![[Guide] to Understanding Every Stage of Your Settlement Process in 2026](https://schaarsilvalaw.com/wp-content/uploads/emplibot/accident-settlement-timeline-hero-1777680559.jpeg)

A car accident turns your life upside down. Between medical bills, insurance calls, and legal questions, the accident settlement timeline can feel overwhelming.

We at Schaar & Silva LLP help people in Santa Cruz County, Sacramento, and Oakland navigate every step of this process. This guide walks you through what happens after your accident, how insurance companies evaluate your claim, and when you’ll actually receive your settlement payment.

The First 48 Hours After Your Accident

Medical Care Cannot Wait

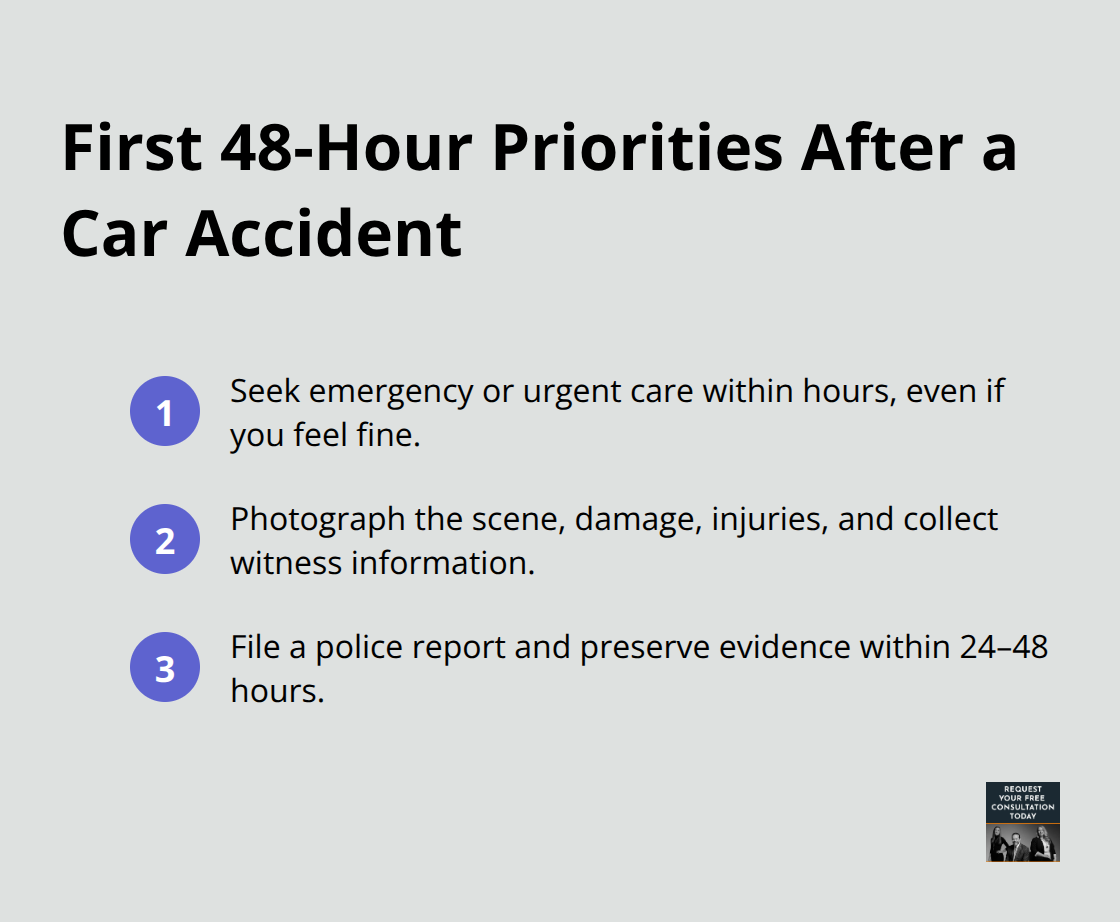

The decisions you make in the first two days after a car accident determine how much compensation you ultimately receive. Most people get this wrong. You need emergency medical care first, even if you feel fine. Injuries like whiplash, internal bleeding, and traumatic brain injury don’t always show symptoms immediately. Insurance companies watch for gaps of 48 to 72 hours between your accident and your first medical visit, and they use those gaps to argue your injuries are pre-existing or unrelated to the crash.

