A car crash can leave you dealing with insurance companies, repair estimates, and paperwork when you’re already stressed. Understanding how car crash property claims work makes the process less overwhelming.

We at Schaar & Silva LLP help people in Santa Cruz County recover fair compensation for vehicle damage. This guide walks you through each step, from documenting the accident scene to negotiating with insurers.

What Counts as Property Damage After a Car Crash

Vehicle Repairs and Total Loss

Property damage in a car crash covers far more than just your vehicle’s repair costs. California law ties your insurer’s payment obligation to your car’s actual cash value at the time of the loss. If repairs cost more than this value, your vehicle is considered totaled, and you receive the replacement cost instead. A car worth $15,000 before the crash, for example, might total $18,000 in repair bills, meaning you’d receive the $15,000 valuation rather than the higher repair estimate. This distinction matters because many people assume their insurer will pay whatever the repair shop quotes.

Items Inside Your Vehicle and Additional Costs

Property damage claims extend beyond vehicle repairs to include personal items inside your car, custom equipment, or modifications you’ve made. A crash that destroys your phone, laptop, or professional tools in the vehicle qualifies those losses for compensation. Rental car costs while yours is being repaired also fall under property damage coverage in most policies. The key is documenting everything with receipts, photos, and repair estimates before negotiating with your insurer.

