A lost wages auto crash can wipe out your income overnight, leaving you scrambling to pay bills while you recover. The financial damage extends far beyond the immediate paycheck you’re missing-it compounds with medical costs, lost benefits, and time away from work.

At Schaar & Silva LLP, we help accident victims in Santa Cruz County, Sacramento, and Oakland recover the income they’ve lost. This guide walks you through calculating your lost wages, documenting your claim, and understanding your legal options to get compensated.

How the Accident Hits Your Wallet Right Now

Immediate Income Loss Stops Everything

An accident stops your income immediately, but the financial damage spreads faster than most people realize. If you’re hospitalized or stuck at home recovering, you’re not earning anything while bills keep arriving. The Insurance Research Council found that claimants who hire representation recover 3.5 times more compensation than those who handle claims alone-this gap widens quickly without proper documentation. Your employer may hold your job, but they won’t hold your paycheck while you heal.

Adrenaline masks injuries in those first hours after a crash, so you might not realize how serious your condition is until days later when you can’t return to work. That’s when lost wages become real. For hourly workers, every shift missed means immediate loss. For salaried employees, you might still get paid during short absences, but extended recovery depletes sick days and vacation time you’ve saved for years. Self-employed workers face the harshest blow: no work means zero income, period. You lose not just today’s earnings but future contracts too.

California Labor Code Section 226 requires employers to provide itemized wage statements showing gross earnings, hours, and deductions. Get copies of these statements immediately after your accident because they become your foundation for calculating what you actually lost.

Long-Term Injuries Reshape Your Earning Power

The longer you’re away from work, the harder the financial pressure becomes. Long-term injuries don’t just steal current paychecks-they can permanently reduce your earning capacity. A construction worker with a spinal injury might never return to heavy labor. A teacher with chronic pain from a brain injury might need to switch to part-time work. These shifts in career trajectory represent years of lost income that compound over your working life.

