A car accident in Santa Cruz County is stressful enough without discovering your insurance doesn’t cover all your damages. If the at-fault driver carries minimal liability coverage, you’re left facing a significant gap between what they owe and what you actually need.

We at Schaar & Silva LLP help accident victims navigate underinsured motorist situations every day. This guide walks you through your options when standard coverage falls short.

What Underinsured Motorist Coverage Actually Covers

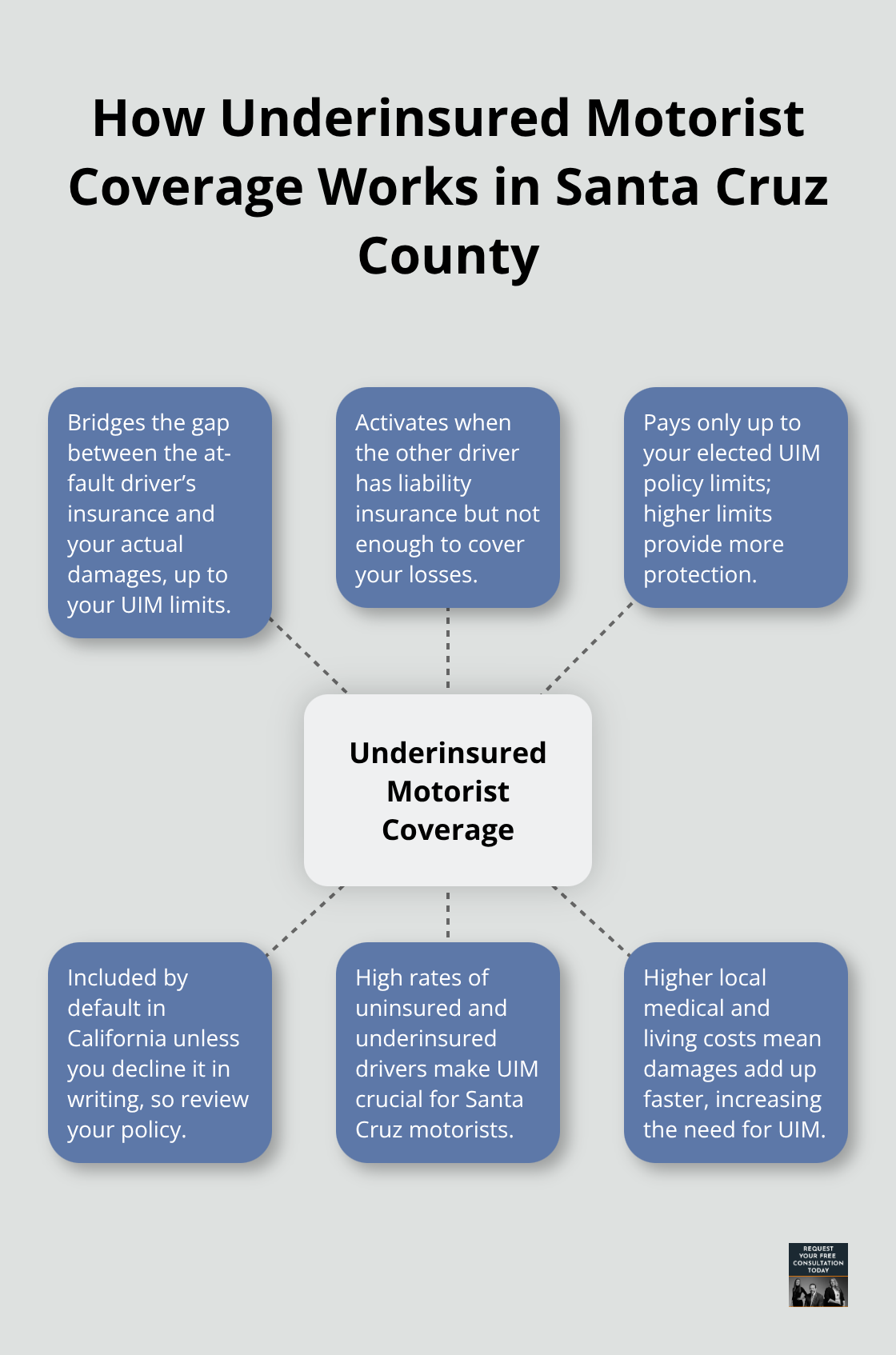

Underinsured motorist coverage activates when the at-fault driver carries liability insurance, but their policy limits don’t cover your actual damages. California requires drivers to carry at least $15,000 per person and $30,000 per accident in liability coverage, according to the California Vehicle Code. That sounds reasonable until you face $50,000 in medical bills, lost wages, and pain and suffering. If the other driver has only the state minimum and your damages exceed that amount, the gap falls on you unless you have underinsured motorist protection. Your own insurance policy steps in to bridge that gap, paying the difference between what the at-fault driver’s insurance covers and your actual losses, up to your policy limits. Most Santa Cruz County residents don’t realize this coverage exists on their policies by default-you must actively decline it in writing to lose it. The Insurance Research Council reported that about 16.6% of California drivers were uninsured in 2019, and underinsured drivers represent an even larger problem.

A driver with a $25,000 liability limit might seem insured until a serious accident happens.

When the Numbers Don’t Add Up

Consider a realistic Santa Cruz scenario: another driver hits you while carrying $15,000 in liability coverage. Your medical expenses cost $40,000, lost wages total $12,000, and pain and suffering is valued at $20,000-a total of $72,000. The at-fault driver’s insurance pays their $15,000 maximum. Without underinsured motorist coverage, you absorb the remaining $57,000 yourself. With it, your own policy covers up to your underinsured motorist limit, which typically matches your liability limit. If you carry $50,000 in underinsured motorist coverage, your insurer pays $35,000 (the $50,000 limit minus the $15,000 already paid by the other driver). The remaining $22,000 gap still exists, but at least you recover substantially more. Santa Cruz County’s higher cost of living makes adequate coverage especially important-medical care and living expenses here exceed state averages, meaning damages accumulate faster than in less expensive regions.

