A car or truck accident in Santa Cruz County leaves you dealing with more than just injuries-property damage claims add stress and confusion to an already difficult situation.

We at Schaar & Silva LLP understand that navigating property damage valuation and insurance claims feels overwhelming when you’re trying to recover. This guide walks you through how damage gets assessed, what your claim requires, and where to find help locally.

How Property Damage Gets Valued After an Accident

Understanding the Assessment Process

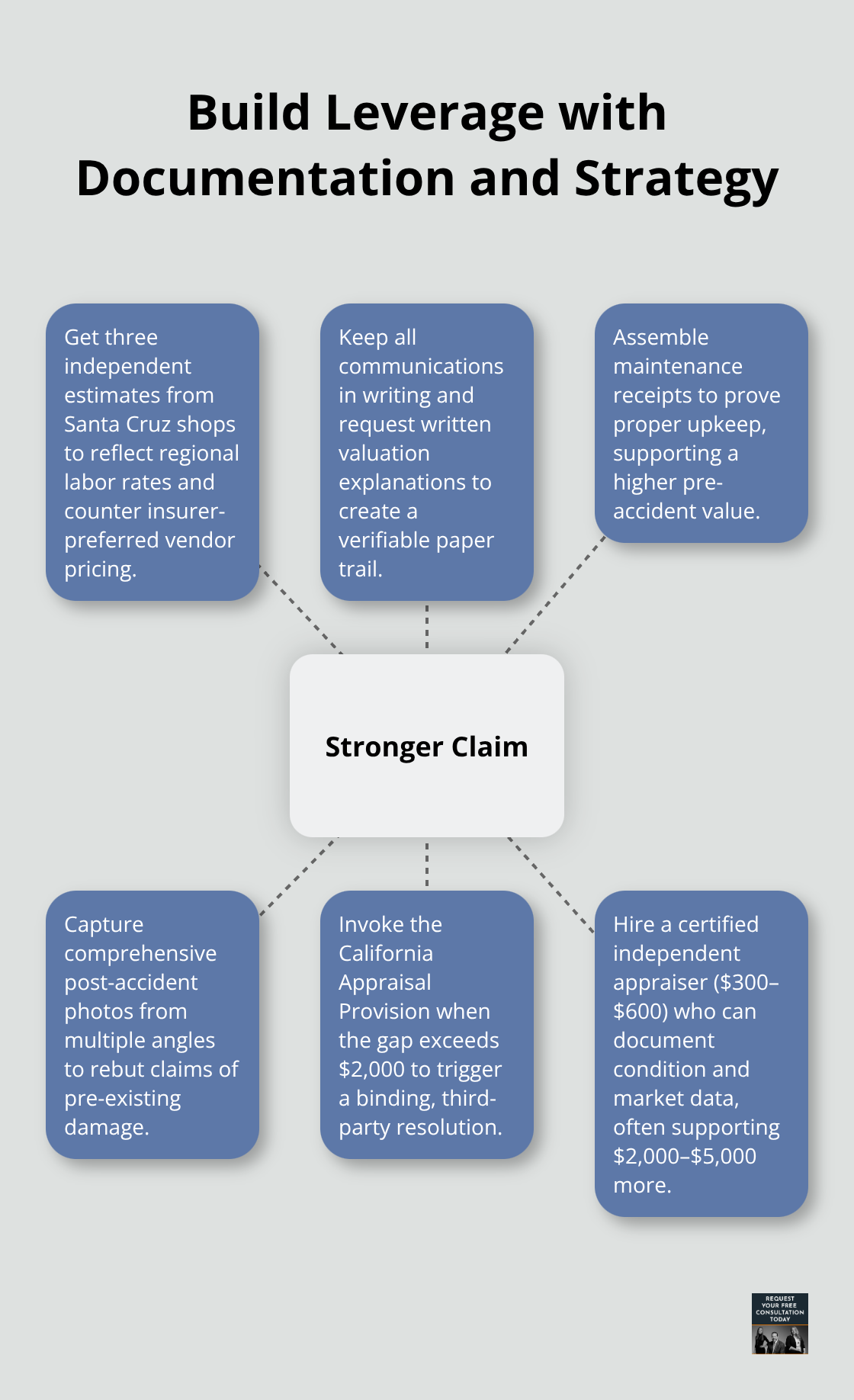

Insurance adjusters in Santa Cruz County don’t use a single method to value your vehicle-they layer multiple approaches, and understanding each one shifts the negotiating power in your favor. The assessment process starts when the adjuster inspects your vehicle in person or, in some cases, relies on photos you submit. During this inspection, they document the extent of damage, note the vehicle’s condition before the accident, and cross-reference repair estimates against national databases like NADA Guides. However, NADA valuations often underestimate local repair costs in Santa Cruz County, where regional labor rates and parts availability typically run 15–25% higher than national averages. A vehicle valued at $15,000 on NADA might actually cost $18,000 or more to repair locally, which is why you must obtain three independent estimates from Santa Cruz shops-not the insurer’s preferred vendors.

What Inspectors Look For

Inspectors focus on frame damage, suspension integrity, electrical systems, and hidden issues like water intrusion or rust, since these can add $5,000–$10,000 to the final repair bill if discovered after work begins. Photographs taken immediately after the accident from multiple angles, combined with your maintenance records, directly counter the adjuster’s assessment and prevent them from claiming pre-existing damage or poor upkeep. You strengthen your position by collecting receipts for oil changes, brake service, and other maintenance-this proof of proper care supports your claimed vehicle value.

