Car accidents happen without warning, and understanding what is bodily injury on car insurance can make the difference between financial protection and devastating costs.

We at Schaar & Silva LLP see how this coverage protects Santa Cruz County drivers when they’re responsible for injuring others in crashes. California requires this insurance, but many drivers don’t fully grasp what it covers or how much they need.

What Does Bodily Injury Coverage Actually Include?

Bodily injury coverage pays medical bills, lost wages, and pain and suffering compensation when you injure someone else in a car accident. This coverage handles hospital costs, rehabilitation expenses, and legal fees if the injured person sues you. The Insurance Information Institute reports the average bodily injury claim reached $15,000 in 2020, but severe injuries can generate claims that exceed $100,000. Your policy also covers funeral expenses if someone dies in an accident you cause.

How Bodily Injury Differs from Property Damage Coverage

Property damage coverage pays for vehicle repairs and damaged property, while bodily injury focuses solely on human injuries. Medical payments coverage works differently too – it pays your passengers’ medical bills regardless of fault, but bodily injury only activates when you’re at fault. Personal injury protection covers your own injuries in no-fault states, but California doesn’t require PIP coverage.

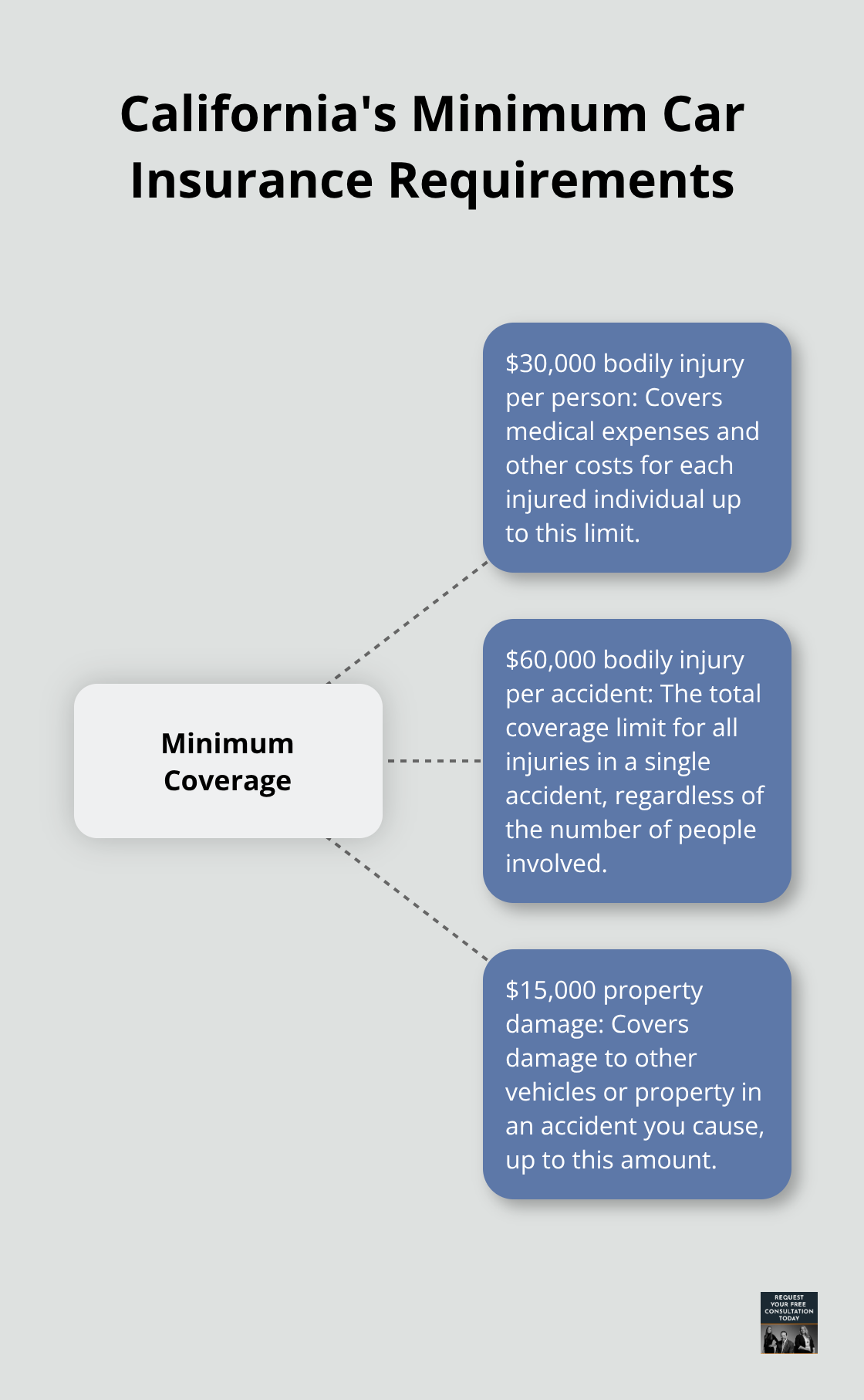

California’s Minimum Requirements Fall Short

California mandates $30,000 per person and $60,000 per accident for bodily injury coverage, plus $15,000 for property damage. These minimums often fall short of actual accident costs. A single emergency room visit averages $2,200 according to the National Association of Insurance Commissioners, while surgery can cost $50,000 or more.

Why Higher Limits Make Financial Sense

Smart Santa Cruz drivers choose $100,000 per person and $300,000 per accident limits (often written as 100/300). The DMV suspends registration if you lack proof of insurance, and insurance companies must electronically report your coverage status. Low-cost insurance programs exist for drivers who can’t afford standard rates.

The next question becomes: how do these coverage limits actually work when an accident happens, and what factors determine your premium costs?

How Do Coverage Limits Actually Work?

Santa Cruz County follows California’s state minimums of $30,000 per person and $60,000 per accident, but these amounts create dangerous financial gaps. When you carry 30/60 limits and injure three people in an accident, each person can receive up to $30,000, but the total payout stops at $60,000 even if all three need the maximum amount. This means the third person might receive nothing if the first two claims exhaust your policy limits.

The National Association of Insurance Commissioners found that 35% of drivers don’t understand their coverage limits, which creates massive liability exposure for Santa Cruz residents.

Smart Coverage Choices for Real Protection

We recommend 100/300/100 limits for most Santa Cruz drivers. This provides $100,000 per person, $300,000 per accident, and $100,000 property damage coverage. Your premium increases roughly 15-20% when you jump from minimum to 100/300 limits, but this small cost prevents personal bankruptcy from serious accidents.

