After a car accident in Santa Cruz, getting the right property damage valuation can mean the difference between covering your losses and falling short. Insurance companies often lowball initial offers, and many people don’t realize they have options to challenge these numbers.

We at Schaar & Silva LLP help accident victims understand exactly how their vehicle damage is assessed and what they can do to fight for fair compensation. This guide walks you through the valuation process and shows you where most people lose money.

How Adjusters Actually Value Your Vehicle

When an adjuster arrives at your location after a Santa Cruz crash, they conduct a structured assessment that directly determines your payout. The inspection typically lasts under an hour, and the adjuster evaluates structural damage, paint condition, mechanical systems, and whether components can be repaired or must be replaced. This initial assessment becomes the baseline for your claim valuation.

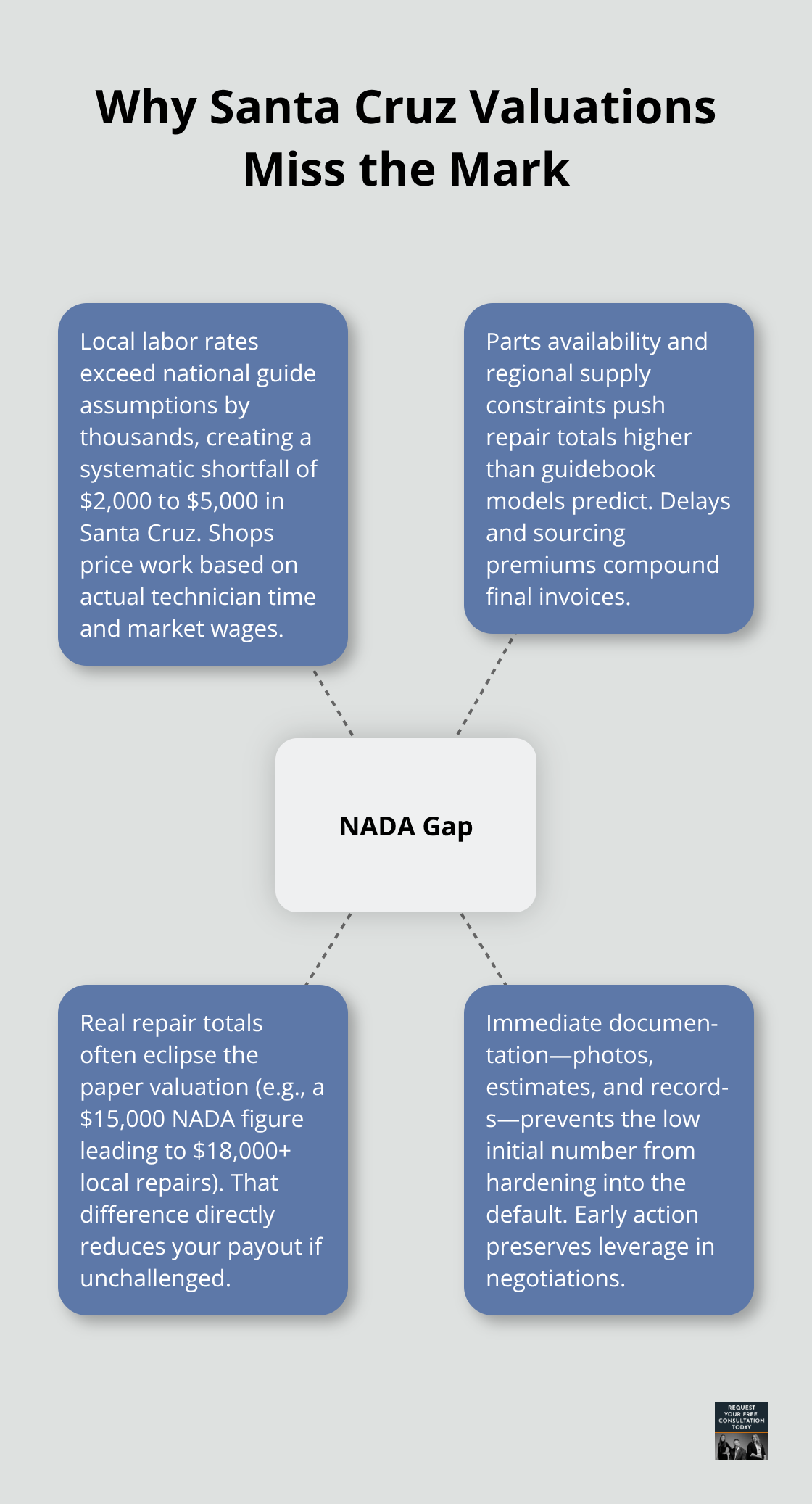

The NADA Guides Problem in Santa Cruz

Adjusters rely heavily on NADA Guides to estimate repair costs, and these guides consistently underestimate local Santa Cruz labor rates and parts costs by roughly $2,000 to $5,000 compared with actual shop pricing. This gap is not accidental-it’s built into the system. A vehicle valued at $15,000 on NADA might cost $18,000 or more to repair locally due to higher labor rates and parts availability in Santa Cruz County. You need to act immediately after the crash to document everything and gather competing information before the adjuster’s valuation becomes the default position.