Get evaluated at an emergency room or urgent care facility within hours of the accident. Document everything the medical provider finds, including pain levels, imaging results, and initial diagnoses. This medical record becomes the foundation of your entire claim.

Photograph and Preserve Evidence Immediately

While you receive treatment, photograph the accident scene if you’re physically able. Take pictures of all vehicle damage, road conditions, traffic signs, weather, and your injuries. Get the names and phone numbers of any witnesses before they leave.

Police reports matter less than people think, but you should still file one for vehicle accidents. The report creates an official record, though it often contains errors or incomplete information. Preserve all physical evidence immediately after the accident. Keep the damaged vehicle, your clothing, medical records, receipts for expenses, and any surveillance footage you can obtain.

Request video from nearby businesses or traffic cameras within 24 to 48 hours, as most facilities only retain footage for 30 days. Send a formal preservation letter to the at-fault driver’s insurance company demanding they retain all evidence.

Handle Insurance Communications Carefully

Don’t give a recorded statement to the other driver’s insurance company, even if they call within 24 hours and pressure you. You’re not legally required to do it, and anything you say can be used against you later. If communication is necessary, keep it written and involve your attorney.

File your claim with your own insurance company promptly, but understand that their job is to minimize what they pay out, not to help you. Report the accident to your insurer within the timeframe specified in your policy, usually within 30 days. Provide basic facts but avoid detailed statements about how the accident happened or who was at fault.

Protect Your Claim on Social Media

Stay off social media completely. Defense teams routinely monitor accident victims’ social accounts and use posts about activities, outings, or statements about your condition to contradict injury claims later. Even innocent photos can be weaponized in settlement negotiations. The evidence you’ve collected and the medical records you’ve started building now move into the investigation phase, where insurance companies begin their formal evaluation of your claim.

