Getting into a car accident can leave you wondering about your insurance options and future rates. Many drivers in Santa Cruz County face the challenge of finding affordable coverage after an incident.

We at Schaar & Silva LLP understand that securing car insurance quotes for drivers with accidents requires careful planning and the right information. This guide walks you through the process step by step.

How Do You Get Insurance Quotes After Your Accident

Start With Your Current Insurance Provider

Call your current insurance company within 24 hours of the accident, even if you plan to switch providers. This conversation provides baseline information about rate increases and helps you understand your current coverage limits. Insurance companies in California must respond to claims within 15 days according to state regulations. Ask your current provider about accident forgiveness programs, which can prevent rate increases for first-time accidents. Companies like Allstate and Progressive offer these programs, but you typically need a clean driving record of three to five years to qualify.

Collect All Documentation Before You Shop

Gather your police report number, accident photos, and damage estimates before you request quotes. Insurance companies need specific details about the incident date, location, and circumstances to provide accurate rates. Collect your current policy documents that show coverage limits and deductibles. The Insurance Information Institute reports that at-fault drivers see rate increases of up to 45%, so complete documentation helps insurers assess your risk accurately. Keep records of all repair estimates and medical bills, as claim amounts directly influence your future premiums.

Compare Multiple Providers Systematically

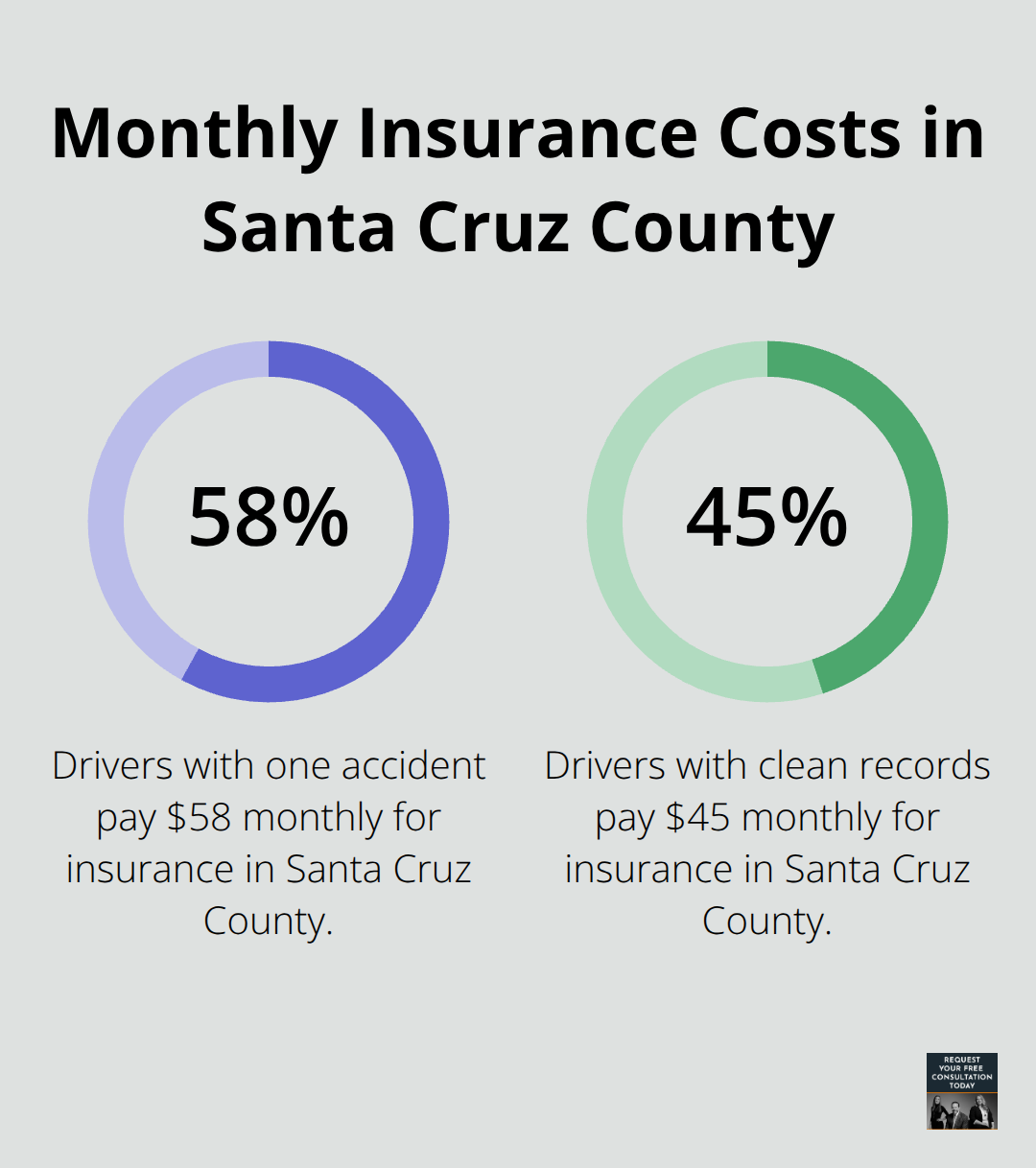

Request quotes from at least five different insurance companies through online tools like Compare.com or direct company websites. Provide identical information to each insurer to get comparable rates. Focus on companies that offer accident forgiveness or safe driver discounts that can offset premium increases. In Santa Cruz County, drivers with one accident pay around $58 monthly compared to $45 for clean records (local insurance data). Shop within 30 days of your accident for the most current rates, as some insurers offer better deals for immediate coverage switches after incidents.

Understanding how accidents affect your rates helps you make informed decisions about coverage options and policy features that matter most to your situation.

What Drives Your Rate Increases After an Accident

Insurance companies use three primary factors to calculate your new premiums after an accident, and this knowledge can save you hundreds of dollars annually. Fault determination carries the heaviest weight in rate calculations. The Insurance Information Institute shows that at-fault drivers face premium increases of up to 45%, while no-fault accidents typically result in minimal or no rate changes. California follows a comparative negligence system, which means your rate increase depends on your percentage of fault. If you share 30% responsibility for the accident, your rate increase will be proportionally lower than someone deemed 100% at fault.

Your Past Record Determines Future Costs

Insurance companies examine your complete history when they set post-accident rates. Drivers with clean records before an accident receive more favorable treatment from insurers. A single previous claim can double your rate increase after a new accident. The National Association of Insurance Commissioners data reveals that multiple claims within three years can result in policy cancellation or non-renewal. Santa Cruz County drivers with one prior accident pay approximately $88 monthly compared to $58 for first-time accident drivers. Your claims frequency matters more than individual claim amounts to most insurers.

Accident Severity Shapes Premium Calculations

