Car accidents in Santa Cruz County leave you facing medical bills, lost wages, and property damage. The insurance company’s first offer rarely reflects what you actually deserve.

We at Schaar & Silva LLP help accident victims navigate Santa Cruz auto compensation claims and fight for fair settlements. This guide walks you through your options, the claims process, and the mistakes that cost people thousands.

What Damages Can You Actually Recover

After a Santa Cruz car accident, you’re entitled to recover multiple categories of damages, but many victims settle for far less than they deserve because they don’t understand what they can claim.

Economic Damages: The Measurable Costs

Economic damages are straightforward and quantifiable. Medical bills, lost wages, vehicle repair costs, and rental car expenses all fall into this category. The Insurance Information Institute reported that the average property damage claim in 2018 exceeded $3,800, and that number has only climbed since then. If your vehicle is a total loss, you recover its actual cash value at the time of the accident, not replacement cost.

Medical expenses span surgery, hospitalization, ambulance transport, doctor visits, prescription medications, therapy, and in-home care. Lost wages include not just missed paychecks but also bonuses, promotions, and reduced earning capacity if your injuries prevent you from returning to your previous job.

Non-Economic Damages: The Hidden Value

Non-economic damages are harder to quantify but equally recoverable. Physical pain, mental anguish, sleep disruption, loss of enjoyment of life, disability, disfigurement, and loss of consortium all constitute legitimate claims. These subjective harms often represent the bulk of what you actually deserve, yet insurance adjusters routinely lowball them.

How Insurance Companies Value Your Claim

Insurance adjusters use formulas that multiply your medical expenses by a factor of 1.5 to 5, depending on injury severity, then add lost wages and property damage. This multiplier approach is industry standard, but it systematically undervalues pain and suffering, especially for moderate injuries. The adjuster’s opening offer typically sits at the low end of what they calculate you could recover, banking on you accepting it out of financial desperation.

California’s comparative negligence rule under Code of Civil Procedure Section 1431.2 means you can recover damages even if you’re partially at fault, though your recovery reduces by your percentage of fault. If you’re 30 percent at fault for $10,000 in damages, you’d recover $7,000. Understanding this rule matters because adjusters sometimes exaggerate your share of fault to justify lower offers.

