A car accident in Santa Cruz County can leave you facing medical bills, lost wages, and vehicle repairs that far exceed what the at-fault driver’s insurance will cover. Underinsured motorist coverage fills that gap, protecting you when someone else’s liability limits aren’t enough.

At Schaar & Silva LLP, we help accident victims understand their rights and recover the compensation they deserve. This guide walks you through what underinsured motorist Santa Cruz coverage means and how to protect yourself.

What Underinsured Motorist Coverage Actually Does

How Underinsured Motorist Coverage Works

Underinsured motorist coverage activates when the at-fault driver’s liability insurance falls short of your actual damages. California law requires this coverage on every auto policy unless you sign a specific written waiver, according to California Insurance Code section 11580.2. In practice, if another driver causes a crash and their liability limits are $30,000 but your medical bills, lost wages, and pain and suffering total $75,000, your underinsured motorist coverage fills that $45,000 gap, up to your policy limits. The coverage applies to you as the named insured, your household relatives, and anyone injured in your vehicle. California uses pure comparative negligence, which means you can recover damages even if you’re partially at fault, as long as you’re not more than 50% responsible. This protection matters because it safeguards your recovery even in complex fault situations.

Setting Your Coverage Limits Appropriately

Your underinsured motorist limits must equal your uninsured motorist limits, yet many people set these too low at California’s minimum of $30,000 per person and $60,000 per accident. Santa Cruz County medical costs and vehicle repair expenses can quickly exceed state minimums, so aligning your underinsured motorist limits with your liability coverage makes financial sense. Try setting limits at $100,000 per person if your financial situation allows, since serious injuries often generate damages well beyond the state minimum.

The Real Gap Between Damages and Coverage

The gap between actual damages and insurance coverage appears immediately after a serious accident. In Santa Cruz County, about 15% of drivers lack insurance entirely, according to the California Department of Insurance, and many others carry minimal liability limits. A single serious injury can generate $50,000 to $150,000 in medical expenses alone, yet the at-fault driver might carry only $15,000 in liability coverage. Vehicle repairs in Santa Cruz run high, with collision damage often exceeding $15,000 for newer vehicles. Lost wages compound the problem, especially if you miss weeks or months of work during recovery. Pain and suffering damages reflect your physical and emotional injury and can be substantial, though they depend on injury severity and medical documentation. Without underinsured motorist coverage, you would absorb these costs yourself or pursue a lawsuit against the at-fault driver personally, which rarely recovers anything if they lack assets.

Why Santa Cruz Drivers Face Elevated Risk

This coverage exists specifically because liability limits often fall short of real-world damages. Santa Cruz drivers face elevated risk from hit-and-run incidents and bicycle crashes, which ranked third statewide for bicycle-involved incidents according to the California Office of Traffic Safety. Understanding your underinsured motorist protection becomes essential when you recognize these local hazards and the financial exposure they create.

