Soft tissue injuries from car accidents often seem minor at first, but they can cause months of pain and expensive medical bills. Insurance companies frequently undervalue these claims, leaving accident victims without fair compensation.

We at Schaar & Silva LLP have helped many Santa Cruz residents navigate soft tissue injury settlements and recover what they deserve. This guide shows you how to build a strong claim and push back against low offers.

What Soft Tissue Injuries Actually Look Like After a Car Crash

Common Soft Tissue Injuries in Santa Cruz Car Accidents

Whiplash, shoulder sprains, and torn ligaments appear most often in Santa Cruz car accidents, and they carry far more serious consequences than insurance companies want you to believe. Whiplash occurs when your neck snaps forward and backward during impact, straining the muscles and ligaments that stabilize your spine. Shoulder injuries happen when your arm gets wrenched during the collision, tearing rotator cuff muscles or labrum tissue. Knee and ankle sprains result when your legs twist or compress against the dashboard or floorboard.

The core problem is that these injuries don’t show up clearly on X-rays the way fractures do, which gives insurers an excuse to downplay them. In California, soft tissue injury settlements range from $2,500 to $15,000 for minor cases, but moderate injuries like torn shoulder ligaments average around $52,000, and disc injuries with nerve involvement reach about $68,500. The difference between these numbers depends entirely on how well you document your injury and its impact on your daily life.

Recovery Timelines Prove Injury Severity

Most soft tissue injuries require physical therapy for four to six months, and some people deal with chronic pain for a year or more. This extended timeline actually strengthens your settlement negotiations because it proves the injury is serious and not just a minor inconvenience. Insurers often pressure you to settle within the first month or two when you’re still in acute pain and haven’t completed treatment-exactly when your claim is weakest.

