A lost wages accident can devastate your finances when you’re already dealing with injuries and recovery. Medical appointments, time away from work, and lost earning capacity add up quickly, leaving many accident victims unsure about their rights.

We at Schaar & Silva LLP help people in Santa Cruz County, Sacramento, and Oakland recover the income they’ve lost due to accidents. This guide walks you through how lost wages are calculated, what compensation options exist, and the concrete steps to recover what you’re owed.

How Lost Wages Are Calculated

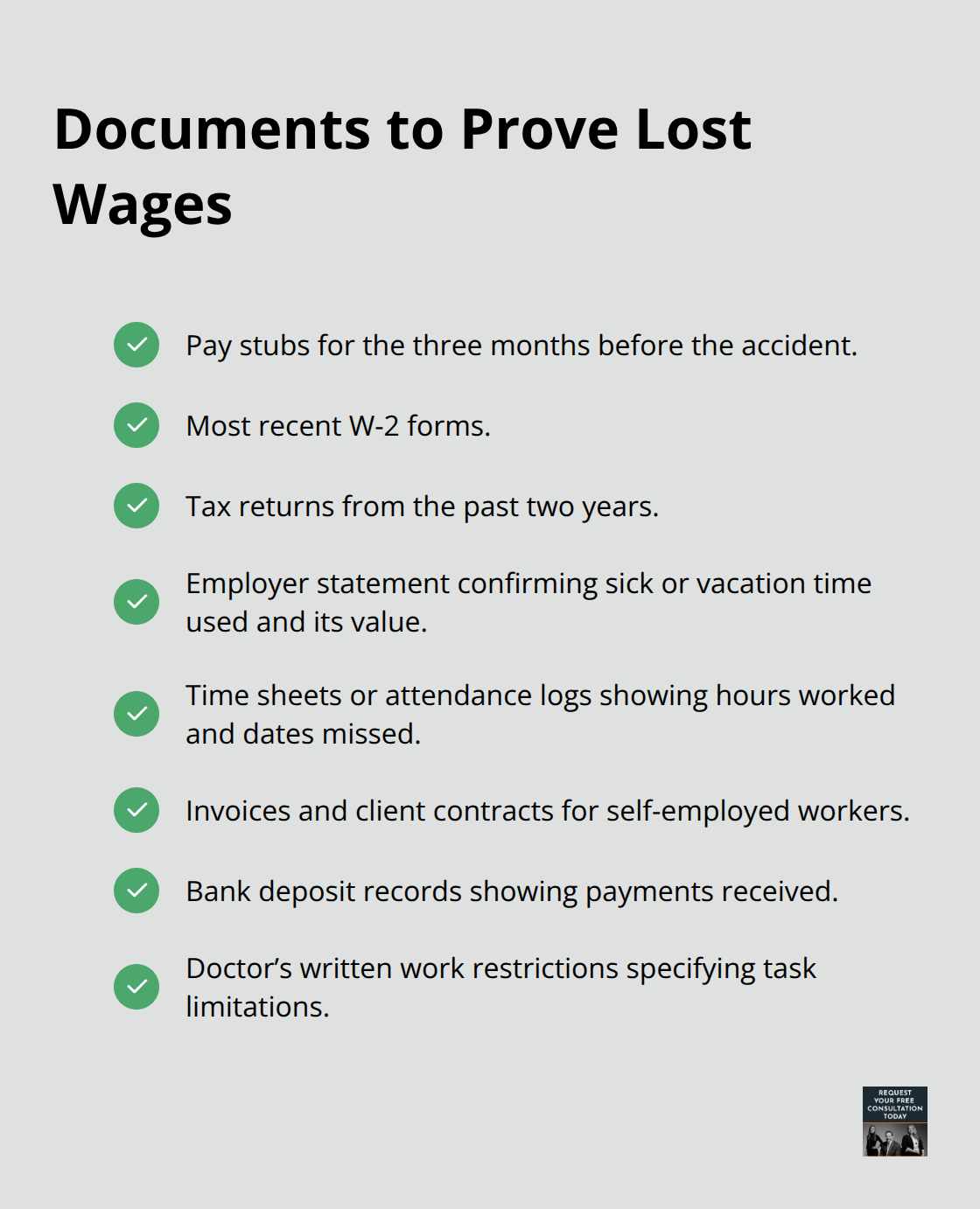

Calculating lost wages after an accident requires understanding your actual income before the crash and documenting every hour you missed. Your pre-accident income forms the foundation for this calculation, and it looks different depending on how you earned money. If you received a salary, your calculation is straightforward-use your gross annual salary divided by the number of working days to find your daily rate. For hourly workers, multiply your hourly rate by the hours you missed. Commission-based and self-employed workers face more complexity because their income fluctuates, which is why tax returns from the past two years, bank deposits showing client payments, and detailed invoices become essential documentation. The strength of your wage-loss claim depends entirely on how thoroughly you document this income. Pay stubs, W-2 forms, and direct deposit records all serve as proof of what you earned before the accident.

