A vehicle accident can turn your life upside down in seconds. Medical bills pile up, your car needs repairs, and insurance companies seem determined to pay you as little as possible.

We at Schaar & Silva LLP know how overwhelming vehicle accident claims can be. This guide walks you through your rights, the claims process, and how to protect yourself when obstacles arise.

What to Do Right After Your Accident

Immediate Actions at the Scene

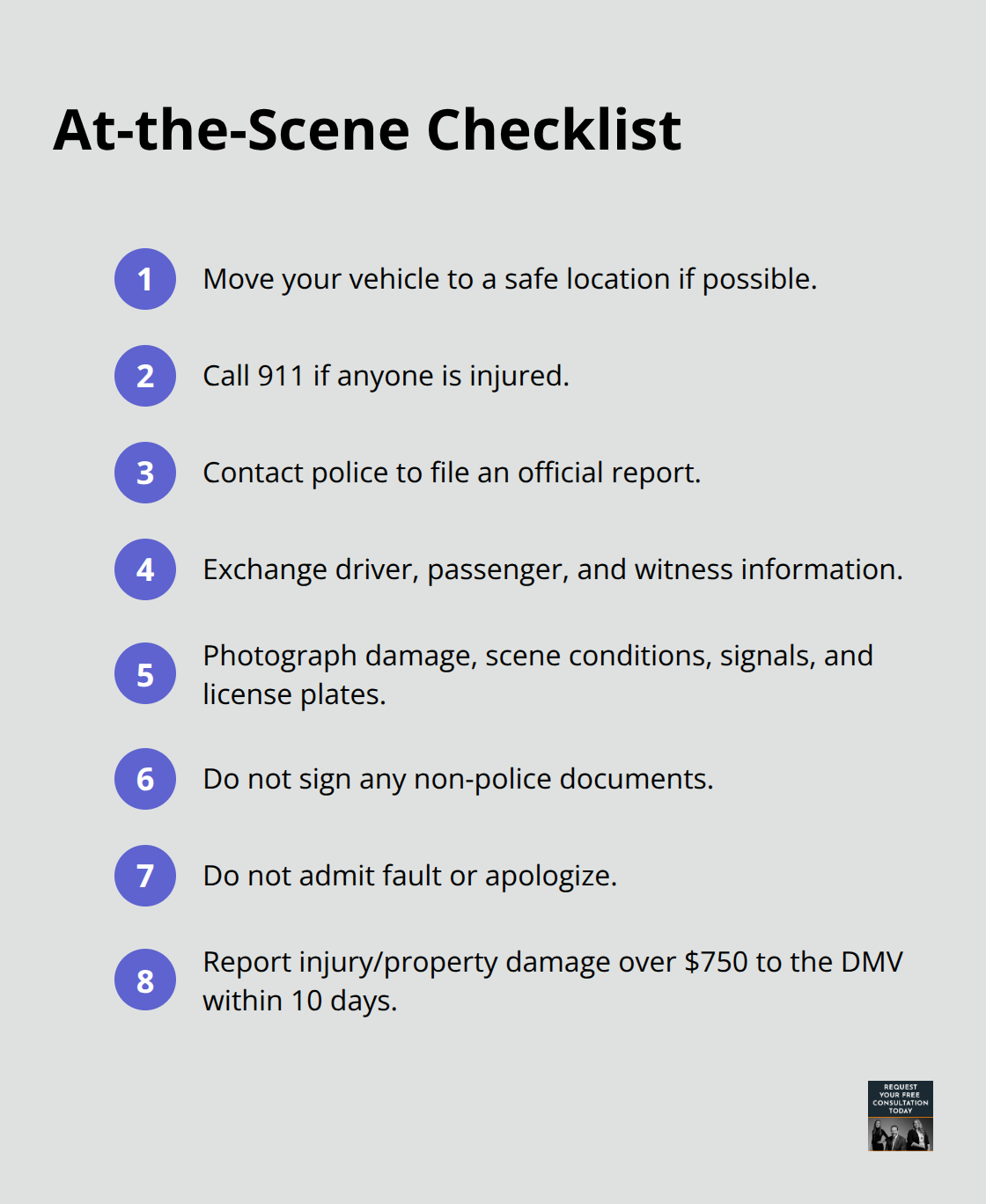

The first minutes after a vehicle accident determine how strong your claim becomes. Stop your vehicle safely, call 911 if anyone is injured, and contact police to file an official report. California law requires you to report accidents involving injuries or property damage exceeding $750 to the Department of Motor Vehicles within 10 days.

