A car crash turns your life upside down in seconds. Between injuries, vehicle damage, and insurance paperwork, the stress can feel overwhelming.

Filing a car crash claim doesn’t have to be complicated. We at Schaar & Silva LLP have helped hundreds of people in Santa Cruz County, Sacramento, and Oakland navigate this process and get the compensation they deserve.

What to Do Immediately After the Crash

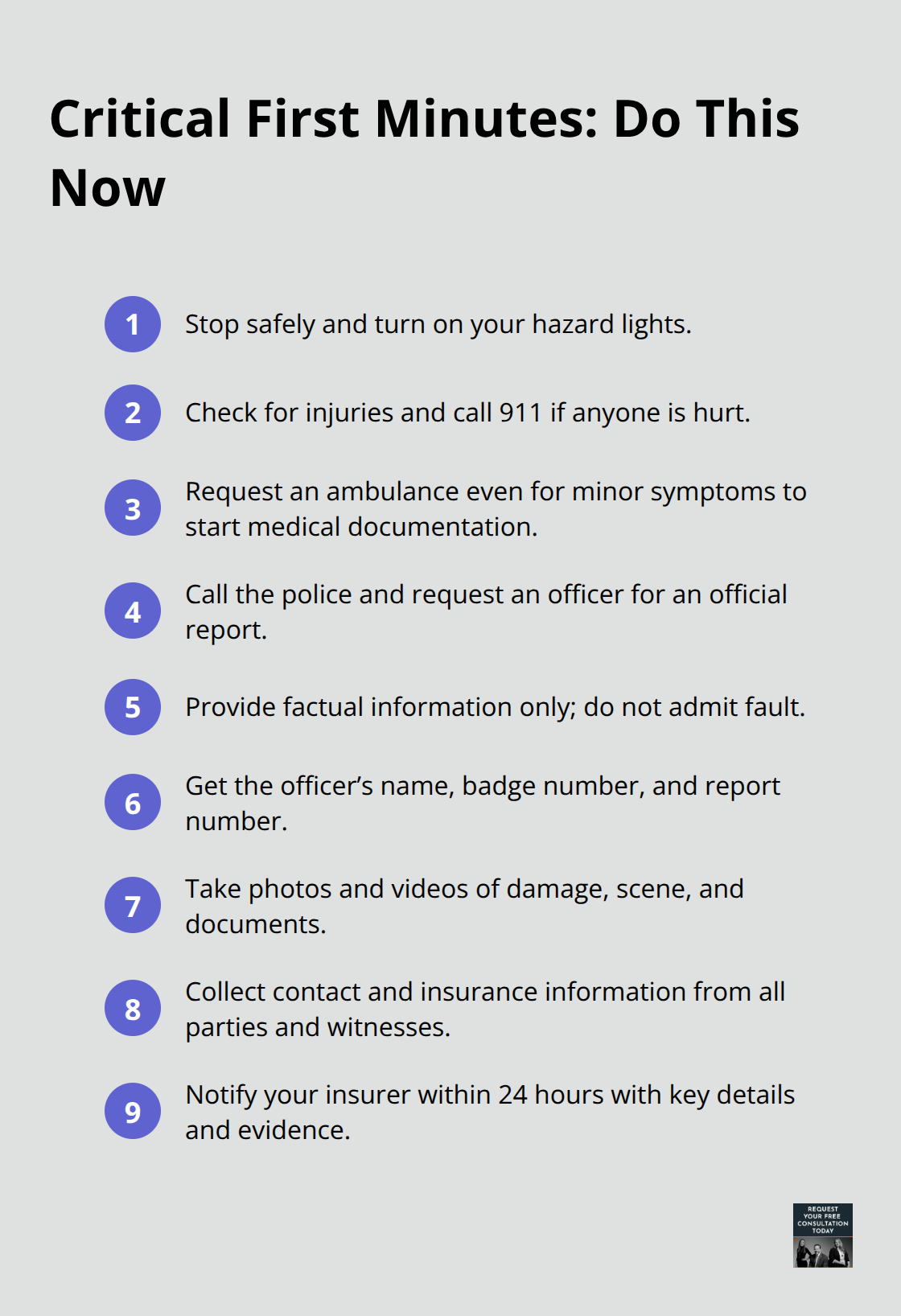

Act Fast in the Critical First Minutes

A car crash transforms your life in seconds. Your actions during the first minutes after impact directly affect your claim’s strength and your ability to recover compensation. Stop your vehicle safely and turn on hazard lights. Check for injuries immediately. If anyone is hurt, call 911 right away.

Even if injuries appear minor, request an ambulance-medical documentation started at the scene strengthens claims significantly. Call the police and request an officer to the scene. You need an official police report as your foundational document.

Provide Information Without Admitting Fault

When the officer arrives, provide factual information about what happened. Do not admit fault or speculate about how the crash occurred. Get the officer’s name, badge number, and report number before they leave. Request the report number in writing if possible. This official record becomes critical evidence for your claim.

Capture Evidence at the Scene

Take photos and videos of everything: vehicle damage from multiple angles, the accident scene including road conditions and traffic signals, debris location, and the overall area. Photograph the other driver’s license, vehicle registration, and insurance card. These images prevent disputes later about what actually happened.

Collect Contact and Insurance Information