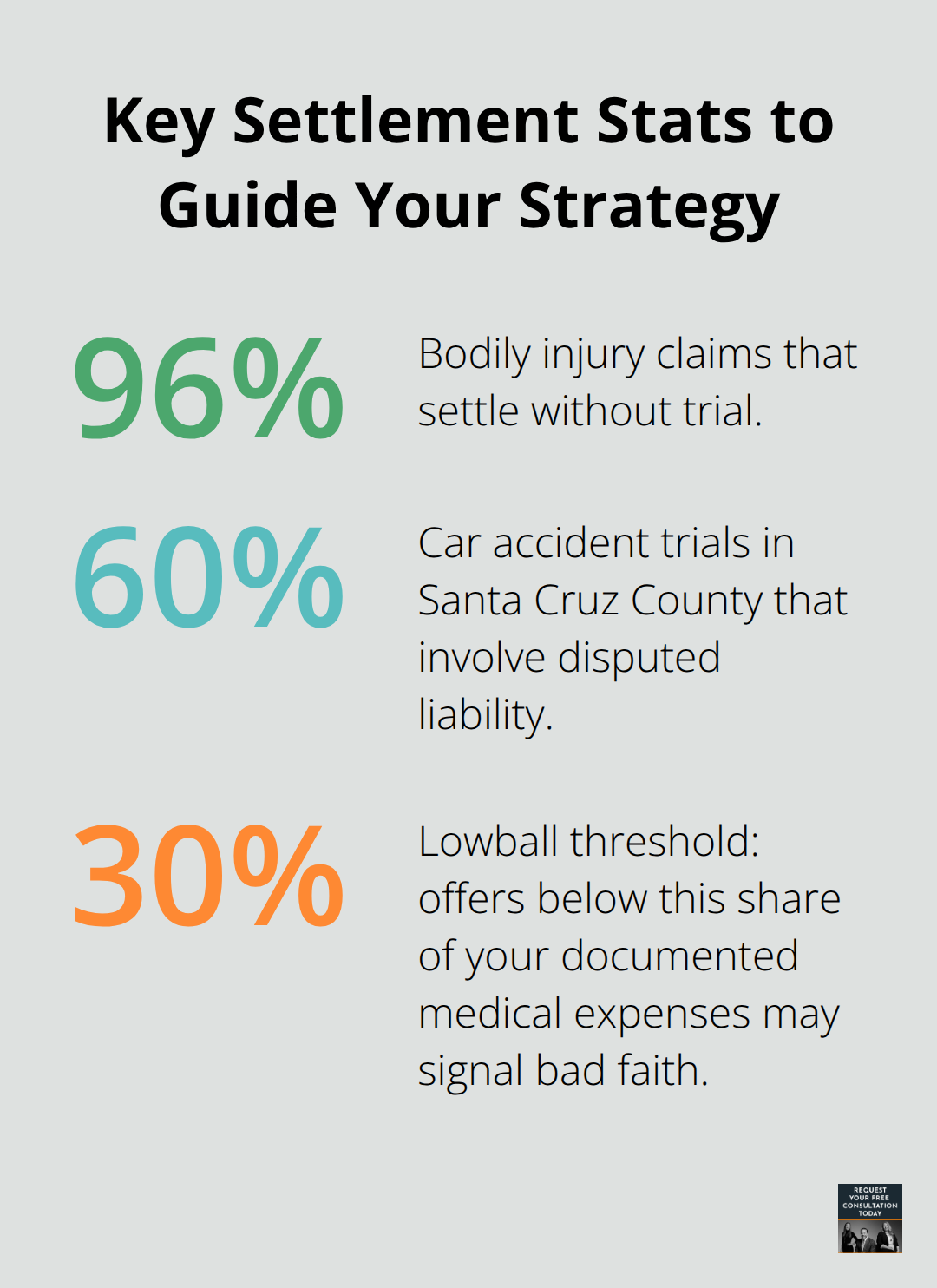

You should refuse early settlement offers and instead focus on completing your medical treatment plan. Keep detailed records of every physical therapy session, every doctor visit, and every day you miss work because of pain or appointments. According to the Insurance Research Council, about 96 percent of bodily injury claims settle without trial, but settlements take an average of six to eight months to resolve. That timeline exists because serious cases need time to accumulate medical evidence and demonstrate lasting impact.

The longer your treatment continues and the more providers document your progress, the stronger your negotiating position becomes when you finally make a demand to the insurance company.

Medical Records Determine Your Settlement Value

Emergency room records, imaging reports from MRI or CT scans, and physical therapy notes form the foundation of a credible claim. Insurance adjusters apply a multiplier of 1.5 to 5 times your medical expenses to calculate pain and suffering damages, but only when your medical records are thorough and consistent. If you have $15,000 in medical bills and treatment gaps or missing documentation, an adjuster might apply a 1.5 multiplier to justify a $22,500 settlement. If your records are complete and show ongoing treatment, that same $15,000 in medical expenses could support a 3 or 4 times multiplier, producing $45,000 to $60,000 in total compensation.

This is why starting treatment immediately after your accident matters so much. Delays in seeking care give insurers ammunition to claim your injuries weren’t that serious or that something else caused them. Complete medical documentation from all your providers-emergency care, imaging, physical therapy, and follow-up visits-transforms a weak claim into a strong one that insurers take seriously during settlement negotiations.