At the scene, collect the other driver’s name, phone number, address, driver’s license number, license plate, vehicle identification number, and insurance information. Get the same details from all passengers and independent witnesses. Take photographs of vehicle damage from multiple angles, the accident scene, road conditions, traffic signals, and license plates. Do not sign any documents except for police officers, and never admit fault or apologize for the accident.

What Not to Say or Do

Many accident victims make the mistake of saying things like “I’m sorry” or “I didn’t see you coming,” which insurers later use against them. Avoid discussing the accident with the other driver’s insurance company without legal representation. The at-fault driver’s insurer is not on your side and will ask many questions to minimize payout. Signing fault statements or releases promising to pay another party’s damages can jeopardize your deductible or recovery.

Understanding California’s Fault-Based System

California operates under a fault-based insurance system, meaning the driver responsible for the accident pays for damages through their insurance. This system protects you because the at-fault driver’s insurer must cover your medical expenses, vehicle repairs, lost wages, and pain and suffering. However, insurance companies routinely undervalue claims by offering settlements before your injuries fully develop or by claiming pre-existing conditions caused your injuries.

Building Your Documentation

Document everything from day one: save all medical records, prescription receipts, repair estimates, photos of damage, and communication with insurance adjusters. Insurance adjusters will inspect vehicle damage and prepare initial repair estimates, but additional damage discovered later may require further inspection. If you disagree with a settlement amount, California law allows you to request an appraisal where each side selects an appraiser. If the appraisers cannot agree, an umpire’s decision becomes binding.

Settlement Ranges for Common Injuries

Whiplash injuries typically settle between $5,000 and $20,000, while knee or shoulder injuries range from $30,000 to $100,000. Herniated discs commonly settle between $50,000 and $100,000 or more. These figures vary based on your specific medical treatment, lost wages, and the defendant’s insurance limits. Understanding these ranges helps you evaluate whether an initial settlement offer reflects the true value of your claim, which brings us to the critical step of notifying your insurance company and beginning formal negotiations.

