After a car accident in Santa Cruz County, property damage valuation becomes one of your biggest concerns. Insurance companies use specific methods to calculate what your vehicle or property is worth, and understanding this process helps you get a fair settlement.

We at Schaar & Silva LLP have helped countless accident victims navigate property damage claims. This guide walks you through how insurers evaluate damage, what documentation matters, and how to challenge offers that fall short of what you deserve.

How Insurers Calculate What Your Vehicle Is Worth

Two Valuation Methods That Determine Your Settlement

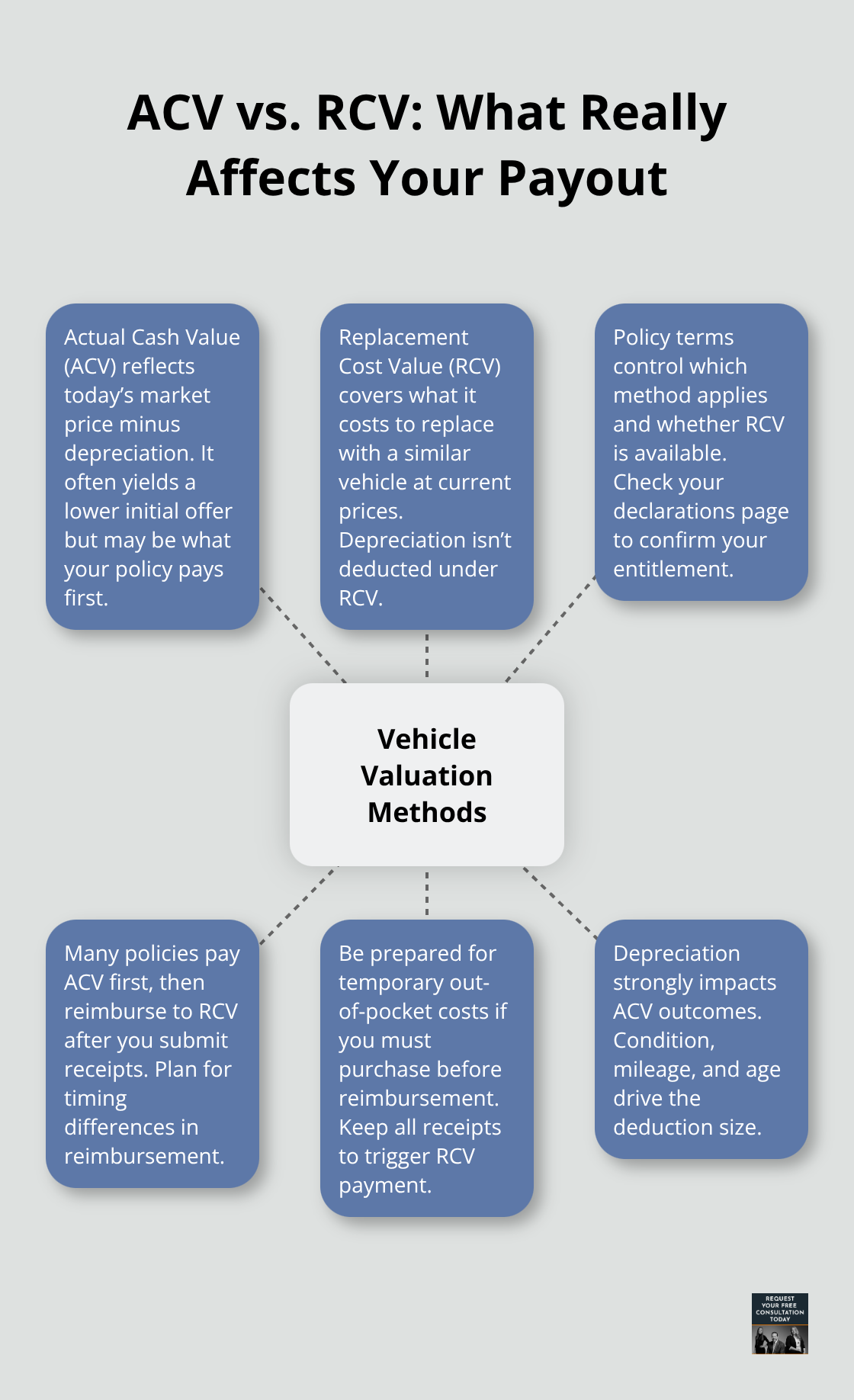

Insurance companies use two primary valuation methods when assessing your vehicle after an accident in Santa Cruz County, and understanding the difference between them directly impacts your settlement. Actual Cash Value, or ACV, represents what your vehicle would sell for on the open market today, accounting for depreciation based on age, mileage, and condition. Replacement Cost Value, or RCV, reflects what it would cost to replace your vehicle with a similar one at current market prices, without depreciation factored in. Most insurers initially offer ACV settlements, which can be substantially lower than RCV, sometimes by thousands of dollars. Your policy language determines which method applies, so reviewing your declarations page before filing a claim reveals what you’re actually entitled to receive.

Many policies pay ACV first, then reimburse the difference to RCV once you provide receipts for replacement purchases, meaning you may need to cover costs out-of-pocket temporarily.

Why NADA Guides Underestimate Local Repair Costs

Insurance adjusters rely heavily on NADA guides and comparable vehicle sales data to establish fair market value, but these tools frequently underestimate true repair or replacement costs in Santa Cruz County’s local market. Obtaining at least three independent repair estimates from licensed local shops becomes non-negotiable. When you present multiple estimates in writing to the adjuster, you create a credible baseline that can push settlements higher by $2,000 to $5,000 for moderate damage. This approach shifts the negotiation in your favor and prevents the insurer from anchoring to artificially low figures.

Hidden Damage Changes Everything

Structural frame damage, water intrusion behind panels, and HVAC smoke damage often emerge only after thorough inspection, yet these issues can dramatically elevate repair costs if discovered late. You should insist on a full mechanic inspection before accepting any settlement offer, and document pre-existing condition through photos and maintenance records. Hidden problems compound valuation issues significantly and can shift your entire claim calculation once identified.