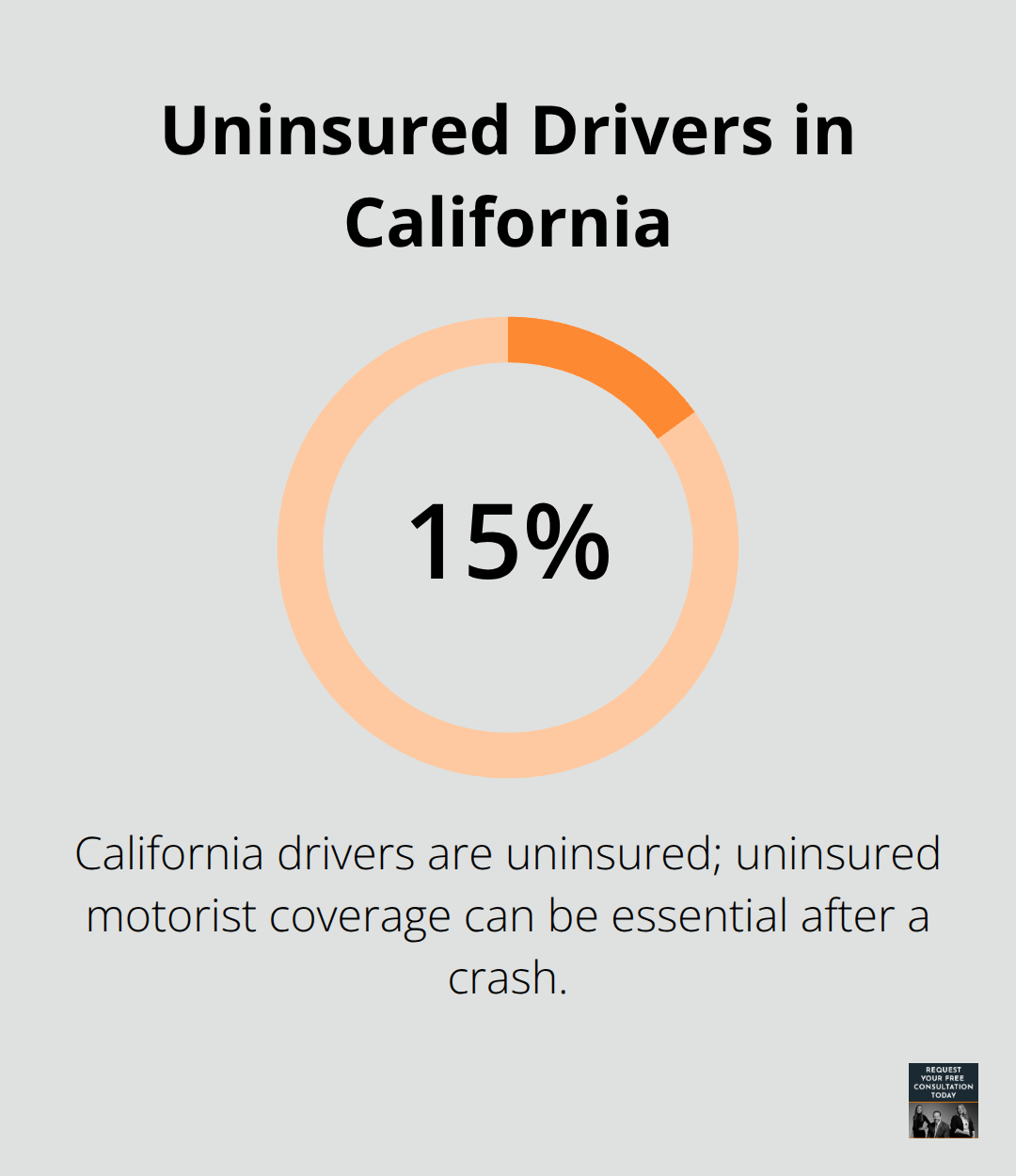

California’s minimum auto insurance limits updated in 2025 under SB 1107 now require $30,000 per person and $60,000 per incident, but serious injuries often cost far more in lost wages alone. About 15 percent of California drivers are uninsured, which means if an uninsured driver hit you, your own uninsured motorist coverage becomes critical.

Hidden Costs That Add Up Fast

Medical appointments eat time too-physical therapy sessions, follow-up visits with surgeons, mental health counseling. That’s time off work that doesn’t appear as a hospital stay but still costs you income. Benefits matter more than people expect: health insurance premiums, retirement contributions, stock options, and bonuses all disappear when you’re not working. If you receive commissions or bonuses based on performance, those losses multiply quickly. A salesperson who can’t work for three months loses not just base salary but commission on deals they would have closed. Vacation days used for recovery are days you can’t use later for actual vacation.

The financial picture gets messier with every week away from work, which is why documenting everything from day one matters so much. When you move forward with calculating your actual losses, you’ll need solid records of what you earned before the accident and what you’ve lost since.