How Insurance Claims Move From Filing to Payment

Notify Your Insurer and Understand the Timeline

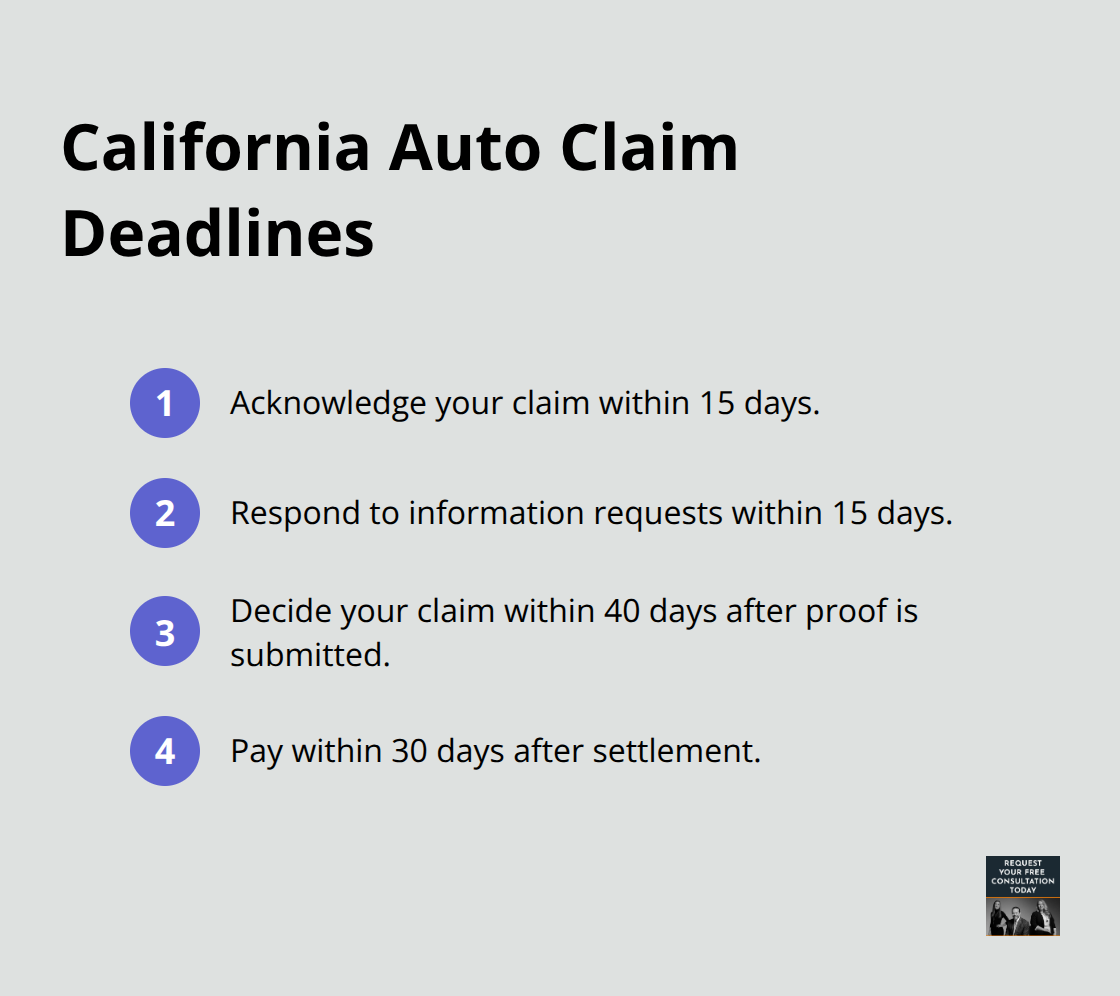

Contact your insurance company within 24 hours of an accident to set the claims process in motion. California’s Fair Claims Settlement Practices Regulations establish strict deadlines: insurers must acknowledge your claim within 15 days, respond to requests within 15 days, decide on your claim within 40 days after you submit proof, and pay within 30 days after settlement. Call your agent or company immediately and provide basic accident details, but avoid giving a recorded statement without careful consideration of your answers first.

The insurer will assign an adjuster who inspects vehicle damage and prepares an initial repair estimate. Additional damage often surfaces during repairs, requiring further inspection and updated estimates.

Control Your Repair Shop and Parts Selection

You control which repair shop handles the work, and California Insurance Code Section 758.5 protects this right. If you choose your own shop instead of accepting the insurer’s recommendation, the insurer must pay reasonable costs according to applicable trade standards. Repair invoices must clearly identify whether parts are original equipment manufacturer (OEM), aftermarket, rebuilt, or reconditioned. Aftermarket parts must match the original in kind, quality, safety, fit, and performance to meet legal standards.

Gather Medical Records and Document All Costs

Request medical records from every healthcare provider you see immediately after treatment, including emergency rooms, urgent care clinics, physical therapists, and specialists. Insurance companies often pressure accident victims to settle quickly for only documented expenses before injuries fully develop, which leaves you uncompensated for future treatment and ongoing pain. Collect receipts for prescriptions, medical equipment, transportation to appointments, and any other accident-related costs. Document lost wages with pay stubs, tax returns, and employer statements showing income lost due to medical appointments or inability to work.