Diminished Value Claims Add Another Layer

California law allows you to pursue diminished value claims, meaning compensation for the vehicle’s depreciation beyond repair costs alone, typically ranging from 5% to 20% depending on the vehicle’s age and mileage. Newer vehicles with low mileage at the time of impact qualify for higher diminished value percentages. Proving diminished value requires professional appraisal, which costs money upfront, but the recovery often justifies the expense. Understanding how adjusters calculate these additional losses positions you to negotiate more effectively when settlement discussions begin.

Filing a Claim Without Leaving Money on the Table

Act Immediately to Protect Your Recovery Window

The moment you file a property damage claim in Santa Cruz County, you enter a process with strict timelines and specific requirements that directly affect your settlement amount. California law requires insurers to acknowledge your claim within 15 days and settle within 40 days after you submit proof of loss, according to the California Department of Insurance. This compressed timeline means you cannot afford delays in documentation or communication. File your claim immediately after the accident, even if you haven’t gathered all photos or repair estimates yet, because waiting can jeopardize your recovery window. Notify your insurer in writing rather than by phone, creating a paper trail that protects you if disputes arise later. Include your policy number, the loss date, and a brief description of what happened.

Attach your initial photos and police report if available, then follow up with additional documentation as you obtain it.

Present Evidence That Counters Lowball Valuations

The adjuster assigned to your case will contact you within days to schedule an inspection, and this is where many Santa Cruz County claimants make critical mistakes by accepting the first valuation without question. Have your three independent repair estimates already in hand when the adjuster arrives, along with photos that document pre-accident condition and the damage itself. Present the estimates in writing and ask the adjuster to explain in writing why their valuation differs from your local contractor quotes. This forces them to justify any lowball offers rather than simply accepting them. The California Department of Insurance states that insurers must stand behind repairs performed at your chosen shop if they meet accepted trade standards, which means poor-quality repairs become the insurer’s liability, not yours.