Valuation Methods Used in Santa Cruz County

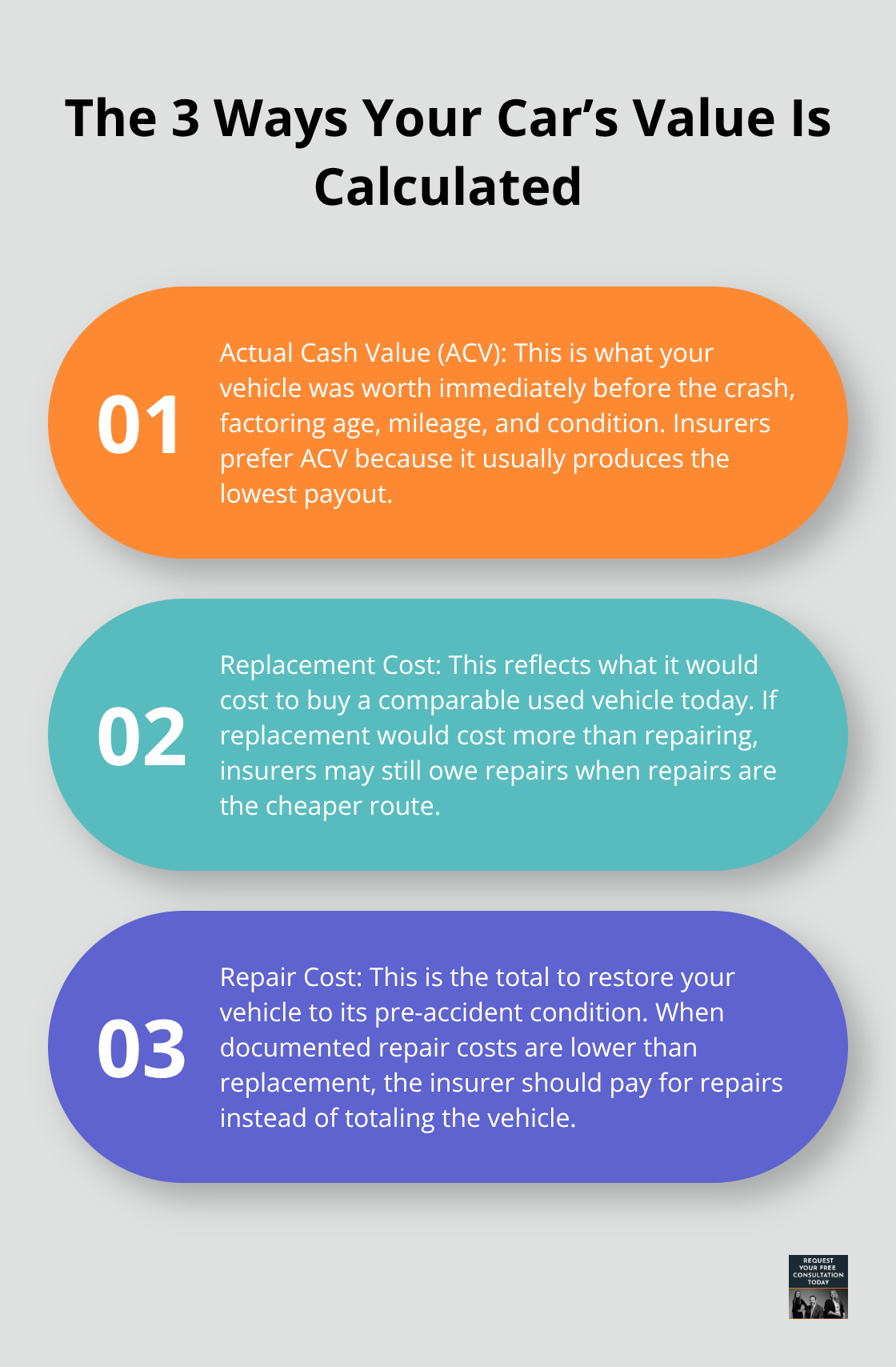

The valuation itself relies on one of three methods: actual cash value (what your vehicle was worth immediately before impact), replacement cost (what it would cost to buy an identical used vehicle), or repair cost (the total bill to restore your vehicle to pre-accident condition). Most Santa Cruz adjusters default to actual cash value because it’s the lowest figure, but if repairs are cheaper than replacing the vehicle, the insurer must pay for repairs. A certified independent appraiser becomes invaluable here-for $300–$600, they document your vehicle’s pre-crash condition and current market data, often justifying $2,000–$5,000 in additional recovery. California law does not require insurers to rely solely on NADA, which means your multiple local estimates carry significant weight in negotiation.

