A car accident turns your world upside down. Medical bills pile up, insurance calls come in, and you’re left wondering what happens next.

At Schaar & Silva LLP, we’ve guided hundreds of people through auto accident claims. This guide walks you through each step-from filing your claim to getting paid.

Understanding Auto Accident Claims

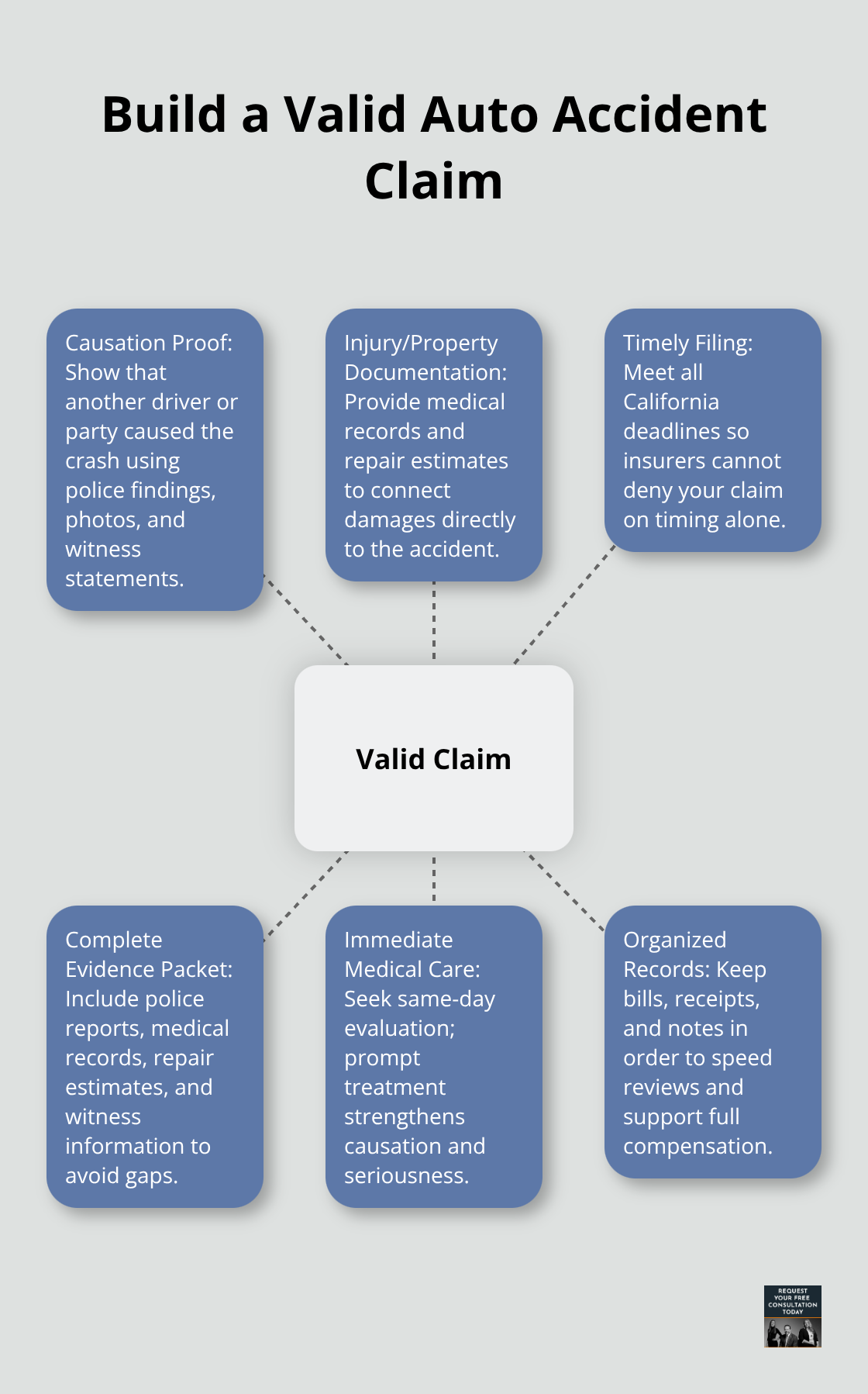

What Makes a Valid Auto Accident Claim

A valid auto accident claim requires three foundational elements: proof that someone else caused the accident, documentation of your injuries or property damage, and timely filing. Without all three, insurers will deny or minimize your claim. The California Department of Insurance emphasizes that claims must include police reports, medical records, repair estimates, and witness statements. If you skip any of these, adjusters will use the gaps against you.

