A car accident in Santa Cruz County leaves you with damaged property and mounting questions about what comes next. Insurance companies often undervalue property damage claims, leaving you short of what you actually need to repair or replace your vehicle.

We at Schaar & Silva LLP have helped countless accident victims navigate property claims in Santa Cruz and recover fair settlements. This guide walks you through how claims work, what affects your payout, and concrete steps to fight for the compensation you deserve.

How Property Damage Claims Work in Santa Cruz County

The Claims Timeline and Initial Response

When you file a property damage claim in Santa Cruz County, the process moves faster than you might expect. Most insurers respond to initial claims within 10 to 15 business days. The adjuster assigned to your case will request photos, police reports, and repair estimates before making an offer. This timeline matters because California law gives you three years from the date of damage to file a lawsuit, but waiting too long weakens your negotiating position. Insurance companies know that accident victims often accept lowball offers when they’re stressed and need their vehicle fixed immediately.

How Insurers Value Your Vehicle and Damage

The adjuster’s job is to minimize payouts, not to help you. They examine your vehicle’s age, maintenance history, and current market value. A 2015 sedan with 120,000 miles receives a different valuation than the same model year with 60,000 miles, even if both sustained identical damage. Insurers also factor in whether your repairs will return the vehicle to pre-accident condition or merely make it roadworthy. This distinction can mean thousands of dollars in difference.

Documentation That Strengthens Your Claim

Many claims get underpaid because claimants submit incomplete documentation. A single repair estimate is rarely enough-insurance adjusters expect at least two independent estimates to verify costs, and you should obtain three if the damage is substantial. Photos matter tremendously. Take images from multiple angles, including close-ups of specific damage areas and wide shots showing the overall context. If a fallen tree damaged your vehicle, photograph the tree, the surrounding area, and any debris. Police reports carry significant weight; if no report was filed at the accident scene, contact the Santa Cruz Sheriff’s Office or local police department to file one afterward.

Repair invoices from previous maintenance work help establish that you maintained your vehicle properly, which can support your claim value. Missing documentation is the single biggest reason claims get underpaid or denied entirely.

Why Claims Get Denied or Underpaid

Insurers often deny claims by claiming pre-existing damage, lack of proof of ownership, or insufficient evidence of causation. They’ll argue that a repair estimate is inflated or that you’re claiming damages unrelated to the accident. Some insurers delay decisions hoping you’ll accept a lower settlement out of frustration. If your claim gets denied, you have options. You can file a complaint with the California Department of Insurance, which investigates insurer misconduct and bad faith practices. You can also pursue legal action if the insurer’s valuation falls significantly short of documented repair costs. The decision depends on repair costs, your deductible, and the strength of your documentation. If repairs exceed $5,000 and your insurer’s offer is $2,000 short, legal action may recover that difference plus attorney fees. If the gap is $500, it probably isn’t worth pursuing in court.

Understanding how insurers evaluate your claim and what documentation they require puts you in a stronger position to negotiate. The next section covers the specific factors that directly influence your settlement amount and how to leverage them in your favor.

What Determines Your Settlement Amount

Vehicle Age and Condition Shape Your Baseline Value

Your vehicle’s age and condition form the foundation of how insurers calculate your settlement. A 2020 Honda Civic with 40,000 miles receives a higher valuation than a 2015 model with 120,000 miles, even if both sustained identical collision damage. Insurers use resources like the National Automobile Dealers Association guide to establish baseline values, then adjust downward based on mileage, accident history, and mechanical condition.

Your maintenance records counter the insurer’s argument that your vehicle depreciated faster than market standards suggest. Document regular oil changes, brake service, and transmission fluid replacements to prove you maintained your vehicle properly. Conversely, if your vehicle required significant repairs before the accident, the insurer will use that against you to justify a lower payout.

Repair Costs Don’t Equal Your Settlement

The repair costs themselves directly impact settlement amounts, but not in the way most people think. Insurers don’t simply add up repair estimates and pay that figure. They compare your estimates against industry repair databases and regional labor rates. A transmission replacement that costs $4,200 at a Santa Cruz dealership might be valued at $3,800 by an adjuster using national averages.

Obtaining multiple estimates from independent shops becomes essential. If you submit only one estimate from a dealership, the insurer will assume it’s inflated and reduce their offer accordingly. Three estimates from reputable independent shops, a dealership, and a specialty repair facility create a compelling case that your quoted price reflects genuine market rates in Santa Cruz County.

Documentation Quality Separates Full Value from Reduced Payouts

Documentation quality separates claims that receive full value from those that get substantially reduced. Police reports carry weight because they establish causation and provide official incident details. Photographs taken immediately after the accident are far more credible than photos taken days later, since time allows for additional deterioration or secondary damage.

