your injuries and losses.

Property damage coverage under uninsured motorist protection generally caps around $3,500, so if your vehicle is worth more, collision coverage becomes essential backup protection. Understanding these options matters because many accident victims don’t realize their own policy can cover them when the other driver has no insurance.

Your next step involves knowing exactly what to do immediately after the collision occurs.

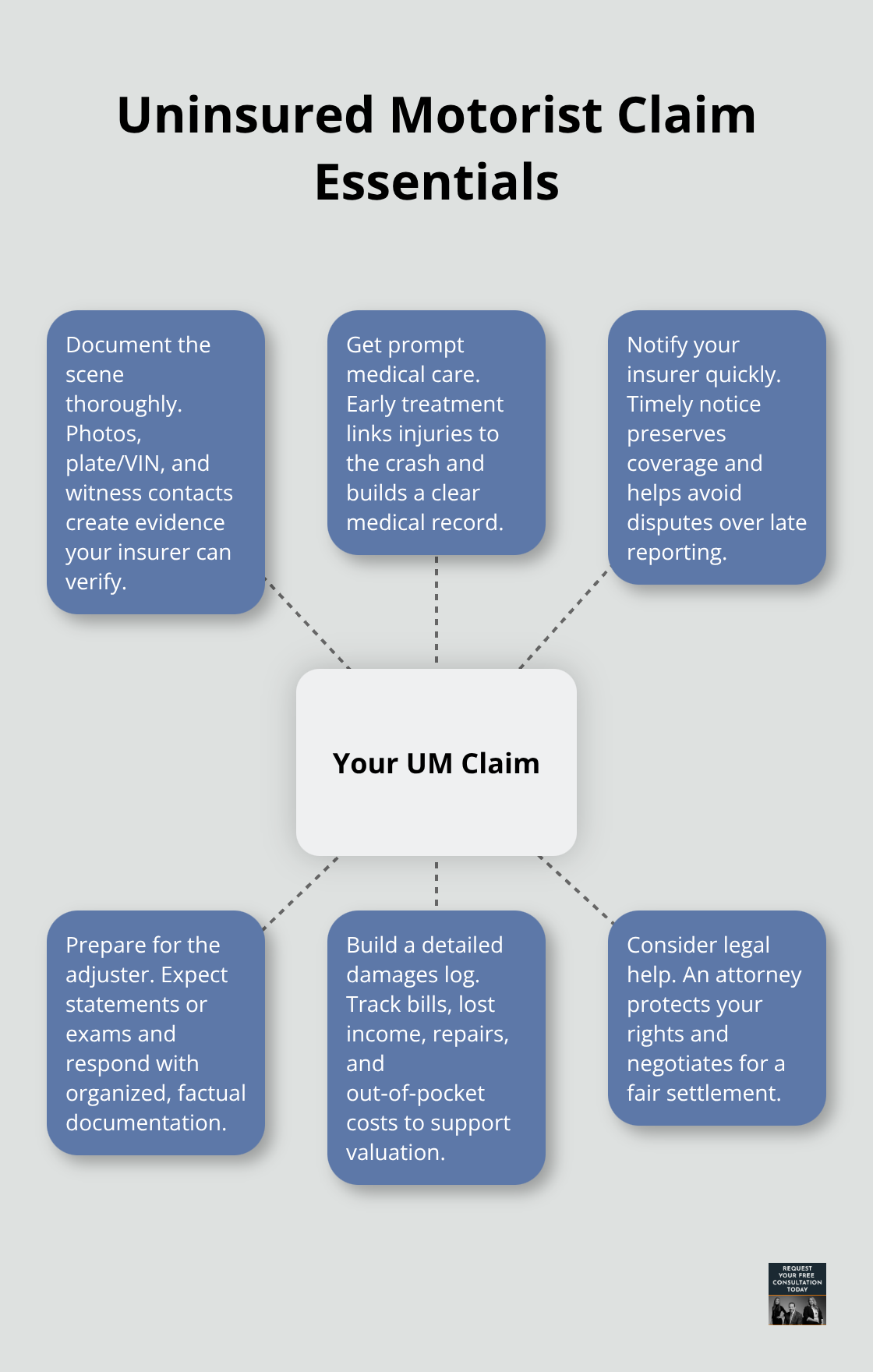

What Happens Right After You Get Hit

Document Everything at the Scene

The first 24 hours after an accident with an uninsured motorist determine the strength of your entire claim. Call 911 immediately if anyone is injured, and request a California Highway Patrol report even for minor collisions. Move to a safe location if possible, and at the scene, photograph the other driver’s license plate, vehicle identification number, damage to both vehicles, and the accident scene from multiple angles. Collect the at-fault driver’s name, address, license number, and insurance information, and note whether they admit to being uninsured. Obtain contact information from any witnesses, as their statements significantly strengthen your case. According to the California Department of Insurance, comprehensive documentation at the scene can speed settlements by roughly 40 percent.

