![[Guide] to Pursuing Maximum Compensation for Life-Altering Injuries](https://schaarsilvalaw.com/wp-content/uploads/emplibot/catastrophic-injury-accident-hero-1776643757.jpeg)

A catastrophic injury accident can transform your life in seconds. Medical bills pile up, work becomes impossible, and the financial pressure feels overwhelming.

We at Schaar & Silva LLP know that maximum compensation requires understanding what damages you can claim and how to fight for them. This guide walks you through calculating your losses, navigating insurance negotiations, and taking legal action when necessary.

What Injuries Qualify as Life-Altering

Spinal Cord Injuries and Permanent Mobility Loss

Spinal cord injuries represent one of the most devastating outcomes from accidents. A complete spinal cord injury at the cervical level (neck) results in quadriplegia, affecting all four limbs and often requiring 24-hour care. Incomplete injuries may preserve some function, but most people face permanent mobility limitations. The costs are staggering-according to the National Spinal Cord Injury Statistical Center, lifetime care costs for a 25-year-old with high tetraplegia exceed $4.7 million, including ongoing medical treatment, home modifications, and assistive equipment.

Traumatic Brain Injuries and Cognitive Changes

Traumatic brain injuries range from mild concussions to severe damage that alters personality, memory, and motor control. The CDC reports that approximately 2.87 million traumatic brain injury-related emergency department visits occur annually in the United States. Moderate to severe TBI survivors often require cognitive rehabilitation, speech therapy, and occupational therapy lasting months or years. Many cannot return to their previous employment, creating long-term financial hardship alongside physical recovery.

Severe Burns and Lasting Disfigurement

Severe burns and disfigurement carry physical and psychological costs that extend far beyond initial healing. Third-degree burns require skin grafting and multiple surgeries, with infection risk remaining high during recovery. Burn survivors often face permanent scarring, reduced mobility in affected areas, and social stigma that impacts employment and relationships.