Take close-up images of damaged areas, wide shots showing vehicle positioning, and photos of the accident scene itself. If a third party caused the damage, photograph their vehicle, their license plate, and the scene to establish liability clearly. Repair estimates should itemize specific parts and labor hours rather than provide vague totals. An estimate that lists worn brake pads, damaged suspension components, and frame straightening with corresponding costs looks far more legitimate than a round number estimate.

Supporting Evidence Strengthens Your Position

Keep all receipts from previous maintenance work, as these demonstrate you maintained your vehicle properly and support your claim that the damage resulted solely from the accident rather than pre-existing mechanical issues. Gather evidence to prove your case: police reports, photographs, repair estimates, receipts, and witness statements all work together to build a strong foundation.

When repair costs exceed $5,000 and your insurer’s offer falls significantly short of documented repair costs, you may need to pursue legal action. The decision depends on the gap between the insurer’s valuation and your documented repair costs, your deductible, and the strength of your documentation. If the difference is substantial, legal action may recover that gap plus attorney fees. Understanding how to present your evidence effectively positions you to negotiate from strength rather than accept an inadequate offer.

How to Maximize Your Settlement Without Leaving Money on the Table

Obtain Multiple Independent Repair Estimates

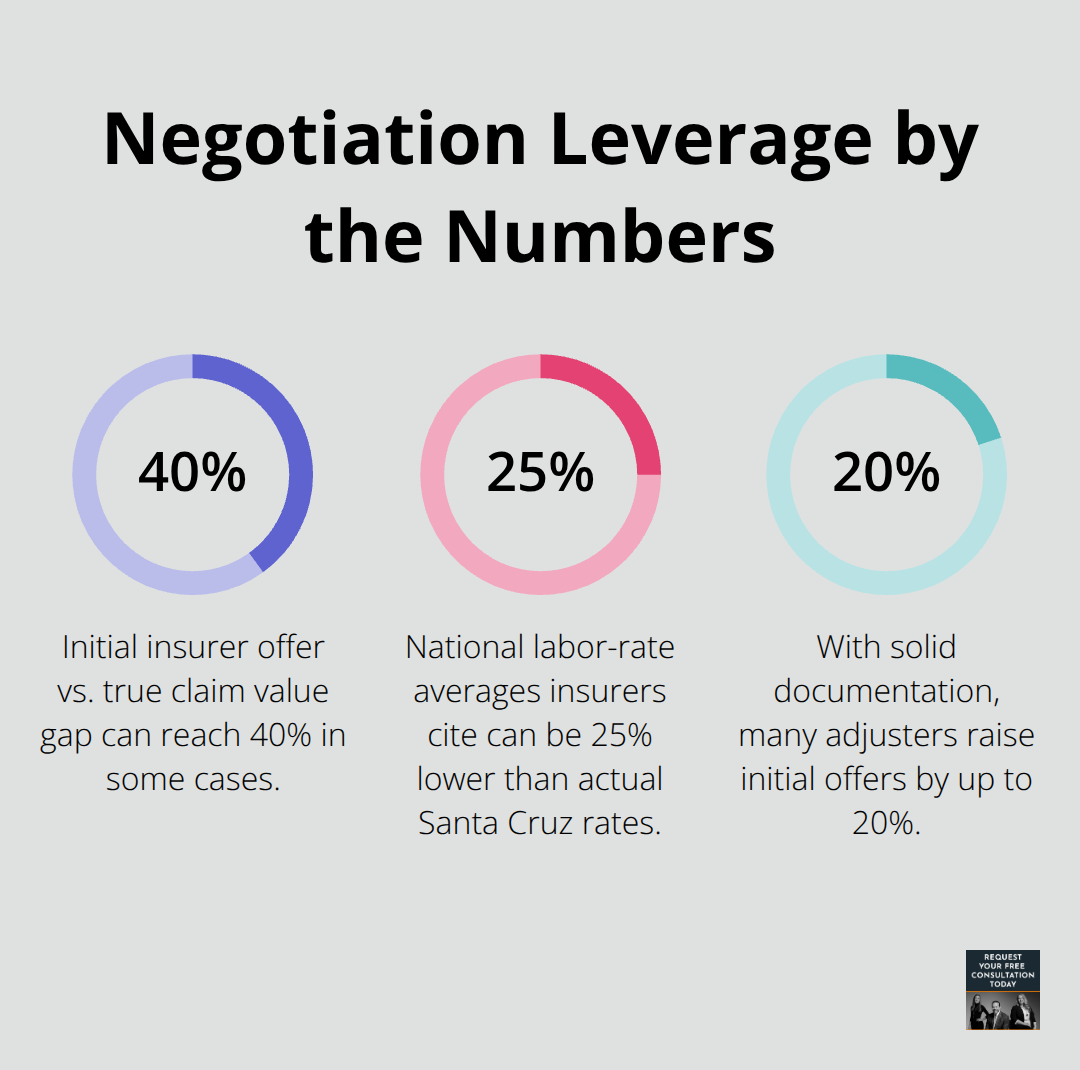

The gap between what insurers initially offer and what your claim is actually worth often reaches 30 to 40 percent. Three independent repair estimates from unaffiliated shops create a pattern that’s difficult for adjusters to dismiss. One estimate gets written off as inflated, two estimates can be dismissed as anomalies, but three credible estimates from different facilities force adjusters to take your documentation seriously.