Notify Your Insurance Company Quickly

Within 24 hours, notify your own insurance company with accurate details about the accident and any injuries, even if you feel fine. The California Department of Insurance reports that filing within 30 days improves approval odds by about 20 percent.

Seek medical attention immediately, as adrenaline masks injuries that may not appear until days after the collision. Keep all medical receipts, treatment records, and documentation of lost wages from work, as these form the foundation of your damages claim.

Prepare for the Adjuster’s Process

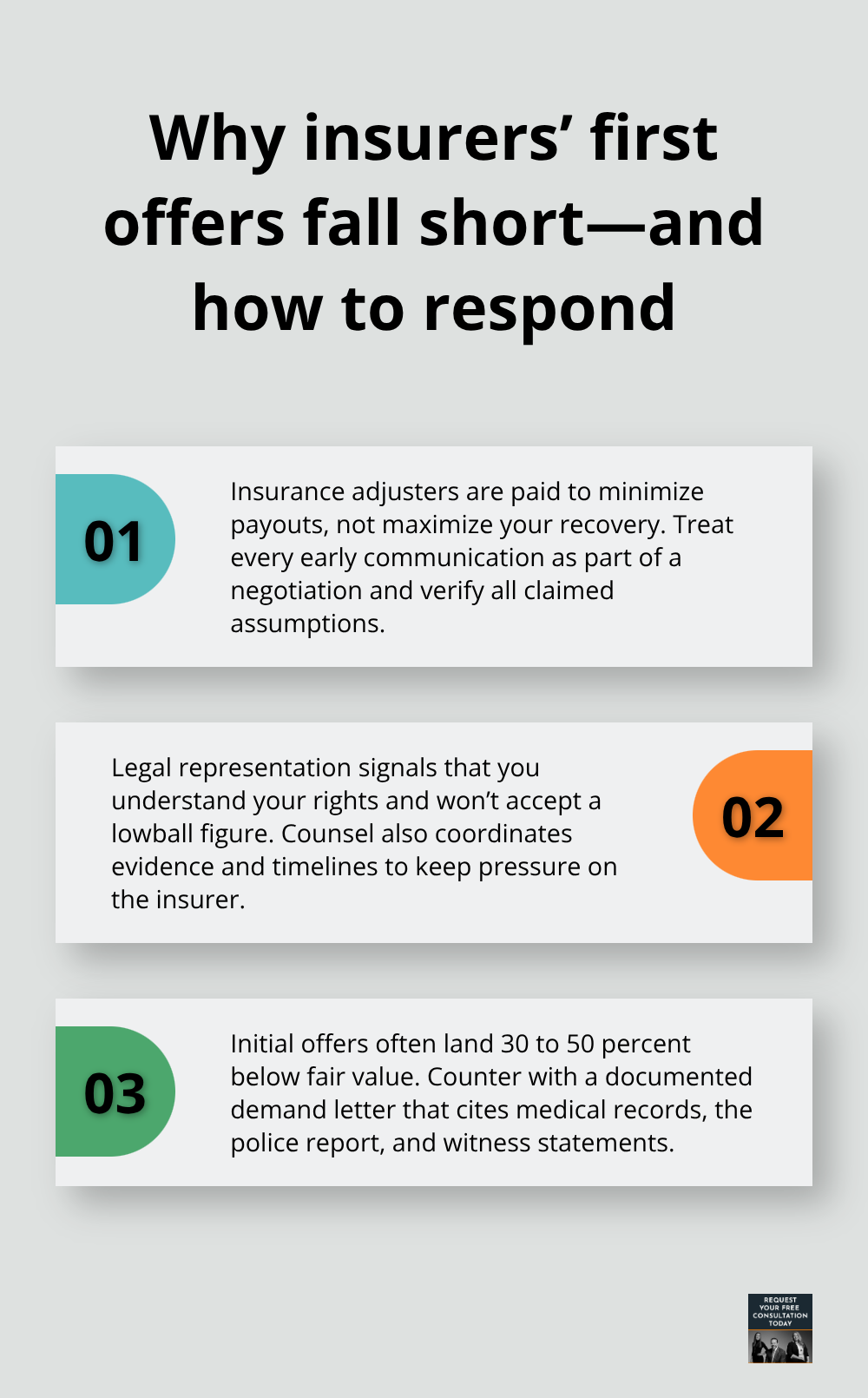

Your insurance company will assign an adjuster to your case, and they may request a recorded statement or require an independent medical examination (this is standard practice, so prepare yourself mentally for these interactions). Do not accept the insurance company’s initial offer without careful consideration; according to the California Department of Insurance, insurers’ first offers typically fall 30 to 50 percent below fair value. Instead, respond with a formal demand letter that cites your documented damages, the police report, witness statements, and medical records.

Build Your Damages Log

Organize all your expenses into a damages log covering medical costs, rehabilitation, prescriptions, transportation, income loss, car rental, and any other accident-related expenses. Your claim includes both economic damages (medical bills, lost wages, vehicle repairs) and non-economic damages (pain and suffering), and presenting documented evidence for both components strengthens your negotiating position. California law provides a two-year statute of limitations to file a personal injury claim, so starting this process early preserves evidence and maintains negotiation leverage. The California Department of Insurance enforces strict timelines: insurers must acknowledge claims within 15 days, respond to communications within 15 days, and accept or deny claims within 40 days after you submit proof of loss.

Once you understand the claims process, the next critical step involves knowing when and how to pursue legal action against the at-fault driver.

How We Can Help With Your Uninsured Motorist Claim

Why Insurance Adjusters Work Against Your Interests

Insurance adjusters work for the insurance company, not for you, and their goal is to minimize payouts rather than maximize your recovery. When you have legal representation, insurers take claims more seriously and settle faster because they know you understand your rights and won’t accept lowball offers. The California Department of Insurance reports that insurers’ initial offers typically fall 30 to 50 percent below fair value, so having someone review the offer before you sign is essential.