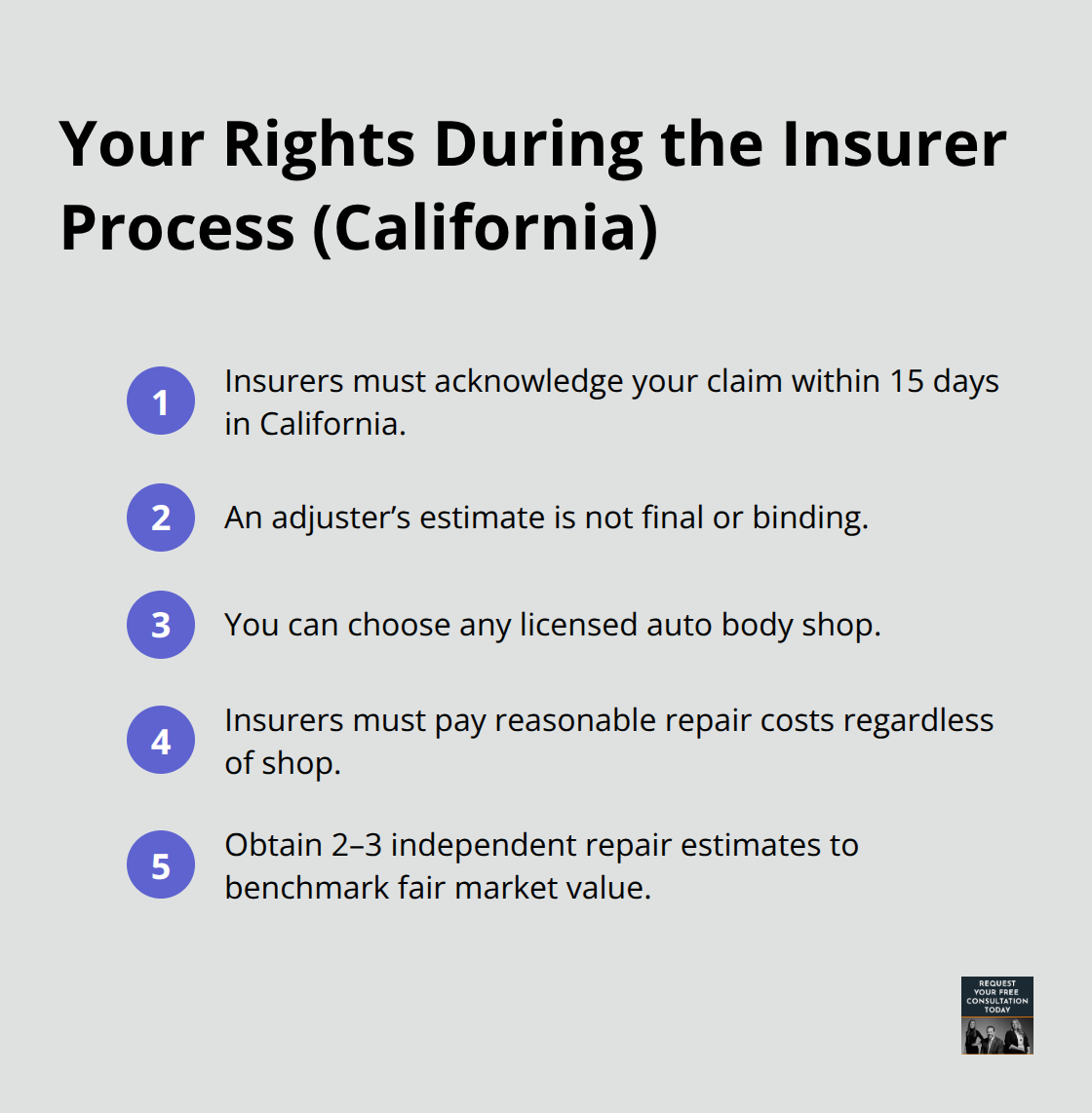

Understanding Insurer Timelines and Your Rights

Insurers must acknowledge your claim within 15 days under California law and begin investigating promptly, though the actual timeline for resolution varies. When you receive an estimate from the insurer’s adjuster, that’s not the final word. You have the right to choose your own auto body shop, and insurers must pay reasonable repair costs regardless of which shop you select. Many people accept the first valuation without question, but gathering 2-3 independent repair estimates reveals whether the insurer’s offer matches fair market value.

Parts Quality and Hidden Damage

Parts matter significantly in repair costs. OEM parts cost more than aftermarket alternatives, but they often provide better durability and resale value. Ask your repair shop to specify which parts they’re using so you understand the quality difference reflected in the estimate. Hidden damage discovered after repairs begin can increase costs significantly, which is why having a qualified professional inspect your vehicle before accepting any settlement protects you from future expenses.

Understanding these property damage categories helps you build a stronger claim and identify what compensation you should pursue. The next section covers the immediate steps you must take at the accident scene to protect your claim.

What to Do Right After the Crash

Act Immediately at the Scene

The first hour after a crash determines how strong your property damage claim becomes. California law requires you to report crashes involving property damage over $750 to the DMV within 10 days, but waiting that long weakens your case. Turn on hazard lights immediately and call 911 if anyone is injured. Move vehicles to a safe location if possible. Do not admit fault at the scene, even if you think the accident was your mistake-what you say can be used against you in settlement negotiations or court.

Exchange names, phone numbers, addresses, and insurance information with the other driver. Get the police or California Highway Patrol case number on the spot, as this number connects your accident report to all future claims. Write down the other vehicle’s make, model, color, and license plate before it leaves. Take a photo of their insurance card and driver’s license if they’re willing.