Negotiating Your Valuation

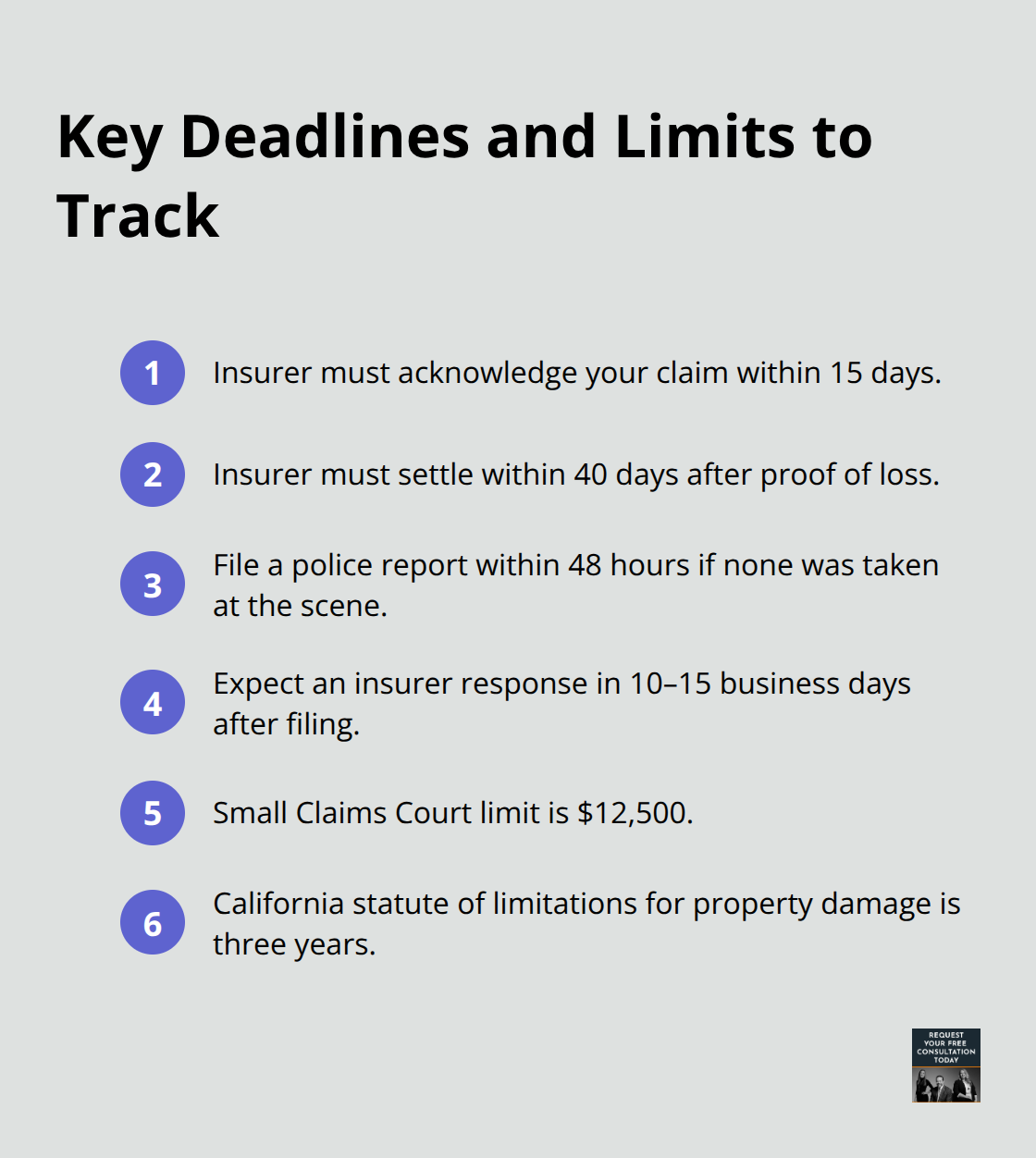

Keep all communication with adjusters in writing via email to maintain a clear record, and request a written explanation of how they calculated both the pre-accident value and damage estimate. If the gap between their offer and your three independent estimates exceeds $2,000, the California Appraisal Provision offers a formal resolution path where both sides select appraisers and an umpire’s binding decision settles the dispute. Insurers typically acknowledge claims within 15 days and must settle within 40 days after proof of loss, so you should document every step and track these timelines closely. Once you have your valuation in hand, the next phase involves filing your claim and gathering the documentation that transforms a low initial offer into fair compensation.

Filing a Property Damage Claim in Santa Cruz County

Act Fast in the First 48 Hours

The first 48 hours after an accident determine whether your claim succeeds or fails. Photograph everything immediately from multiple angles-the vehicle damage, the accident scene, road conditions, and any visible injuries-because these images become your strongest defense against adjuster skepticism.

File a police report within 48 hours if one wasn’t completed at the scene; obtain the officer’s name, badge number, and report number, since police documentation carries significant weight in settlement negotiations. Contact your insurance company without delay, but do not accept any initial settlement offer. Insurers in Santa Cruz County typically respond within 10–15 business days after filing, which gives you a narrow window to gather independent estimates before they lock in a low valuation.

Gather Documentation That Counters Low Offers

Collect repair estimates from at least three Santa Cruz shops-not the insurer’s preferred vendors-because local labor rates run 15–25% higher than national databases account for, and these estimates directly counter the adjuster’s figures. Gather maintenance receipts for oil changes, brake service, and other upkeep to prove you maintained your vehicle properly, which supports your claimed pre-accident value. Organize all documentation (photos, police report, estimates, receipts, and proof of ownership) into a single file and present it in writing to the adjuster. This organized approach shifts negotiations away from phone calls and emotional appeals toward documented facts that adjusters cannot easily dismiss.

Negotiate with Written Records and Clear Expectations

Initial settlement offers typically run 30–40% below actual repair costs, so expect the first number to disappoint. Request a written explanation of how the adjuster calculated both your vehicle’s pre-accident value and the damage estimate, then compare their figures against your three independent estimates. Keep all communication in writing via email-never rely on phone conversations-because written records protect you if the claim escalates or you need to file a complaint with the California Department of Insurance. If negotiations stall and the gap between the adjuster’s offer and your estimates exceeds $2,000, invoke the California Appraisal Provision, where both sides select appraisers and an umpire’s binding decision resolves the valuation dispute.