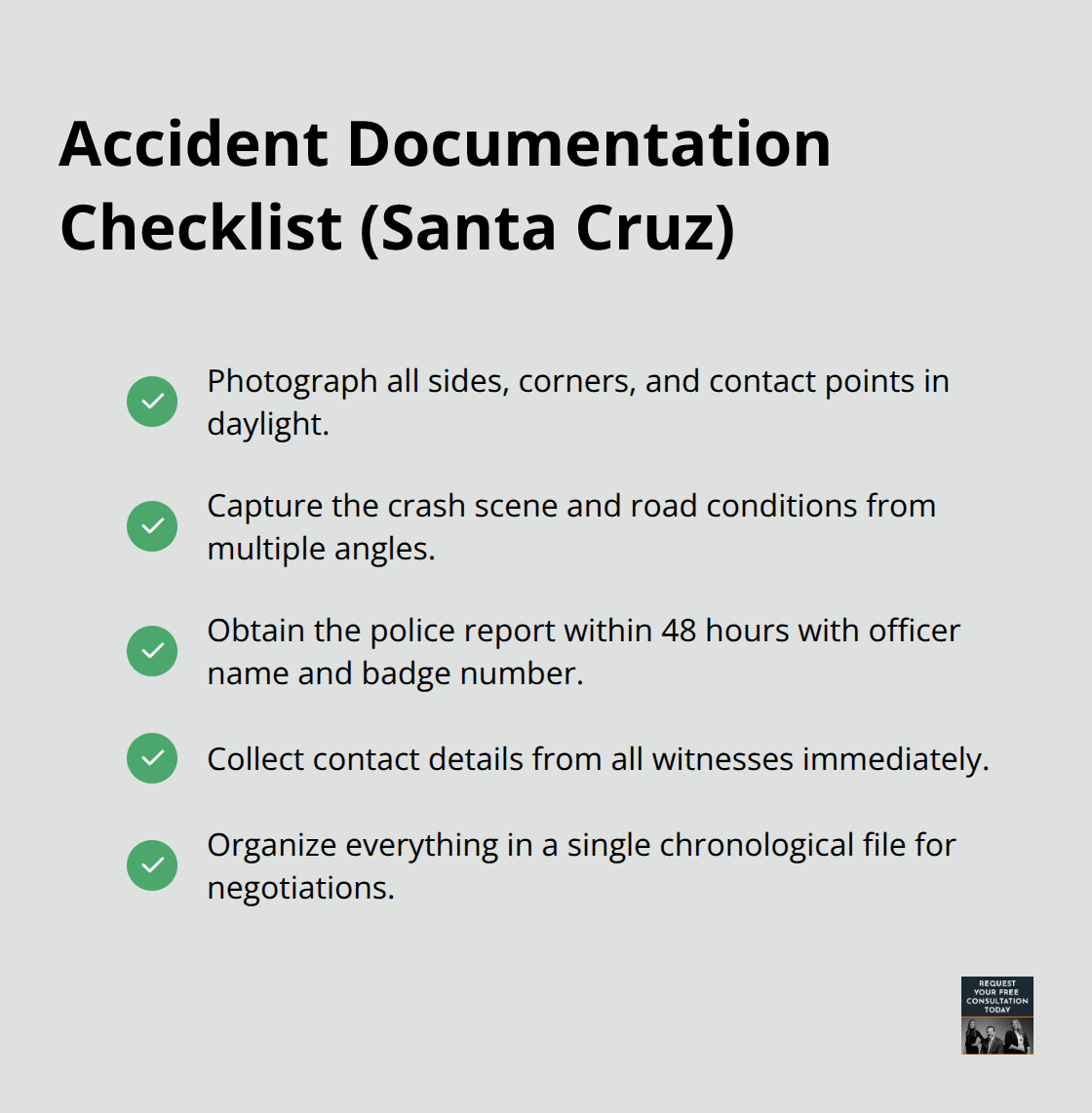

Building Your Documentation Package

Photograph your vehicle from multiple angles in daylight and capture the crash scene and road conditions. Collect the police report within 48 hours along with the officer’s name and badge number, and get contact details from witnesses. This documentation creates a paper trail that supports your later negotiations and shifts power away from the adjuster’s initial assessment.

What Three Independent Estimates Reveal

Before accepting any settlement offer, obtain written repair estimates from three licensed Santa Cruz repair shops with no financial ties to your insurer. These estimates serve a critical purpose: they reveal the actual cost gap between what the adjuster’s NADA-based calculation says and what local shops will actually charge to fix your vehicle. Present these three estimates to the adjuster at the inspection, in writing, along with pre-accident photos and your police report. This shifts the conversation from a generic valuation to a documented cost comparison.

Challenging Total Loss Declarations

If your vehicle is declared a total loss (meaning repair costs exceed the vehicle’s fair market value), the insurer will pay the depreciated value minus salvage. You can challenge this outcome with an independent appraisal, which typically costs $300 to $600 upfront but can justify $2,000 to $5,000 or more in additional payout. The California Department of Insurance requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, so organize all documentation chronologically in a single file to keep negotiations on track and pressure timely responses.

Understanding how adjusters work and what documentation carries weight sets the stage for negotiating effectively. The next section reveals the common mistakes that allow insurers to keep settlements artificially low.

Common Valuation Mistakes That Cost You Money

