After an auto accident, insurance companies often make low initial offers hoping you’ll accept quickly. We at Schaar & Silva LLP know that settlement negotiation tactics can mean the difference between inadequate compensation and what you actually deserve.

This guide walks you through how insurers calculate payouts, what red flags to watch for, and how to build a stronger negotiating position with evidence and documentation.

How Insurance Companies Value Your Claim

The Formula Insurers Use (and Why It Fails You)

Insurance companies apply a formula-based approach to calculate settlement values, but the numbers they arrive at often underestimate what your claim is truly worth. They start with your medical bills and multiply them by a factor typically ranging from 1.5 to 5, depending on injury severity. However, this method ignores the real impact on your life. The Insurance Research Council reports that represented claimants recover on average 3.5 times more than unrepresented claimants, even after attorney fees. This gap exists because insurers count on you accepting their initial low offer without understanding how damages should actually be calculated.

What Insurers Actually Count

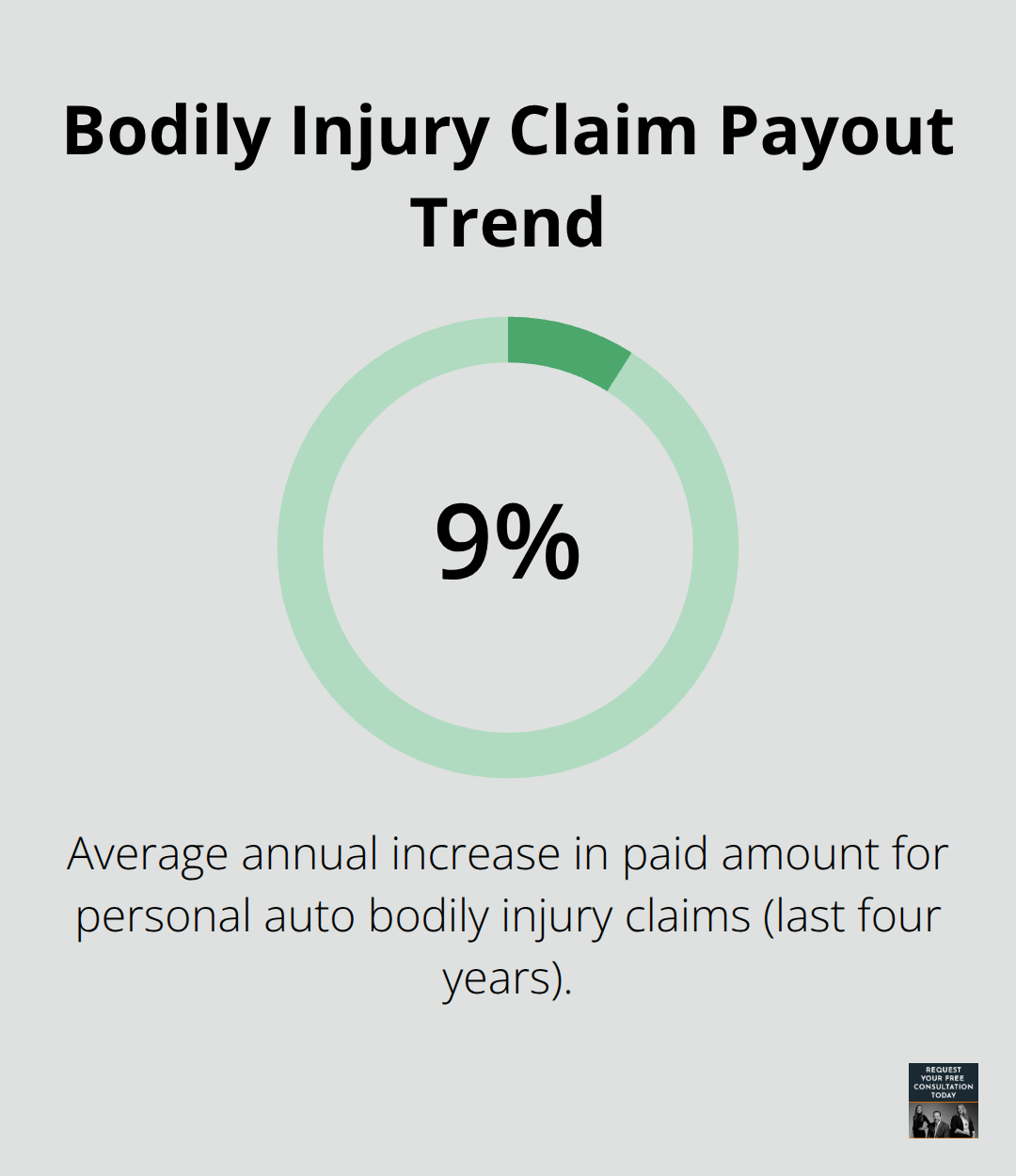

Insurers factor in documented past medical costs, lost wages from time off work, and sometimes future medical expenses. Yet they deliberately anchor their numbers to inflated medical bills rather than to the actual injury severity. Over the last four years, the average paid per personal auto bodily injury claim has risen roughly 9% per year, yet insurers still resist settlements that reflect this trend. The reason is straightforward: they know most accident victims have no idea what their cases are worth.

Adjuster Tactics That Push Settlements Down

Adjusters use specific tactics to push settlements down before you have time to gather evidence. They request the same medical records multiple times, switch adjusters mid-claim to restart negotiations, or challenge whether your treatment was truly necessary by questioning the provider’s decisions. Two-thirds of third-party injury claims have a delta-V of 9 mph or less, yet many claimants receive advanced procedures like spinal injections and radiology early in treatment. Insurers exploit this by claiming your treatment was excessive relative to the accident impact, even when the treatment was clinically justified.

Red Flags in Initial Offers

Red flags appear immediately in their initial offers: they arrive within days of your accident before you’ve finished medical treatment, they reference only partial medical bills, they ignore lost wages entirely, or they include language suggesting this is their final offer when you haven’t even submitted a formal demand. If an insurer pressures you to sign a release quickly or suggests you don’t need an attorney, that’s a clear warning sign they’re trying to exploit your vulnerability. The strongest protection is thorough documentation from day one and professional representation that understands how to counter their anchoring tactics with evidence-based demands.

