![[Guide] to Winning Better Terms in Your Auto Accident Settlement](https://schaarsilvalaw.com/wp-content/uploads/emplibot/settlement-negotiation-tactics-hero-1776902957.jpeg)

After a car accident, insurance companies rarely offer what you actually deserve on their first proposal. At Schaar & Silva LLP, we’ve seen settlement negotiation tactics that work-and we’ll show you exactly how to use them.

This guide walks you through the concrete steps to push back against lowball offers and get fair compensation for your injuries, medical bills, and vehicle damage.

What Counts as Fair Compensation

Medical Expenses and Future Care Costs

A fair settlement covers everything the accident cost you, both immediate and long-term. Insurance companies know most people underestimate their damages, which is why they start with offers that recover only 30 to 40 percent of actual losses. Medical expenses form the foundation of any settlement, but the number most people miss is future care costs. If you suffered a back injury requiring ongoing physical therapy, that compounds over years. Ongoing treatment expenses add up quickly and represent a significant portion of your total claim value.

Lost Wages and Earning Capacity

Lost wages matter too-not just what you missed while recovering, but reduced earning capacity if the injury limits your work long-term. Many accident victims fail to account for the income they’ll lose over months or years as they heal. This category often represents one of the largest components of your settlement, yet insurance adjusters frequently minimize it without solid documentation of your employment history and income projections.

Property Damage and Non-Economic Losses

Property damage seems straightforward until you realize repair estimates often undervalue structural or mechanical damage that surfaces later. Pain and suffering, the non-economic damage category, typically multiplies your medical bills by a factor of 1.5 to 5 times depending on injury severity. A fracture might justify a 2x multiplier, while permanent nerve damage could justify 4 or 5x. Insurance companies deliberately lowball initial offers because they understand most people accept quickly out of financial pressure or frustration.

Why Insurers Open with Low Numbers

The reason insurers open with insufficient numbers comes down to profit margins and predictable human behavior. According to the Insurance Information Institute, initial settlement offers from insurance companies are typically 25 to 40 percent below what claims ultimately settle for-they treat first offers as negotiating starting points, not final positions. They count on you lacking documentation, feeling overwhelmed, or needing money immediately. The companies employ trained adjusters whose job includes identifying gaps in your evidence and using those gaps to justify reduced payouts. They might delay processing claims, request unnecessary paperwork repeatedly, or claim injuries are pre-existing conditions without solid proof.

How Strong Documentation Changes the Outcome

Victims with organized medical records, clear liability evidence, and documented lost wages consistently receive settlements 50 to 70 percent higher than those negotiating alone. The gap exists because insurers adjust their offers based on case strength, not generosity. When you present a comprehensive demand backed by medical records, police reports, witness statements, and economic documentation, you signal that you’ve done the work and won’t accept a weak number. That signal alone shifts the negotiation dynamic. The next section shows you exactly how to build that documentation and create a demand package that forces insurers to take your claim seriously.

Build Your Evidence Before Negotiating

The moment you stop collecting evidence is the moment your settlement value stops growing. Insurance adjusters know that most accident victims gather information haphazardly, leaving gaps that justify lower offers. You need a systematic approach that captures everything relevant to your claim before you sit down to negotiate.

Capture the Accident Scene Thoroughly

Start at the accident scene itself. Photograph from multiple angles showing vehicle damage, road conditions, traffic signals, and any visible injuries. Get photos of the accident location from different times of day if possible, since lighting and visibility affect liability assessments. Record video if you can, capturing the full scene and any relevant street signs or landmarks. Collect names and contact information from every witness, not just those who saw the collision happen. People who arrived moments after, saw the other driver’s behavior, or noticed road hazards all matter.

Request the police report within days of the accident and verify its accuracy; errors in those reports frequently appear in settlement negotiations and need correction immediately. Insurance companies use incomplete police reports as justification for lower offers, so if critical details are missing, request an amended report or file a supplemental statement.

Document Your Medical Treatment and Injuries

Your medical documentation becomes the financial foundation of your entire settlement. Seek medical attention within 72 hours of the accident, even if you feel fine. Injuries like whiplash, soft tissue damage, and internal injuries often manifest days later, and delayed treatment records give insurers ammunition to claim injuries are unrelated to the accident.

Keep every receipt, bill, and explanation of benefits from every medical provider involved. Document your treatment timeline in detail, including dates, provider names, specific treatments received, and costs. If you need ongoing treatment, obtain a medical evaluation that projects future care costs. Many accident victims fail to include future treatment expenses in their settlements, leaving them personally responsible for years of additional medical bills.

