A crash leaves you with damaged property and a pile of questions about what happens next. Insurance companies use specific methods to value your vehicle, and understanding these methods helps you get fair compensation.

At Schaar & Silva LLP, we help Sacramento property damage victims navigate repair estimates, adjuster negotiations, and total loss decisions. This guide walks you through the valuation process and shows you how to protect your claim.

How Insurance Companies Value Your Damaged Vehicle

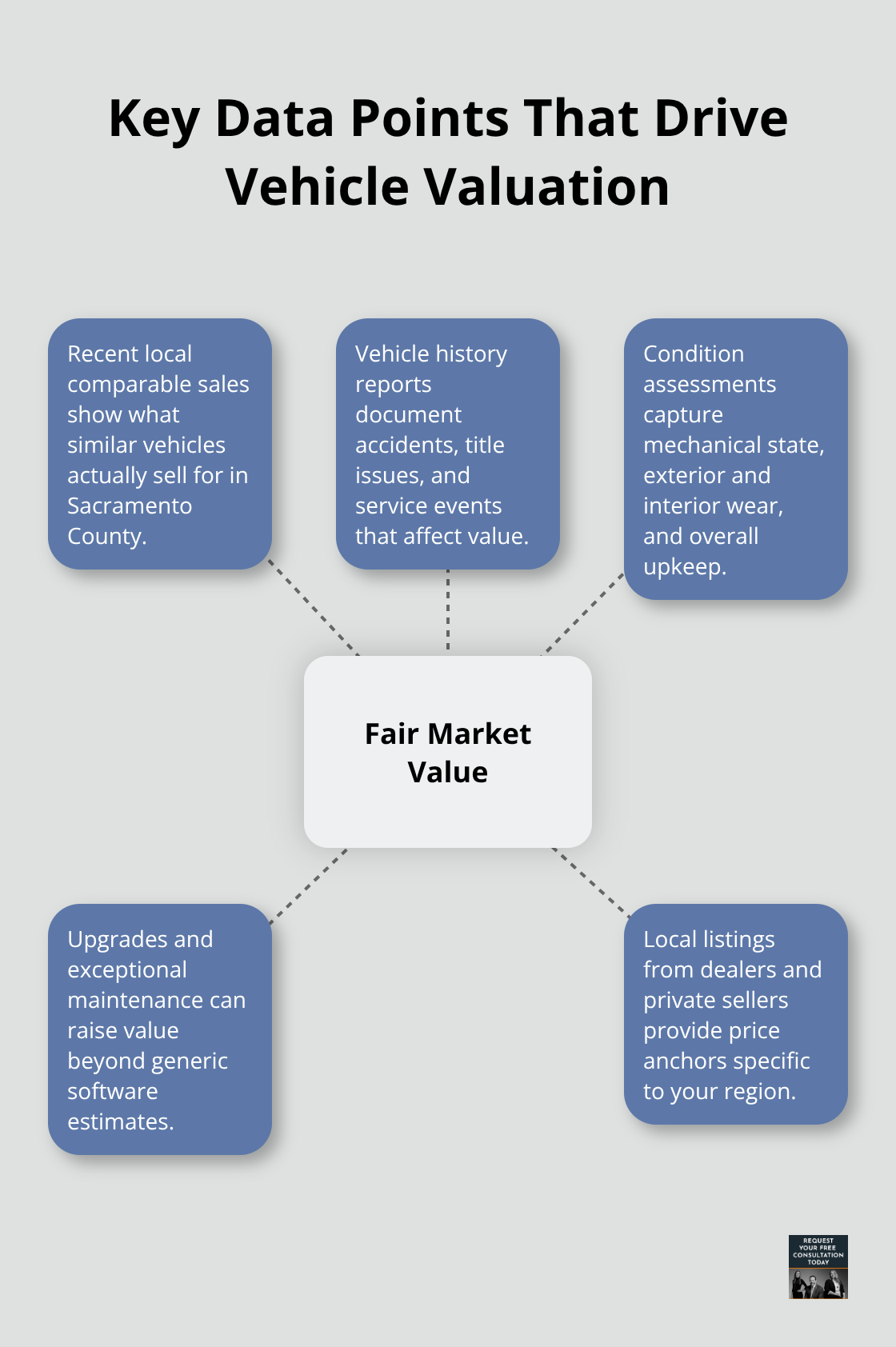

Insurance adjusters don’t simply eyeball your car and offer a number. They use specific valuation methods that you need to understand to spot undervalued offers. The most common approach is actual cash value, which calculates what your vehicle was worth immediately before the crash, minus depreciation. This differs fundamentally from replacement cost, which is what it would cost to buy an identical vehicle today.