Common Scenarios Where Underinsured Motorist Coverage Applies

When the At-Fault Driver Carries Minimal Liability Limits

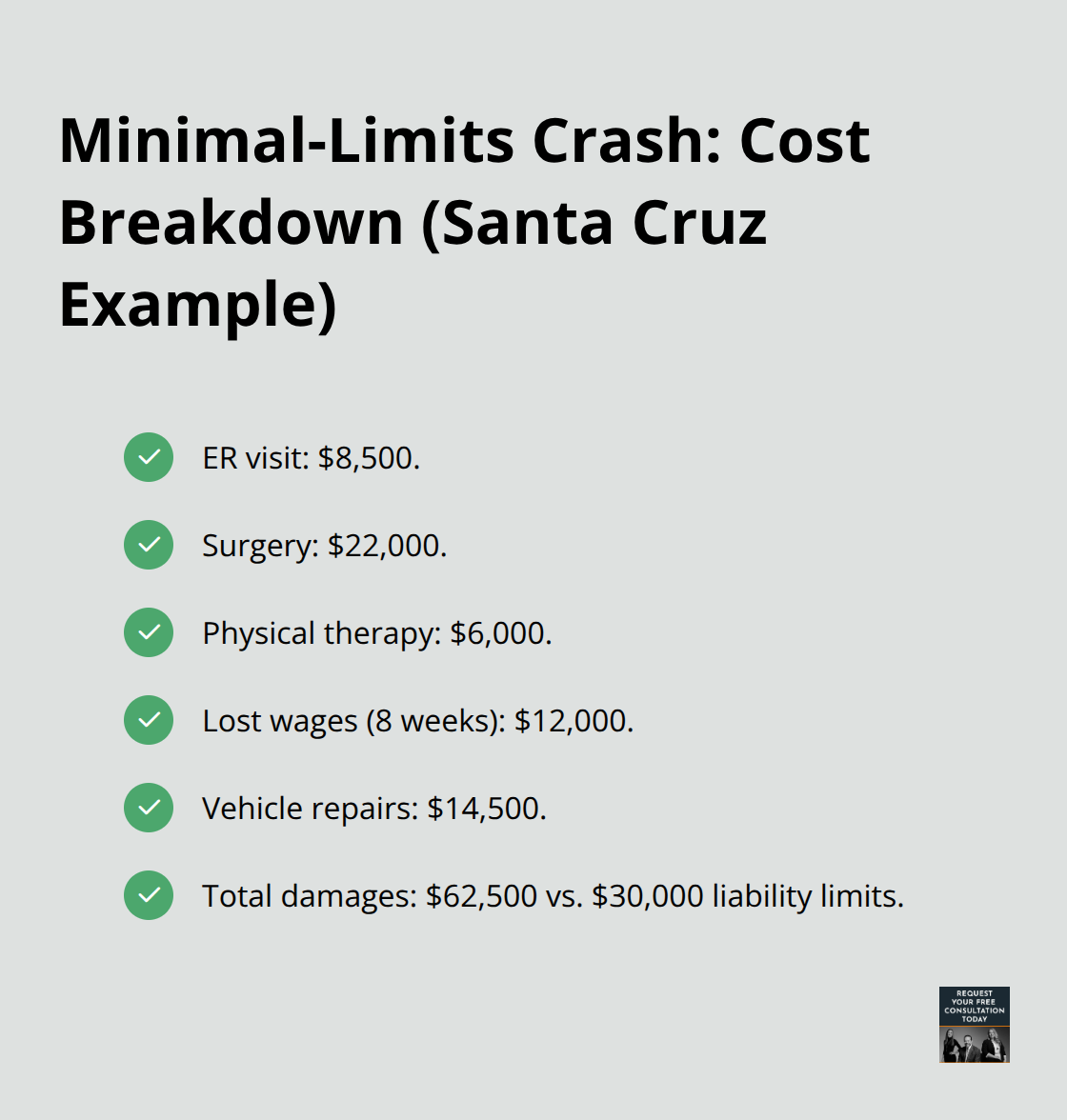

A driver hits your car at an intersection in Santa Cruz, and police arrive within minutes. The at-fault driver carries $30,000 in liability coverage, which sounds reasonable until you tally your actual losses. Your emergency room visit costs $8,500, surgery runs $22,000, physical therapy will be $6,000, and you miss eight weeks of work totaling $12,000 in lost wages. Your vehicle repair estimate is $14,500. That’s $62,500 in real damages against a $30,000 liability policy. This scenario plays out constantly in Santa Cruz County because many drivers carry minimal liability limits despite California’s rising medical and repair costs.

Your underinsured motorist coverage activates immediately once the at-fault driver’s liability limits are exhausted, covering the $32,500 gap up to your policy limits. California Insurance Code section 11580.2 requires insurers to offer this protection, and the coverage applies regardless of whether you’re partially at fault under California’s pure comparative negligence rule.

Multiple Injuries and Stacked Damages

Multiple serious injuries amplify this gap dramatically. A crash involving two passengers, the driver, and a pedestrian can generate $150,000 to $300,000 in combined medical expenses alone, yet the at-fault driver might carry only $60,000 in liability coverage. Each injured person’s medical bills, lost wages, and pain and suffering claims compete for the same limited liability pool. The at-fault driver’s $60,000 coverage splits among all claimants, leaving substantial shortfalls that your underinsured motorist coverage must address. Serious injuries-those requiring surgery, hospitalization, or long-term therapy-create particularly large gaps between available liability coverage and actual damages.