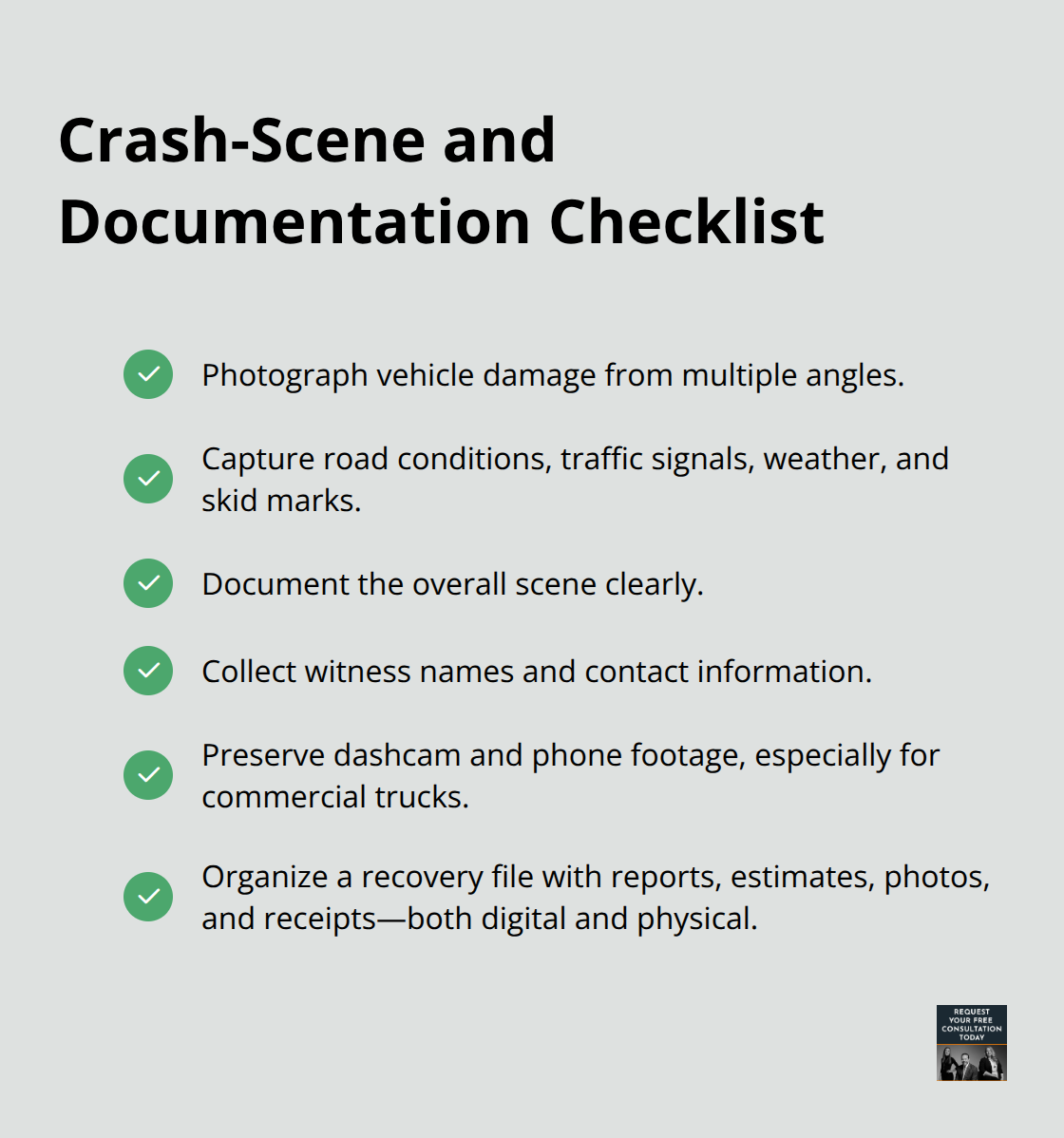

Document Everything with Photos and Evidence

Photograph everything before anyone leaves: vehicle damage from multiple angles, road conditions, traffic signals, weather, skid marks, and the overall scene. These photos become your evidence if the other driver’s insurer disputes fault or undervalues repairs. Collect contact information from witnesses who saw the crash happen, not just bystanders. Witness statements often decide cases when accounts conflict.

If a commercial truck is involved, preserve dashcam footage and phone recordings of crash mechanics immediately, as trucks frequently disappear or change ownership. Organize everything into a recovery file from day one: medical records if you were injured, repair estimates, the police report, photos, insurance communications, and receipts. Keep this file digital and physical, as insurers sometimes claim they never received documents.