Why Santa Cruz Residents Face Real Exposure

Higher living costs in Santa Cruz County mean your actual damages climb quickly after an accident. A month of physical therapy at local clinics, rental car expenses during recovery, and lost income from interrupted work add up fast. If your underinsured motorist limit equals your liability limit, you’re protected proportionally. Many drivers carry only the state minimum $15,000 in liability, which also caps their underinsured motorist coverage at $15,000 unless they explicitly purchased higher limits. This creates a dangerous situation in Santa Cruz, where medical and living costs are substantially higher than the statewide average. The smart approach involves matching your underinsured motorist limit to your actual assets and income needs, not just the legal minimum. Annual policy reviews help confirm your coverage reflects current Santa Cruz County expenses, especially after life changes or income increases.

Moving Forward with Your Coverage

Understanding what underinsured motorist coverage actually pays is the first step. The next step involves knowing exactly what to do when an accident happens and you discover the other driver’s insurance falls short.

Steps to Take After an Accident with an Underinsured Driver

Act Within the Critical First 24 Hours

The first 24 hours after an accident determine how smoothly your underinsured motorist claim proceeds. At the scene, move vehicles to safety if possible and call 911 to document the crash officially. Obtain the other driver’s name, license number, address, license plate, vehicle description, and insurance information directly. Take photos of vehicle damage, road conditions, traffic signals, and street signs from multiple angles. Collect contact information from at least two witnesses and note their observations about how the accident happened.

Do not sign statements admitting fault or accepting responsibility at the scene. Document only facts: time, location, weather, vehicle positions, and what you observed. A police report creates an official record that confirms the at-fault determination and documents the other driver’s insurance details, making it invaluable evidence later. Request the report number and file a copy with your own insurer within 24 hours. Filing within 30 days of an accident improves claim approval odds significantly. Delays or incomplete initial reports give insurers ammunition to deny or minimize payouts, so speed and accuracy during this window matter significantly.