Hit-and-Run Incidents in Santa Cruz County

Hit-and-run incidents in Santa Cruz County present a different but equally serious problem. The California Office of Traffic Safety reported 13 hit-and-run crashes in Santa Cruz County during 2021, and many hit-and-run drivers carry no insurance whatsoever. In these situations, your uninsured motorist coverage handles the claim first, but if your damages exceed your uninsured motorist limits, your underinsured motorist coverage provides an additional safety net. The key difference is timing: underinsured motorist coverage activates after the other driver’s liability limits are exhausted, while uninsured motorist coverage applies when there is no other driver’s coverage to tap. Both coverages require you to exhaust the at-fault party’s liability before accessing your own protection, and California law gives you up to two years from the accident date to file a claim or start arbitration, though filing within 30 days improves approval chances by roughly 20 percent according to the California Department of Insurance.

Understanding these scenarios helps you recognize when your underinsured motorist coverage becomes your lifeline. The next section walks you through the specific steps you must take immediately after an accident to protect your claim and maximize your recovery.

What to Do Right After an Underinsured Motorist Accident

Immediate Actions at the Scene

The first hours after a crash determine whether your underinsured motorist claim succeeds or fails. Stop safely and call 911 if anyone is injured, then move to a vehicle to a safe location if possible. Photos and video at the scene capture vehicle damage, road conditions, traffic signs, and the overall scene from multiple angles-this documentation strengthens your claim significantly. Exchange full information with the other driver: name, address, driver’s license number, license plate, vehicle identification number, and insurance details. Collect contact information from at least two witnesses if possible, as witness statements decisively influence fault determinations and claim outcomes. Avoid admitting fault at the scene and refuse to sign any documents promising to pay or accepting fault.

Police Report and Initial Notification

File a police report with the Santa Cruz Police Department within 10 days as required by California law, since a police report provides critical documentation that strengthens your underinsured motorist claim. The police fault determination helps insurers, though carriers perform their own investigations, so your evidence matters significantly. Notify your insurance company within 24 hours, ideally sooner, since prompt notice improves claim approval chances by roughly 20 percent according to the California Department of Insurance. The California Department of Insurance requires insurers to acknowledge claims within 15 days and complete investigations within 15 days, so timely action protects your rights.