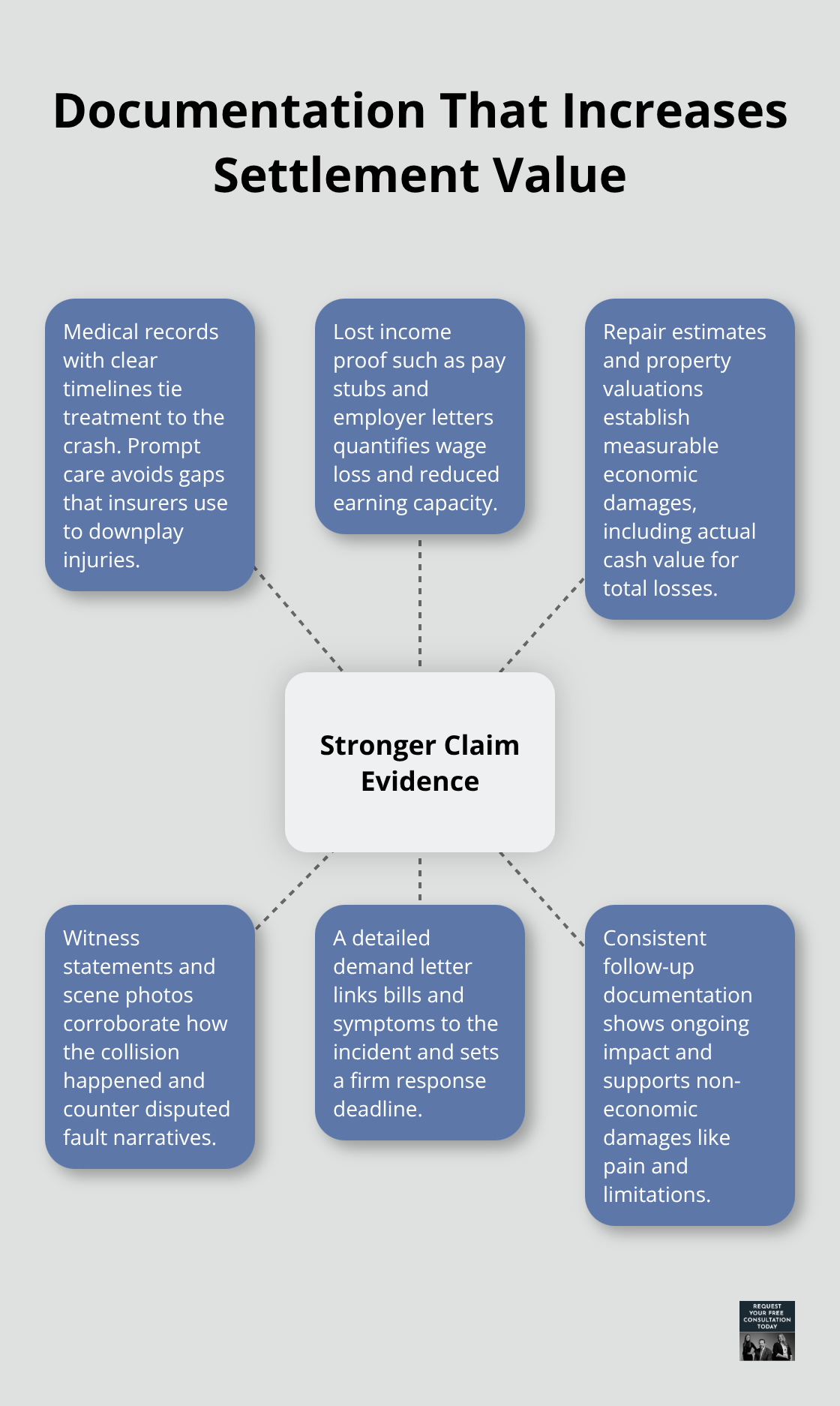

Documentation Determines Your Settlement Value

Your settlement depends entirely on the strength of your documentation: medical records with clear treatment timelines, pay stubs showing lost income, repair estimates, and witness statements. Gaps between your injury date and when you started medical treatment weaken your position significantly because adjusters assume delayed treatment means less serious injury. The adjuster’s calculation method leaves room for negotiation, but only if you present evidence that contradicts their initial assessment.