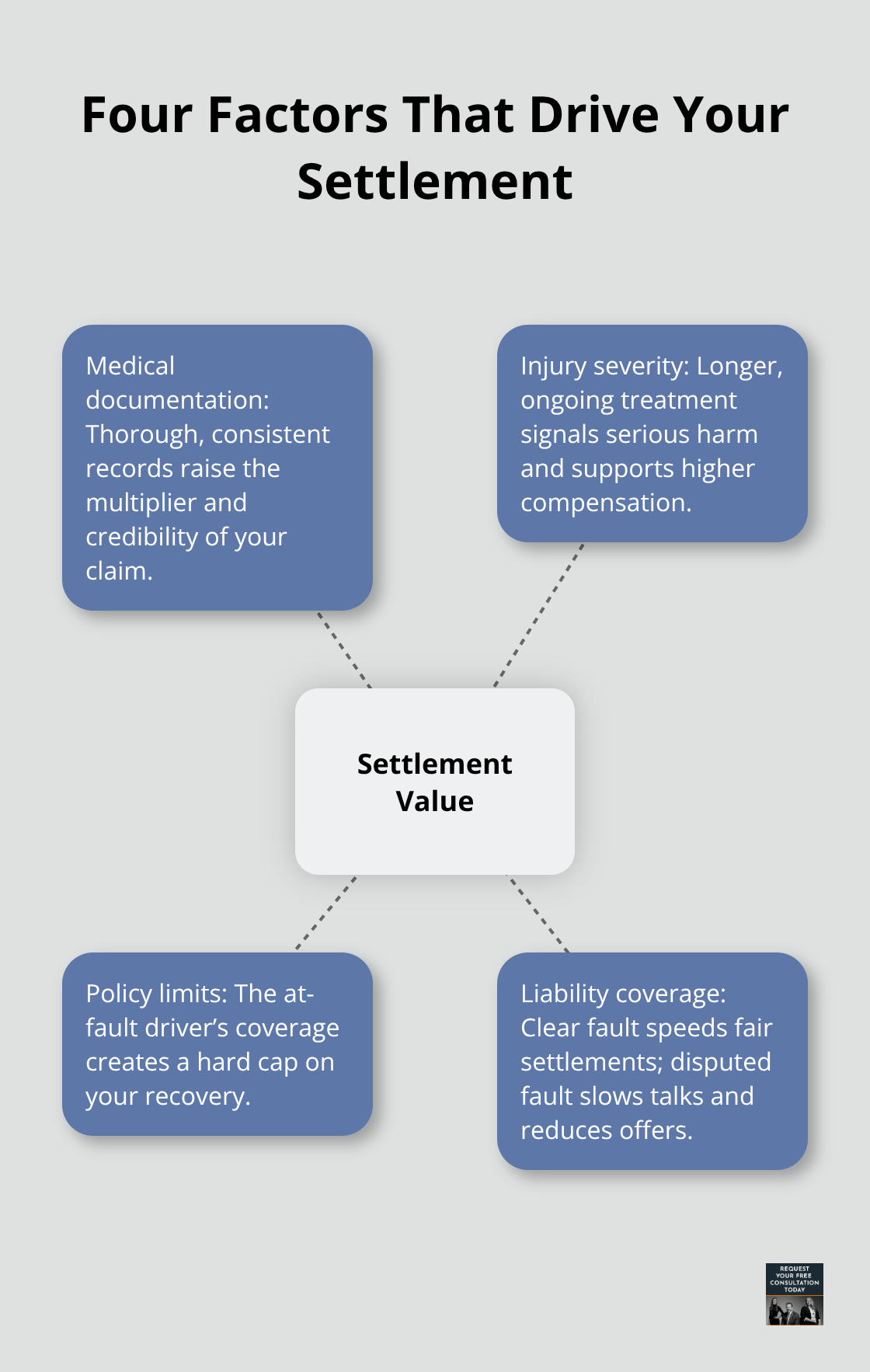

What Really Determines Your Settlement Value

Your settlement amount comes down to four concrete factors that insurance adjusters measure and calculate every single day. Medical documentation directly controls the multiplier insurers apply to your case. Injury severity, measured by treatment duration and ongoing medical needs, shapes how adjusters view your claim. Insurance policy limits create a hard ceiling on what you can recover. Liability coverage determines whether the at-fault driver’s policy can actually pay your claim. Understanding how each factor works gives you real leverage during negotiations because you’ll know exactly what numbers insurers use behind closed doors.