Notify Your Insurer and Gather Repair Estimates

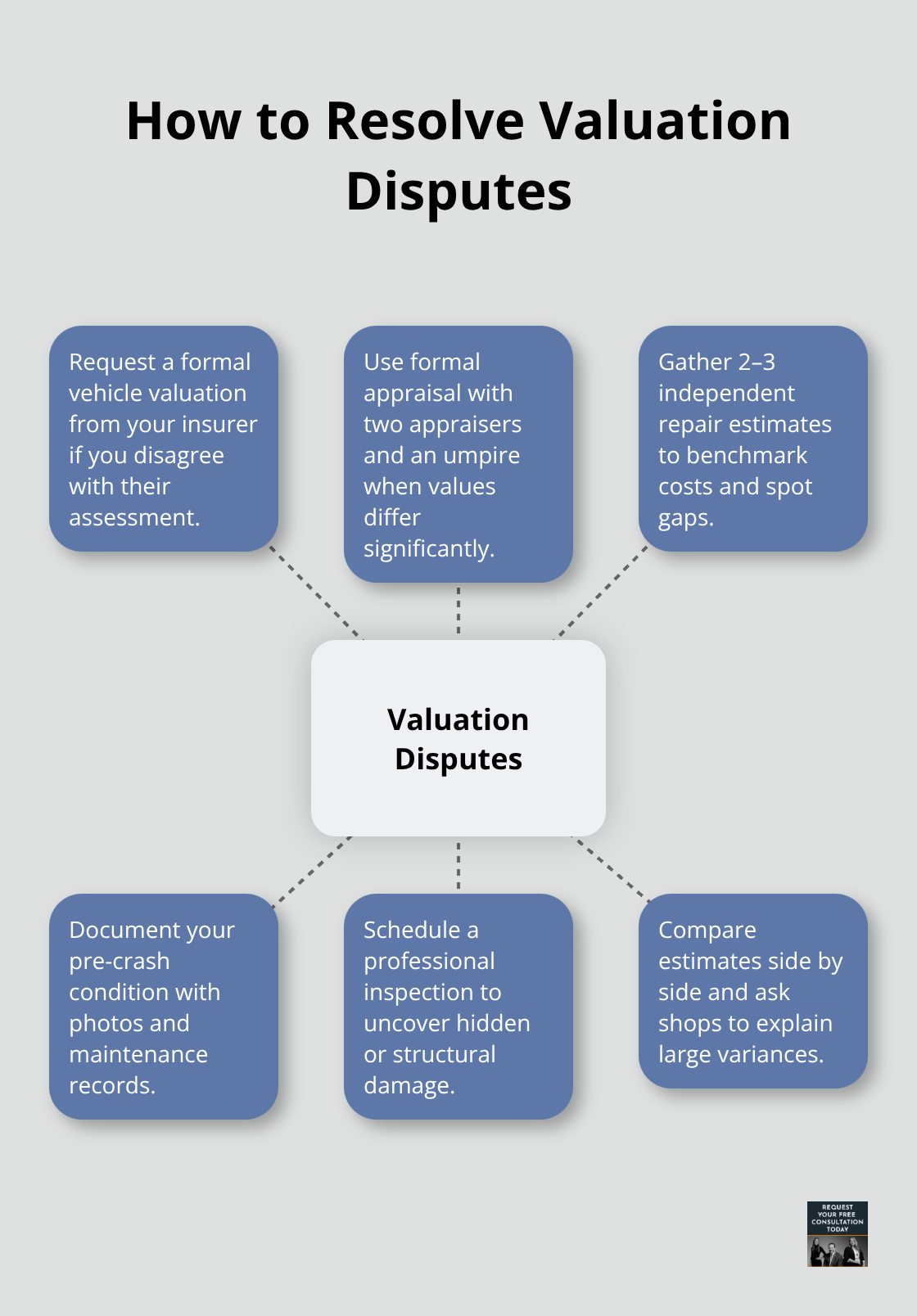

Notify your insurance company within 24 hours and request a documented accident report from the adjuster. The adjuster assesses damage and determines liability, but you have the right to choose your own auto body shop regardless of where your insurer sends you. Get 2-3 independent repair estimates before accepting any settlement offer, as estimates often vary by $2,000 to $5,000 depending on the shop and parts used.