The initial settlement offer from an insurance company is rarely final, yet most accident victims in Santa Cruz accept it without question. This single mistake costs claimants thousands of dollars. The adjuster’s first number reflects what the insurer believes it can get away with, not what your vehicle damage actually costs to repair. Within the first week after your crash, the adjuster will contact you with an offer based on that one-hour inspection and NADA Guides. This offer assumes you won’t push back. If you accept it immediately, you forfeit your right to negotiate and lock in a lowball figure. The gap between initial offers and documented repair costs typically ranges from $2,000 to $5,000 or more in Santa Cruz County. Treat the first offer as an opening position, not a final decision.

Accepting the First Offer Without Question

Most accident victims settle too quickly because insurers pressure them to finalize claims fast. The adjuster frames the initial offer as reasonable and suggests that further negotiation will only delay your payout. This tactic works because people want closure after a stressful accident. However, accepting without supporting documentation leaves thousands on the table. Obtain three written repair estimates from licensed Santa Cruz shops before you respond to any settlement offer. Present these estimates to the adjuster in writing, along with pre-accident photos and your police report. This shifts the conversation from a generic valuation to a documented cost comparison that the insurer cannot easily dismiss.

Failing to Document All Damage

Many accident victims photograph their vehicle but miss critical details that strengthen negotiation leverage. The adjuster’s one-hour inspection glosses over hidden damage such as frame misalignment, water intrusion behind panels, suspension issues, and electrical problems that only emerge during detailed repair work. When you fail to document these potential issues upfront, the adjuster has no reason to account for them in the initial valuation. Photograph the interior, undercarriage, and all contact points immediately after the crash. Collect the police report with the officer’s name and badge number within 48 hours. Organize maintenance records and service receipts to prove your vehicle was well-maintained, which prevents insurers from claiming pre-existing damage. Store everything in a single chronological file before memory fades and documents scatter.