How Insurers Calculate Your Multiplier

Insurance adjusters start with your economic damages-medical bills, lost wages, vehicle repairs, and rental car costs. According to the Insurance Information Institute, property damage from vehicle accidents averages over $3,800, and medical expenses typically run much higher for soft tissue cases. Once they have your economic total, they multiply it by a factor between 1.5 and 5 to create your pain and suffering award. A case with $20,000 in medical expenses and a 1.5 multiplier produces $30,000 total. The same $20,000 with a 3 multiplier produces $60,000. That single multiplier number determines whether you recover fairly or get shortchanged.

Insurers assign lower multipliers when your medical records have gaps, when treatment stopped early, or when documentation is sparse. They assign higher multipliers when your records show consistent treatment over months, when multiple providers confirm your injury, and when physical therapy notes document ongoing impairment. This means the quality of your medical documentation directly translates to thousands of dollars in your pocket. If you stop physical therapy at week eight because you feel better but your doctor recommends sixteen weeks, that early stop gives insurers justification to apply a 2 multiplier instead of a 3.5 multiplier. The difference on $20,000 in medical costs is $30,000 in lost compensation.

Injury Severity Extends Your Negotiating Timeline

Severe soft tissue injuries require longer treatment periods, and longer treatment periods generate more medical records that support higher settlement values. A minor ankle sprain that heals in six weeks typically settles for $6,750 to $12,000. A moderate shoulder injury with ligament damage that requires physical therapy for five months settles for around $52,000. A disc injury with nerve involvement that involves ongoing care for eight months or longer reaches $68,500 or higher.

The treatment duration itself becomes evidence of severity. Insurance adjusters know that people with minor injuries stop treatment quickly because pain subsides. People with serious injuries continue treatment for months because they still hurt and still cannot function normally.

Your ongoing care needs create a paper trail that proves to any reasonable person that your injury matters. You should never stop treatment early just to settle faster. Continuing treatment as long as your doctor recommends strengthens your claim and typically increases your final settlement by 40 to 60 percent compared to cases where victims cut treatment short. This extended timeline actually works in your favor during negotiations because it demonstrates that your injury is real and persistent, not temporary or exaggerated.

Policy Limits Create Your Settlement Ceiling

Every auto insurance policy in California has a bodily injury liability limit, typically $15,000 per person or $30,000 per accident for basic coverage. Some drivers carry higher limits like $100,000 or $250,000. If the at-fault driver carries only $15,000 in liability coverage and your medical bills total $35,000, you cannot recover more than $15,000 from their insurance no matter how strong your claim is. This hard cap on recovery frustrates many accident victims who assume their damages will be fully covered.

Uninsured or underinsured motorist coverage on your own policy becomes your path to full recovery when the other driver’s coverage runs out. Many Santa Cruz residents carry only minimum coverage without realizing that a serious soft tissue injury can quickly exceed $50,000 in total damages. You cannot control what coverage the other driver carries, but you can control what happens next. If their policy limit is too low to cover your claim fairly, your own uninsured motorist coverage kicks in to bridge the gap. This is a critical detail that many accident victims overlook until it’s too late, which is why understanding your own policy limits matters as much as understanding theirs.

How Liability Coverage Affects Your Recovery Options

Liability coverage determines whether the at-fault driver’s insurance company will actually pay your claim or fight it tooth and nail. Clear liability (where the other driver is obviously at fault) makes settlements faster and easier because the insurance company knows they will lose at trial. Disputed liability (where fault is unclear or contested) slows negotiations because insurers have leverage to offer lower amounts, knowing you might not win if the case goes to court. In Santa Cruz County, about 60 percent of car accident trials involve disputed liability, which means fault determination is unclear or contested. When liability is disputed, your evidence becomes everything-police reports, witness statements, accident scene photos, and vehicle damage patterns all matter. Strong liability evidence combined with strong medical documentation creates the conditions for a fair settlement, even when the other driver’s insurance company initially resists paying what your claim is worth.