Collect names, phone numbers, addresses, and email addresses from all drivers and passengers involved. Ask for witness contact information immediately-witnesses often disappear and become impossible to locate later. Get the other driver’s insurance company name and policy number. If they claim to lack insurance, note this carefully. Do not accept payment from the other driver at the scene or sign any documents promising payment. These actions can complicate your claim significantly.

Notify Your Insurer Within Hours

Notify your insurance company within 24 hours, though sooner is better. Provide the date, time, location, police report number, and a basic description of what happened. Share your photos and the other driver’s information. Your insurer will assign a claims adjuster who will contact you within 15 days according to California Department of Insurance timelines. This initial documentation phase determines whether your claim proceeds smoothly or encounters delays and disputes. With your evidence organized and your insurer notified, you’re ready to understand which claim option fits your situation best.

Your Claim Options Explained

First-Party vs. Third-Party Claims

You have two main paths forward after a car crash: file with your own insurance company or pursue a claim against the at-fault driver’s insurer. Your choice depends on fault determination, coverage limits, and how quickly you need compensation. If you caused the crash, your collision coverage pays for vehicle repairs regardless of fault, though you’ll pay your deductible. If the other driver caused it, you can file a first-party claim with your own insurer or a third-party claim directly against their liability coverage.

First-party claims typically resolve faster because your own insurer has financial incentive to process quickly and follows California Department of Insurance timelines: acknowledgment within 15 days, investigation start within 15 days, and claim decision within 40 days after proof of claim. Third-party claims often take longer because the at-fault driver’s insurer has less urgency and may dispute liability or damages. The California Department of Insurance enforces these timelines, so violations can be reported if your insurer misses deadlines.