How to Navigate the Santa Cruz Claims Process

File Your Claim Within 30 Days

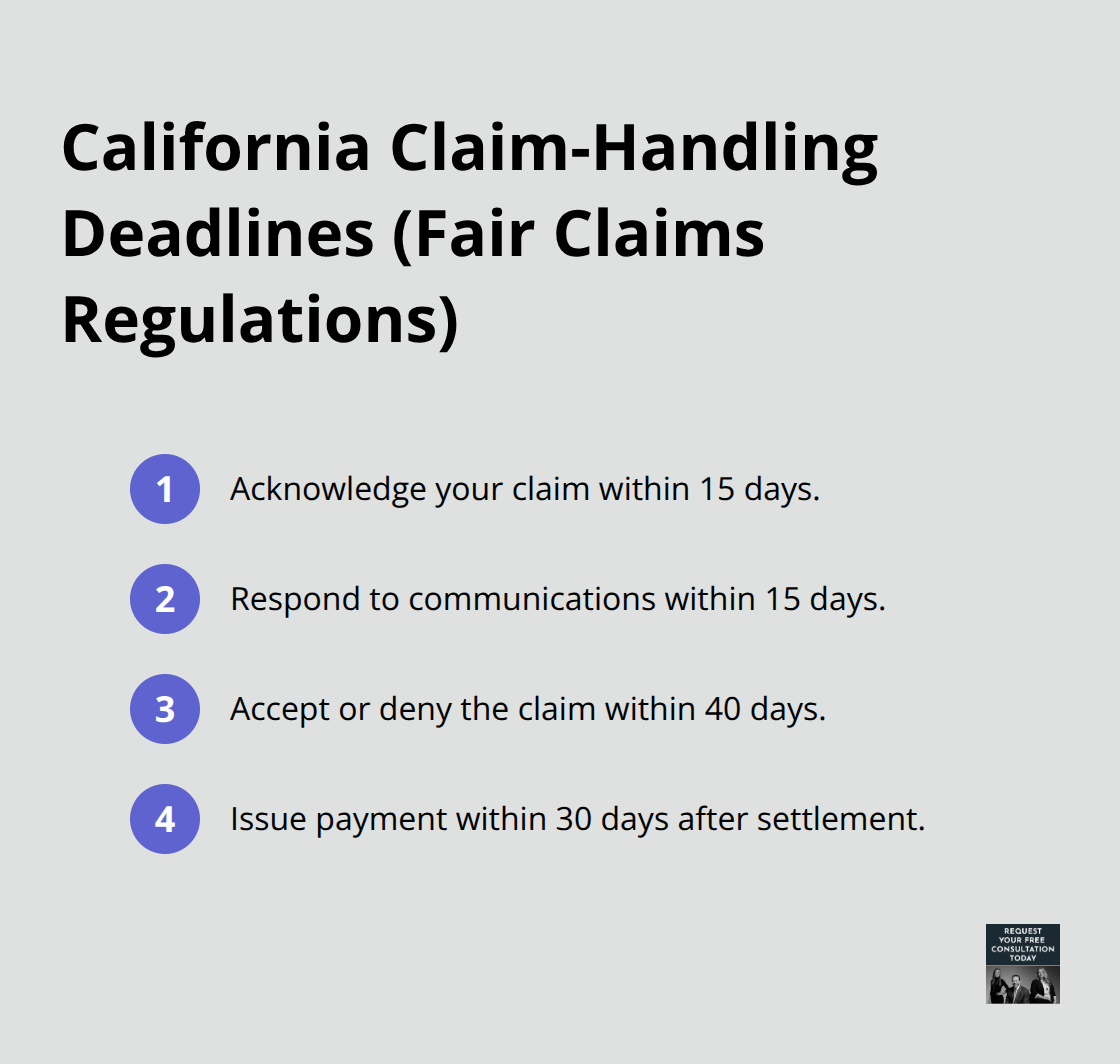

File your claim within 30 days of your accident-this deadline is non-negotiable. California’s Fair Claims Settlement Practices Regulations require insurers to acknowledge your claim within 15 days, respond within 15 days, decide to accept or deny within 40 days, and pay once settled within 30 days. Most people miss this window because they’re overwhelmed, but delays cost you money. The insurance company uses that time to gather statements from witnesses whose memories fade, to photograph damage that becomes harder to assess, and to build a narrative that minimizes fault.

You report the accident to your insurer, provide basic information about the collision, and submit your claim form. Keep copies of everything you send and document the date and time of each submission. If your insurer doesn’t contact you within a reasonable period after filing, call your agent directly rather than waiting passively.

Build Your Medical Documentation File

Medical treatment documentation determines how much you recover, which is why the timing matters enormously. Start treatment promptly after the accident because gaps between injury and treatment invite adjusters to claim your injuries weren’t serious. Gather comprehensive medical records including dates, diagnoses, treatment notes, prescriptions, and any imaging or test results. As your case progresses, medical lien services become relevant if you lack health insurance or your coverage is insufficient. These services defer payment until your settlement resolves, allowing you to receive necessary care without delay.