Building Your Case With Documentation and Evidence

Collect Evidence Immediately After the Accident

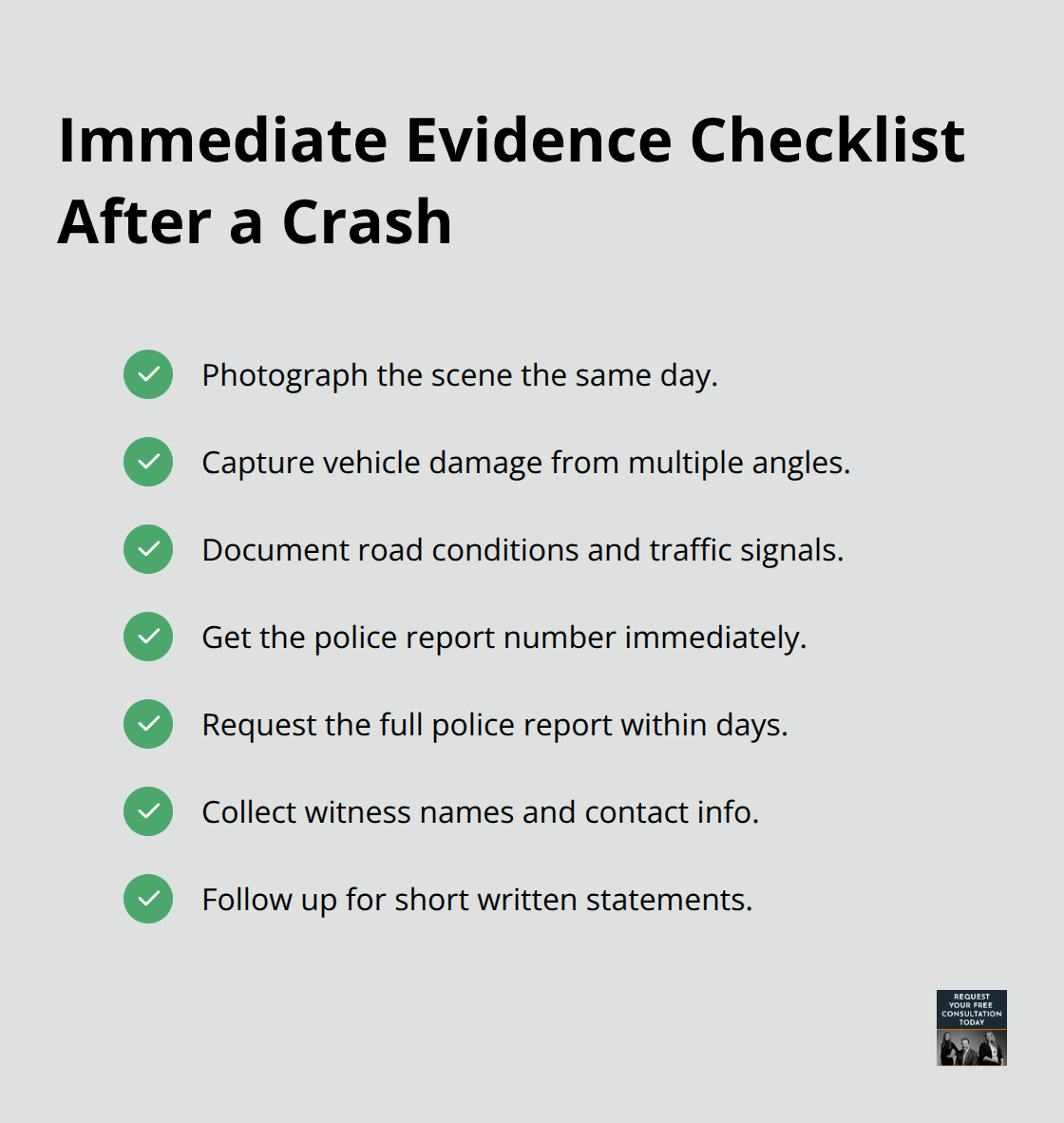

Photograph the accident scene from multiple angles on the day it happens, not weeks later. Capture vehicle damage, road conditions, and traffic signals in your images. Obtain the police report number immediately and request the full report within days. Gather contact information from all witnesses at the scene and follow up with written statements while their memory remains fresh.

This early documentation counters the insurer’s tactic of anchoring to inflated bills by establishing a clear factual record before memories fade or details get lost.

Organize Medical Records and Expense Documentation

Medical documentation forms the backbone of your claim, so attend every appointment and keep copies of all bills, imaging reports, test results, and provider notes. Create a single organized file with medical records, wage loss statements from your employer, receipts for accident-related expenses, and a daily symptom journal noting pain levels, activity limitations, and how injuries affect your daily life. This systematic approach proves that your treatment was medically justified and necessary, not excessive or premature as insurers often claim.

Structure Your Demand Letter Around Evidence

Your demand letter must be grounded in evidence, not emotion or inflated numbers. Open with a clear summary of liability, supported by police reports, witness statements, or dashcam footage. Outline your injuries with specific medical diagnoses and treatment dates, then calculate damages in three categories: past medical costs with itemized bills, lost wages with employer verification, and future medical expenses with provider recommendations. Price future care conservatively based on documented treatment plans, not speculation. Include a damages summary that shows how you arrived at your total figure.

Counter Offers With Documented Analysis

When the insurer responds with a counter-offer, evaluate it against your documented damages and policy limits rather than accepting pressure to settle quickly. If their offer falls far below your documented losses, counter with a detailed response explaining the gaps in their calculation and requesting specific justification for any reductions they propose. This discovery-based approach shifts the burden of proof to them and demonstrates you understand your claim’s actual value. Hold firm on numbers anchored to real expenses and clinical evidence.