Ignoring Hidden Damage and Long-Term Issues

Adjusters conduct quick inspections that miss structural and mechanical issues completely. A vehicle with $8,000 in visible damage might have another $5,000 to $10,000 in hidden frame or suspension damage that only a licensed Santa Cruz technician can identify. Insist on a full pre-repair mechanical inspection focusing on frame straightness, suspension integrity, and electrical system damage. This inspection typically costs $200 to $400 but prevents you from accepting a settlement that excludes thousands in repair costs. Once repairs begin and hidden damage surfaces, the insurer will argue that the damage was pre-existing or caused by poor repair work, leaving you responsible for the bill. The California Department of Insurance states that insurers must stand behind repairs performed at your chosen shop if they meet accepted trade standards, which shifts liability back to the insurer. If you discover hidden damage during repairs, notify the adjuster immediately with updated estimates. Document everything in writing and keep all invoices and photos organized to support a claim for additional compensation. The statute of limitations for property damage claims in California is three years, so maintain records well beyond the initial settlement window.

Understanding these mistakes positions you to challenge low valuations with real documentation. The next section shows you how independent appraisals and strategic negotiation tactics can recover the money insurers initially withhold.

Getting Fair Compensation in Santa Cruz

Why Independent Appraisals Matter

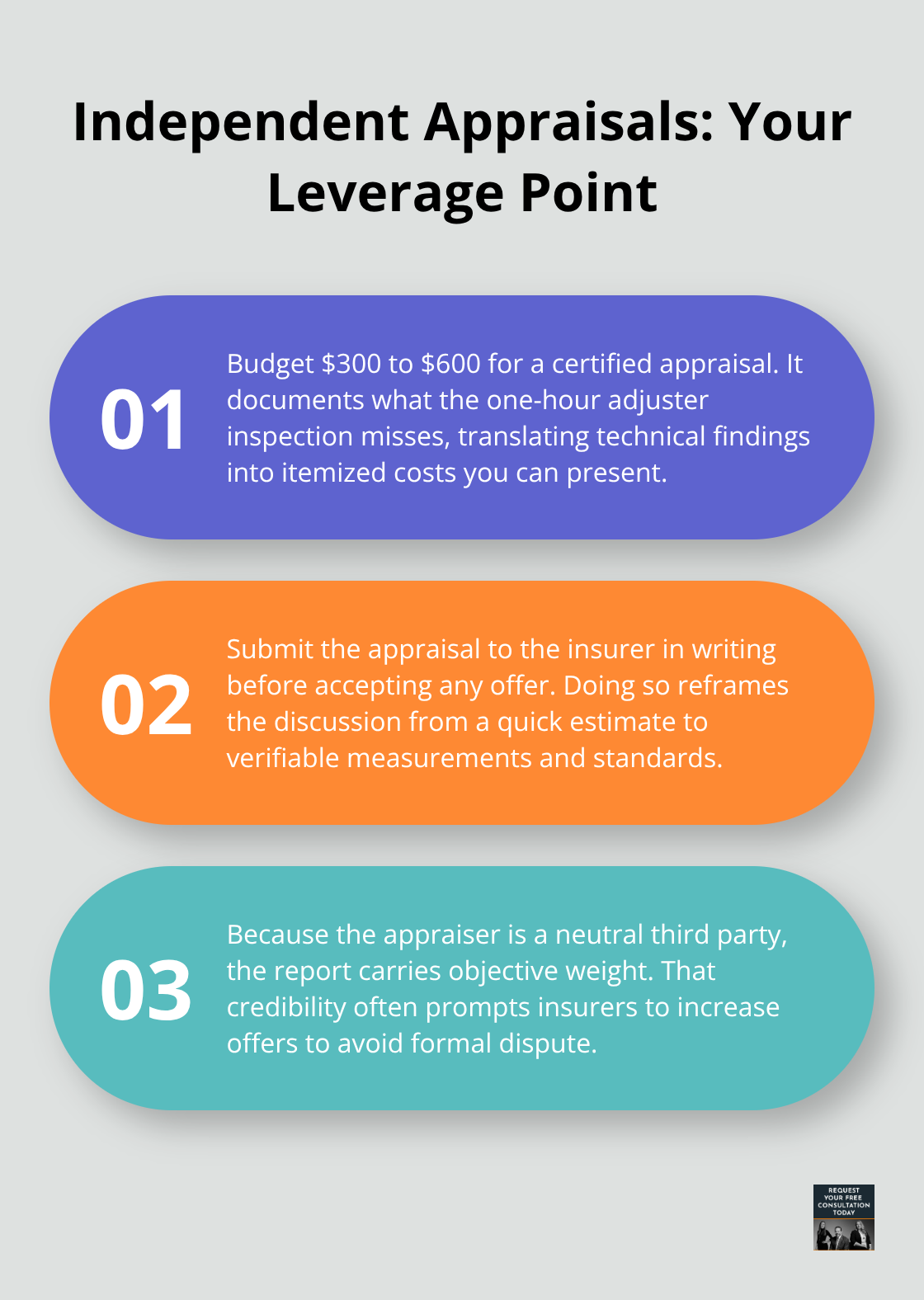

An independent appraisal is not optional if you want to close the gap between what the insurer offers and what your vehicle actually costs to repair. The appraisal typically costs $300 to $600 upfront, but it documents exactly what the adjuster missed during that one-hour inspection. A certified appraiser examines frame alignment, paint thickness, suspension components, and electrical systems with precision that an adjuster rushing through a quick assessment will never match. Present this appraisal to the insurer in writing before accepting any settlement.

The document carries weight because it comes from a neutral third party with no financial stake in the outcome.

Insurance adjusters rely on NADA Guides, which systematically undervalue local Santa Cruz labor and parts by $2,000 to $5,000, so an appraisal that accounts for actual shop pricing becomes your leverage point. Insurers know that appraisals create paper trails and increase the likelihood of dispute resolution, so many will increase their offer once you submit one rather than face formal challenge.

Recognizing Insurer Pressure Tactics

Insurers employ specific tactics designed to pressure quick settlement before you gather documentation. The adjuster will frame the initial offer as fair and final, suggesting that further negotiation only delays payment. They may claim that three repair estimates are unnecessary or that hidden damage claims lack credibility without visible proof. Ignore this pressure entirely.