Time Away from Work Adds Up Faster Than You Think

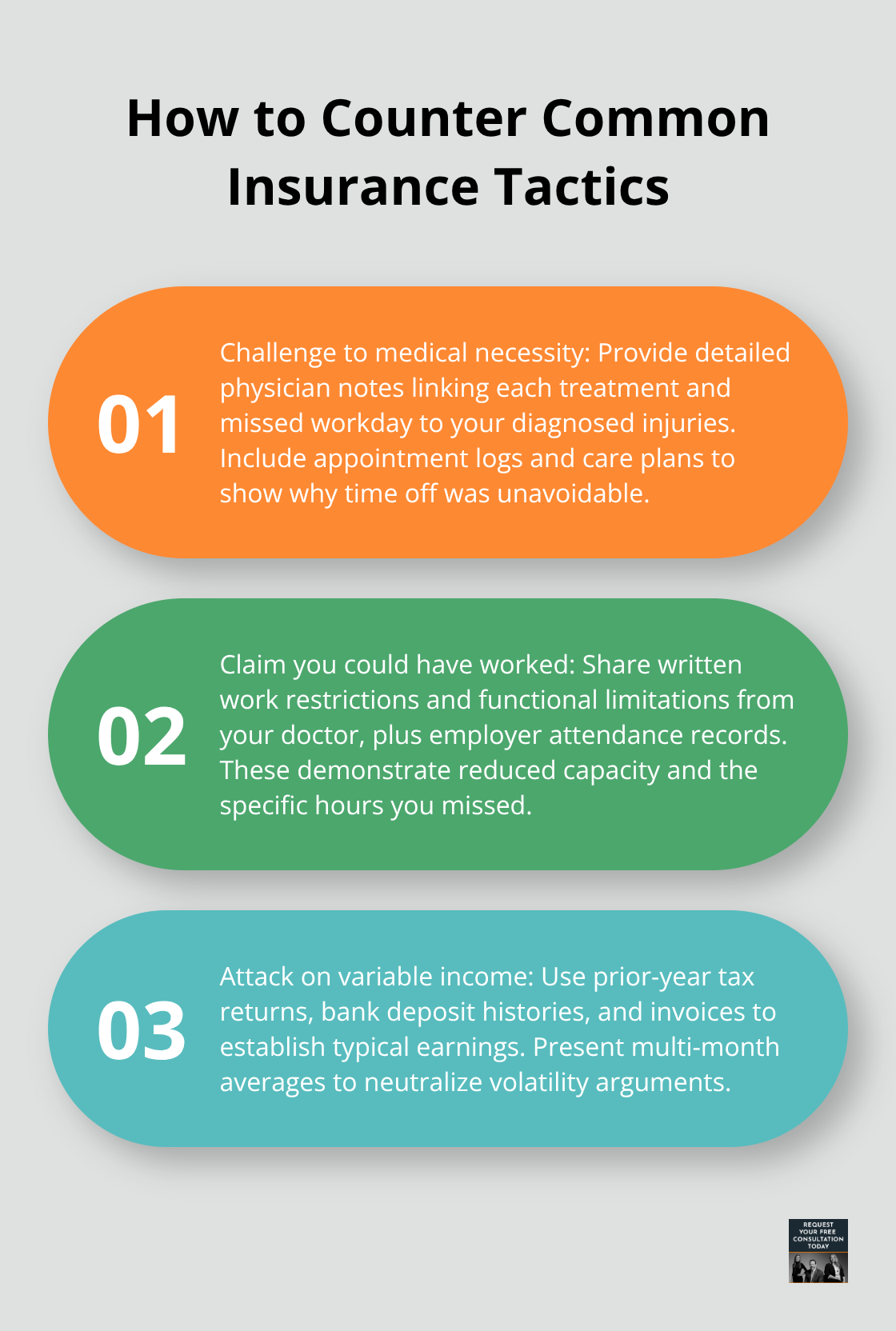

Medical appointments, recovery time, and physical limitations create gaps in your work schedule that translate directly into lost income. If you took sick leave or vacation time for treatment, that loss still counts as a wage-loss claim because you depleted earned benefits that have real financial value. Returning to work with restrictions or reduced hours also generates wage-loss claims if your earnings dropped or your job duties became limited due to injuries. You should document every medical appointment with dates and duration, obtain written work restrictions from your treating physician that specify what tasks you cannot perform, and collect attendance records showing the hours you missed. Insurance companies often challenge these claims by questioning whether treatment was necessary or whether you could have worked around appointments, so clear documentation from your doctor linking your missed work directly to the accident strengthens your position.

Future Earning Capacity Requires Professional Assessment

When injuries cause permanent effects that limit your ability to earn in the future, your claim should include diminished earning capacity as a separate damage from past wage loss. This requires vocational analysis and earnings projections, often prepared by vocational professionals or economists who review your medical restrictions, work history, and job market data. A permanent injury that prevents you from performing your previous job or requires a career change has real financial consequences that extend years beyond your recovery period. If you suffered a brain injury, spinal injury, or other serious condition from your accident, the long-term impact on your earning ability can dwarf the immediate lost wages. Calculating these complex damages involves working with qualified professionals who can quantify what your reduced earning capacity means in dollars.