Evaluating Settlement Offers

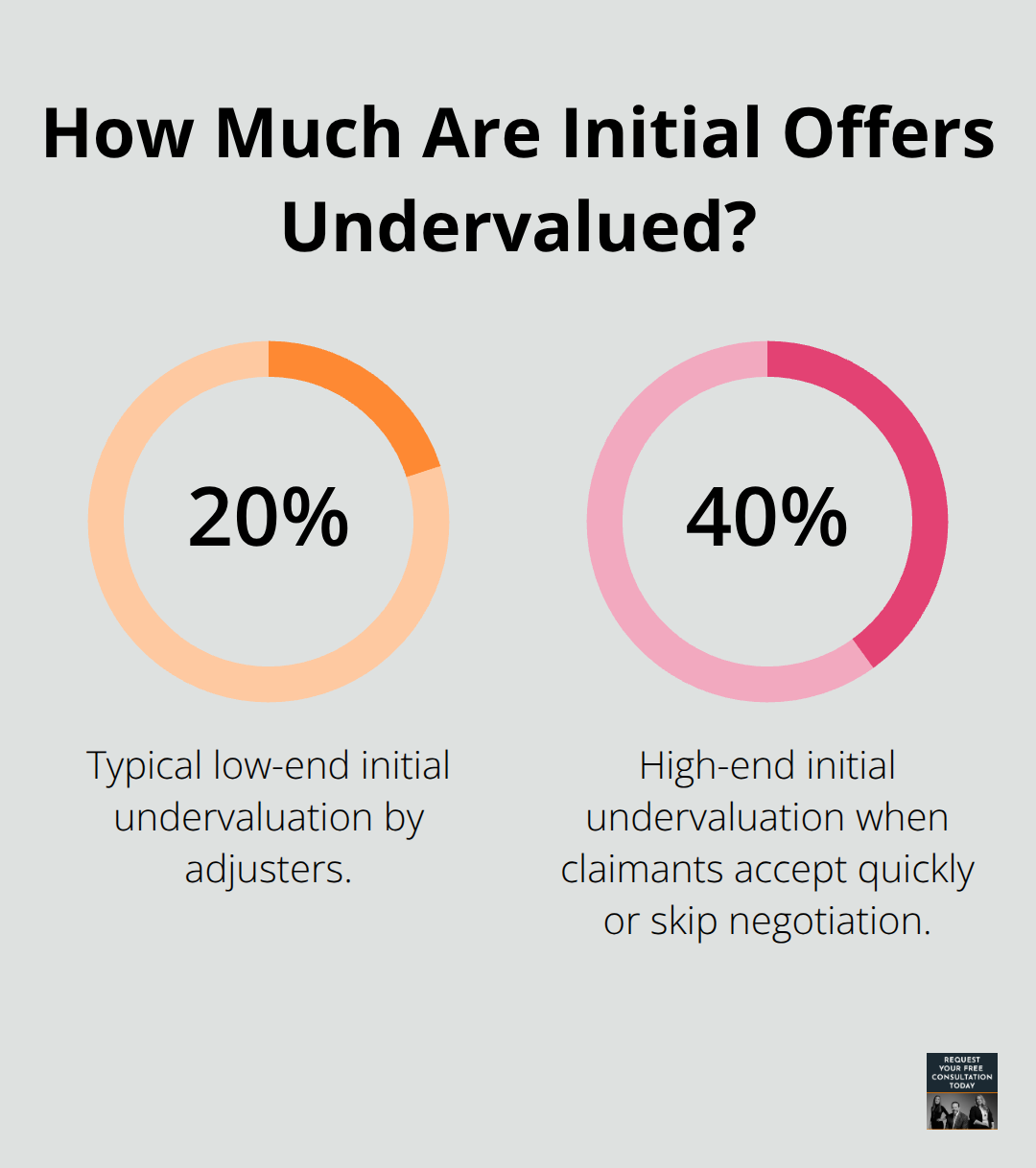

Your settlement offer rarely reflects full compensation on the first attempt. Adjusters typically undervalue claims by 20 to 40 percent initially, testing whether you’ll accept immediately without negotiation. Never accept the first offer without having your injuries fully evaluated by a medical provider.

If you’ve undergone surgery, physical therapy, or ongoing treatment, your claim’s value increases substantially but only if you have documentation.

Gather all medical bills, diagnostic reports, lost wage statements from your employer, and repair estimates before negotiating. If the offer falls short, request an itemized breakdown showing how the adjuster calculated damages, then counter with your own figures supported by documentation.

Handling Vehicle Damage Settlements

For vehicle damage, the insurer typically pays the lesser of repair costs or actual cash value. If repairs uncover additional hidden damage, they must re-inspect and adjust the settlement. This protection prevents insurers from underpaying based on incomplete initial assessments.