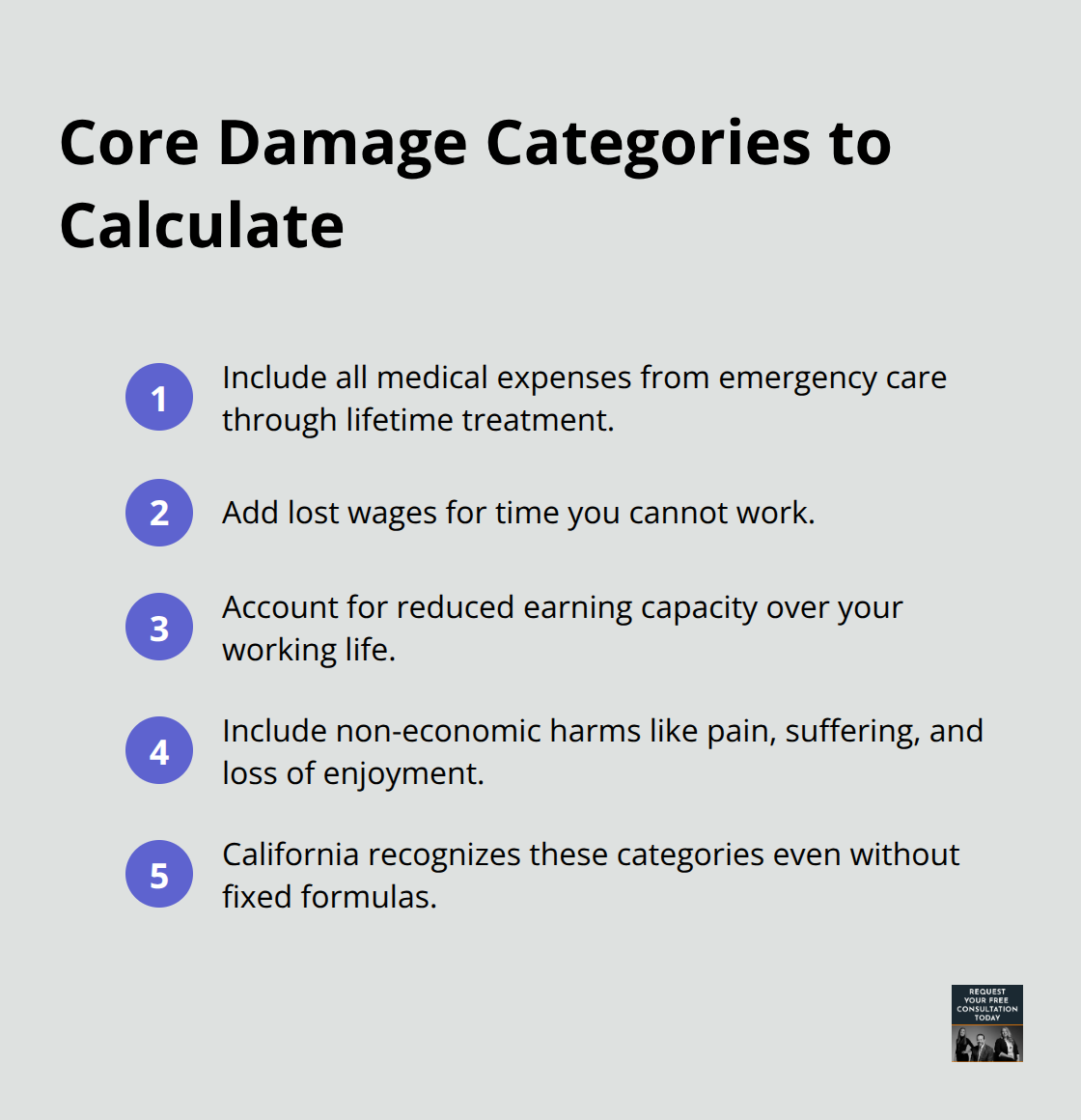

Calculating Your Economic and Non-Economic Damages

The financial impact of these injuries demands aggressive compensation strategies. Economic damages include all medical expenses, from emergency care through lifetime treatment, plus lost wages and reduced earning capacity. Someone paralyzed at age 30 who would have earned $50,000 annually until age 67 loses roughly $1.85 million in future wages alone. Non-economic damages address pain and suffering, loss of enjoyment of life, and loss of companionship.

California courts recognize these as legitimate compensation categories, though they lack fixed formulas.

Building Your Damage Case Before Negotiations

The strongest cases combine detailed medical documentation showing ongoing needs with testimony quantifying future care costs. Life care planners and medical professionals help build comprehensive damage calculations before negotiations begin. Acting quickly matters because the two-year statute of limitations for personal injury claims moves fast, and evidence preservation becomes harder as time passes. Understanding what damages you can claim sets the foundation for the next critical step: gathering the documentation and evidence that insurers cannot ignore.

What Damages Can You Actually Claim

Medical Costs That Extend Far Beyond Initial Treatment

Medical bills after a life-altering injury spiral quickly, and most people underestimate what they can recover. When someone suffers a spinal cord injury, the initial hospitalization and emergency care might cost $50,000 to $100,000 alone, but the real financial burden emerges over decades. If you’re paralyzed at age 35, your lifetime medical costs could exceed $4.7 million according to the National Spinal Cord Injury Statistical Center, factoring in surgeries, medications, physical therapy, home modifications, and assistive equipment. This is where many injured people make a critical mistake: they accept a settlement based only on past medical bills, ignoring future treatment costs.

A life care planner-a professional who calculates long-term care needs-quantifies exactly what you’ll need for the rest of your life. This document becomes your foundation for demanding fair compensation.

Lost Wages and Earning Potential

Lost wages hit even harder because your injury didn’t just stop you from working today; it eliminated your earning potential. Someone earning $60,000 annually who becomes unable to work faces not just lost income but also lost retirement contributions, health insurance benefits, and promotions they would have received. Over 32 working years, that amounts to potentially $1.92 million in direct wages plus thousands more in lost benefits.

If your injury reduces your earning capacity rather than eliminating it entirely-meaning you can work but earn less-you still deserve compensation for that difference. Tax returns, pay stubs, and employment records prove past losses, while vocational professionals quantify future earning loss based on your age, education, and injury severity.