California requires insurers to act in good faith and thoroughly investigate claims, which means they must justify their valuation with concrete market data, not guesses. When an adjuster provides a low offer, ask for a written explanation of how they calculated the amount. If they reference only one valuation source, that’s a red flag. Reputable adjusters cross-reference multiple data points including recent sales of comparable vehicles in your local market, vehicle history reports, and condition assessments.

Understanding Total Loss Thresholds

For totaled vehicles, the calculation hinges on fair market value thresholds. California doesn’t have a statewide total loss percentage, but most insurers use 70 to 80 percent of fair market value as the trigger point. If your vehicle’s repair costs exceed that threshold, insurers typically declare it a total loss.

The problem is that many adjusters underestimate fair market value by excluding recent repairs, upgrades, or exceptional maintenance. You counter this by gathering your own market data before negotiations begin. Check local classified listings, dealer inventory, and pricing guides specific to Sacramento County. Compare vehicles with matching mileage, condition, and features to your own car. This legwork takes three to five hours but directly protects your settlement amount.

Building Your Documentation Package

Adjusters make decisions based on evidence. The stronger your documentation, the harder it is for them to justify a low valuation. Collect your service records and maintenance receipts immediately after a crash. These documents prove you maintained the vehicle properly, which supports a higher valuation.

Take photos of the damage from multiple angles within 24 to 72 hours while details are fresh. Include wide shots showing the overall scene and close-ups of specific damage areas. Obtain a repair estimate from a trusted local shop within two to three weeks of the accident. Sacramento has several reputable shops that provide detailed, itemized estimates that adjusters respect.

Store all communications with the insurer including emails, letters, and notes from phone calls. Document the date, time, and adjuster name for each interaction. If the adjuster pressures you to settle quickly or dismisses your evidence without explanation, that’s a negotiation tactic you should resist. Request that the adjuster provide their valuation methodology in writing before you respond. This forces transparency and gives you concrete points to challenge.

Understanding how adjusters value your vehicle puts you in control of the negotiation. With solid documentation and market research in hand, you’re ready to work with repair shops and navigate the adjuster process to protect your claim.

Selecting Repair Shops and Managing the Adjuster

Choose Certified Repair Shops in Sacramento

The repair shop you select directly influences what the insurance company will pay. Sacramento has certified shops that work regularly with insurers and understand how to document damage in ways adjusters accept. When you contact a shop, ask whether they hold certification from your vehicle’s manufacturer or accreditation from the National Institute for Automotive Service Excellence. Certified shops maintain training standards and quality guarantees that matter in negotiations.

Request a detailed, itemized estimate that breaks down labor costs, parts prices, and the hours required for each repair. A vague estimate that lists only totals gives the adjuster room to dispute individual line items and reduce the payout. Most Sacramento shops produce detailed estimates within 48 hours if you provide photos and a description of the damage.

Don’t Rush to Authorize Repairs

Once you have the estimate, resist the urge to authorize repairs immediately. The estimate itself serves as your negotiation tool with the insurance company, and you need time to compare it against the adjuster’s valuation before committing to work. Adjusters often use software like CCC Valuations or Mitchell to generate their initial offers, and these tools frequently undervalue repairs by omitting labor costs or using outdated parts pricing.