Many people file incomplete claims and watch them get rejected, then waste months resubmitting.

Start gathering evidence immediately at the accident scene. Photograph vehicle damage, road conditions, and the other driver’s information. Get the police report number and request it within days. Medical documentation is non-negotiable; even minor injuries require a doctor’s visit with written findings. Without it, insurers treat your claim as worthless regardless of your actual pain.

Damages You Can Actually Recover

California law allows you to recover two categories of damages: economic and non-economic. Economic damages are straightforward-medical bills, lost wages, and vehicle repair costs. Non-economic damages cover pain and suffering, emotional distress, and loss of enjoyment. The distinction matters because insurers fight harder on non-economic damages.

According to industry data, the average auto accident settlement nationwide sits around $19,000, but this number masks enormous variation. Catastrophic injuries with clear medical costs settle for far more; soft tissue injuries without ongoing treatment settle for far less. The settlement formula is simple: add your past medical bills, future medical bills, past lost wages, and future lost wages, then multiply by a pain-and-suffering factor tied to your treatment and impairment. Online calculators cannot capture this accurately.

Santa Cruz County accident claims rarely exceed six figures unless spinal injuries or permanent disability exist. The California Department of Insurance notes that about 94% of California auto claims from major carriers settle within 90 days, meaning your timeline depends on how quickly you document damages.

California’s Time Limits Are Shorter Than You Think

California gives you exactly three years to file a personal injury claim from the accident date, but this deadline is deceptive. If the claim involves a government vehicle or public entity, notice requirements shrink to six months or 30 days depending on the agency. Missing these tight deadlines bars recovery entirely-no exceptions. For property damage claims, the statute extends to four years, but insurers push settlement much faster.

Most claims resolve within six to eight months if you pursue them aggressively; cases that stall often miss the window for optimal settlement value. The California Department of Insurance requires insurers to acknowledge your claim within 15 days, begin investigation immediately, and respond to your proof of claim within 40 days. If they miss these timelines, file a complaint with the California Department of Insurance.

Acting fast strengthens your position because fresh evidence is stronger evidence and witness memories remain sharp. Delay weakens your claim and gives adjusters reasons to question your injuries or their severity. Once you understand what damages you can recover and the time pressure you face, the next step involves gathering the specific documentation that transforms a claim from incomplete to compelling.

The Claims Filing Process

Gather Evidence at the Accident Scene

The moment after an accident, most people feel overwhelmed and unsure what to document. This confusion costs money. Photograph vehicle damage from multiple angles, capture road conditions, traffic signals, and debris patterns. Obtain the other driver’s name, phone number, address, driver’s license number, and insurance information. Write down the police report number immediately and request the full report from the Santa Cruz County Sheriff’s Office or local police within 48 hours. The California Department of Insurance emphasizes that claims without police reports face immediate skepticism from adjusters.

Take photos of your injuries if visible, though this feels awkward in the moment. Witness contact information is gold; many accidents lack witnesses, so if someone saw what happened, collect their phone number and email before they leave. Medical documentation cannot wait either. Visit an urgent care or emergency room the same day if possible, even for seemingly minor injuries. Adjusters routinely deny claims where injury treatment starts weeks after the accident because they assume the injuries weren’t serious.

Document Medical Records and Expenses

Your medical records must show objective findings: X-rays, imaging, examination notes, and doctor’s assessment. Soft tissue injuries without imaging are treated as exaggerated by insurers, so push your doctor to order imaging if pain persists. Gather all receipts for medical expenses, pharmacy bills, rental car charges, and any other accident-related costs. Spreadsheet these with dates and amounts; disorganized documentation signals to adjusters that you’re not serious about your claim.

Notify Your Insurance Company Immediately

Notify your insurance company within 24 hours, not days. The California Department of Insurance requires insurers to acknowledge your claim within 15 working days, but calling immediately shows you’re engaged and creates a paper trail. When you call, state the facts only: date, time, location, vehicles involved, and that you’re injured. Do not admit fault, apologize, or speculate about what happened. Say exactly this: I was in an accident and need to file a claim.

The insurer will send a form or direct you to their website. Complete it fully and submit it with your police report, medical records, repair estimates, and photos attached. Do not omit sections or leave fields blank; incomplete submissions give adjusters reasons to delay. Once filed, an adjuster will contact you within days to schedule an inspection and statement.