Know Your Rights and Timelines

California law requires insurers to acknowledge claims within 15 days and settle within 40 days after proof of loss, so track these timelines and reference them when pushing for resolution. If the insurer denies your claim or underpays despite strong documentation, the California Department of Insurance accepts complaints about suspected bad-faith practices. For complex claims involving substantial damage or unclear liability, consulting legal representation can determine whether pursuing additional recovery through Small Claims Court or civil litigation makes financial sense given your specific circumstances. Once you understand your claim options and have documented your position, you’ll want to know what local resources and support are available to help you move forward.

Local Resources and Support for Property Damage in Santa Cruz County

Finding Qualified Repair Shops Near You

Santa Cruz County offers specific resources that most accident victims overlook, and knowing where to turn makes the difference between settling for less and recovering what you’re owed. Repair shops in Santa Cruz typically charge 15–25% more than national labor rate databases reflect, which means finding a local shop that understands regional pricing becomes your first priority. Start by contacting three independent repair facilities in Santa Cruz-shops certified by AAA or the National Institute for Automotive Service Excellence-and request written estimates that break down labor, parts, and overhead separately. These shops can identify hidden damage during their inspection, such as frame misalignment or suspension failure, which adjusters often miss and which can add $5,000–$10,000 to your final bill. Ask each shop for references from previous accident claims and confirm they will stand behind their work under California’s repair shop protection law, which requires insurers to honor repairs performed at your chosen facility if they meet accepted trade standards.

Medical Lien Services for Related Expenses

Medical providers in Santa Cruz County frequently work with lien arrangements, meaning they defer payment until your settlement resolves, which prevents you from paying out-of-pocket for treatment while fighting your property damage claim. Contact your medical provider’s billing department directly and ask whether they accept medical liens; if they do, document this arrangement in writing and include it in your claim file. This approach protects your cash flow and demonstrates to the adjuster that you manage expenses responsibly.

Legal Assistance and Claim Support

When your claim stalls or the insurer’s offer falls significantly short of your documented repair costs, legal assistance becomes the practical next step. Small Claims Court in Santa Cruz County handles claims up to $12,500 with filing fees around $30–$100 and hearings at the Watsonville Courthouse on Thursdays. You can now file electronically through the Odyssey Guide and File system, which streamlines the process considerably. For claims exceeding $12,500 or involving substantial complexity, civil litigation allows you to recover not only repair costs but also rental car expenses and diminished value-damages that insurers often refuse to acknowledge in settlement negotiations. California’s three-year statute of limitations gives you time to pursue this path, but the sooner you gather documentation and assess your position, the stronger your leverage. If the insurer denies your claim outright or exhibits bad-faith practices despite your thorough documentation, file a complaint with the California Department of Insurance, which investigates suspected violations and can pressure resolution. The combination of independent repair estimates, organized documentation, and willingness to pursue formal remedies through appraisal or litigation shifts negotiations decisively in your favor and prevents you from accepting an underpayment that leaves you responsible for the gap.

Final Thoughts

Property damage Santa Cruz claims succeed when you act decisively in the first 48 hours and build a documented case that counters low insurance offers. Photograph damage from multiple angles, file a police report, contact your insurer, and collect three independent repair estimates from local shops that reflect regional labor rates. The gap between initial offers and actual repair costs typically reaches $2,000–$5,000, and your organized documentation closes that gap by presenting facts adjusters cannot dismiss.

When negotiations stall despite your strong file, the California Appraisal Provision and Small Claims Court offer formal resolution paths without extensive legal involvement. For claims exceeding $12,500 or involving substantial complexity, civil litigation recovers rental car costs and diminished value that settlement talks often exclude. If the insurer denies your claim or underpays despite thorough documentation, file a complaint with the California Department of Insurance to pressure resolution.

We at Schaar & Silva LLP help accident victims evaluate property damage claims and navigate toward fair recovery. Our team reviews your documentation, assesses your claim’s value, and guides you through appraisal or litigation if necessary. Contact us to discuss your specific situation and determine the best approach for your claim.