Request written statements from your doctors about how the accident caused your injuries and what long-term effects you may experience. These statements carry weight that your personal account alone cannot match. Photograph any visible injuries at the time of the accident and document their progression through recovery. Daily photos over weeks or months create compelling visual evidence that insurance companies cannot easily dismiss.

Establish Accurate Property Damage Values

Property damage valuations require independent verification because insurance company estimates frequently undervalue repairs. Obtain repair estimates from at least two independent auto body shops, not just the insurer’s preferred vendor. Detailed estimates should break down labor costs, parts costs, and any hidden damage discovered during disassembly.

If your vehicle is totaled, research comparable vehicles sold in your region using NADA Guides or Kelley Blue Book to establish fair market value. Document any additional property damage beyond your vehicle, such as personal items inside the car, phones, glasses, or clothing that were damaged or destroyed. Many people overlook these secondary damages and leave money on the table.

If your vehicle had recent repairs, maintenance records, or upgrades that increased its value, include documentation of those investments. Your demand letter should reference specific repair estimates and market comparisons by name and date, not vague references to damage. When you present numbered repair estimates and market data, you eliminate the insurer’s ability to claim uncertainty about property damage value. This foundation of concrete evidence sets the stage for presenting a demand package that forces insurers to take your claim seriously.

Why You Need Legal Counsel in Settlement Negotiations

How Insurers Exploit Information Imbalances

Insurance companies employ trained negotiators whose sole job is minimizing payouts. When you negotiate alone, you face professionals equipped with settlement formulas, delay tactics, and psychological leverage. Adjusters know your medical prognosis after reviewing your records. They understand comparative negligence rules and how courts in Santa Cruz County typically value similar injuries. They know whether your case would survive summary judgment if filed as a lawsuit. You lack that institutional knowledge, which is why legal counsel shifts the entire negotiation dynamic.

What Legal Representation Actually Changes

A lawyer handles all communications with the insurer, preventing statements that could be used against you later. Your attorney presents a demand package formatted professionally with itemized damages, medical expert opinions, and clear liability evidence. Insurance companies treat attorney-backed demands differently than claims from unrepresented victims because they recognize the case is now trial-ready and the company faces genuine litigation risk if they refuse reasonable settlement terms. Studies show that accident victims represented by attorneys receive settlements 2 to 3 times higher than those negotiating independently, even accounting for attorney fees. The reason isn’t magic-it’s that insurers adjust their offers based on case strength and perceived litigation costs. When you have counsel, the insurer’s cost-benefit analysis changes immediately.

Recognizing When to Reject Settlement Offers

Knowing when to reject an offer requires understanding what your case is genuinely worth and what litigation would cost both sides. Many victims accept settlements before reaching maximum medical improvement, meaning they settle before understanding the full extent of their injuries and long-term treatment needs. This is a critical mistake because once you sign a release, you cannot renegotiate or reopen the claim in California. If you discover six months later that you need surgery or ongoing therapy, you’ve already waived your right to additional compensation. Your attorney should advise you to wait until your medical treatment has stabilized and your doctors have provided prognosis statements about future care.