Work with Adjusters During Inspection

Before the adjuster calls, write down your account of the accident in chronological order while details are fresh. During the inspection, the adjuster will examine your vehicle and may photograph it. Stay present during this inspection and take your own photos of what the adjuster documents. If additional damage surfaces later, the insurer may refuse to cover it, claiming it existed before the accident.

After the inspection, the adjuster will request your medical records directly from providers. Do not wait for them to ask; send copies yourself with a cover letter listing what you’re submitting. The California Department of Insurance mandates that insurers respond to proof of claim within 40 days. If 40 days pass without a response, file a complaint with the California Department of Insurance at 1-800-927-4357. This pressure often accelerates settlement discussions and moves your claim toward the negotiation phase where settlement offers arrive and your real leverage emerges.

Negotiating and Reaching Settlement

Evaluate Settlement Offers Against Your Actual Damages

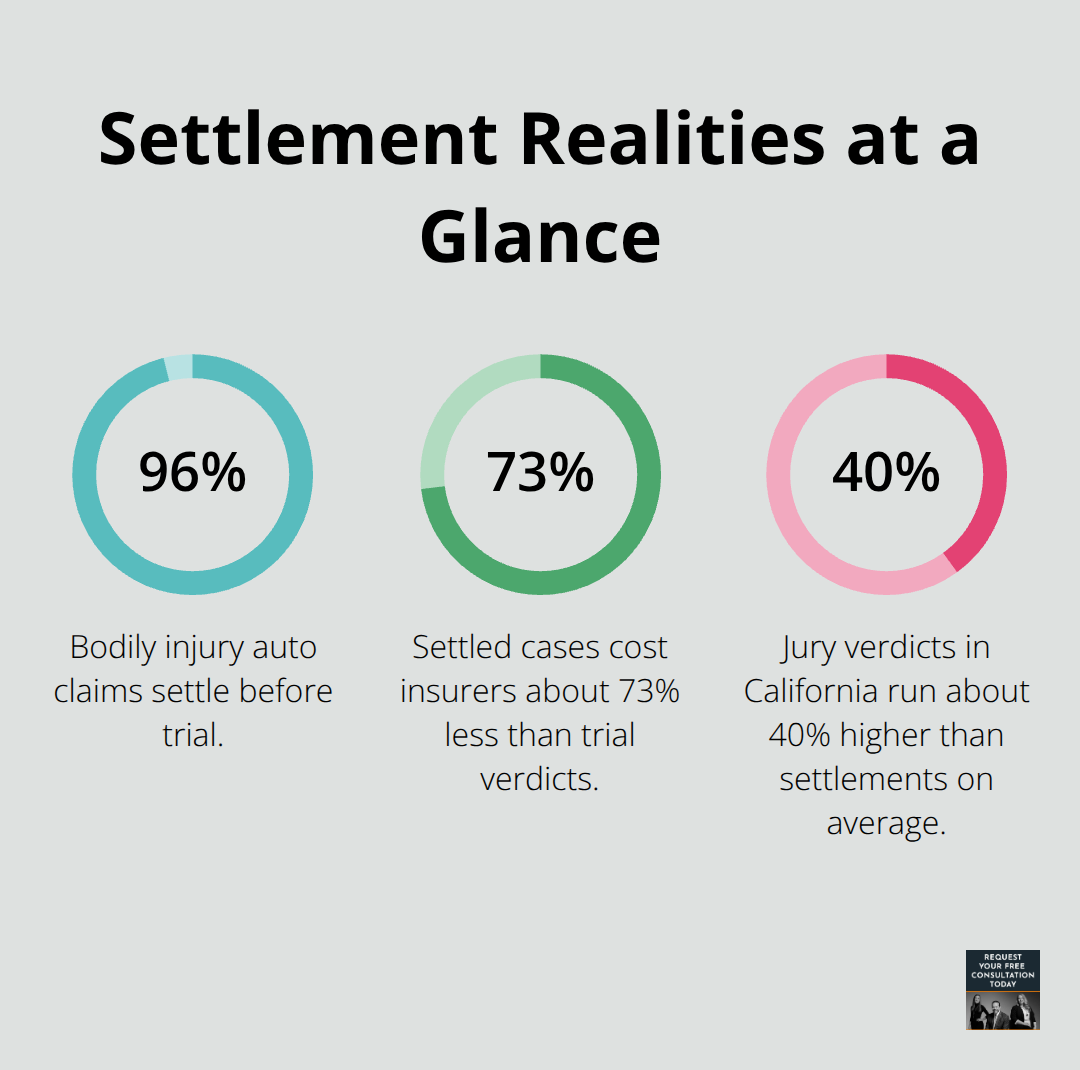

Your adjuster will contact you within two weeks of filing with a settlement offer. This first offer is almost always low. According to the American Insurance Association, settled cases cost insurers about 73% less than trial verdicts, which is why they push settlement early before you fully understand your claim’s value. The Insurance Research Council reports that 96% of bodily injury auto claims settle before trial, but that statistic masks a critical reality: most people accept the first offer because they don’t know better.

