A car crash can turn your life upside down in seconds. Medical bills pile up, your vehicle needs repairs, and you’re dealing with pain and stress while trying to navigate the claims process.

We at Schaar & Silva LLP know that car crash injury claims in California involve specific rules and deadlines that most people don’t understand. This guide walks you through the legal framework, shows you what evidence matters most, and explains how to handle insurance companies effectively.

How California’s Fault System Affects Your Claim

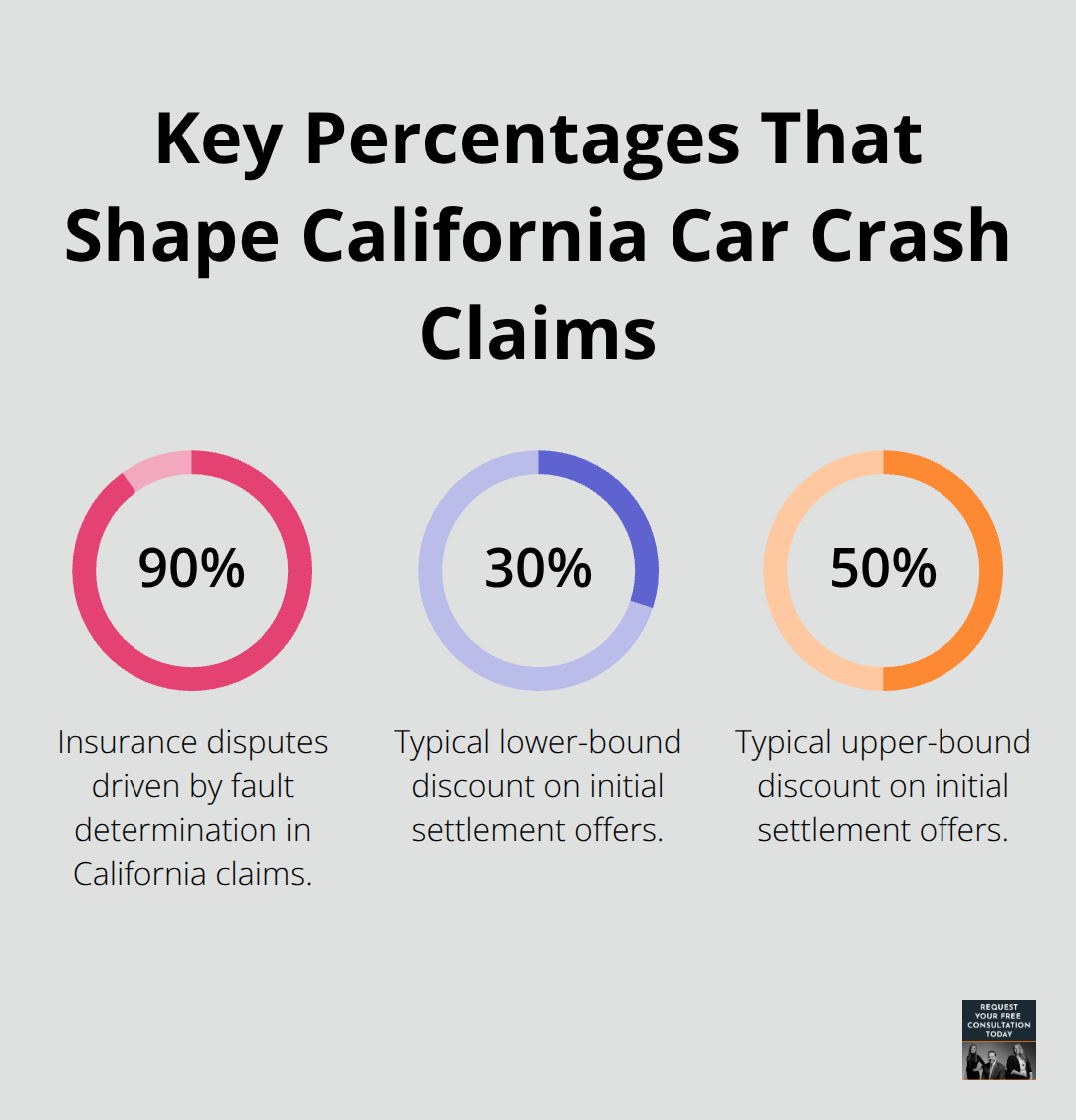

A car crash can turn your life upside down in seconds. California operates under a fault-based insurance system, meaning the driver who caused the crash pays for damages. This matters because it shapes everything about your claim. The state also applies comparative negligence rules, so if you bear partial responsibility for the crash, your recovery gets reduced by your percentage of fault. More than 200,000 car accidents involving injuries occur in California each year, and fault determination causes roughly 90% of insurance disputes. You need to understand this upfront because your entire recovery depends on proving fault clearly and convincingly.