Evaluate Settlement Offers and Use Appraisal Rights

When settlement negotiations begin, insurers frequently offer initial amounts well below what your case warrants. Your documented medical records, wage loss statements, and photos of vehicle damage provide leverage to counter low offers. Settlement ranges depend heavily on injury severity and lost wages-whiplash cases typically settle between $5,000 and $20,000, while herniated disc injuries commonly settle between $50,000 and $100,000 or higher. If you disagree with the settlement amount, request an appraisal where each side selects an appraiser to evaluate damages. If those appraisers cannot agree, an umpire’s decision becomes binding. Understanding whether an offer reflects the true value of your claim requires careful analysis of your specific injuries, medical treatment, and lost income-a task that becomes significantly more complex when multiple parties or coverage limits enter the picture.

What Stops You From Getting Fair Compensation

Insurance companies deny and underpay claims far more often than accident victims realize. The California Department of Insurance received over 10,000 complaints about claim handling in 2024, with underpayment and unreasonable denials ranking among the top issues.

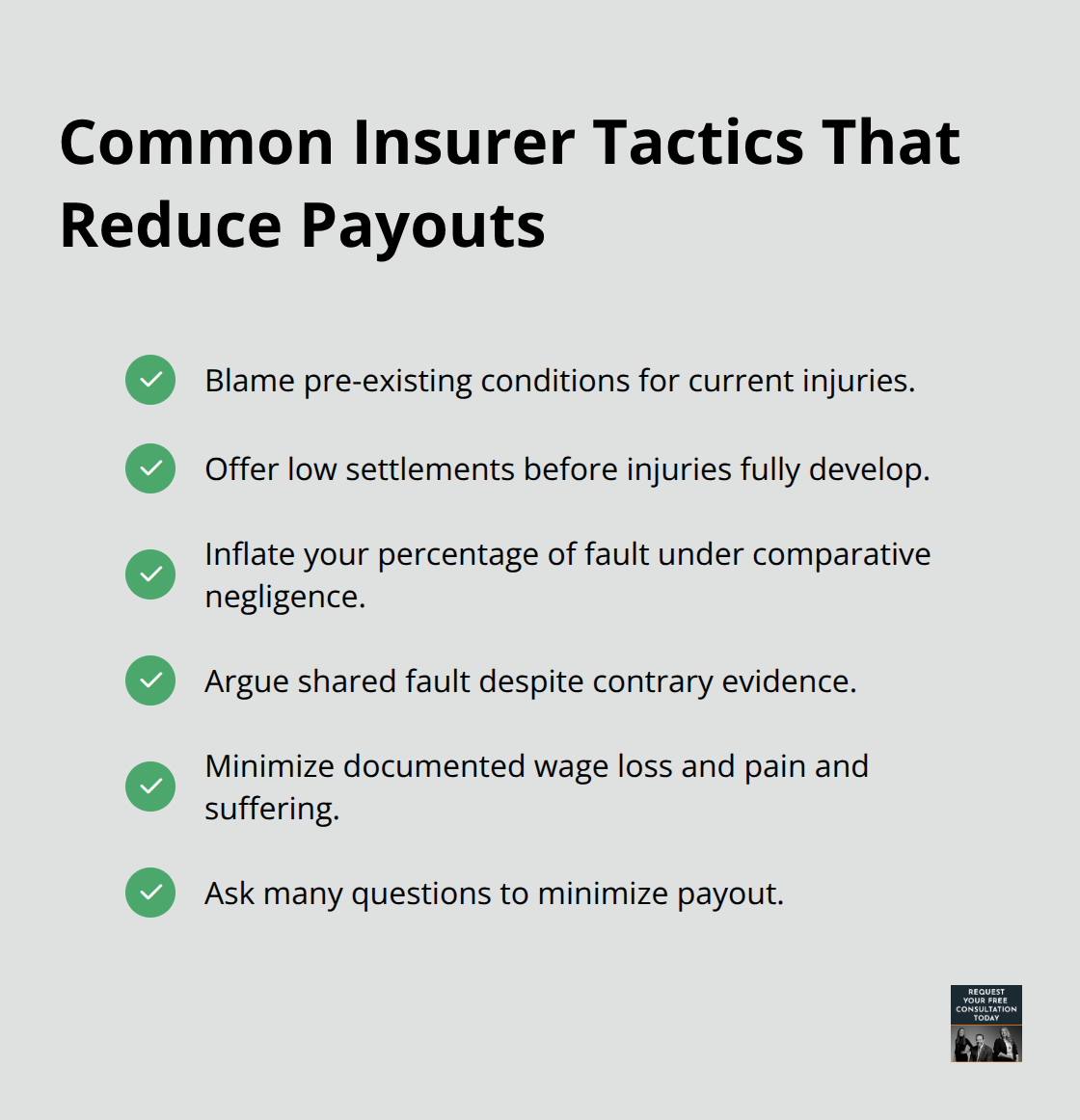

Insurers use several tactics to reduce payouts: they claim pre-existing conditions caused your injuries, argue you share fault even when evidence shows otherwise, or simply offer settlements before your medical picture becomes clear.

Pre-Existing Conditions and Injury Development

If an adjuster tells you your claim is denied because of a pre-existing condition, request the specific medical records supporting that claim and have your treating physician document how the accident worsened your condition. Many injuries take weeks or months to fully develop, so accepting a quick settlement offer leaves future treatment costs entirely on you. Your physician’s statement that the accident aggravated or accelerated a pre-existing condition can overcome this denial tactic and restore your claim’s value.

Liability Disputes and Fault Assignment

Liability disputes create another major obstacle, especially in cases involving multiple vehicles, unclear traffic signals, or witness disagreements. California’s comparative negligence rule allows you to recover damages even if you are partially at fault, but insurers weaponize this by inflating your percentage of fault to minimize their payout. When an insurer claims you were 40% at fault in a collision you believe was entirely the other driver’s fault, that claim directly reduces your recovery by 40%.