Pain, Suffering, and Loss of Life Quality

Non-economic damages address the pain, suffering, and life quality you’ve lost, and California courts take these seriously. There’s no fixed formula for what a day of pain and suffering is worth, which frustrates many people, but this actually works in your favor if you build a strong case. Medical records showing ongoing pain, depression, or anxiety provide the foundation.

Day-in-the-life videos that document how your injury affects daily activities-struggling to shower, managing medications, attending therapy sessions-create emotional impact that numbers alone cannot. Testimony from family members about changes in your personality, independence, and relationships strengthens these claims significantly. Courts in California have awarded substantial non-economic damages when evidence clearly demonstrates permanent life changes.

Calculating Total Compensation Through the Multiplier Method

The multiplier method often applies here: take your economic damages and multiply by 1.5 to 5 depending on injury severity and evidence quality. A case with $500,000 in economic damages and strong non-economic evidence might justify $1.5 million to $2.5 million in total compensation. Insurance companies count on injured people accepting lowball offers out of desperation, but understanding what you can legitimately claim shifts the negotiating power in your direction.

Now that you know what damages you can claim, the next step requires gathering the documentation and evidence that insurers cannot ignore or dismiss.

Turning Evidence Into Leverage

Collect Evidence Immediately After the Accident

The moment after an accident is when evidence matters most, yet most injured people focus on pain management instead of documentation. Start collecting evidence immediately: the police report, witness contact information, scene photographs and videos, medical records from every visit, pay stubs showing lost income, repair estimates, and receipts for any accident-related expenses. This foundation determines whether insurers take your claim seriously or lowball you by 50 percent or more. Medical records deserve special attention because they create the paper trail proving your injuries are real and ongoing. Each doctor visit, therapy session, and prescription refill strengthens your damage calculation.

Photograph your injuries at different stages of healing, and preserve anything showing how the accident disrupted your life.

Protect Your Case During the Investigation Phase

Insurance companies investigate aggressively, so expect them to request medical authorizations and conduct surveillance. Do not sign broad medical authorizations that give them access to unrelated records, and avoid social media posts about your recovery or activities. Anything you post can be twisted to suggest your injuries are less severe than documented, so consider a temporary online absence until your case settles. Maintain a detailed journal documenting daily limitations-this record becomes powerful evidence when insurers question the severity of your condition.

Build a Comprehensive Demand Package

Insurance negotiations typically begin within weeks of your claim filing, and this is where most injured people lose thousands of dollars. Insurers count on you accepting quick settlements before you understand your full damages picture. Never negotiate without a comprehensive demand package that includes your economic damages breakdown, medical summaries, life care plan if applicable, liability analysis showing the other party’s fault, and supporting exhibits like medical records and pay stubs. The demand should exceed what you actually expect to receive because negotiation involves counteroffers.