Using Appraisal When Negotiations Stall

If negotiations stall, the appraisal provision in your policy allows both sides to select appraisers and an umpire to determine a binding settlement amount, avoiding litigation costs. This process usually takes 30 to 60 days and costs roughly $500 to $1,500 split between parties.

When Professional Guidance Matters

Complex cases involving serious injuries, multiple vehicles, or uninsured motorist claims warrant professional guidance. Schaar & Silva LLP can evaluate whether settlement offers adequately cover your damages and future medical needs, particularly if you’re navigating claims in Santa Cruz County. Once you understand your claim options and settlement dynamics, the next critical step involves managing your medical treatment and documenting every expense to strengthen your position.

Navigating Medical Treatment and Documentation

Seek Medical Attention Immediately After the Crash

Medical attention within 24 hours of a car crash strengthens your claim significantly. Many injuries from car crashes produce no symptoms for hours or days, which is why delayed care weakens your position substantially. The California Department of Insurance expects insurers to acknowledge your claim within 15 days, but they scrutinize whether you obtained medical evaluation promptly. If you wait weeks before seeing a doctor, the adjuster will argue your injuries weren’t serious or weren’t caused by the crash.

Schedule an appointment with your primary care physician or visit an urgent care clinic within 24 hours of the accident, even if you feel fine. Request that the medical provider document the crash as the cause of your visit. This creates an official medical record linking your injuries directly to the incident. If you experience symptoms later-headaches, neck pain, back pain, or numbness-schedule follow-up appointments immediately and inform each provider about the original crash date. Insurance adjusters often undervalue claims by 20 to 40 percent when medical documentation is sparse or delayed.