Learn From Real Settlement Outcomes

Amica Mutual Insurance resolved a case for $18,000 after disputing $31,000 in inflated medical bills and questioning unjustified treatment decisions, proving that disciplined, evidence-based negotiation works better than accepting initial lowball offers. The core principle underlying this success is straightforward: injury makes the treatment; treatment does not make the injury. When you anchor your negotiations to proven injury severity and documented medical necessity, you shift the conversation away from what insurers want to pay and toward what your case actually warrants. This evidence-centered strategy prepares you to move forward into direct negotiations with insurance companies, where your documentation and clear demand become your strongest tools.

Why You Need an Attorney for Settlement Negotiations

An attorney transforms your negotiating position from reactive to evidence-driven. When you handle settlement talks alone, insurers exploit information asymmetry and apply pressure tactics designed to close cases quickly at reduced values. Unrepresented claimants accept offers worth far less than their documented damages because they lack the framework to evaluate fairness. The Insurance Research Council found that represented claimants recover on average 3.5 times more than unrepresented claimants, even after contingency fees. This multiplier exists because attorneys anchor negotiations to injury severity and clinical evidence rather than to inflated medical bills or emotional narratives.

How Attorneys Evaluate Your Claim’s True Value

An experienced attorney evaluates your case by analyzing your documented medical diagnoses, treatment progression, and functional limitations alongside your lost wages and future care needs. They calculate a demand figure grounded in these facts, not in what the insurer initially offered. When the insurer counters with a lowball response, your attorney identifies specific gaps in their calculation and responds with discovery-based questions that shift the burden of proof to them. This approach forces the insurer to justify their reductions with evidence rather than assumption. Your attorney also identifies damages you might overlook, including lost wages, future medical care, and pain and suffering that the insurer hopes you won’t claim.

Countering Insurer Pressure and Delay Tactics

Adjusters routinely request duplicate medical records, switch personnel mid-negotiation to restart discussions, or re-litigate liability months after your accident when you’re financially exhausted. Your attorney manages these communications and prevents you from making recorded statements that insurers later use to reduce your payout. When liability is disputed, your attorney counters with dashcam footage, police reports, witness statements, or accident reconstruction evidence rather than accepting the insurer’s narrative. If the insurer delays unreasonably, your attorney files a lawsuit to move the process forward, which typically accelerates settlement discussions because insurers know litigation costs them more in defense expenses and management overhead. California’s two-year statute of limitations creates breathing room that insurers exploit, so having counsel ensures deadlines are met and momentum is maintained throughout negotiations.

Managing Settlement Payment and Protecting Your Recovery

After settlement is reached, payment does not arrive immediately. Checks typically arrive within 10 to 21 business days, and your attorney deposits the funds, deducts the contingency fee (commonly 33 to 40 percent), and negotiates any medical liens or health insurance reimbursements before you receive your net amount. Medical liens and insurance subrogation claims can significantly reduce your final payout if not handled strategically. Your attorney negotiates these obligations when possible and ensures the settlement release covers current and reasonably anticipated future damages related to your injuries.

This final stage protects you from creditors and health insurers pursuing reimbursement from your settlement funds after you’ve already received your check.

Final Thoughts

Settlement negotiation tactics succeed when you anchor your position to documented evidence rather than emotion or pressure. Insurers count on you accepting quickly before you understand your claim’s value, so waiting until your medical treatment stabilizes and presenting a demand grounded in evidence shifts negotiating power in your favor. California’s two-year statute of limitations provides time, but act promptly, maintain organized records, and avoid social media posts about your case that insurers can use against you.

Accepting a settlement makes sense when the offer reflects your documented damages, your medical treatment has reached maximum improvement, and you’ve exhausted negotiation opportunities. Most cases settle faster and with less financial risk than litigation, particularly when liability is clear and your evidence is organized. However, if the insurer’s final offer falls significantly below your documented losses and policy limits allow for more recovery, pursuing litigation may yield better results despite longer timelines and higher costs.

After settlement is reached, checks typically arrive within 10 to 21 business days, and your attorney handles fee deductions and negotiates medical liens before you receive your net amount. We at Schaar & Silva LLP understand that settlement negotiations feel overwhelming when you’re recovering from injuries, and our team helps Santa Cruz County residents evaluate fair offers and counter lowball tactics. Contact us for a free consultation to discuss your specific situation and timeline.