When you request estimates, ask the shop to itemize every component separately rather than provide a lump sum. A detailed breakdown showing frame straightening at $1,200, suspension replacement at $800, and paint and materials at $600 carries far more weight than an estimate stating total damage at $2,600. Call each shop and ask about their hourly labor rates in Santa Cruz County. National averages that insurers use often run 15 to 25 percent lower than actual Santa Cruz rates, and you can use this gap to push back against lowball valuations.

Document Everything in Writing

Photographs taken immediately after the accident matter far more than photos taken days later, so capture multiple angles, close-ups of damage, and wide shots showing the accident scene and vehicle positioning. Include photos of your maintenance records and any service receipts proving you maintained your vehicle properly before the accident.

Document everything in writing, including email confirmations of estimates, shop certifications, and the estimator’s experience level. Written records create accountability and can be referenced later if you pursue legal action. Keep all communication with adjusters in writing through email rather than phone calls, since written documentation strengthens your position considerably.

Negotiate with Adjusters Using Data

Adjusters operate within constraints set by their employer. An adjuster who consistently approves high payouts faces scrutiny from management, so their incentive is to minimize what they approve. When the adjuster contacts you with an offer, never accept it immediately. Instead, ask for a written explanation of how they calculated the vehicle’s pre-accident value and how they arrived at their damage estimate.

If their offer falls short of your three independent estimates, respond in writing with a detailed comparison showing the differences between their valuation and market rates in Santa Cruz County. State specific numbers: if they valued repairs at $3,500 but your three estimates average $4,200, highlight that $700 gap and cite the regional labor rate difference. Insurance adjusters respond to pressure backed by documentation far more readily than they respond to frustration or anger. Most adjusters will increase their initial offer by 10 to 20 percent when presented with solid documentation and a reasoned written response, which means your effort to gather proper estimates and documentation directly translates to additional money in your pocket.