When the adjuster presents a number, ask for an itemized breakdown showing how they calculated economic damages and what they assigned to pain and suffering. If they refuse or provide vague language like “your pain and suffering is worth 2 times medical bills,” push back immediately. That formula is arbitrary and undervalues most claims. A 2024 industry analysis shows that jury verdicts in California run about 40% higher than settlements on average, which means accepting 60% of potential verdict value costs you real money.

Calculate your economic damages precisely: list every medical bill, every pharmacy charge, every day missed from work with hourly rate, rental car costs, and any other direct expenses. This total should exceed the economic portion of the offer, or the offer is mathematically insufficient. For pain and suffering, research what similar injuries settled for in Santa Cruz County. Herniated discs, for example, commonly settle in the $40,000 to $150,000 range depending on treatment, while neck injuries settle higher. If your settlement offer’s pain and suffering component falls below what comparable cases received, the offer is low.

Recognize Common Insurance Company Tactics

Insurance companies use specific tactics because they work on people who don’t understand the process. One tactic is the exploding offer: the adjuster claims the settlement is only good for 10 days, creating false urgency. Ignore this pressure. California law gives you three years to file suit, and most claims settle within six to eight months anyway.

A second tactic involves low-balling your future medical costs. If your doctor recommends ongoing physical therapy, surgery follow-up, or pain management, the adjuster may claim these are speculative and refuse to fund them. Counter this by obtaining a medical provider’s written estimate of future treatment costs and timeline. A third tactic involves offering to pay your medical bills directly to providers rather than paying you the full settlement amount. This looks generous but actually transfers negotiating power to the medical providers, who may accept less than their bills to get paid faster. Demand the full settlement amount be paid to you so you control how medical liens are resolved.

Push Back on Low Offers With Documentation

Send a written response to the adjuster explaining your objections and proposing a counter-offer 20% to 30% higher than their figure. Most adjusters will move their number when faced with documented reasoning rather than emotional arguments. Demand they show their math. Ask what medical records they reviewed, what future treatment they accounted for, and whether they factored in permanent impairment. Most adjusters will not have done this work thoroughly, and your questions force them to.

If your medical treatment exceeded $50,000, insurers typically order independent medical exams to challenge your doctors’ findings. When this happens, bring your own medical records to that exam and have your treating physician prepare a detailed response to the independent examiner’s report. Settlement negotiations in Santa Cruz County in 2024 averaged higher when claimants documented ongoing treatment and obtained imaging confirming soft tissue injuries, which means your documentation directly influences the offer amount.

Know When to Consult an Attorney

If adjusters refuse to budge after two or three exchanges, consult an attorney. Many firms offer free case reviews and can often recover enough additional settlement value to cover their fees and then some. At Schaar & Silva LLP, we serve Santa Cruz County and help clients evaluate whether their settlement offers reflect the true value of their claims. We can assist with medical bill issues and property damage evaluation to strengthen your position before settlement discussions conclude.

Final Thoughts

Auto accident claims follow a predictable path from filing to settlement, but success depends on how thoroughly you document each step. The process rewards preparation-you gather evidence immediately, notify your insurer within 24 hours, respond to adjuster requests with complete documentation, and evaluate settlement offers against comparable cases in Santa Cruz County. Most claims settle within six to eight months when you stay organized and push back on low offers with data rather than emotion.

The first settlement offer is rarely fair because adjusters count on people accepting quickly without confidence in their claim’s value. You now understand that economic damages are straightforward to calculate, that pain and suffering factors vary widely by injury type and treatment, and that jury verdicts run about 40% higher than settlements on average. Use this knowledge to counter low offers with written responses showing your math and demanding itemized breakdowns from adjusters.

Consulting an attorney makes sense when adjusters refuse to move their numbers after two or three exchanges. We at Schaar & Silva LLP serve Santa Cruz County and help clients evaluate whether settlement offers reflect true claim value, assist with medical bill issues, and navigate property damage evaluation. Contact us for a free consultation to review your specific situation and clarify whether your auto accident claims settlement is adequate.