Seek Medical Care and Build Your Documentation Record

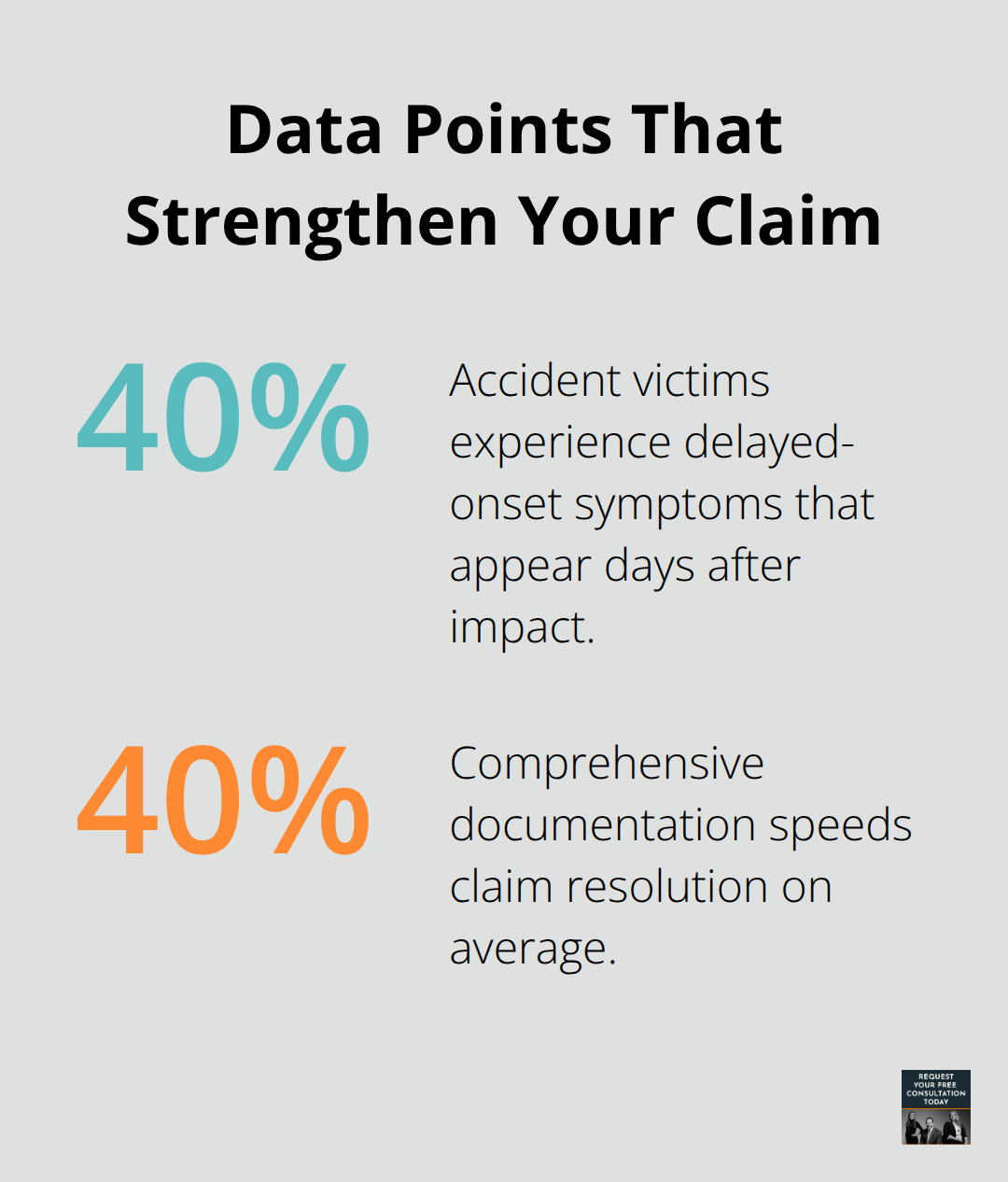

Seek medical attention immediately, even if you feel fine. Research shows about 40 percent of accident victims experience delayed-onset symptoms (like neck pain, headaches, or back injuries) that appear days after impact. A medical record dated shortly after the accident strengthens your claim and links your injuries directly to the crash.

Keep every medical receipt, bill, and treatment record organized in a dedicated folder. Document lost wages with pay stubs and employer notices confirming missed work days. Maintain a detailed damages log tracking medical costs, rehabilitation expenses, medications, transportation costs, rental car charges, and income loss. Comprehensive documentation settles claims roughly 40 percent faster on average, so organized records directly accelerate your recovery. Store copies digitally to prevent loss.