Building Your Lost Wages Documentation

Start Collecting Documents Immediately After Your Accident

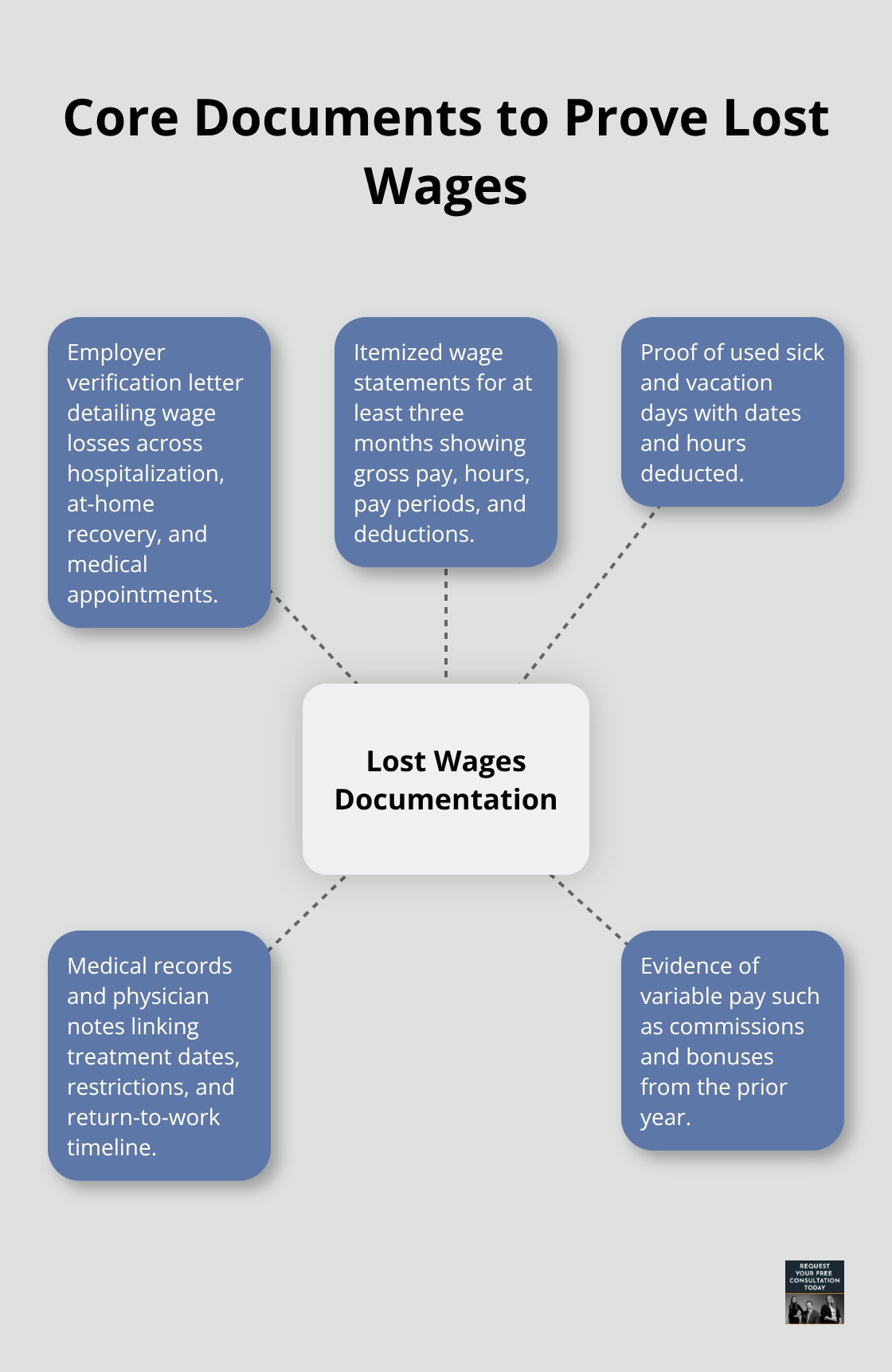

Collect documents the day after your accident, not weeks later when memories fade and records become harder to find. Your employer’s wage verification letter stands as the single most important document you’ll need-this isn’t optional, it’s foundational. The letter must break down exactly what you lost: wages during hospitalization, wages during at-home recovery, wages lost to medical appointments, and any sick or vacation days you burned through.

California Labor Code Section 226 mandates that employers provide itemized wage statements with gross earnings, hours worked, pay periods, and deductions, so request copies of every statement from the three months before your accident. These statements establish your baseline earnings and make your claim credible to insurers.

Calculate Your Lost Income Based on Your Work Type

For salaried employees, multiply your daily rate by missed workdays to reach your total. For hourly workers, account for the actual hours you would have worked, including overtime if you typically worked extra hours during that season. Self-employed workers face a harder task but have more flexibility: pull your tax returns from the past two years, gather invoices and contracts showing what you would have earned, and document cancelled assignments or lost contracts directly tied to your injury.

One critical mistake we see constantly is underestimating lost income because workers forget about variable pay. If you earn commissions, bonuses, or performance-based income, your losses are significantly higher than base salary alone. A real estate agent who misses three months loses not just their salary but all commissions on deals they would have closed-that’s often 50 to 75 percent of their actual income. Pull your commission statements and bonus history from the past year to show what percentage of your income came from variable sources.

Account for Benefits Losses That Have Real Monetary Value

Benefits losses get overlooked constantly, yet they represent real money out of your pocket. Health insurance premiums, retirement contributions, stock options, and paid time off all carry monetary value. If your accident forced you to use two weeks of vacation days for recovery, you’ve lost those days forever-quantify that loss. Some employers contribute to 401k plans or offer profit-sharing; document those contributions as part of your wage loss. For your employer’s verification letter, ask them to calculate the total value of benefits you lost during your recovery period, not just base wages.