Establishing Fault Requires Solid Evidence

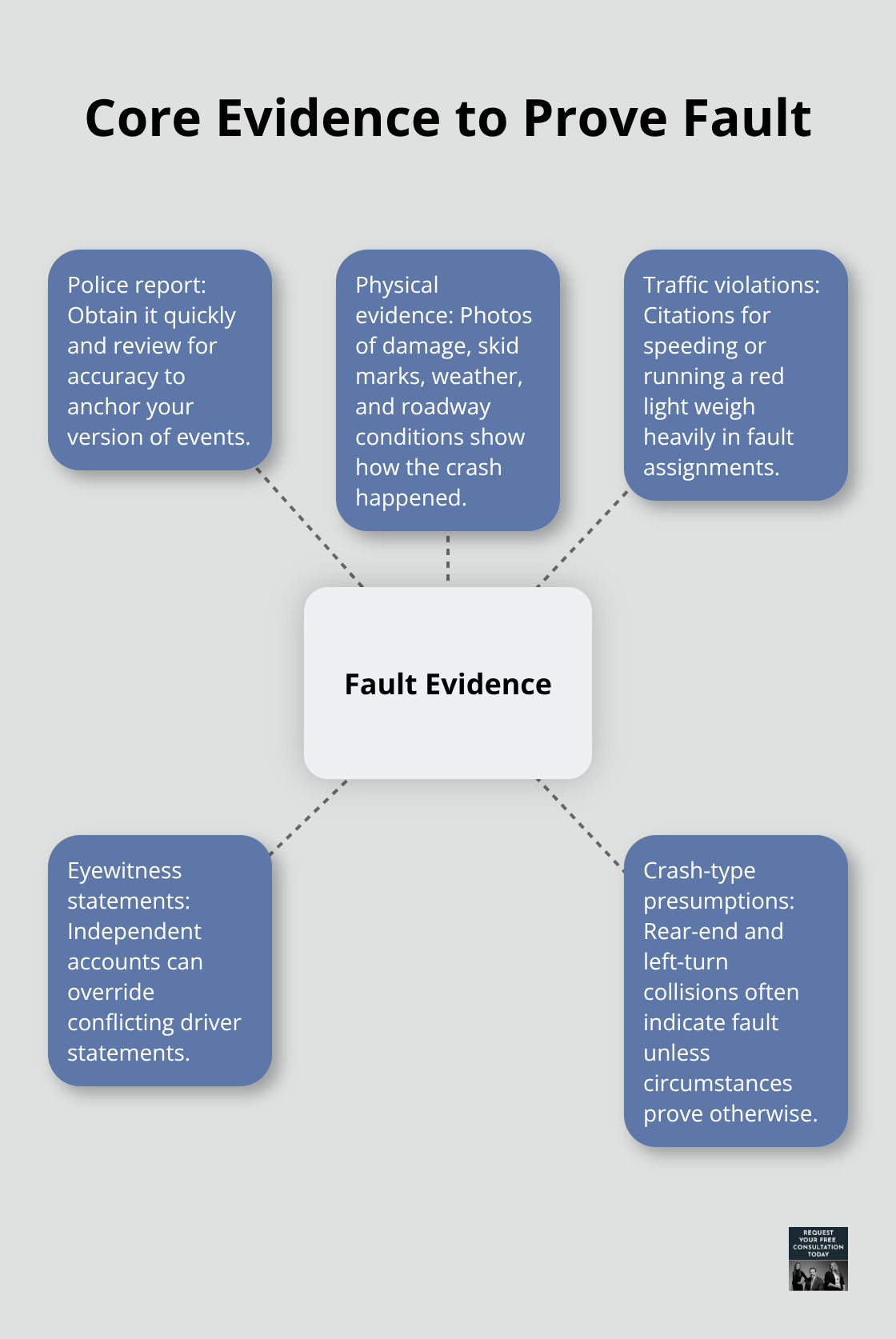

Fault determination starts with the police report, which serves as your foundation. Request this report immediately after the crash and review it carefully for accuracy. Physical evidence from the scene matters enormously: vehicle damage patterns, skid marks, weather conditions, and road layout all tell the story of what happened. Traffic violations are decisive-running a red light or speeding significantly influences fault assignments. Rear-end crashes almost always assign fault to the following driver, while left-turn collisions typically fault the turning driver unless circumstances prove otherwise. Insurance adjusters investigate these factors, but their conclusions aren’t final if you have stronger evidence.