How Insurance Companies Value Your Claim

The Adjuster’s Playbook

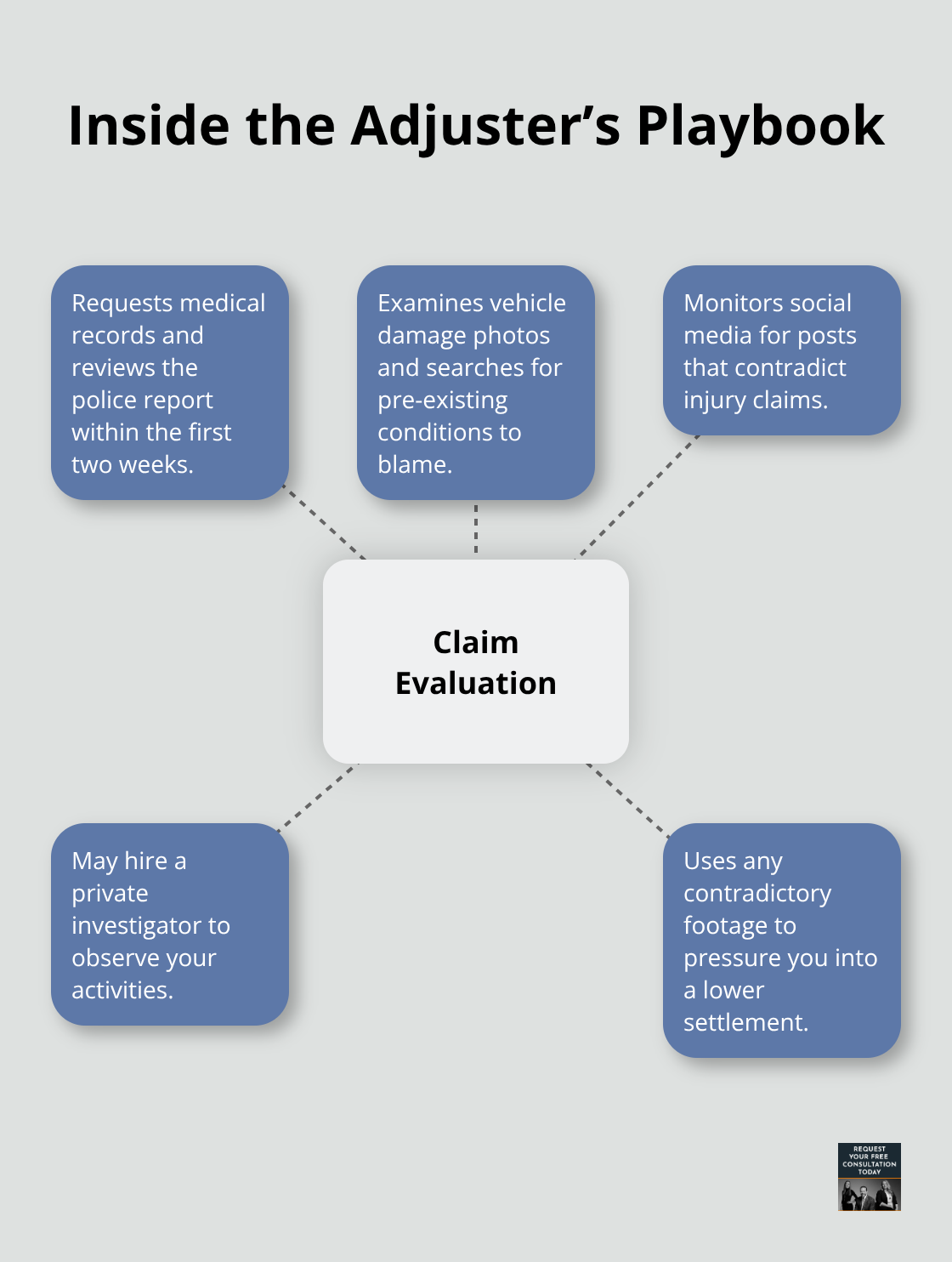

Insurance adjusters follow a predictable playbook when evaluating your claim, and understanding their methods gives you a significant advantage during negotiations. Within the first two weeks after your accident, the adjuster requests your medical records, reviews the police report, examines vehicle damage photos, and often pulls your medical history to identify pre-existing conditions they can blame instead. They monitor your social media accounts and may hire a private investigator to observe your activities. If they catch you on video doing something that contradicts your injury claims, they use that footage to pressure you into accepting a lower settlement.

Insurance companies delay deliberately. They know that financial pressure, mounting medical bills, and emotional exhaustion push accident victims to accept inadequate offers. Some adjusters employ stall tactics for months, hoping you’ll give up or run out of money. This is intentional strategy, not incompetence.

Medical Records Drive Your Claim’s Value

Your medical records form the centerpiece of your claim’s value. The adjuster calculates damages based on your treatment frequency, the type of care providers you saw, the duration of treatment, and whether your condition improved or worsened over time. A gap of two weeks without medical appointments signals to the insurer that your injuries weren’t serious. Conversely, consistent treatment from an emergency room visit through physical therapy lasting six months creates a compelling narrative of genuine injury.

Document every appointment, every cost, and every symptom. Keep receipts for medications, copays, and travel expenses related to medical care. This documentation becomes your strongest defense against low settlement offers.

Timing Your Settlement After Maximum Medical Improvement

Negotiation begins after you reach maximum medical improvement (MMI), the point where your doctors determine your condition has stabilized and major improvement is unlikely. This timing is critical. Accept a settlement before MMI, and you have no way to account for future medical expenses or long-term complications.

Most straightforward cases with minor injuries settle within three to six months, while complex cases involving serious injuries or disputed liability take 12 to 24 months. Insurance companies count on you not knowing this timeline. They present their first offer early, often within weeks of your accident, hoping you’ll accept before understanding the full scope of your damages. This initial offer is almost always substantially below fair value. Reject it.

Negotiating Multiple Rounds of Counteroffers

The insurer’s opening position leaves enormous room for negotiation. Expect multiple rounds of counteroffers, each closer to fair value but still designed to benefit the insurance company. Your settlement should cover past and future medical expenses, lost wages, property damage, pain and suffering, and emotional distress. If the insurer’s offer doesn’t account for all these categories, it’s incomplete.