What Compensation Options Exist for Your Lost Income

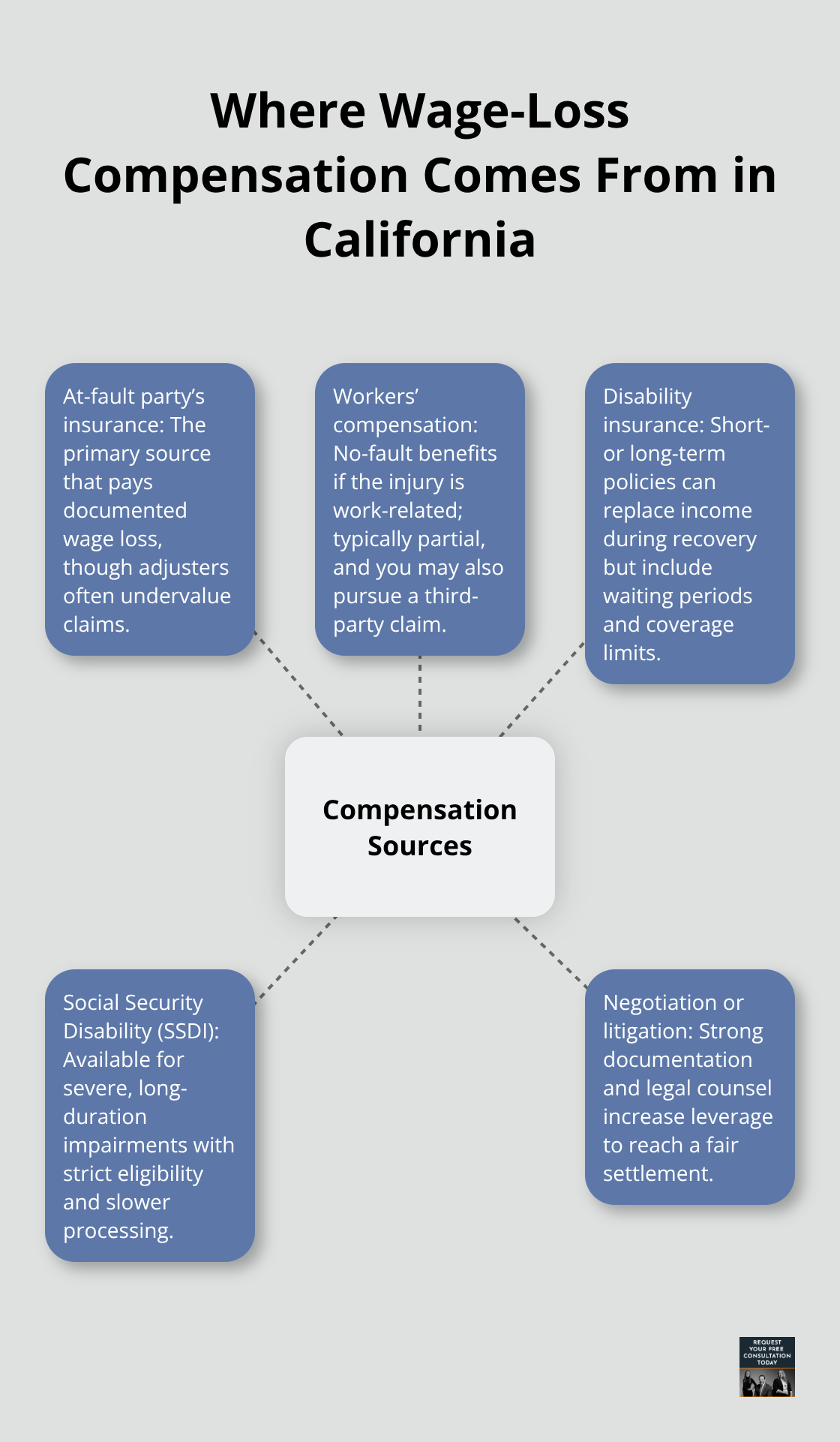

Understanding the different sources of compensation available to you helps you pursue all avenues for recovery. Economic damages from the at-fault party’s insurance cover lost wages directly tied to the accident, while workers compensation benefits may apply if your accident occurred during work. Disability insurance and Social Security benefits (in some cases) provide additional income replacement, though these sources have specific eligibility requirements and may not fully cover your losses. The type of compensation you qualify for depends on your employment status, the nature of your injuries, and the circumstances of your accident. Exploring each option ensures you recover the full amount you’re owed rather than settling for partial compensation.

Where Your Lost Wages Compensation Actually Comes From

The at-fault party’s insurance company bears the primary responsibility for compensating your lost wages in California. When you file a claim, the insurance adjuster calculates your wage loss based on documentation you provide, though they often underestimate the figure or challenge the legitimacy of your claim. Insurance companies frequently argue that your treatment wasn’t intensive enough to justify time off work or that you could have worked around medical appointments. This is why documentation matters so intensely-pay stubs, tax returns, employer verification letters, and written work restrictions from your doctor create a paper trail that’s harder to dispute.

How Insurance Companies Challenge Your Wage-Loss Claim

Insurance adjusters question wage-loss claims in predictable ways. They may claim your treatment wasn’t necessary, that you could have worked despite your injuries, or that your lost income stems from market conditions rather than the accident itself. If you earned commissions, tips, or variable income, the insurance company may argue your pre-accident earnings were inflated or unsustainable. Strong documentation that directly links your missed work to the accident and your injuries is your best defense against these challenges. Pay stubs, tax returns, employer verification letters, and written work restrictions from your doctor all strengthen your position when negotiating with the insurance company.

Workers Compensation as an Additional Recovery Source

Workers compensation benefits apply if your accident happened while you were working or commuting to a job-related location. California’s workers comp system is no-fault, meaning you don’t need to prove the employer was negligent to receive benefits, but you generally cannot sue your employer for additional damages. However, if a third party caused the accident-a delivery driver, another vehicle, or a defective product-you can pursue a personal injury claim against that party while also collecting workers comp. Many accident victims overlook this opportunity and settle for workers comp alone, which typically covers only a portion of their actual losses.