Secure Written Cooperation From Your Employer

If your employer resists providing detailed documentation, that’s a red flag-they’re either disorganized or reluctant to help your claim. Contact the Human Resources department directly and request written confirmation in writing, not verbal promises. If an employer refuses to cooperate, a formal request typically unlocks cooperation quickly.

Track Medical Appointments and Lost Work Hours

Keep meticulous records of every medical appointment-dates, times, duration-because each one represents lost work hours. Track mileage to appointments and any wages lost specifically because of medical treatment, separate from general recovery time. Insurance adjusters scrutinize these calculations heavily, so precision matters. Inconsistencies between your wage claim and your medical records will be used against you to reduce your settlement, so coordinate with your physician to document a clear recovery timeline that aligns with when you actually returned to work. Once you’ve gathered all this documentation and calculated your total losses, you’re ready to understand how to file your claim and what legal options exist to recover what you’ve lost.

Legal Options for Recovering Lost Wages

File Your Insurance Claim With Complete Documentation

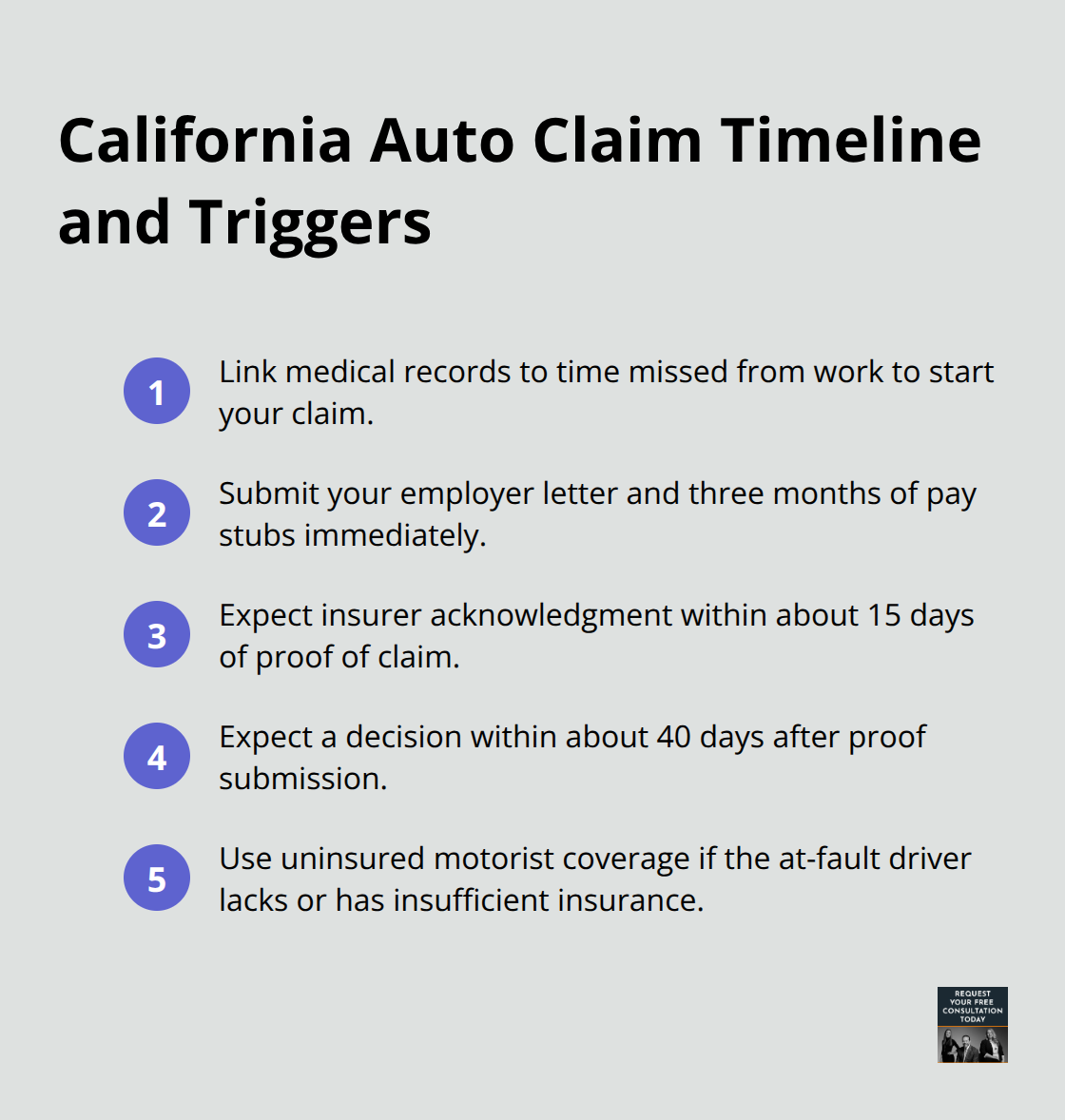

Your third-party claim against the at-fault driver’s liability insurance starts the moment medical records link your injuries to time away from work. Submit your employer’s verification letter immediately along with pay stubs from the three months before your accident-these documents form the foundation of your claim. The California Department of Insurance requires insurers to respond within about 15 days and decide within about 40 days after you submit proof of claim, so track your submission date carefully.

California’s updated minimum liability limits from SB 1107 require $30,000 per person and $60,000 per incident, yet serious injuries often exceed these caps significantly. When the at-fault driver carries insufficient coverage or no insurance at all, your own uninsured motorist coverage activates to cover lost wages up to your policy limits. About 15 percent of California drivers are uninsured, making this protection essential for your financial security.

Many accident victims accept early settlement offers before their recovery timeline becomes clear, which means they undervalue lost wages significantly. Wait until your physician provides a realistic return-to-work date, then recalculate your total losses including any future earning capacity reduction before you settle.

Pursue a Personal Injury Lawsuit When Insurance Falls Short