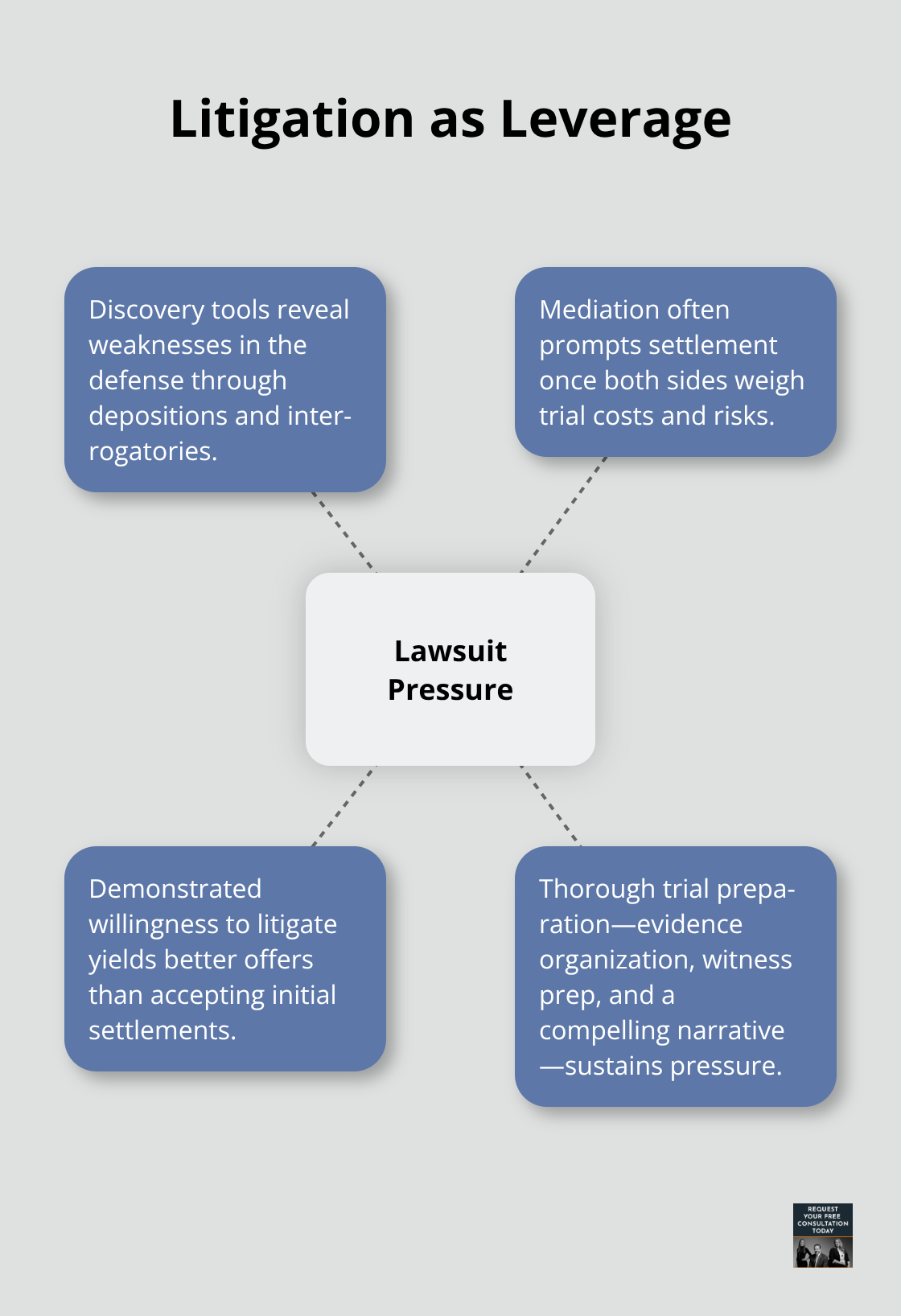

Use Litigation as Leverage When Needed

If the insurer rejects your demand or offers significantly less, filing a lawsuit shifts leverage dramatically because discovery tools like depositions and interrogatories expose weaknesses in their defense. Many cases settle during mediation after a lawsuit is filed, when both sides recognize the costs and risks of trial. Willingness to litigate often produces better settlements than accepting initial offers.

If settlement negotiations stall, your attorney should prepare for trial by organizing evidence, preparing witnesses, and developing a compelling narrative about your injuries and their impact.

Act Within the Statute of Limitations

The statute of limitations gives you two years from your injury date to file a lawsuit, so timing matters strategically. Acting quickly preserves evidence, locks in witness testimony while memories are fresh, and prevents the other party from destroying documents.

Final Thoughts

Maximizing compensation after a catastrophic injury accident requires you to act strategically within the two-year statute of limitations, document everything immediately, and refuse lowball offers from insurers. Most injured people settle too quickly because they underestimate future medical costs, lost earning potential, and non-economic damages-a spinal cord injury survivor deserves $4.7 million or more in lifetime care costs, and lost wages extend decades beyond your current job. Building a comprehensive demand package with medical documentation, life care plans, and liability analysis forces insurers to take your claim seriously instead of dismissing it with initial offers.

Having legal representation changes everything because insurers negotiate differently when they know you’re prepared to litigate. An attorney who understands California’s damage rules, has trial experience, and won’t accept inadequate settlements shifts the entire negotiation dynamic in your favor. We at Schaar & Silva LLP serve Santa Cruz County and surrounding areas, and we help injured people navigate the legal complexity of medical bills, property damage claims, and recovery.

You’ve been through enough without fighting insurance companies alone. The compensation you deserve exists, but only if you pursue it strategically and refuse to settle for less than what your injuries actually cost.