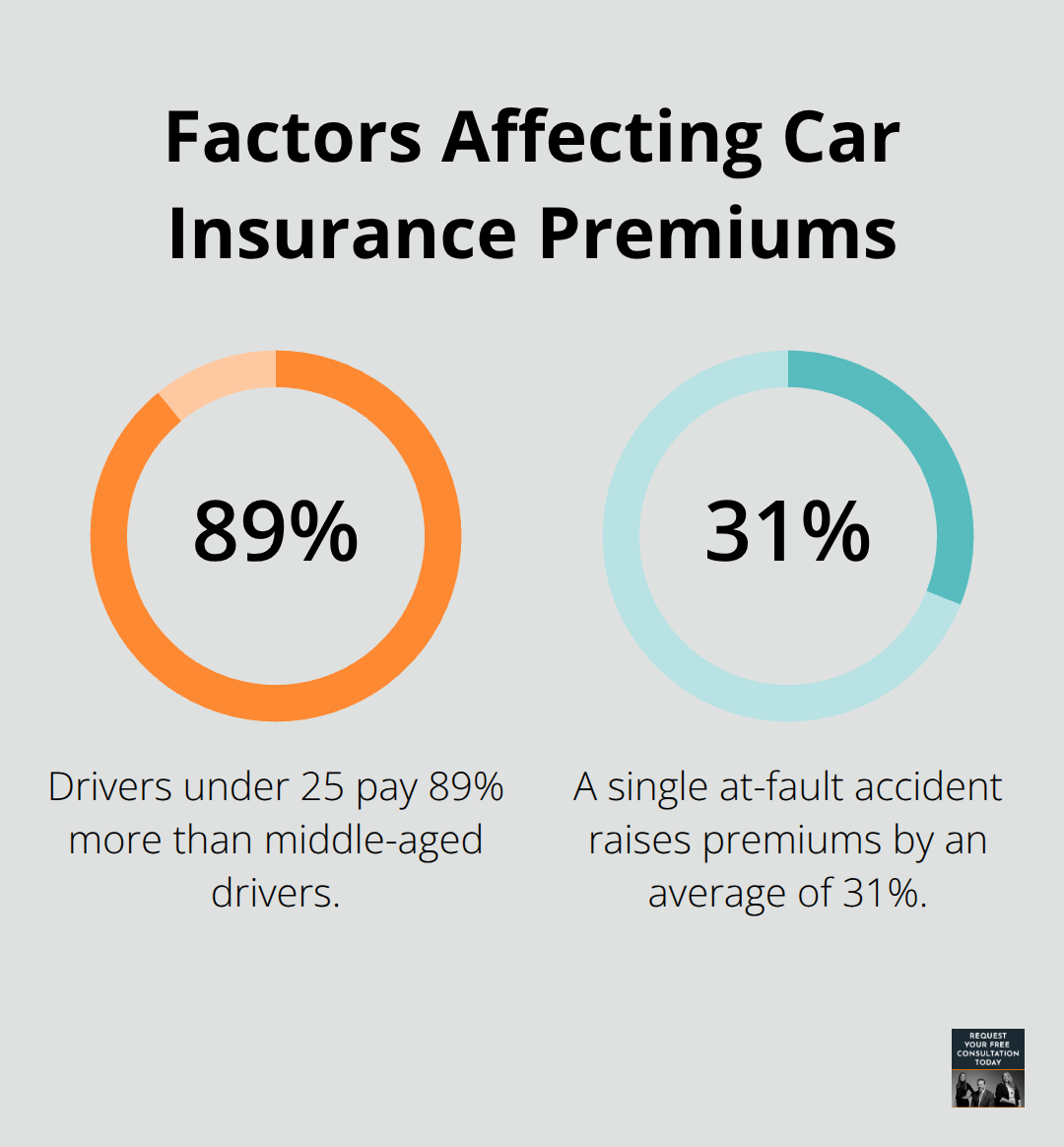

Insurance companies calculate your rates based on your record, age, vehicle type, and credit score in California. Drivers under 25 pay 89% more than middle-aged drivers according to recent industry data, while a single at-fault accident raises premiums by an average of 31%.

Premium Factors You Can Control

Your vehicle choice dramatically impacts costs. Luxury cars and sports vehicles cost 40-60% more to insure than standard sedans. Continuous coverage prevents rate increases, as gaps trigger higher-risk classifications (insurance companies view coverage lapses as red flags).

Defensive courses can reduce premiums by 5-10% with most insurers. Bundling auto and home insurance typically saves 10-25% on both policies. Santa Cruz drivers with excellent credit save up to $800 annually compared to those with poor credit scores.

When Coverage Limits Matter Most

Real accidents show why adequate limits matter. A pedestrian injury can generate $200,000 in medical bills within the first month. Multiple vehicle accidents with serious injuries routinely exceed $500,000 in total claims. Your personal assets become vulnerable when claims exceed your policy limits.

These coverage decisions become critical when accidents actually happen and you need to file claims with insurance companies.