Pursue Legal Action When the Gap Justifies It

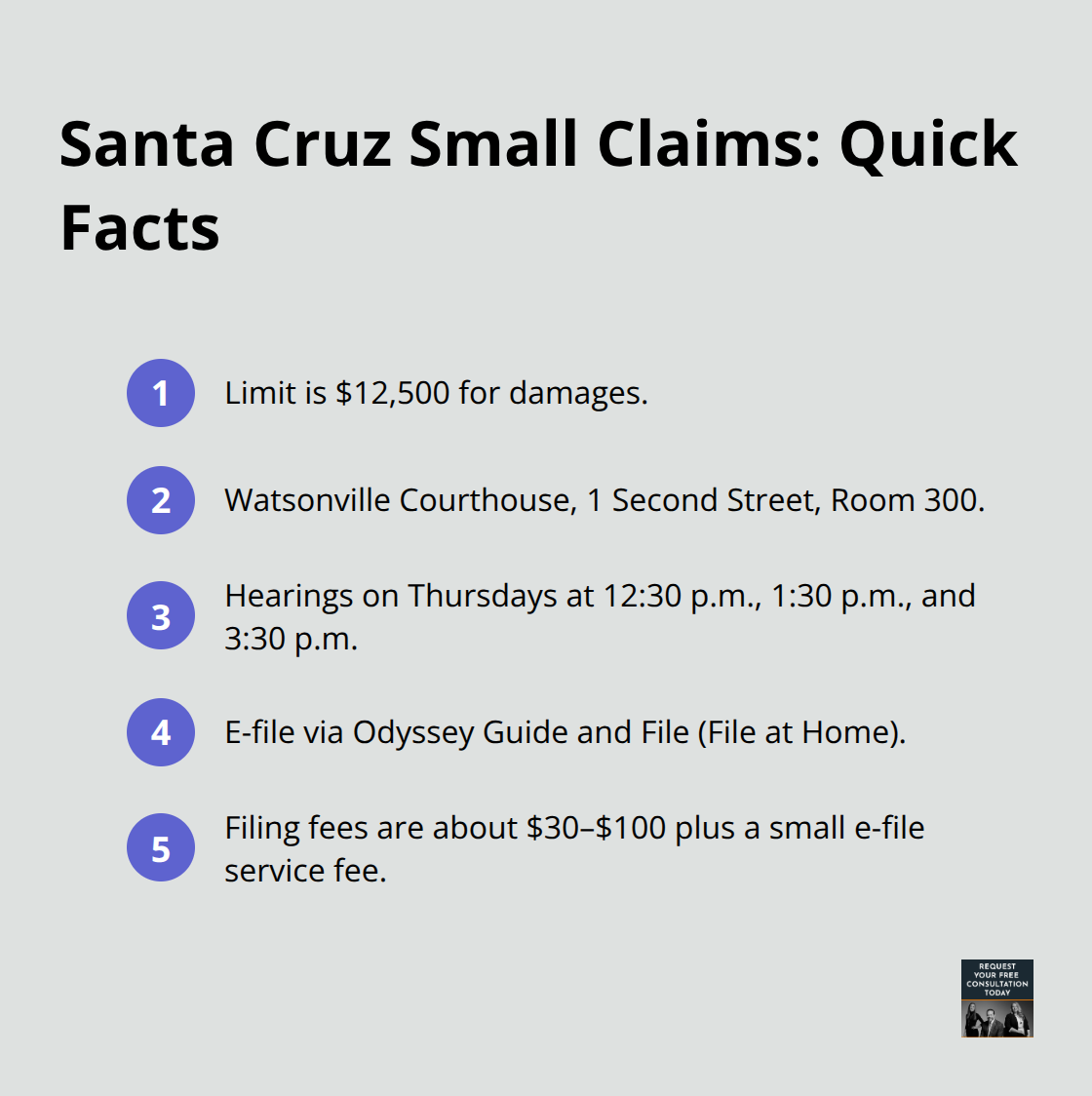

Legal action becomes the appropriate path when the insurer’s valuation falls substantially short of documented repair costs and the gap exceeds your deductible by a meaningful margin. If repairs genuinely cost $5,000, your deductible is $500, and the insurer offers $3,200, that $1,300 gap justifies pursuing a claim in Santa Cruz County Small Claims Court if the total damages remain under $12,500.

Small Claims Court in Santa Cruz handles damages of $12,500 or less and does not allow attorneys, making the process straightforward and fast. All Santa Cruz County Small Claims filings and hearings take place at the Watsonville Courthouse at 1 Second Street, Room 300, with hearings scheduled on Thursdays at 12:30 p.m., 1:30 p.m., and 3:30 p.m. You can file electronically through File at Home via the Odyssey Guide and File system, which lets you prepare forms online and submit them directly to the court.

Filing fees run approximately $30 to $100 depending on your claim amount, plus a small e-file service fee if you submit electronically.

Evaluate Larger Claims with Professional Guidance

For larger claims exceeding $12,500 or situations involving complex liability questions, we at Schaar & Silva LLP can evaluate whether pursuing a full civil lawsuit makes financial sense. The decision hinges on the size of the gap between what you’re owed and what the insurer offers, the strength of your documentation, and whether additional damages like rental car costs or diminished vehicle value strengthen your position beyond just repair costs.

Final Thoughts

Property claims in Santa Cruz require persistence, documentation, and a clear understanding of what your settlement should cover. The gap between an insurer’s initial offer and fair compensation often reaches thousands of dollars, but only if you take concrete steps to support your position. Three independent repair estimates, thorough damage photographs, a police report, and written communication with adjusters transform your claim from passive acceptance into active negotiation backed by evidence.

Your documentation directly determines your payout, since adjusters reviewing itemized repair estimates, maintenance records, and detailed photographs make different decisions than those reviewing a single estimate and casual photos. If your insurer’s offer falls significantly short of documented repair costs, Small Claims Court in Santa Cruz County provides a straightforward path to recover what you deserve (claims under $12,500 move quickly through the Watsonville Courthouse with Thursday hearings and electronic filing options). The filing fees remain modest, and you avoid the complexity of larger civil litigation.

For property claims Santa Cruz residents face that exceed $12,500 or involve complicated liability questions, we at Schaar & Silva LLP can evaluate your situation and guide you toward the best resolution. Contact us to discuss whether your claim warrants professional representation or if Small Claims Court represents the faster, more cost-effective path forward.