Building Your Case Step by Step

Insurance companies count on accident victims to panic and settle too quickly, which is why solid evidence matters more than almost anything else before you negotiate. Start with your police report the day after your accident, not weeks later when details fade. Request the official report from the Santa Cruz County Sheriff or local police department and verify that it accurately describes how the crash happened, road conditions, and any citations issued. Next, photograph your vehicle damage from multiple angles, the accident scene if you can safely return, and any visible injuries like bruising or swelling. Collect contact information from all witnesses at the scene, not just one or two, because multiple witness statements carry significantly more weight during settlement negotiations than a single account. Document the date, time, and location of your accident with precision because insurance adjusters cross-reference these details against traffic camera footage and weather records to either strengthen or weaken liability arguments.

Medical Records Form Your Settlement Foundation

Your medical records determine your settlement value, so start treatment within 48 hours of your accident and never skip appointments. Request records from every provider you see, including the emergency room, your primary care doctor, physical therapists, and any specialists, then compile them into a single chronological document showing your treatment timeline and progress. Insurance adjusters specifically look for gaps in treatment because they use those gaps to claim your injuries healed faster than your medical records suggest. If you see a physical therapist twice a week for six weeks then stop for four weeks before returning, that four-week gap gets weaponized against you during settlement discussions.

Document Your Daily Impact

Keep a detailed pain journal that records daily symptoms, medications, missed work days, and activities you cannot do because of your injury, then attach it to your demand letter when you present your settlement position. This journal transforms abstract pain into concrete evidence that insurers cannot dismiss. The more specific your documentation (for example, “unable to lift my right arm above shoulder height” rather than “shoulder hurts”), the stronger your claim becomes during negotiations.

Understand Insurer Timelines and Compliance

According to California’s Fair Claims Settlement Practices Regulations, insurers must acknowledge your claim within 15 days, respond within 15 days, decide within 40 days, and pay within 30 days after settlement. These clear deadlines give you leverage to track their compliance and escalate if they miss them. When insurers offer settlements far below your documented medical expenses and pain and suffering multipliers, reject the offer in writing and explain exactly why it falls short.

Recognize Bad Faith Negotiation Patterns

Offers that represent less than 30 percent of your documented medical expenses typically signal bad faith negotiation patterns according to the California Department of Insurance, which gives you grounds to push back harder or pursue litigation if necessary. Insurance companies know most accident victims lack legal representation and will accept lowball offers out of desperation or exhaustion. You should not accept these offers. Instead, counter with a detailed demand letter that includes your complete medical chronology, economic damages, pain and suffering calculations based on the multiplier method, and comparable case results from Santa Cruz County. This professional response signals that you understand your claim’s value and will not accept pennies on the dollar.

Final Thoughts

Soft tissue injury settlements in Santa Cruz demand careful attention because insurance companies profit when they pay you less than your claim deserves. You now understand how multipliers work, why medical documentation transforms weak claims into strong ones, and how to spot offers that fall short of fair compensation. The gap between accepting a lowball settlement and fighting for what you actually deserve often reaches tens of thousands of dollars, which makes patience and thorough documentation throughout your recovery absolutely worth your effort.

Complete your medical treatment exactly as your doctor recommends, not faster than necessary to settle quickly. Organize your police report, medical records, wage documents, and witness statements into one file, then calculate your economic damages with precision and track your pain and suffering through a detailed journal. When the insurance company presents an offer, measure it against the multiplier method you learned here and reject any offer that falls below 30 percent of your medical expenses or applies a multiplier lower than your injury severity justifies.

We at Schaar & Silva LLP help Santa Cruz residents recover fair compensation for soft tissue injury settlements by handling the legal work while you focus on healing. Our team connects you with medical lien services so you receive treatment without upfront costs, evaluates your property damage claim for fair valuation, and provides the support you need throughout your recovery. Contact us for a free case evaluation to discuss your situation and learn how we can help you secure the compensation you deserve.