Notify Your Insurer and File Your Underinsured Motorist Claim

Notify your own insurance company promptly and formally request a claim for underinsured motorist coverage. Provide the police report number, medical records, bills, and witness statements. Your insurer will verify that the at-fault driver’s liability limit falls short of your actual damages before activating your underinsured motorist coverage. This verification step confirms the claim qualifies under your policy terms.

Understanding your specific policy limits and how they interact with the at-fault driver’s coverage prevents surprises later when settlement discussions begin. Your insurer calculates the gap between what the other driver’s insurance paid and your total damages, then determines what your underinsured motorist coverage owes. This calculation directly affects how much additional compensation you receive. Once you’ve submitted complete documentation and your insurer has verified the underinsured status, you’re positioned to pursue recovery beyond the at-fault driver’s limits.

Recovering More Than the At-Fault Driver’s Insurance Pays

After you’ve documented everything and filed your underinsured motorist claim, the real work begins. Your own insurer will calculate what they owe based on the gap between the at-fault driver’s liability limit and your total damages. But here’s the reality: initial settlement offers from insurers typically fall 30 to 50 percent below fair value. This is where most Santa Cruz accident victims make a critical mistake-they accept the first number without pushing back.

Push Back Against Lowball Offers

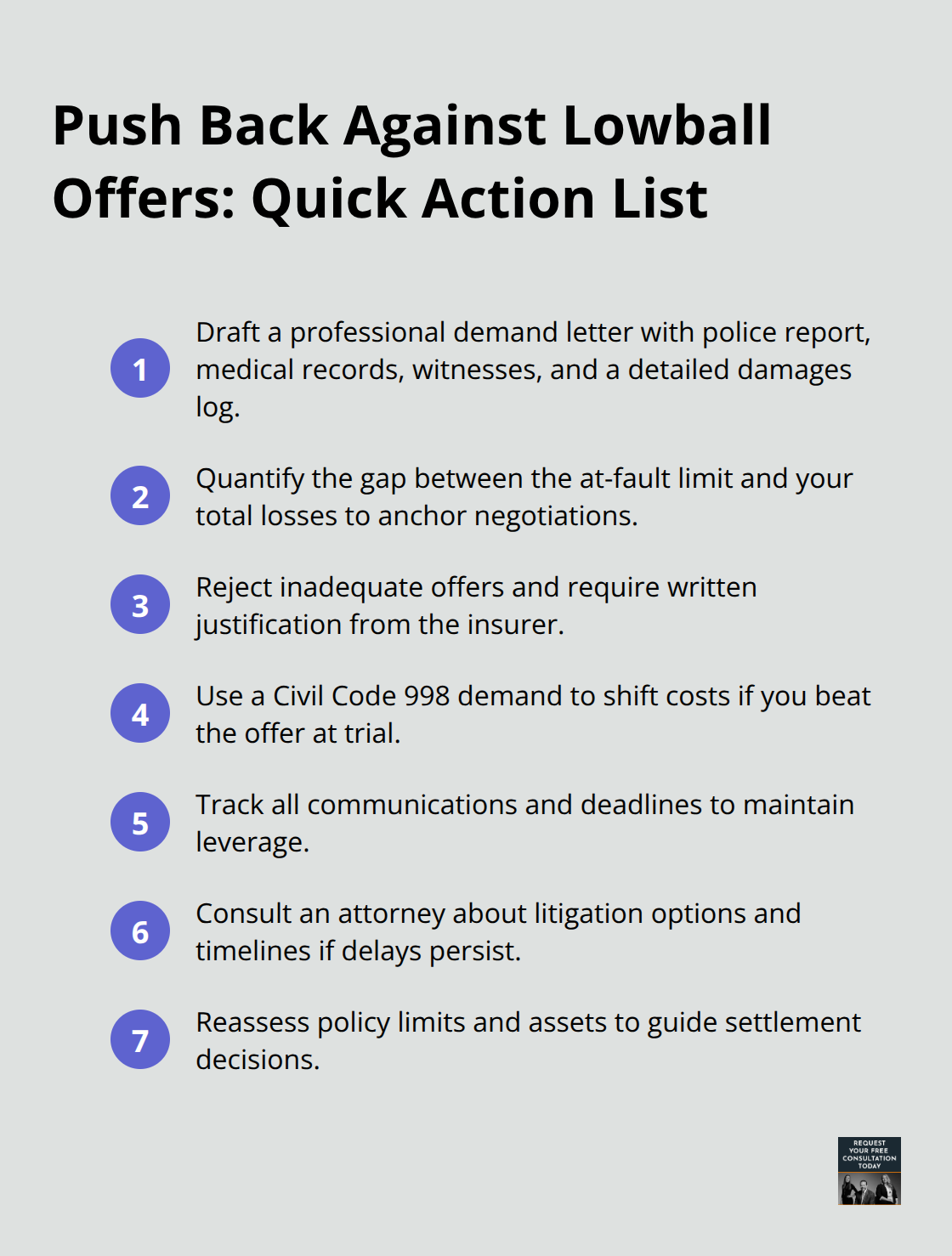

You possess leverage that most people don’t realize. A professional demand letter referencing your police report, complete medical records, witness statements, and detailed damages log forces the insurer to justify their offer in writing. If the at-fault driver’s insurance paid $15,000 and your actual damages total $72,000, your underinsured motorist coverage should bridge a substantial portion of that gap. Don’t settle for less than what the evidence supports.

If your insurer delays or refuses to pay what you’re clearly owed, California case law like Jordan v. Allstate and Maslo v. Ameriprise establishes that insurers have a duty of good faith and fair dealing. You can assert this duty to pressure them toward timely payment.

Use a Civil Code 998 Demand to Shift Negotiations

A Civil Code 998 demand-a formal settlement offer-shifts the negotiating dynamic significantly. If your insurer rejects a reasonable 998 demand and you ultimately recover more at trial, California law allows you to recover costs beyond your underinsured motorist limit (including attorney fees and court costs). This mechanism exists specifically to discourage lowball offers and reward claimants who refuse to accept unfair settlements.