Handle Hidden Damage and Extended Timelines

If you discover hidden damage during repairs, immediately notify your adjuster and provide updated estimates, as the 40-day settlement window can be extended for legitimate additional losses. Keep all receipts, invoices, and communication records in a single organized file, and maintain these documents for at least three years due to California’s property damage statute of limitations. This documentation protects you throughout the claims process and beyond.

Know When to Challenge the Settlement Offer

If your insurer denies the claim or offers substantially less than your documented losses, the next step involves determining whether negotiation or legal action will recover what you deserve. We at Schaar & Silva LLP can review the settlement and help you understand your options for moving forward.

Getting More Than the Insurer’s First Offer

Start with the Reality That Initial Offers Fall Short

Your initial settlement offer from the insurance company is almost never their final position, and treating it as a starting point rather than a conclusion dramatically improves outcomes for Santa Cruz County accident victims. The adjuster’s valuation reflects their internal calculations and company profit margins, not necessarily what your vehicle is actually worth in today’s local market. When you present three independent repair estimates from licensed Santa Cruz shops, you create objective evidence that contradicts their number. If those estimates total $12,000 and the insurer offers $10,500, the $1,500 gap represents real money you’re leaving on the table by accepting passively.

Request Written Justification for Every Discrepancy

Request a written explanation from the adjuster for any discrepancy between your estimates and their valuation, forcing them to justify the difference rather than simply asserting it. Many adjusters will adjust their offer upward when confronted with credible local data they cannot easily refute. This written communication creates a paper trail that protects you if disputes escalate later and demonstrates that you took reasonable steps to resolve the matter before pursuing further action.

Leverage California’s Appraisal Provision to Pressure Fair Settlements

Challenging a lowball offer requires understanding California’s appraisal provision, which allows either party to dispute the settlement amount through a binding process involving two appraisers and an umpire. This mechanism prevents one-sided decisions and creates pressure on insurers to offer fair value rather than face appraisal costs and delays. If your vehicle suffered $10,000 in damage and the insurer offers $8,500, demanding appraisal typically prompts them to reconsider rather than commit to a lengthy dispute process.