The type and cost of your accident directly influence rate adjustments. Minor fender-benders with damages under $1,000 typically increase rates by 10-20%, while major accidents that involve injuries or significant property damage can raise premiums by 40% or more. Accidents that require emergency response or result in citations carry heavier penalties. Insurance companies maintain detailed databases that track accident types and their associated risk levels. Multi-vehicle accidents and highway incidents receive higher risk ratings than parking lot mishaps. The duration of rate increases also varies (minor incidents affect rates for three years while major accidents can impact premiums for five years).

When you request quotes from different providers, you’ll need specific information about your accident and current coverage to get accurate rates.

What Information You Need for Accurate Quotes

Insurance companies require specific documentation to calculate accurate post-accident rates. Missing information can delay quotes by weeks or result in higher premiums than necessary. Start with your police report number and incident details that include the exact date, time, and location of the accident. Insurance underwriters use police report data to verify fault determination and assess risk factors. California Department of Motor Vehicles requires accident reports within 10 days for damages that exceed $750, and this same report becomes the foundation for your insurance quotes. Document all parties involved with their insurance information, driver’s license numbers, and vehicle details. Take photos of all vehicle damage, the accident scene, and any relevant road conditions or traffic signs.

Police Report and Accident Details

Obtain your official police report number within 48 hours of the incident. This document contains the officer’s assessment of fault, witness statements, and traffic violations issued at the scene. Insurance companies cross-reference your account with police findings to verify accuracy. Include detailed descriptions of weather conditions, road hazards, and traffic patterns that contributed to the accident. The Insurance Information Institute notes that approximately 30% of drivers lack insurance coverage, so police reports help verify all parties’ insurance status. Collect contact information for witnesses who can support your version of events if disputes arise during the claims process.

Current Coverage Limits and Deductibles

Gather your current insurance declarations page that shows coverage limits, deductibles, and policy effective dates. Insurance companies need to see your liability limits, comprehensive and collision coverage amounts, and any additional coverages like rental car reimbursement. Your current premium amount and payment history also influence new quotes (insurers view consistent payment patterns favorably). Collect documentation of any previous claims within the past five years, as the Insurance Research Council data shows that claim frequency affects rates more than individual claim amounts. Provide proof of accident forgiveness coverage or safe driver discounts on your current policy when you request new quotes.

Vehicle Information and Damage Assessment

Provide your vehicle identification number, year, make, model, and current mileage when you request quotes. Insurance companies use this information to calculate replacement costs and repair estimates for future claims. Include professional damage assessments from licensed auto body shops, as these estimates help insurers understand the severity of your recent accident. Submit repair receipts if work has already been completed, along with any diminished value assessments. The actual cash value of your vehicle before the accident affects how insurers perceive your risk profile and coverage needs for future incidents (newer vehicles typically cost more to insure due to higher replacement values).