California law requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, according to the California Department of Insurance, but this timeline does not prevent you from presenting additional documentation that extends the process legitimately. When you submit three written repair estimates from independent Santa Cruz shops at the adjuster’s inspection, you shift control away from the insurer’s preferred valuation method.

Building Your Written Record

Do not accept verbal explanations for low offers; demand written justification for any valuation discrepancies so you have a clear record. If the insurer refuses to increase the offer after you present independent estimates and an appraisal, invoke the California Appraisal Provision, which allows either party to demand binding appraisal with two appraisers and an umpire who renders a final decision. This formal step signals that you will not accept lowball treatment, and many insurers will negotiate seriously once they realize you will pursue this route.

Keep all communications organized chronologically in a single file, including the police report, repair estimates, photos, maintenance records, and appraisal. Present this complete package to the adjuster and reference specific California Department of Insurance timelines to maintain pressure for timely response.

When to Pursue Legal Review

If negotiations stall after you have exhausted these steps, legal review becomes the practical next move to determine whether additional compensation is justified. The legal team at Schaar & Silva LLP can evaluate your case and help you understand whether pursuing additional compensation makes financial sense for your specific situation.

Final Thoughts

Property damage valuation in Santa Cruz requires action, not acceptance. The gap between what insurers initially offer and what your vehicle actually costs to repair typically ranges from $2,000 to $5,000 or more, and you close this gap by obtaining three written repair estimates from licensed local shops, hiring an independent appraiser for $300 to $600, and presenting a complete documentation package that includes your police report, pre-accident photos, and maintenance records. The California Department of Insurance requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, so organize everything chronologically and reference these timelines to maintain pressure for fair resolution.

Most accident victims in Santa Cruz settle too quickly because insurers frame initial offers as final and pressure fast closure. Resist this tactic and present your independent estimates and appraisal in writing, demand written justification for any valuation gaps, and invoke the California Appraisal Provision if negotiations stall. These steps shift control away from the adjuster’s one-hour inspection and NADA-based calculation toward documented evidence of actual repair costs.

When negotiations reach an impasse despite your documentation efforts, legal review becomes the practical next step. The team at Schaar & Silva LLP can evaluate whether your case warrants additional pursuit and help you understand your options for recovery in property damage valuation matters. Contact us to discuss your specific situation and determine the best path forward for your claim.