Document everything that proves liability: traffic camera footage, police reports with officer conclusions, witness statements recorded immediately after the accident, and expert reconstruction reports if the accident was serious. These materials shift the negotiation in your favor and make it harder for insurers to inflate your fault percentage without evidence.

Multiple Parties and Coverage Limits

Multiple parties and coverage limits create the most complex obstacles. If a commercial truck hit you, that truck driver’s employer carries separate insurance, and California law may allow claims against both the driver and the company. Your own uninsured or underinsured motorist coverage applies if the at-fault driver lacks sufficient insurance, but you must understand your specific policy limits.

A serious spinal cord injury that warrants $800,000 in compensation becomes catastrophic if the at-fault driver carries only $15,000 in liability coverage. Identifying all available insurance sources-including the at-fault driver’s policy, your own underinsured motorist coverage, and any commercial policies involved-determines whether you recover full compensation or face a significant shortfall. When you face these layered obstacles, the legal team at Schaar & Silva LLP can help identify all available insurance sources and pursue maximum recovery from each one.

Final Thoughts

Vehicle accident claims demand more than paperwork and hope. You now understand the immediate steps at the scene, how to document evidence, what obstacles insurers throw in your path, and why settlement ranges vary based on injury severity and lost wages. Hiring an attorney becomes essential when your injuries are moderate to severe, when liability is disputed, or when multiple parties and coverage limits complicate recovery.

Insurance companies have teams of adjusters and lawyers working to minimize payouts, so you deserve someone equally equipped to fight for your interests. An attorney identifies all available insurance sources, challenges low settlement offers with medical and economic evidence, and pursues maximum recovery from each responsible party. Most vehicle accident claims settle during negotiations after discovery, when both sides have reviewed medical records, wage documentation, and liability evidence.

The legal team at Schaar & Silva LLP guides you through each stage of your claim, from initial filing through final settlement or trial. We assist with property damage evaluation, connect you with medical lien services to manage bills during your case, and provide access to emotional support specialists.