Medical Evaluation and Documentation

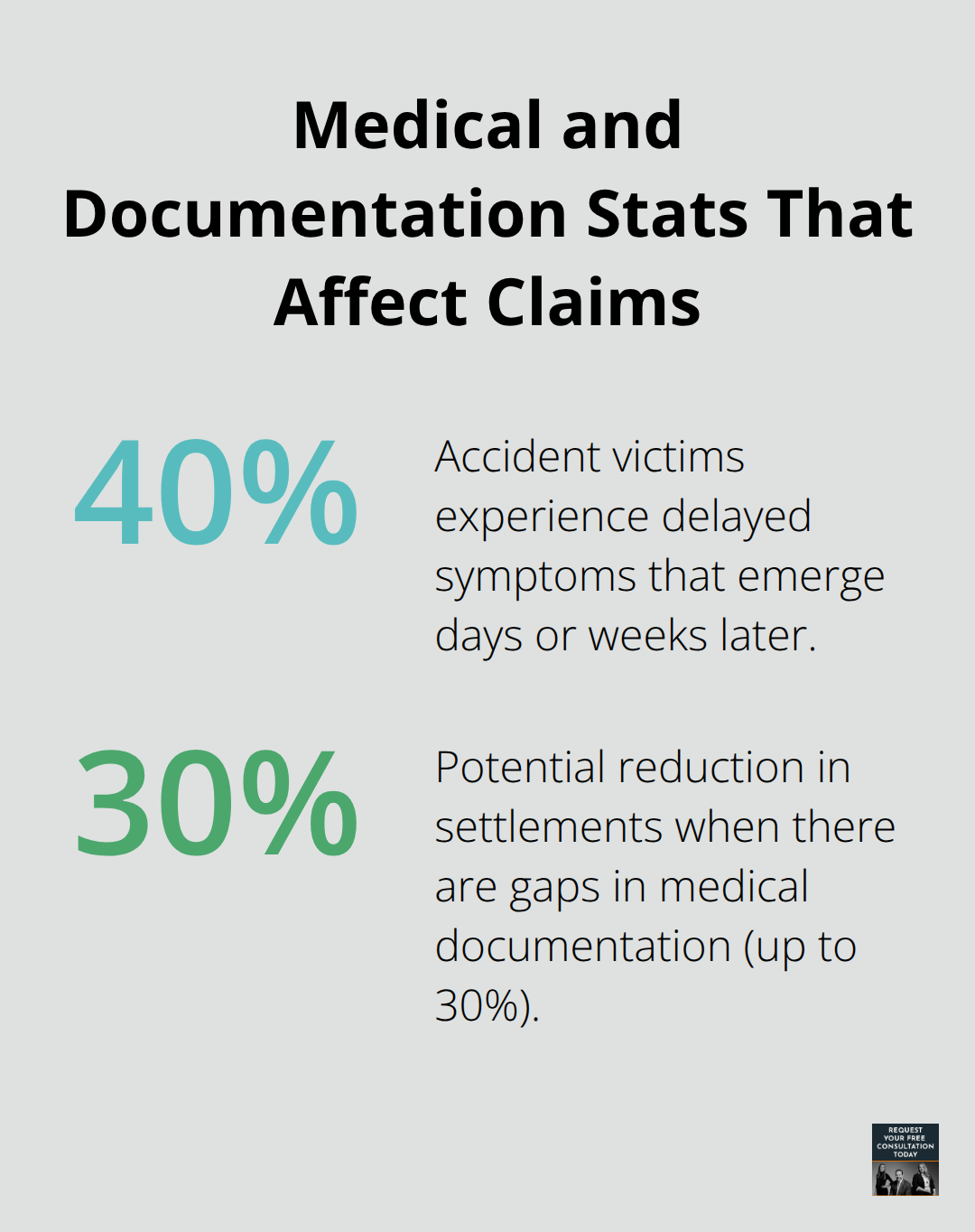

Seek medical evaluation immediately even if you feel fine, because about 40 percent of accident victims experience delayed symptoms that emerge days or weeks later. Document every medical visit, treatment, and expense with receipts and explanations of benefits, as gaps in medical documentation can reduce settlements by up to 30 percent. Gather medical bills, wage-loss information showing time missed from work, and vehicle repair estimates from local Santa Cruz shops.

Your insurer may request a recorded statement and may require a medical examination, so prepare organized documentation of all injuries and expenses.

Filing Your Underinsured Motorist Claim

File your underinsured motorist claim within 30 days to improve approval chances, though California law allows up to two years from the accident date. Medical lien services can facilitate bill payment while your case resolves, allowing you to focus on recovery rather than creditor calls. We at Schaar & Silva LLP can help direct you to these services and guide you through the claim process.

Final Thoughts

Underinsured motorist Santa Cruz coverage protects you when the at-fault driver’s liability limits fall short of your actual damages. Santa Cruz County faces real hazards-hit-and-run incidents, bicycle crashes, and drivers carrying minimal liability coverage-that can leave you financially exposed without this protection. Setting your limits to match your liability coverage rather than accepting California’s minimum of $30,000 per person gives you meaningful protection against the high medical and repair costs you face locally.

The claim process requires immediate action and thorough documentation. Filing within 30 days improves your approval chances significantly, and organizing medical records, wage information, and repair estimates strengthens your position against insurer resistance. Many insurers initially offer settlements below what your damages warrant, so strong evidence and organized documentation become your tools for pushing back against lowball offers.

Legal support makes a measurable difference in underinsured motorist claims. We at Schaar & Silva LLP help accident victims navigate the claim process, connect you with medical lien services to manage bills during recovery, and evaluate property damage fairly. Contact Schaar & Silva LLP to discuss your options and receive a free initial consultation with no obligation.