Eyewitness accounts provide independent perspectives that can override conflicting driver statements. Santa Cruz County experienced 147 total fatal and injury crashes in 2021, with 19 speed-related crashes and 13 hit-and-run incidents, underscoring how common fault disputes become. You should photograph and document the crash scene thoroughly, including road signs, traffic signals, lighting, and any visible damage. Gather witness contact information immediately-multiple independent witnesses strengthen your position significantly when you negotiate or dispute fault determinations.

Understanding Deadlines That Cannot Be Extended

California gives you two years from the crash date to file a personal injury lawsuit for injuries, but property damage claims allow three years. This deadline applies whether you are a driver, passenger, bicyclist, pedestrian, or motorcyclist. If the crash involved a government vehicle like a city bus or fire truck, you must file a notice of claim within six months (this stricter deadline catches many people off guard).

Minors have an advantage: the two-year clock does not start until they turn 18. Soft tissue injuries and other conditions sometimes are not immediately apparent, and the discovery rule may extend your deadline if the injury was not discoverable at the time of the crash. Missing these deadlines bars you from recovering damages permanently, making early action essential.

Calculating the Damages You Can Recover

You can recover economic damages like medical bills, lost wages, vehicle repairs, and rental car costs. Non-economic damages cover pain and suffering, emotional distress, and lost quality of life. California does not cap these damages in most cases, though the amount depends on injury severity and how well you document losses. Insurance adjusters will scrutinize your documentation, so you need to organize medical records, receipts, and wage statements carefully. The stronger your evidence of fault and the more thoroughly you support your damage claims, the better your negotiating position becomes when you face settlement discussions with insurance companies.

What Evidence Wins Insurance Disputes

The evidence you gather in the first hours and days after a crash determines whether you win or lose your claim. Insurance adjusters rely on documentation to make fault decisions, and weak evidence leads to reduced settlements or denials.

Medical Records Create the Foundation

Medical records establish an unbreakable link between the crash and your injuries. Visit a doctor immediately, even if you feel fine-soft tissue injuries often appear days later, and delayed treatment weakens your claim. Request copies of every medical record, imaging report, and treatment note from your providers. The California Department of Insurance requires insurers to respond within 15 days and decide claims within 40 days after you submit proof, so organized medical documentation speeds up your settlement.

Police Reports and Scene Documentation

Police reports carry significant weight because adjusters use them as the official account of what happened. Call 911 at the scene and request the officer’s name and badge number. When you receive the report, read it line by line for errors-incorrect descriptions of vehicle damage, wrong intersection details, or misquoted statements can hurt your position. If the report contains inaccuracies, contact the police department and request a correction or supplemental report.

Photographs and video evidence from the scene show exactly how the crash occurred. Photograph vehicle damage from multiple angles, road conditions, traffic signals, street signs, weather, lighting, and any skid marks or debris. In Santa Cruz County, nighttime crashes numbered 16 in 2021 according to the California Office of Traffic Safety, so lighting conditions matter for establishing visibility and fault.

Witness Statements Provide Credibility

Witness statements provide the credibility that insurance companies demand. Collect full names, phone numbers, email addresses, and home addresses from anyone who saw the crash. Independent witnesses carry more weight than friends or family members. Request that witnesses write down what they saw while memory is fresh, or record their verbal account with their permission. Multiple unrelated witnesses make it nearly impossible for an adjuster to deny your version of events.

Organizing and Protecting Your Documentation

Insurance adjusters scrutinize every detail, so organize all documentation in a single folder with clear labels and dates. Keep originals and provide copies only to your insurer and attorney. Do not discuss the accident with anyone except your doctor, attorney, and insurer-statements to others can be used against you later. If you disagree with the insurance company’s investigation or fault determination, submit new evidence or witness statements in writing.

The appraisal process allows you to challenge settlement amounts if the insurer’s valuation of your vehicle or damages differs significantly from repair estimates. Two appraisers review the evidence, select an umpire if they disagree, and the umpire’s decision becomes binding. Each side pays its own appraiser, so the cost is reasonable when the dispute amount is substantial. Strong documentation gives you leverage when you face settlement negotiations with insurance companies, and understanding how to present this evidence effectively shapes your outcome in the next phase of your claim.