When Does Your Bodily Injury Coverage Actually Pay

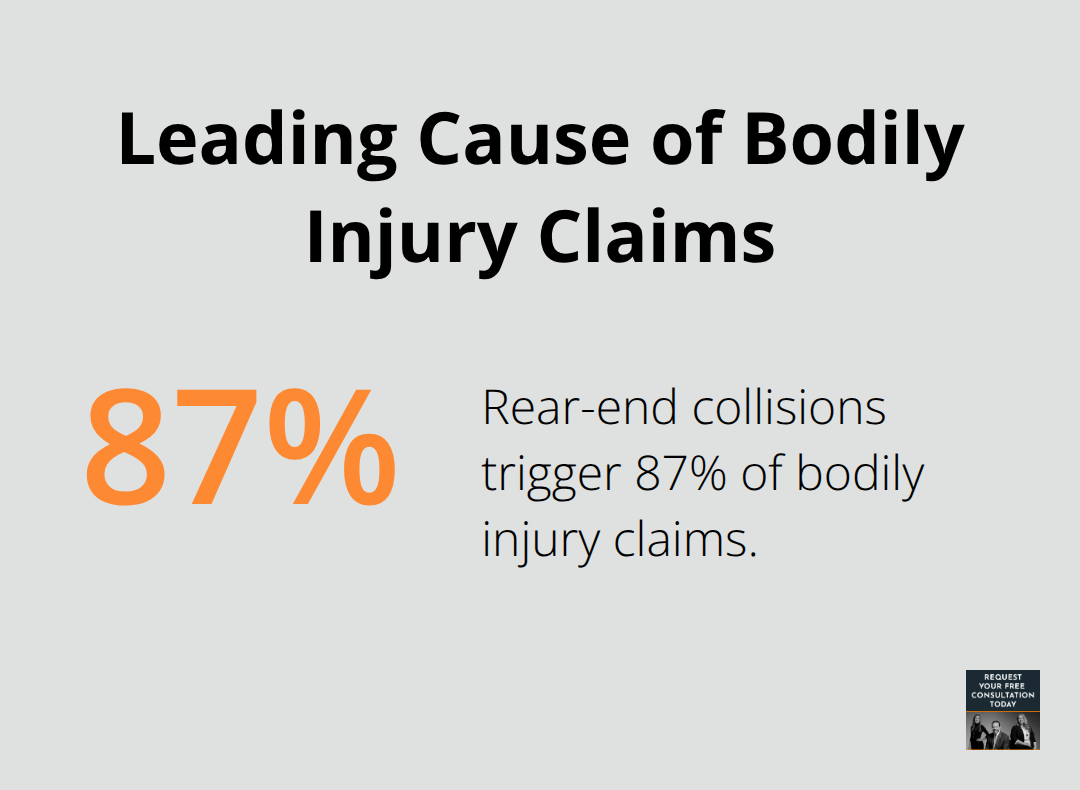

Your bodily injury coverage activates the moment police or insurance investigators determine you caused an accident that injured someone else. Rear-end collisions trigger 87% of bodily injury claims according to the National Highway Traffic Safety Administration, followed by left-turn accidents and intersection crashes. Running red lights, texting while driving, or failing to yield right-of-way automatically makes you liable for injuries. Weather conditions don’t excuse fault – if you slide on wet pavement and hit a pedestrian, your coverage still applies.

Coverage Extends Beyond Medical Bills

Your policy pays far more than hospital costs. Lost wages represent 40% of total bodily injury payouts and cover income the injured person loses during recovery. Pain and suffering damages often equal or exceed medical expenses in serious cases. Rehabilitation costs, physical therapy, and ongoing care all fall under your coverage. If someone dies in an accident you cause, your policy covers funeral expenses (averaging $9,000 in California). Legal defense costs get covered separately from your policy limits, meaning a $100,000 policy provides $100,000 for damages plus attorney fees.

Insurance Companies Move Fast After Accidents

Insurance adjusters contact injured parties within 24-48 hours of reported accidents. They record statements, review medical records, and calculate settlement offers quickly. The Insurance Research Council found that 95% of bodily injury claims settle without going to court, but initial offers typically start at 40-60% of actual damages. Insurance companies profit by paying less than full value and create adversarial relationships with injured parties.

Legal Representation Changes Everything

Smart accident victims hire attorneys before they accept any settlement offers. Legal representation increases average payouts by 3.5 times according to industry data. Attorneys understand insurance tactics and negotiate from positions of strength rather than desperation. They also handle all communication with insurance companies, preventing victims from making statements that damage their cases.

Final Thoughts

Santa Cruz County drivers who understand what is bodily injury on car insurance protect themselves from financial disaster when accidents happen. California’s minimum requirements of $30,000 per person and $60,000 per accident create dangerous gaps that bankrupt families who face serious injury claims. The average bodily injury claim of $15,000 appears manageable until you confront multiple victims or catastrophic injuries that generate hundreds of thousands in damages.

Smart drivers select 100/300 limits that cost only 15-20% more than minimums but provide real protection. Your personal assets face risk when claims exceed policy limits (making adequate coverage essential rather than optional). Higher limits prevent personal bankruptcy and protect your financial future when serious accidents occur.

After any accident that involves injuries, contact law enforcement immediately and avoid admissions of fault. Document everything with photos and witness information before you leave the scene. Most importantly, contact Schaar & Silva LLP before you speak with insurance adjusters who profit from low settlements and quick closures.