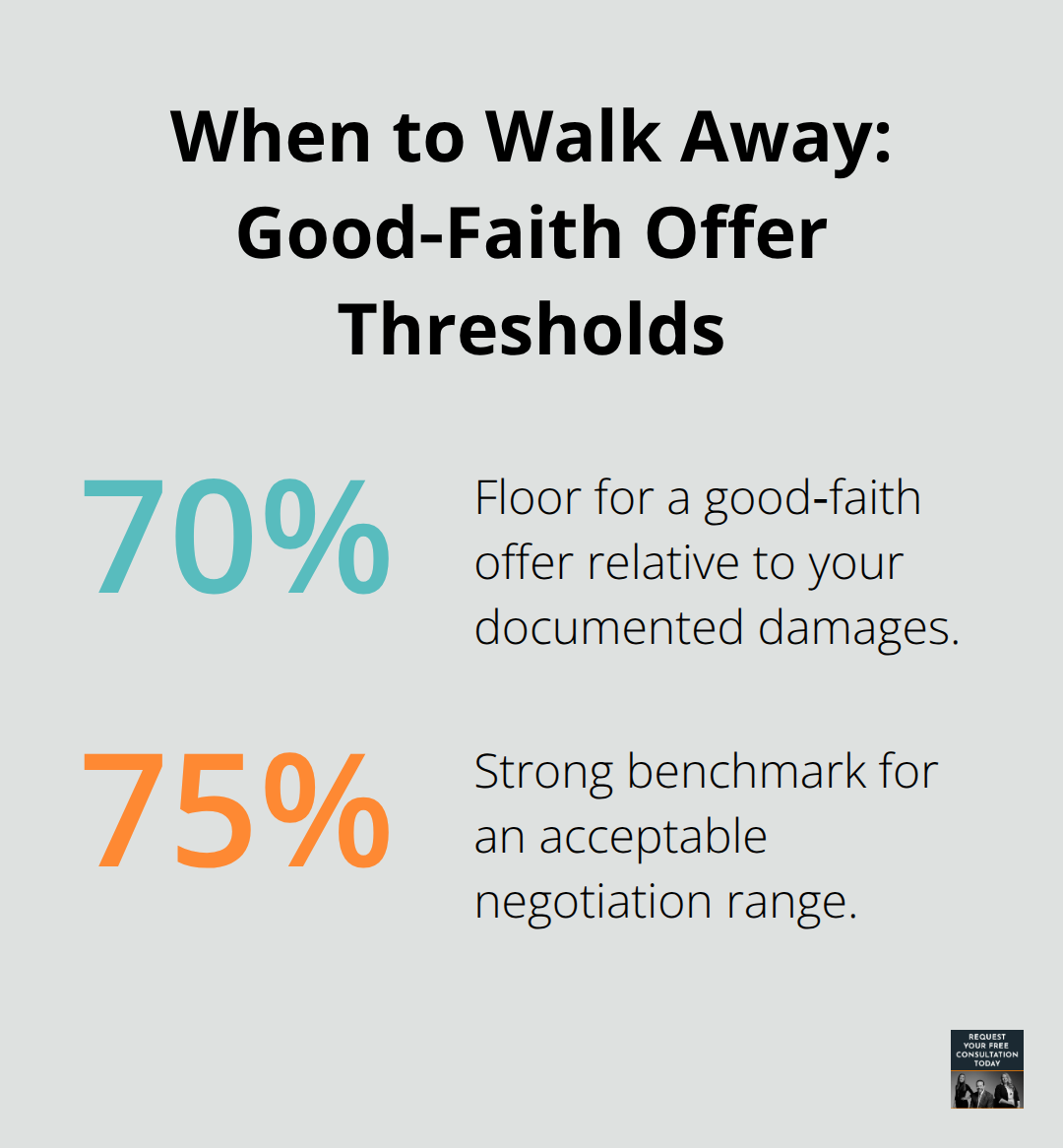

During negotiations, if an insurer’s offer consistently falls below 70 to 75 percent of your documented damages calculation, that signals they’re not negotiating in good faith. At that point, filing a lawsuit becomes the appropriate leverage. Filing suit costs the insurer money immediately through defense attorney fees and discovery expenses. It also introduces jury uncertainty-jurors in Santa Cruz County might award pain and suffering damages at a higher multiplier than the insurer’s internal formula allows.

Using Litigation as Negotiation Leverage

The threat of litigation, backed by actual case preparation, frequently breaks settlement stalemates. Your attorney should prepare every case as if trial is inevitable, conducting thorough investigations, securing medical expert reports, and identifying strong liability evidence. This trial-ready posture signals to insurers that you’re serious and willing to litigate if fair terms aren’t offered. Most cases settle before trial, but those settlements happen at much higher values when the insurer knows you’re genuinely prepared to present evidence before a judge.

The decision to file suit should never stem from frustration-it should be a calculated strategic choice based on clear settlement value analysis and realistic assessment of litigation costs versus potential recovery. At Schaar & Silva LLP, we serve Santa Cruz County with dedicated client service and in-depth legal knowledge to guide you through this critical decision point.

Final Thoughts

Winning better settlement terms requires three concrete actions: building ironclad documentation, understanding what your claim is actually worth, and recognizing when to push back against inadequate offers. Settlement negotiation tactics that work involve presenting evidence so organized and complete that insurers cannot justify low numbers without looking unreasonable. When you document medical expenses, lost wages, property damage, and pain and suffering with receipts, medical records, and expert opinions, you force the conversation away from what the insurer wants to pay and toward what the evidence supports.

Once you reach maximum medical improvement, you have the information needed to calculate your true settlement value. If an insurer’s offer falls significantly below your documented damages at that point, walking away from negotiation and filing a lawsuit becomes the right move. Most cases settle before trial, but settlements happen at substantially higher values when insurers know you’re genuinely prepared to litigate.

Before you sign any release, review the language carefully to verify the settlement covers all damages you’ve documented and that you understand whether the agreement is structured as a lump sum or periodic payments. Once you sign in California, you cannot reopen the claim, so verify every detail matches your understanding of the settlement terms. Schaar & Silva LLP handles settlement negotiations and property damage valuations so you can focus on recovery while we manage the legal complexities of your case.