Negotiating with Insurance Companies

How Insurance Companies Calculate Settlement Offers

Insurance adjusters apply a formula-based approach to calculate settlement offers, and understanding this process gives you leverage during negotiations. They start with your medical expenses, add a multiplier ranging from 1.5 to 4 times that amount for pain and suffering depending on injury severity, then subtract your deductible and any comparative negligence percentage assigned to you. The California Department of Insurance requires insurers to acknowledge your claim within 15 days, respond to requests within 15 days, and make decisions on settlement within 40 days after you submit proof. This timeline pressure works in your favor if you have organized documentation ready to submit immediately. Initial offers typically fall 30 to 50 percent below what the insurer will ultimately pay, so treat the first number as a starting point rather than a final decision. Adjusters count on you accepting quickly out of financial desperation, which is why they frontload settlement discussions with low figures. Your documented evidence directly influences the multiplier they apply to your medical bills. A well-organized medical file with clear treatment progression, imaging reports, and specialist notes pushes your multiplier upward. Conversely, gaps in treatment or missing documentation lower it significantly. Insurance companies also use delay tactics intentionally, hoping you will accept less money rather than wait longer for resolution. If your claim involves a government vehicle like a city bus or fire truck, the insurer operates under even stricter timelines and different procedural rules that require immediate attention.

Recognizing Common Insurance Company Tactics

Insurance adjusters employ specific tactics designed to minimize payouts, and recognizing these moves protects your claim. They may request unnecessary medical records or demand that you sign blanket authorizations that give them access to your entire medical history, not just crash-related treatment. Refuse blanket authorizations and provide only records directly related to your injuries. They frequently use recorded statements against you, so answer questions carefully and avoid elaborating beyond what they ask. Some adjusters suggest that your injuries were pre-existing or that you delayed seeking treatment to inflate your claim, which is why seeking medical attention immediately after a crash matters. They may also pressure you to accept a settlement before you fully understand the extent of your injuries, knowing that soft tissue injuries often worsen over weeks or months. Never accept an offer while you are still in active treatment or before you reach maximum medical improvement. Adjusters sometimes reference their own repair estimates that undervalue your vehicle damage, knowing most people lack the technical knowledge to challenge them. Request independent appraisals from certified mechanics if the insurer’s valuation seems low. If you disagree with the settlement amount offered, the appraisal process gives you a formal mechanism to challenge it. Two appraisers review the damage, select an umpire if they disagree, and the umpire’s decision becomes binding on both sides. Each party pays its own appraiser, making this process affordable when the disputed amount exceeds several hundred dollars. Adjusters count on you not knowing this right exists, so asserting it early signals that you understand the process and will not accept lowball offers without a fight.

Deciding When to Accept or Reject Settlement Offers

Accepting a settlement ends your right to pursue additional compensation, so the timing of that decision shapes your entire financial recovery. Reject an offer if you are still in active medical treatment, if your medical providers have not released you, or if you have not reached maximum medical improvement. Accepting while treating sends the message that your injuries were minor, which undermines your claim value. The insurer knows this psychology, which is why they push for early settlement. Reject offers that fail to account for future medical care your doctors indicate you will need. Chronic pain conditions, ongoing physical therapy, or recommended surgery should factor into your settlement value before you sign anything. If the offer does not cover your documented lost wages or if it undervalues your vehicle damage based on comparable repair estimates, rejection is warranted. Conversely, accepting becomes reasonable once your doctors confirm you have reached maximum medical improvement, all treatment is complete, and your medical records support the settlement amount offered. At that point, continuing to negotiate often yields minimal gains while delaying your recovery. An attorney can identify whether the multiplier applied to your medical expenses aligns with your injury severity and whether the calculation accounts for all recoverable damages.

Final Thoughts

Building a strong car crash injury claim in California requires you to act immediately after the crash. You must photograph the scene, collect witness contacts, request the police report, and document every medical visit from day one. You then organize this evidence systematically so you can present it clearly to insurance adjusters, and you understand that initial settlement offers rarely reflect your actual damages.

We at Schaar & Silva LLP work with Santa Cruz County residents who navigate car crash injury claims every day. We help you evaluate whether the insurance company’s settlement offer reflects your actual damages, connect you with medical lien services to manage bills while your case resolves, and address the legal complexity so you can focus on healing. Insurance company pressure and uncertainty about your rights create unnecessary stress when you should be recovering.

Contact Schaar & Silva LLP today for a consultation to discuss your specific situation and understand your options. We can identify whether your claim is positioned for maximum recovery and what your next steps should be.