Present Strong Evidence to Your Adjuster

When negotiating with the insurance adjuster, bring your complete documentation file: police report, medical records, photographs from the accident scene, witness statements, repair estimates, and lost wage documentation like pay stubs and employer letters. The adjuster’s initial offer typically undervalues your claim significantly, banking on you accepting out of desperation. Counter with a demand letter that itemizes economic damages with supporting receipts, itemizes non-economic damages with specific descriptions of your pain and limitations, references California’s comparative negligence rules if applicable, and sets a clear 30-day response deadline.

Navigate Multiple Rounds of Negotiation

Expect multiple rounds of negotiation. Adjusters may request additional information or issue counteroffers. Document every communication, deadline, and counteroffer in writing. If settlement negotiations stall or the adjuster’s final offer falls short of what your documentation supports, you may need to evaluate whether pursuing a lawsuit makes financial sense for your situation. The decision to litigate depends on the strength of your evidence, the size of your claim, and the adjuster’s willingness to negotiate fairly-factors that require careful analysis of your specific circumstances.

Mistakes That Sabotage Your Settlement

The Cost of Accepting the First Offer

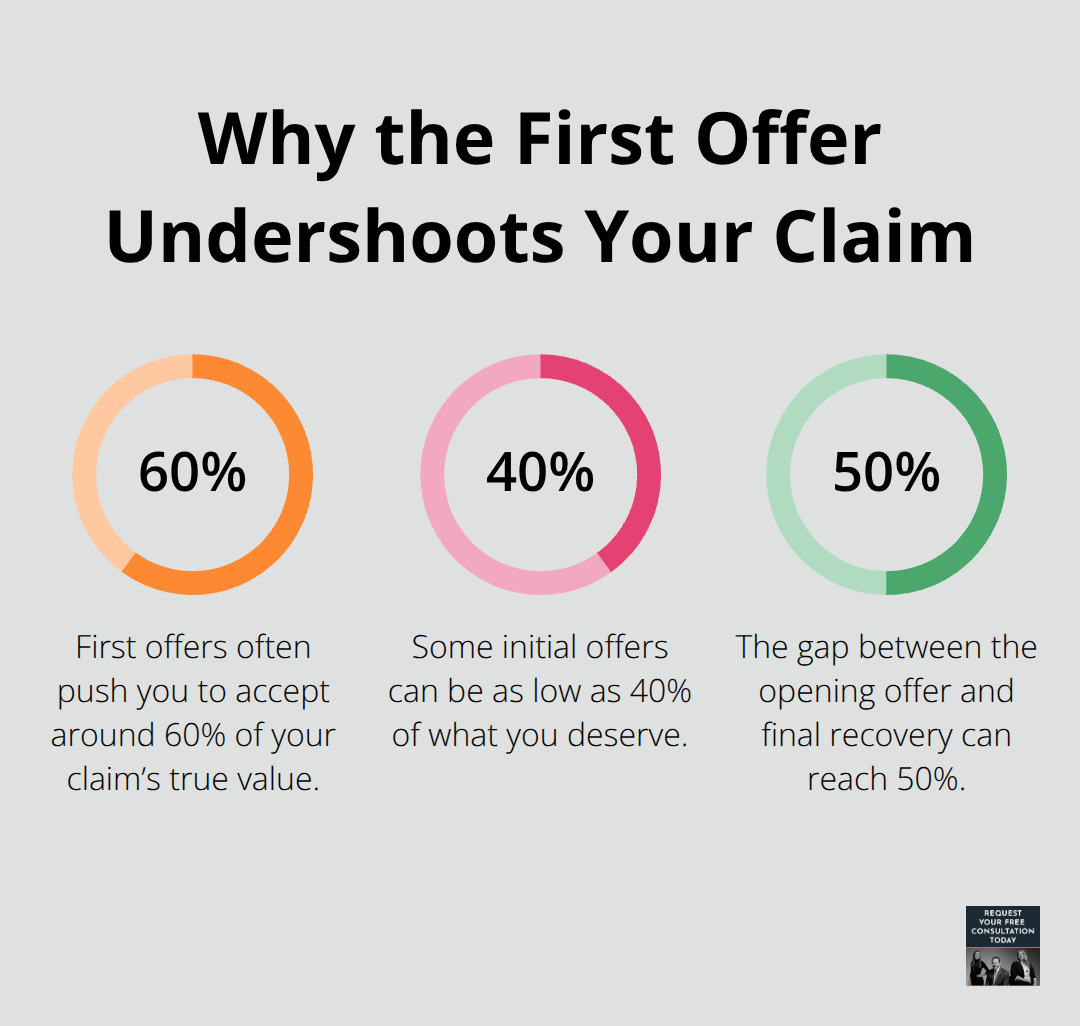

The biggest mistake you can make is accepting the insurance company’s first offer without understanding what your claim is actually worth. Adjusters count on financial pressure and confusion to push you into settling quickly for 40 to 60 percent of what you deserve. Their initial offer arrives fast, often within days, because speed works in their favor. The longer you wait, the more you might gather evidence that strengthens your position.

When an adjuster calls with an offer, they’re testing your knowledge. If you accept immediately, they know they underestimated. If you push back with documentation, they know you understand your claim’s value. The gap between their opening offer and what you ultimately recover often ranges from 20 to 50 percent, depending on how you respond. Never verbally accept an offer or make statements that sound like acceptance. Get everything in writing and take time to evaluate it against your actual damages before responding.

Recorded Statements Lock In Your Words

Recorded statements without legal review cost accident victims thousands in lost recovery. Insurance companies record your statement to lock in your words early, before you fully understand your injuries or their long-term impact. What feels like a casual conversation becomes evidence used against you in settlement negotiations.