Compare Estimates Against Adjuster Valuations

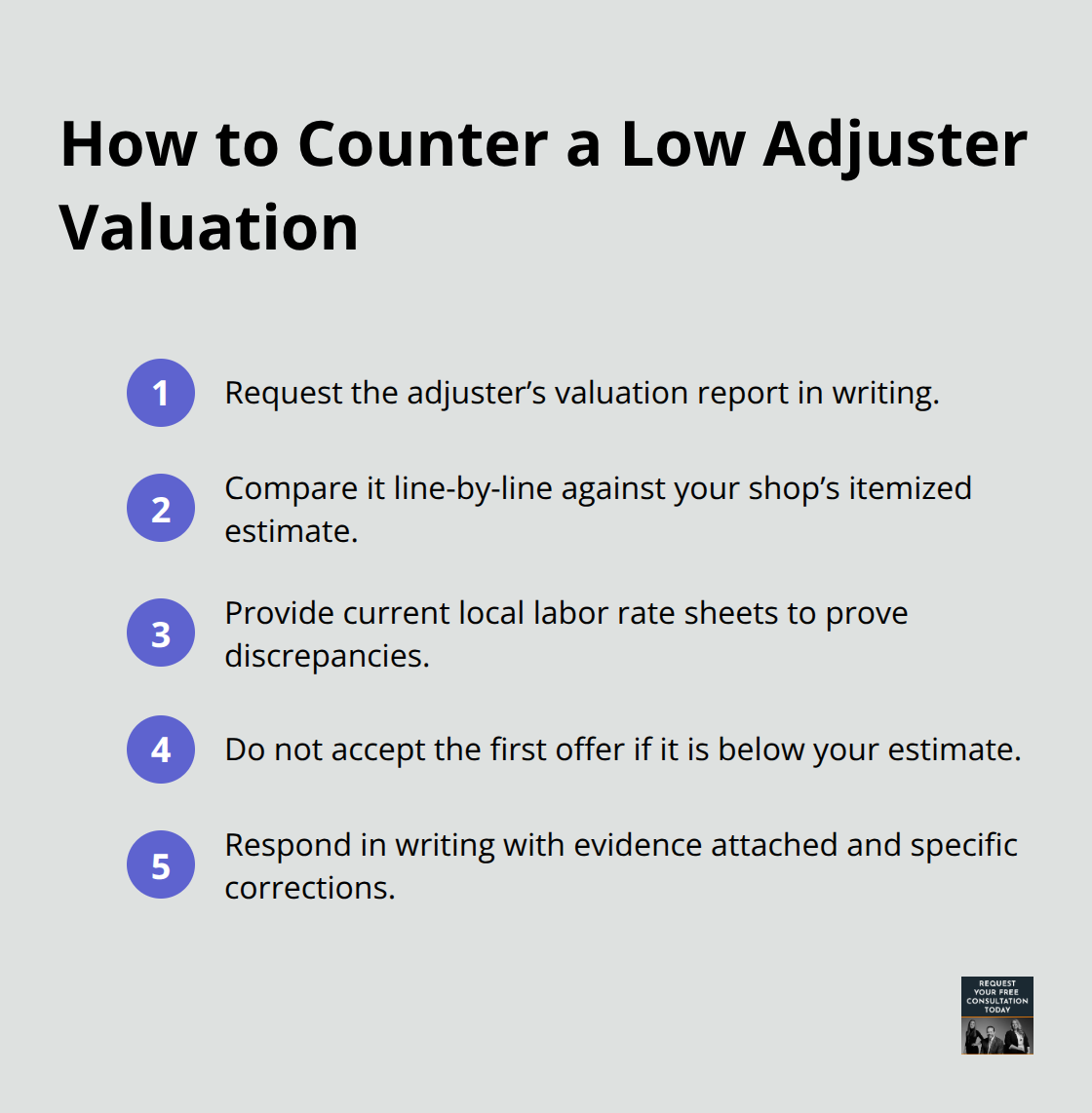

Request a written copy of the adjuster’s valuation report and compare it line-by-line against your repair shop’s estimate. If the adjuster’s report shows lower labor rates than what Sacramento shops actually charge, provide current rate sheets from local shops to prove the discrepancy. Don’t accept the first offer if it falls short of your shop’s estimate.

Respond in writing with your repair estimate attached and explain specifically where the adjuster’s numbers don’t match market reality in your area. Many adjusters will increase their offer by 10 to 20 percent when presented with solid local evidence rather than national pricing data.