Verify whether estimates specify OEM parts, aftermarket parts, or reconditioned parts, since this affects repair quality and fair compensation. Schedule a professional inspection to identify hidden damage that may not be visible immediately after the crash. Unseen frame damage, suspension issues, or internal component damage discovered later can cost thousands more.

Resolve Valuation Disputes

California insurers must acknowledge your claim within 15 days and begin investigating, though timelines for resolution vary widely. If the insurer’s valuation differs significantly from your estimates, you can pursue formal appraisal with two appraisers and an umpire to resolve the dispute fairly. This process protects you from accepting an offer that undervalues your vehicle or repairs.

The steps you take now directly affect how much compensation you receive and how quickly the process moves forward. Once you’ve documented the scene and gathered estimates, understanding your policy coverage limits and negotiating with professionals becomes your next priority.

How to Get Fair Compensation for Your Vehicle Damage

Collect Multiple Repair Estimates

Three repair estimates are non-negotiable if you want fair compensation. Most people accept their insurer’s first valuation without question, but estimates typically vary by $2,000 to $5,000 depending on the shop and parts specified. Contact three independent auto body shops in Santa Cruz County and request detailed written estimates that break down labor costs, parts, and materials separately. Ensure each estimate specifies whether they use OEM parts, aftermarket parts, or reconditioned parts, since this directly affects both repair quality and the fair market value of your vehicle. OEM parts cost more but provide better durability and resale value compared to aftermarket alternatives.

Your insurer must pay for reasonable repair costs regardless of which shop you choose, so don’t let them pressure you into their preferred vendor. Once you have three estimates, compare them side by side and identify where costs diverge. If one estimate is significantly higher or lower, ask that shop why. Hidden damage discovered during inspection often explains price differences, and a qualified professional inspection before you accept any settlement protects you from future expenses that could cost thousands more.

Understand Your Policy Coverage Limits

Your insurance declaration page lists your coverage limits for collision, comprehensive, and liability, but many people never read these sections carefully. If your vehicle is totaled and your actual cash value is $18,000 but your policy limits are only $15,000, you receive $15,000 regardless of what the repairs would cost. California law requires insurers to pay the lesser of repair costs or your vehicle’s actual cash value at the time of loss, so this distinction matters enormously.

Request a formal vehicle valuation from your insurer if you disagree with their assessment. If the gap is significant, you can pursue formal appraisal where two independent appraisers and an umpire resolve the dispute fairly. This process takes longer than accepting an offer, but it protects you from accepting an undervalued settlement.

Challenge Low Valuations with Documentation

Document your vehicle’s condition before the crash with photos and maintenance records, as this strengthens your argument for a higher valuation. If your insurer’s valuation seems artificially low, push back rather than accept their first offer. Insurers acknowledge claims within 15 days under California law and begin investigating promptly, though timelines for resolution vary widely. A formal appraisal process (involving two appraisers and an umpire) resolves valuation disputes when you and your insurer cannot agree on fair market value.

Final Thoughts

Car crash property claims require careful documentation and strategic action from the moment the accident happens. You now understand what counts as property damage, how to protect your claim at the scene, and how to negotiate fair compensation with insurers. The three repair estimates, the formal appraisal process when valuations don’t match, and your right to choose your own repair shop are your strongest tools against undervalued settlements.

Most property damage claims resolve within weeks if you follow these steps consistently. California law gives you three years from the crash date to file a lawsuit for property damage, but waiting that long weakens your case as evidence fades and witnesses become harder to locate. Act within the first few weeks while details are fresh and documentation is complete.

Some situations demand legal guidance beyond what you can handle alone. If the other driver disputes fault, if your insurer’s valuation is significantly lower than your repair estimates, or if hidden damage emerges after initial assessments, contact Schaar & Silva LLP to protect your rights and secure fair compensation for your loss.