You might downplay your pain because you’re in shock, minimize your treatment needs because you’re uncertain about the extent of your injuries, or accidentally admit fault through imprecise language that the adjuster twists later. California’s Fair Claims Settlement Practices Regulations require adjusters to acknowledge and respond to claims within specific timelines, but those same regulations don’t prevent them from using recorded statements strategically. Before any recorded statement, consult with a legal professional who can prepare you for tough questioning and advise which questions you should answer.

Missing Statutory Deadlines Eliminates Your Rights

Missing the 2-year statute of limitations for personal injury claims in Santa Cruz County is irreversible and eliminates your right to recover anything. The clock starts on your accident date, not when you discover your injuries. Many people delay action thinking they have time, then find themselves unable to file.

The 6-month deadline for government vehicle injuries is even shorter and catches people off guard. If you’re unsure about your timeline, file your claim immediately and consult with someone who understands Santa Cruz County court procedures. Document your accident details, medical treatment, and damages now rather than relying on memory later.

Final Thoughts

Handling a car accident claim alone puts you at a disadvantage because insurance adjusters negotiate settlements every day and know exactly how much pressure to apply. You recover from injuries, manage medical appointments, and deal with financial stress while adjusters work to minimize what they pay you. Having someone in your corner who understands Santa Cruz County law and insurance tactics makes the difference between a settlement that barely covers your costs and one that actually compensates you fairly for your Santa Cruz auto compensation claim.

We at Schaar & Silva LLP have spent years helping accident victims navigate claims that adjusters tried to minimize, and we know where insurance companies typically undervalue claims and how to present evidence that forces them to increase their offers. Our team handles the negotiation process so you can focus on healing rather than fighting with adjusters over documentation and liability percentages. We also evaluate property damage claims to verify fair valuations and guide you through California’s comparative negligence rules and Santa Cruz County court procedures if your case requires litigation.

Contact Schaar & Silva LLP for a free case evaluation to discuss your specific situation and learn what fair compensation looks like for your claim. Call (844) 730-0233 anytime to start the process and take control of your recovery.