Disability Insurance and Social Security Options

Disability insurance, whether short-term or long-term coverage through your employer or a private policy, provides income replacement during recovery but has specific eligibility requirements and waiting periods that vary by policy. Social Security Disability Insurance (SSDI) requires that you’ve worked long enough and paid into the system, plus you must prove your condition is severe enough to prevent substantial work for at least twelve months, making it a slower and more restrictive option than insurance-based compensation. These supplemental sources help fill gaps in your income, but they rarely cover your full losses. The reality is that most accident victims rely on the at-fault party’s insurance as their primary source of wage-loss recovery, making the strength of your claim and your willingness to negotiate or litigate the determining factors in what you ultimately recover. Understanding how to document your losses and present them effectively to the insurance company directly impacts the compensation you receive, which is why the next section focuses on the concrete steps you must take to protect and advance your wage-loss claim.

How to Recover Lost Wages in Santa Cruz County

Organize Your Financial Records Before Contacting Insurance

You must compile every document that proves your pre-accident income before you contact the insurance company. Collect pay stubs from the three months before your accident, your most recent W-2 forms, and tax returns from the past two years. Self-employed workers should obtain invoices from clients, bank deposit records showing payments received, and any contracts that outline work arrangements. Hourly workers need time sheets or attendance logs showing hours worked before the accident and specific dates missed due to medical appointments or recovery.

Request a written statement from your employer confirming how many days you used sick leave or vacation time and the value of those benefits. This documentation makes your claim difficult for insurance companies to dismiss. The sooner you compile these records, the stronger your position becomes when negotiating with the insurance company. Insurance adjusters scrutinize wage-loss claims more aggressively than other damages, so incomplete documentation gives them ammunition to reduce your settlement offer.

Submit Your Claim with Complete Documentation

You should report your claim to the insurance company with your documentation attached, but understand that the adjuster’s initial calculation will likely underestimate your losses. Insurance companies systematically lowball wage-loss claims because most injured people accept the first offer rather than push back. Do not accept the insurance company’s initial wage-loss figure without professional review, particularly if you earned commissions, tips, or variable income where your pre-accident earnings fluctuated. An attorney can identify gaps in the insurance company’s calculation, such as failure to account for lost commission income or undervaluing your future earning capacity. If your injuries are permanent or long-term, vocational professionals can quantify your reduced earning capacity in dollars, which insurance companies often ignore entirely in their initial offers.

Negotiate Your Settlement with Professional Representation

The negotiation phase determines whether you recover 50 percent of your actual losses or 90 percent, making professional representation essential for maximizing your recovery. Insurance adjusters expect most claimants to lack documentation or legal knowledge, so they anchor their offers low and wait to see if you’ll accept. When you present organized records (pay stubs, tax returns, employer verification letters, and written work restrictions from your doctor), you shift the negotiation dynamic in your favor.

An attorney communicates with the insurance company on your behalf, presents your losses in a format that’s harder to dispute, and knows when to escalate toward litigation if the insurer refuses a fair settlement. For accident victims in Santa Cruz County, having experienced legal representation transforms a wage-loss claim from a one-sided negotiation into a credible demand backed by documentation and legal leverage.

Final Thoughts

California law protects your right to recover lost wages after an accident caused by someone else’s negligence. Your compensation covers the income you missed during recovery, the benefits you depleted, and the earning capacity you lost if your injuries are permanent. The strength of your lost wages accident claim depends entirely on how thoroughly you document your pre-accident income and the work you missed.

Start by gathering pay stubs, W-2 forms, and tax returns from before your accident. If you’re self-employed, collect invoices, bank deposits, and client contracts that show your typical earnings. Request written statements from your employer confirming sick leave or vacation time used for medical treatment, and obtain clear work restrictions from your doctor that specify what tasks you cannot perform. These documents form the foundation of your wage-loss claim and make it harder for insurance companies to dispute your losses.

The insurance company will likely underestimate your wage-loss claim in their initial offer, particularly if you earned commissions, variable income, or worked for yourself. Do not accept the first offer without professional review, especially if your injuries affect your long-term earning ability. Contact Schaar & Silva LLP for a free case review-the sooner you act, the stronger your claim becomes.