Use Multiple Estimates to Strengthen Your Position

If the gap remains large, obtain a second estimate from another reputable Sacramento shop. Insurance companies respect competing estimates because they demonstrate a pattern in local pricing. When you submit the second estimate, note in your response that two independent shops arrived at similar figures, which validates the accuracy of both. This approach works particularly well for older vehicles where depreciation calculations become subjective and adjusters are more willing to negotiate based on concrete repair data.

Once you’ve secured fair repair valuations and documented the adjuster’s methodology, you’re positioned to address what happens when repair costs exceed the vehicle’s market value-the total loss determination that can dramatically change your claim’s direction.

When Your Vehicle Becomes a Total Loss

A total loss declaration fundamentally changes your claim because the insurer stops paying for repairs and instead offers you the vehicle’s fair market value. Most Sacramento accident victims don’t realize they can challenge this determination, and many accept lowball valuations without understanding California’s specific rules. The threshold that triggers a total loss declaration varies by insurer but typically falls between 70 and 80 percent of fair market value. If your vehicle’s repair costs exceed that percentage, the insurance company declares it totaled rather than repaired. The problem is that insurers often manipulate fair market value downward to reach the total loss threshold faster, which reduces what they ultimately owe you. You need to understand how this calculation works and what documentation strengthens your position during negotiations.