Evaluating Your Claim’s True Value

We at Schaar & Silva LLP evaluate your claim to determine whether the adjuster’s valuation of your vehicle damage aligns with fair market value and challenge underestimates. We also verify that the insurer properly calculated your medical damages, lost wages, and pain and suffering, since many adjusters overlook or undervalue non-economic damages. This review protects you from accepting settlements that fall short of what you actually deserve.

Investigating Legal Action Against the At-Fault Driver

If the at-fault driver can be identified and located, we investigate whether pursuing a lawsuit against them makes financial sense, especially if their personal assets exceed your policy limits. Some uninsured motorists have savings, vehicles, or other property that can be seized to satisfy a judgment, making legal action worthwhile even when insurance won’t cover your full damages.

Managing Medical Bills and Emotional Recovery

We connect you with medical lien services to help manage your medical bills until your case resolves. We also connect you with psychological support specialists if the accident caused emotional trauma. Your focus remains on healing while we handle the legal details and insurance negotiations required under California’s strict claim timelines.

Final Thoughts

Being hit by an uninsured motorist in Santa Cruz leaves you facing medical bills, vehicle damage, and financial uncertainty that feels overwhelming. The good news is that California law provides protections through your own insurance policy, and you have clear steps to follow that improve your chances of fair compensation. Uninsured motorist coverage exists specifically for situations like yours, and filing your claim within 30 days significantly improves approval odds.

Document everything at the accident scene, notify your insurer within 24 hours, seek immediate medical attention even if you feel fine, and build a detailed damages log covering all your expenses. Insurance adjusters typically offer 30 to 50 percent below fair value on first proposals, so never accept their initial offer without careful review. California’s two-year statute of limitations gives you time, but starting early preserves evidence and strengthens your negotiating position.

If you’re uncertain about the valuation, facing pushback from the insurance company, or dealing with significant injuries and lost wages, we at Schaar & Silva LLP can help you navigate your Santa Cruz uninsured motorist claim by evaluating whether settlement offers are fair, investigating legal action against the at-fault driver when appropriate, and connecting you with medical lien services and psychological support as you recover. Contact us today to discuss your case and learn how we can help you move forward.