Don’t Overlook Diminished Value Claims

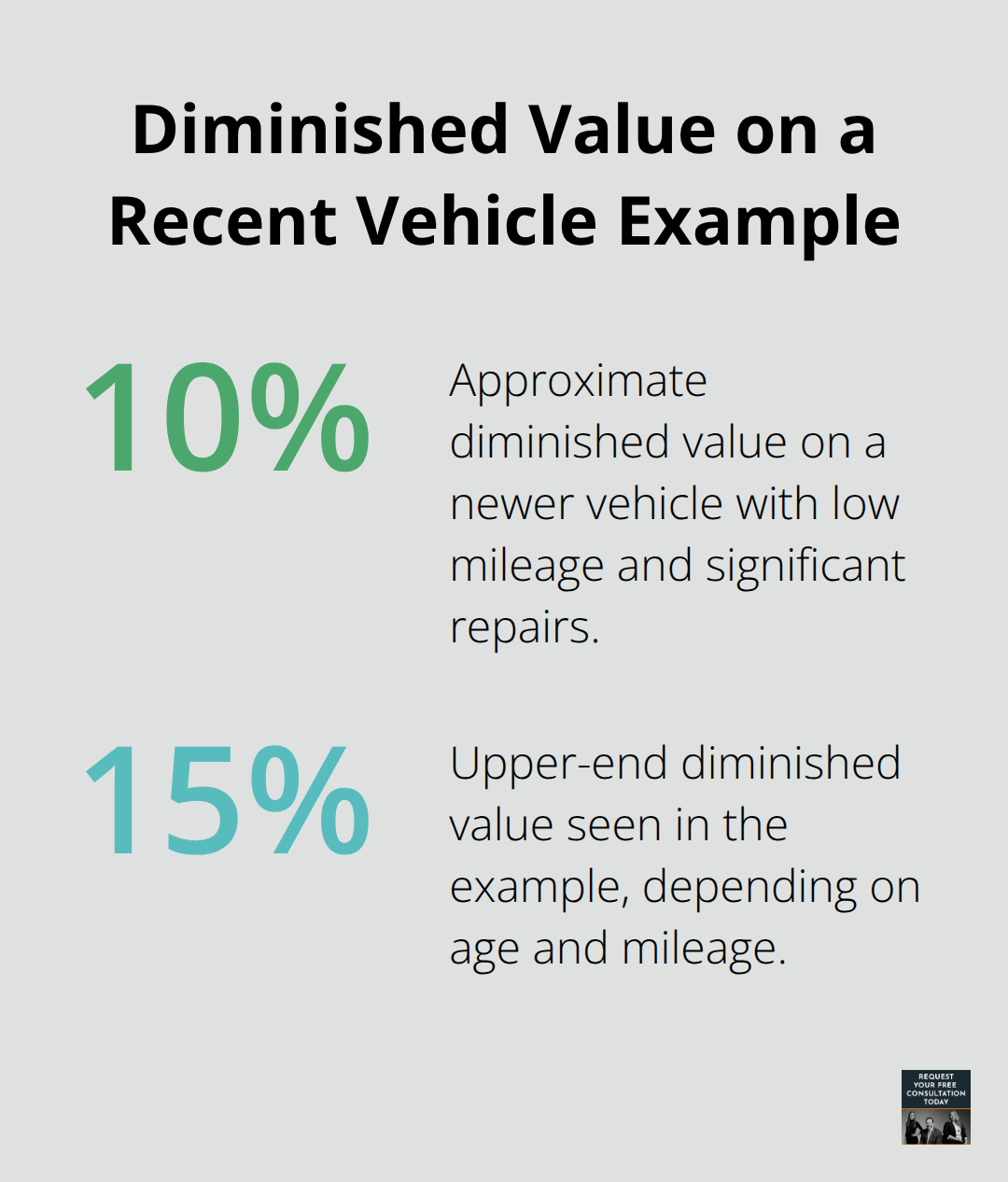

Diminished value claims deserve particular attention because many Santa Cruz claimants abandon them without attempting negotiation. A 2022 Hyundai Kona with 6,000 miles and $10,000 in repairs qualifies for diminished value compensation of roughly 10 to 15 percent beyond repair costs, potentially adding $1,000 to $1,500 to your settlement.

Insurers count on claimants not knowing this entitlement exists. California law allows you to pursue these claims, and professional appraisal (though it costs money upfront) often justifies the expense through recovery.

Know When Legal Representation Becomes Necessary

When the insurer refuses reasonable adjustments after you’ve presented strong documentation, legal representation becomes the practical next step. An attorney can evaluate your settlement offer and help determine whether negotiation or formal action recovers what you actually deserve, ensuring you understand your options before deciding how to proceed.

Final Thoughts

Property damage valuation after a car accident in Santa Cruz County demands documentation, persistence, and knowledge of your rights under California law. The methods insurers use to calculate settlement amounts often undervalue what you actually deserve, which is why presenting independent repair estimates, understanding ACV versus RCV, and pursuing diminished value claims matter so much. Your initial settlement offer is rarely final, and requesting written justification for discrepancies shifts negotiations in your favor.

Santa Cruz County residents have access to local repair shops, independent appraisers, and public adjusters who can strengthen your position during claims negotiations. The California Department of Insurance provides guidance on fair claims practices, and your policy declarations page contains the specific coverage and valuation methods that apply to your situation. Organized records of all communications, estimates, and receipts protect you throughout the process and beyond the three-year statute of limitations window.

When settlement disputes arise or your insurer refuses to adjust their offer despite strong documentation, legal representation becomes the practical path forward. We at Schaar & Silva LLP can review your settlement offer, explain your options, and guide you toward recovery that matches what you actually deserve. Contact us to discuss your property damage claim and learn how we can support your case.