Final Thoughts

Most insurance companies process new applications within 24-48 hours, but coverage takes effect immediately once you complete payment. Start your search for car insurance quotes for drivers with accidents within one week of your incident to secure the best rates before your current policy renewal. Focus on companies that offer accident forgiveness programs or safe driver discounts to offset premium increases.

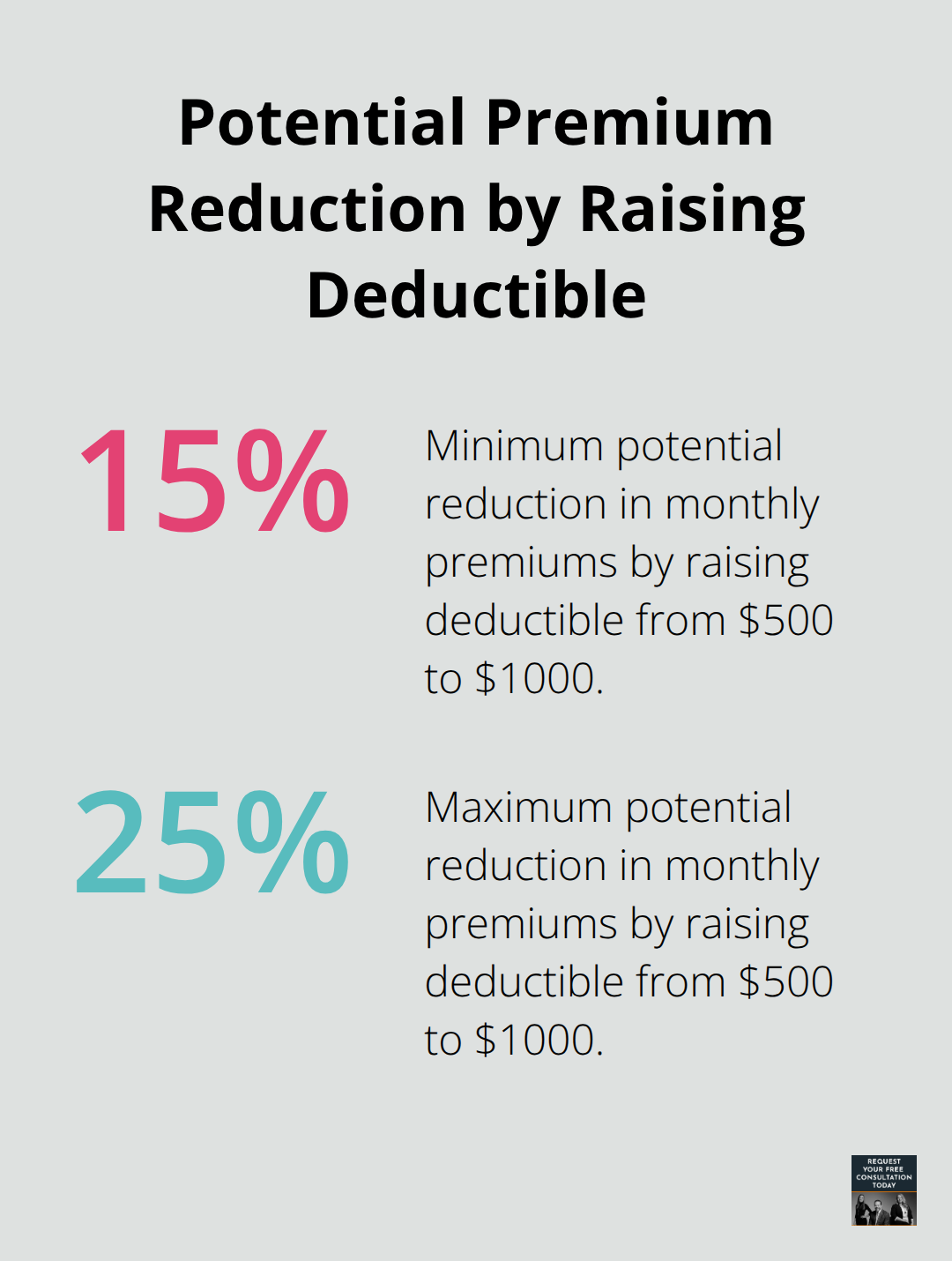

Bundle your auto insurance with home or rental coverage to reduce overall costs. Consider raising your deductible from $500 to $1,000 to lower monthly premiums by 15-25%, but maintain adequate savings for potential claims. Most insurers provide immediate online quotes that reflect your accident history accurately.

If your accident involved significant injuries, property damage over $10,000, or disputes over fault determination, legal representation becomes valuable (especially when insurance companies deny coverage based on technicalities). We at Schaar & Silva LLP help Santa Cruz County residents navigate complex insurance claims and property damage evaluations. Insurance companies often undervalue claims, so legal support protects your rights and maximizes your settlement potential while we handle negotiations with insurance providers.