Understand Your Litigation Timeline and Options

Litigation typically lasts six to eighteen months in Santa Cruz County, and California gives you two years from the accident date to file a personal injury lawsuit. This timeline protects your rights if settlement negotiations stall. An attorney identifies whether suing the at-fault driver directly makes financial sense based on their assets and whether they own property or have wages that could be garnished. Some drivers carry virtually no assets, making a judgment uncollectible. Others have resources that justify pursuing a lawsuit.

Evaluate Whether to Pursue Legal Action

The decision to litigate depends on your specific damages, the at-fault driver’s financial situation, and how aggressively your insurer negotiates. Early legal representation-often on a contingency basis where you pay nothing unless you recover-can improve your results substantially. This distinction between collectible and uncollectible judgments determines whether you recover additional compensation beyond what your underinsured motorist coverage provides. Don’t navigate this alone or accept the first offer thinking it’s your only option.

Final Thoughts

Underinsured motorist Santa Cruz coverage protects you when the at-fault driver’s insurance falls short of your actual damages. This protection exists on your policy by default unless you’ve signed a written waiver, making it one of the most overlooked safety nets available to local drivers. The gap between California’s minimum liability limits and real-world accident costs is substantial, especially in Santa Cruz County where medical care and living expenses exceed state averages.

Your coverage options depend on three critical decisions: matching your underinsured motorist limit to your liability limit, maintaining comprehensive documentation after an accident, and refusing to accept lowball settlement offers. Initial settlement offers typically run 30 to 50 percent below fair value, giving you room to negotiate or pursue litigation. The two-year window to file a personal injury lawsuit provides real leverage during settlement negotiations, and a professional demand letter backed by police reports, medical records, and witness statements forces insurers to justify their offers.

We at Schaar & Silva LLP help Santa Cruz accident victims navigate underinsured motorist situations and recover fair compensation. Our team assists with medical bill coordination, property damage evaluation, and the legal strategy needed to maximize your recovery. If you’re facing an underinsured motorist claim, contact us for a consultation to discuss your specific situation and next steps.