A personal injury lawsuit becomes necessary when the insurance settlement falls short of your actual losses or when liability is contested. Pure comparative negligence in California means your recovery gets reduced by your percentage of fault-if you’re 30 percent at fault, you still recover 70 percent of your damages. The lawsuit process takes longer than insurance settlement, typically months or years depending on case complexity, but the potential recovery justifies the wait when injuries are serious. Economic damages in your lawsuit include not just wages lost to date but also diminished earning capacity if your injury permanently limits your ability to work at your previous level or earn at your previous rate.

Quantify Future Earning Losses With Expert Analysis

Vocational experts quantify future losses by calculating the difference between what you would have earned without the injury versus what you can realistically earn going forward, accounting for your age and remaining working years. This analysis transforms vague claims about “lost potential” into concrete dollar figures that courts and juries understand. The Insurance Research Council found that claimants with representation recover 3.5 times more than unrepresented claimants, a gap that widens dramatically when future earning capacity enters the calculation. Your attorney coordinates with your physician to document how injuries affect your work capacity, preserves evidence before it disappears, and prevents you from making recorded statements to adjusters that could undermine your claim later.

Final Thoughts

The first 48 hours after your accident determine whether you’ll recover lost wages fully or accept a settlement that leaves you short. Secure the scene, call 911 if anyone is injured, and move to safety if possible. Exchange the other driver’s license, registration, and insurance details, then write down the police report number immediately. California law requires reporting to the DMV within 10 days if injuries or property damage exceed $750, so file that report quickly to create an official record.

Start collecting documents the day after your crash and request your employer’s wage verification letter breaking down exactly what you lost across hospitalization, at-home recovery, medical appointments, and used vacation time. Gather pay stubs from three months before the accident to establish your baseline earnings, and keep copies of every medical bill, prescription receipt, and treatment record. This documentation transforms vague claims into concrete proof that insurers cannot dispute, and it forms the foundation of your lost wages auto crash recovery.

A lost wages auto crash recovery depends heavily on having someone in your corner who understands California’s insurance laws and knows how to negotiate with adjusters. The Insurance Research Council found that claimants with legal representation recover 3.5 times more compensation than those handling claims alone. At Schaar & Silva LLP, we help accident victims throughout Santa Cruz County, Sacramento, and Oakland recover the income they’ve lost while focusing on healing.