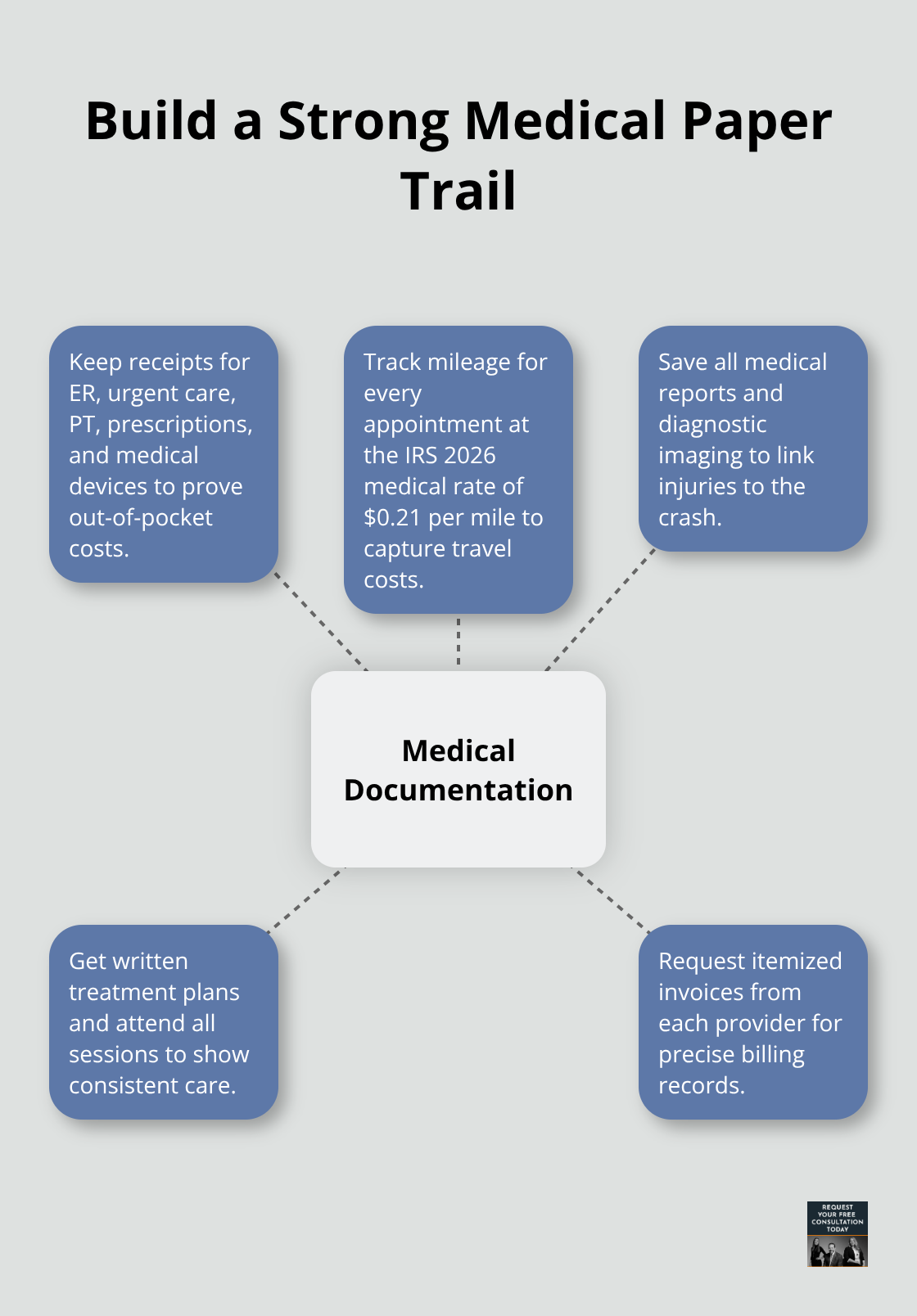

Build a Complete Medical Documentation File

Create a dedicated folder containing receipts from emergency room visits, urgent care visits, physical therapy sessions, prescription medications, and medical devices like braces or crutches. The IRS allows 21 cents per mile for medical travel in 2026, so calculate this cost if you’re traveling significant distances for treatment in Sacramento or Oakland. Track mileage to and from all appointments with precision.

Obtain copies of all medical reports, diagnostic imaging results, and provider statements about your prognosis and treatment timeline. If your doctor recommends physical therapy for 12 weeks, get written documentation of that recommendation and attend every session-missing appointments signals to adjusters that injuries aren’t serious. Request itemized invoices from each provider rather than accepting summary statements.

Present Organized Records During Settlement Negotiations

When you negotiate your settlement, present these organized records to demonstrate actual damages. Adjusters respond to concrete evidence. If you’ve incurred 40 medical appointments at $150 each, that’s $6,000 in medical costs alone before discussing lost wages or pain and suffering. Without documentation, you’re asking the adjuster to trust your word, which they won’t.

Gather all medical bills, diagnostic reports, and lost wage statements from your employer before negotiating. If the offer falls short, request an itemized breakdown showing how the adjuster calculated damages, then counter with your own figures supported by documentation. Your organized medical file becomes your strongest negotiating tool.

Final Thoughts

Filing a car crash claim requires organization, speed, and persistence. The steps you take in the first 24 hours determine whether your claim moves forward smoothly or encounters delays and disputes. Document everything at the scene, notify your insurer immediately, understand whether a first-party or third-party claim serves you best, and seek medical attention without delay. Never accept the first settlement offer, as adjusters routinely undervalue claims by 20 to 40 percent, testing whether you’ll settle quickly without negotiation.

Some situations demand legal guidance. If you’ve suffered serious injuries requiring surgery or ongoing physical therapy, if the other driver was uninsured, or if the insurer denies your claim, professional representation protects your interests. We at Schaar & Silva LLP help people throughout Santa Cruz County, Sacramento, and Oakland navigate complex claims and negotiate fair settlements.

Your recovery matters more than speed. Take time to heal fully before settling, continue all recommended medical treatment, and maintain detailed records throughout the process. The filing car crash claim process tests your patience, but organized preparation and professional guidance when needed ensure you receive compensation that reflects your actual damages and future medical needs.