How Insurers Determine Fair Market Value for Totaled Vehicles

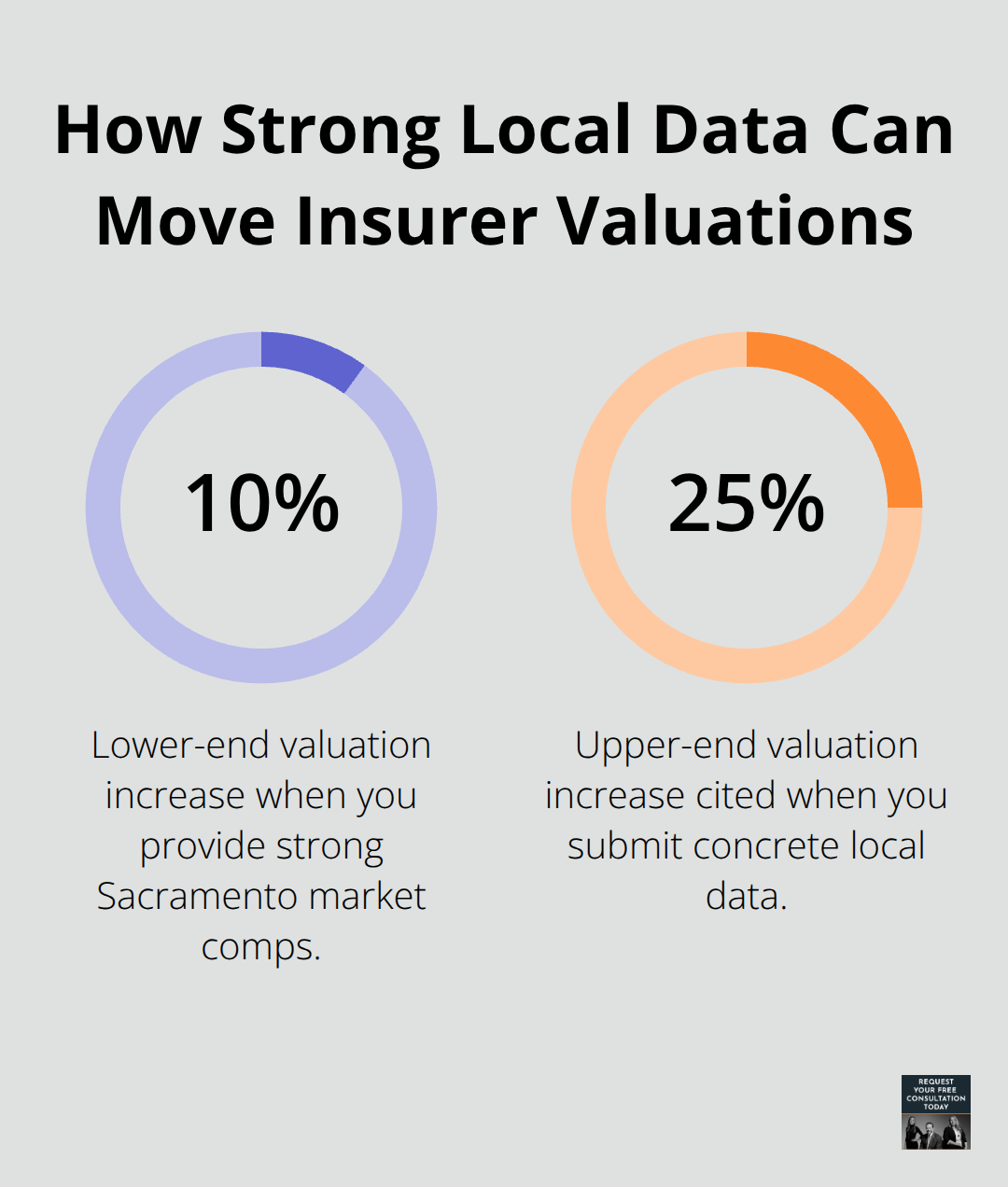

Insurers use valuation tools like CCC Valuations or Mitchell to generate fair market value estimates, but these software programs rely on national data that frequently undervalues Sacramento-area vehicles. The tools don’t account for local market conditions, recent upgrades, or exceptional maintenance that increases a vehicle’s actual worth. Request the insurer’s valuation report and compare it against current listings for identical or nearly identical vehicles in Sacramento County. Check dealer inventory, private sales on Craigslist and Facebook Marketplace, and pricing guides specific to your region. If the insurer’s fair market value estimate falls below what similar vehicles actually sell for locally, document this discrepancy in writing and submit it with comparable listings attached. Many insurers increase their valuation by 10 to 25 percent when presented with concrete local market data rather than relying solely on national software estimates.

Challenging Salvage Value Calculations

Once the insurer declares your vehicle a total loss, they’ll deduct the salvage value from their fair market value offer. Salvage value is what the vehicle would fetch if sold to a junkyard or salvage auction, typically ranging from 200 to 800 dollars depending on the vehicle’s age and condition. Request an itemized breakdown showing how the insurer calculated salvage value. Some adjusters inflate this figure to reduce the final settlement amount. If the salvage value seems high, obtain a quote from a local Sacramento salvage yard to challenge the number.

Negotiating the Total Loss Settlement

Respond to the total loss offer in writing with your market research attached and state your minimum acceptable amount based on comparable vehicle sales. Include documentation of any recent repairs or upgrades that enhance value, such as a new transmission, suspension work, or premium tires installed within the past two years. The insurer’s obligation to act in good faith under California law requires them to justify their valuation with specific market data, not generic software outputs. If the gap between their offer and your research remains substantial, request mediation through your state insurance commissioner’s office rather than accepting an unfair settlement.

Final Thoughts

Sacramento property damage claims require systematic documentation and strategic negotiation from the moment a crash occurs. Start by photographing the damage from multiple angles within 24 to 72 hours, collecting your vehicle’s service records and maintenance receipts, and obtaining a detailed repair estimate from a certified Sacramento shop within two to three weeks. Store all communications with your insurer including emails, call notes, and letters, as this documentation package becomes your negotiation foundation.

Request a written explanation of how the adjuster calculated their valuation and compare their figures against current market listings for similar vehicles in Sacramento County and repair rates from local shops. If the offer falls short, respond in writing with your evidence attached and state a specific counteroffer based on your research. Don’t accept the first offer, and don’t authorize repairs until you complete this comparison.

For total loss claims, challenge the insurer’s fair market value estimate by submitting comparable vehicle sales from your local market and request an itemized breakdown of how salvage value was calculated. If negotiations stall, consider mediation through the California Department of Insurance or consulting with a property damage attorney. We at Schaar & Silva LLP assist Sacramento accident victims in evaluating their claims and securing fair valuations for their losses.