Many accident victims accept settlements that fail to include future medical care, leaving them responsible for ongoing treatment costs. Don’t make this mistake. Understanding what your settlement must contain protects you from accepting an inadequate offer that leaves you financially vulnerable long after your case closes.

What Your Settlement Actually Covers

Economic and Non-Economic Damages in Your Settlement

Your settlement agreement specifies exactly what compensation you receive and what claims you release forever. This document is legally binding, so understanding what goes into it before you sign matters more than anything else in your case. Your settlement must cover all economic damages: past medical expenses, future medical care, lost wages from time off work, property damage to your vehicle, and costs for medical equipment or home modifications your injury requires.

Non-economic damages address pain and suffering, emotional distress, loss of consortium, and permanent scarring or disfigurement. Many accident victims make the critical mistake of accepting settlements that cover only past medical bills and lost wages, overlooking future treatment costs entirely. California law allows you to recover compensation for reasonably foreseeable future expenses directly caused by the accident.

The Release of Claims and Confidentiality Restrictions

The settlement includes a release of claims, which means you waive the right to sue for anything related to this accident after you sign. This is permanent and irreversible, so you cannot discover new injuries later and file another claim. Some settlements include confidentiality clauses preventing you from discussing the terms publicly, though California law restricts overly broad confidentiality provisions that would prevent you from reporting illegal conduct or cooperating with authorities.

How Insurance Companies Calculate Your Settlement Amount

The calculation of your settlement amount depends on several concrete factors that insurance companies use systematically. They multiply your special damages (your documented out-of-pocket costs like medical bills and lost wages) by a multiplier ranging from 1.5 to 5 depending on injury severity. A minor soft tissue injury might use a 1.5 multiplier, while a traumatic brain injury or permanent disability uses a 4 or 5 multiplier.

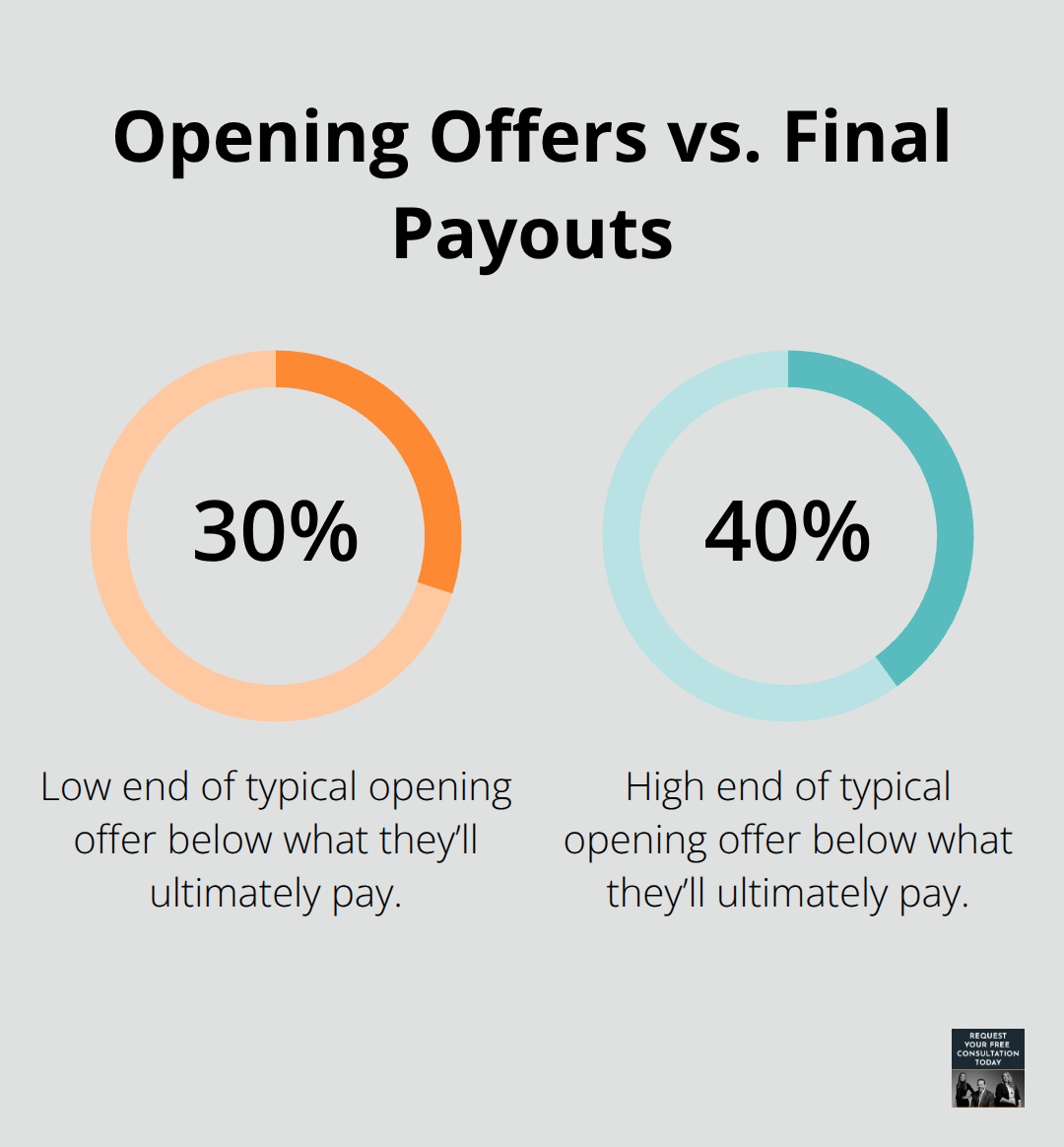

For example, if your special damages total $50,000 and your injury severity warrants a 3 multiplier, your pain and suffering calculation reaches $150,000, making your total settlement approximately $200,000 before attorney fees and liens. Insurance companies rarely offer this full amount initially. They anchor their opening offer low, typically 30 to 40 percent below what they’ll ultimately pay, counting on your financial desperation to accept quickly.

Timing Your Settlement Acceptance for Maximum Value

You should never accept a settlement offer within the first month after your accident. The insurer presents these early offers specifically because you haven’t reached maximum medical improvement and don’t yet understand your total damages. Timing your acceptance after your treatment concludes, your doctor confirms your prognosis, and you’ve gathered complete documentation of all expenses gives you negotiating power the insurer wants to prevent you from having.

Payment Structures: Lump-Sum Versus Structured Settlements

Payment arrives through different structures depending on what you negotiate. Lump-sum settlements pay your entire amount at once, typically within 30 to 45 days after you sign the settlement agreement and the release period expires. Structured settlements distribute payments over time, which can help manage cash flow but locks you into a payment schedule that cannot be changed if your circumstances shift. A financial advisor can help you understand the tax implications of your settlement structure, since some settlement components are tax-free while others may create tax liability depending on how they’re categorized.

Final Thoughts

Your accident settlement timeline follows a predictable path once you understand what happens at each stage. From the first 48 hours after your crash through the final payment, knowing what to expect removes uncertainty and prevents costly mistakes. You now understand why immediate medical care matters, how insurance companies calculate your claim’s value, and why accepting early settlement offers leaves money on the table.

The critical milestones in your case are straightforward: seek emergency medical care within hours of your accident, gather and preserve evidence immediately, reject the insurer’s first offer, document every medical appointment and expense, reach maximum medical improvement before negotiating seriously, and then evaluate multiple rounds of counteroffers before accepting a settlement that covers all economic and non-economic damages. Legal representation becomes important if your injuries are serious, if the accident involved a commercial vehicle or government entity, if you’re unsure about a settlement offer, or if the insurer denies your claim. The sooner you involve an attorney, the stronger your position becomes.

We at Schaar & Silva LLP help people in Santa Cruz County, Sacramento, and Oakland navigate this entire process and understand what your claim is actually worth. Contact us to discuss your case and let us guide you through each stage of your accident settlement timeline.