A Santa Cruz uninsured motorist claim can mean the difference between covering your medical bills and facing financial hardship after an accident. California law requires insurers to offer UM coverage, yet many drivers don’t understand how it works or what they’re entitled to recover.

At Schaar & Silva LLP, we’ve helped countless Santa Cruz residents navigate these claims and secure the compensation they deserve. This guide walks you through the process step by step.

What Is Uninsured Motorist Coverage in Santa Cruz

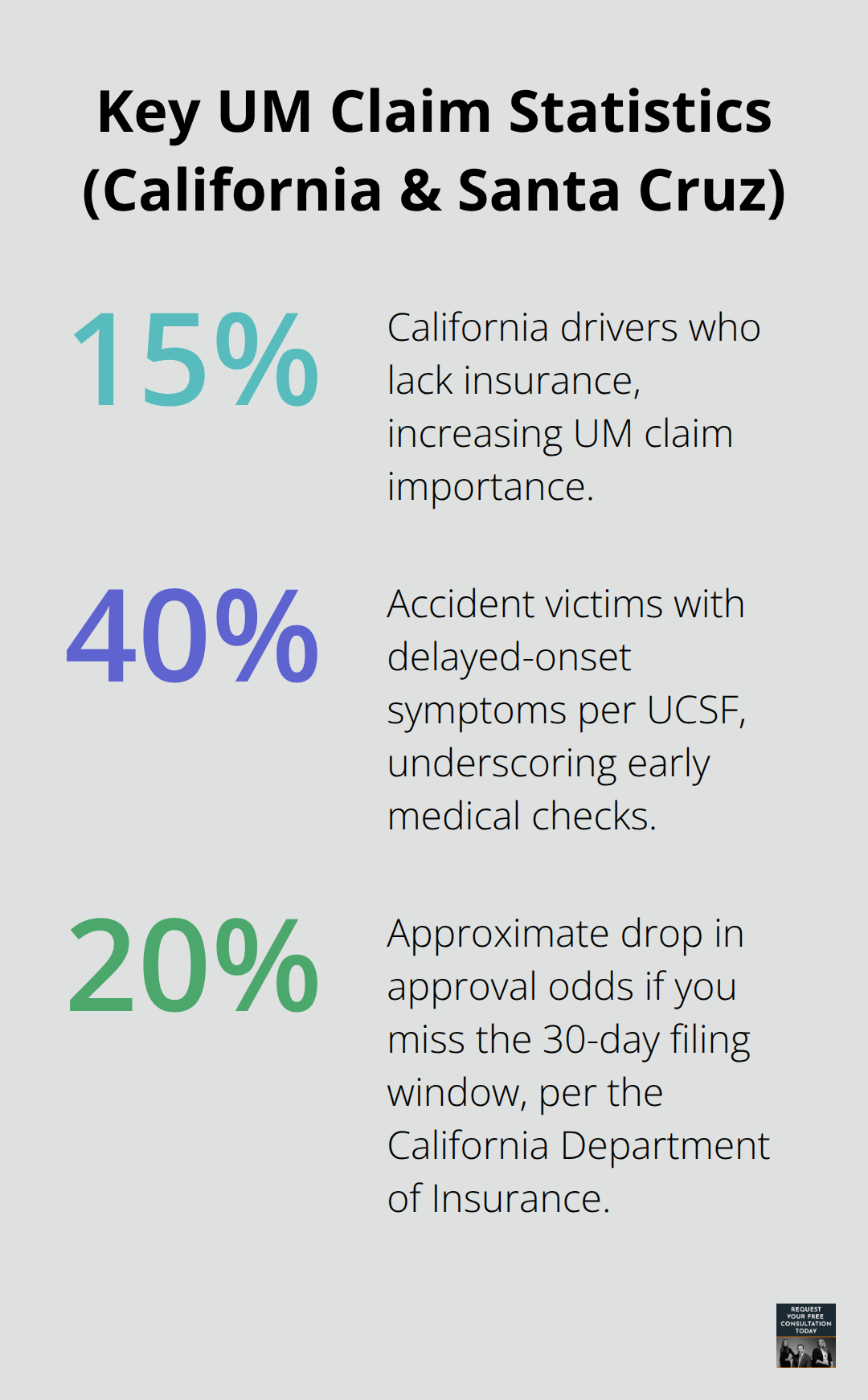

California law mandates that every auto insurer offer uninsured motorist coverage, though you can decline it in writing. About 15% of California drivers lack insurance, and Santa Cruz County experiences elevated hit-and-run incidents and bicycle-involved crashes, making UM coverage far more than a theoretical safety net. UM protects you when the at-fault driver carries no insurance or flees the scene, covering medical expenses, lost wages, pain and suffering, and vehicle damage up to your policy limits. The California Department of Insurance reports that UM is one of the cheapest auto coverages available, yet many Santa Cruz residents either skip it or fail to understand its scope. Underinsured motorist coverage, or UIM, activates when the responsible driver has some insurance but insufficient limits to cover your actual damages. For example, if your claim totals $50,000 and the at-fault driver carries only $15,000 in liability coverage, UIM bridges that gap up to your policy limits. UM and UIM typically share the same limits, so a 25/50 liability policy usually allows matching 25/50 UM and UIM protection. Property damage under UM generally caps around $3,500, so if your vehicle is worth more, collision coverage becomes essential backup protection.

UM Limits Must Match Your Liability Coverage

Set your UM limits equal to your liability limits to prevent a dangerous coverage gap that could leave you paying medical bills from your own pocket. Many Santa Cruz drivers mistakenly accept lower UM amounts than their liability coverage, creating a mismatch that leaves them underprotected. The California Department of Insurance emphasizes that aligning these limits ensures you have adequate financial protection if hit by an uninsured driver. Higher living costs in Santa Cruz County make robust UM coverage especially important for covering medical expenses and maintaining financial stability after an accident. When you file a UM claim, you pursue recovery through your own insurer rather than suing the uninsured driver directly, which simplifies the process but requires thorough documentation to succeed.

Common Errors That Weaken Your Claim

Declining UM coverage in writing is legally permissible but financially risky in Santa Cruz (given the prevalence of uninsured drivers and higher medical costs). Wait too long to seek medical evaluation, and insurers will argue your injuries weren’t serious, even though up to 40% of accident victims experience delayed-onset symptoms according to UCSF Medical Center research. Fail to file your claim within 30 days of the accident, and approval odds drop by approximately 20%, per the California Department of Insurance. At the scene, many victims make critical mistakes by signing statements that admit fault or accepting settlement offers without legal review (which insurers later use to minimize payouts). Document the accident thoroughly at the scene by collecting the other driver’s details, obtaining witness contact information, and photographing damage and injuries-this creates the foundation for a successful claim that settles roughly 40% faster with comprehensive documentation.

Why Professional Guidance Matters Now

The gap between what you think you’re owed and what your insurer offers to pay often widens without proper legal support. Insurance adjusters employ tactics designed to reduce payouts, and navigating policy language alone leaves most accident victims at a disadvantage. When you work with experienced legal counsel, you gain someone who understands Santa Cruz County’s specific accident patterns and knows how insurers operate locally. The team at Schaar & Silva LLP offers medical bill assistance, property damage claim evaluation, and connections to specialists who address the emotional toll of accidents-services that help you focus on recovery while we handle the legal complexities.

Understanding your UM coverage is only the first step. The real challenge begins when you file your claim and face the insurance company’s investigation and settlement process.

How to File Your UM Claim in Santa Cruz

Act Immediately After the Accident

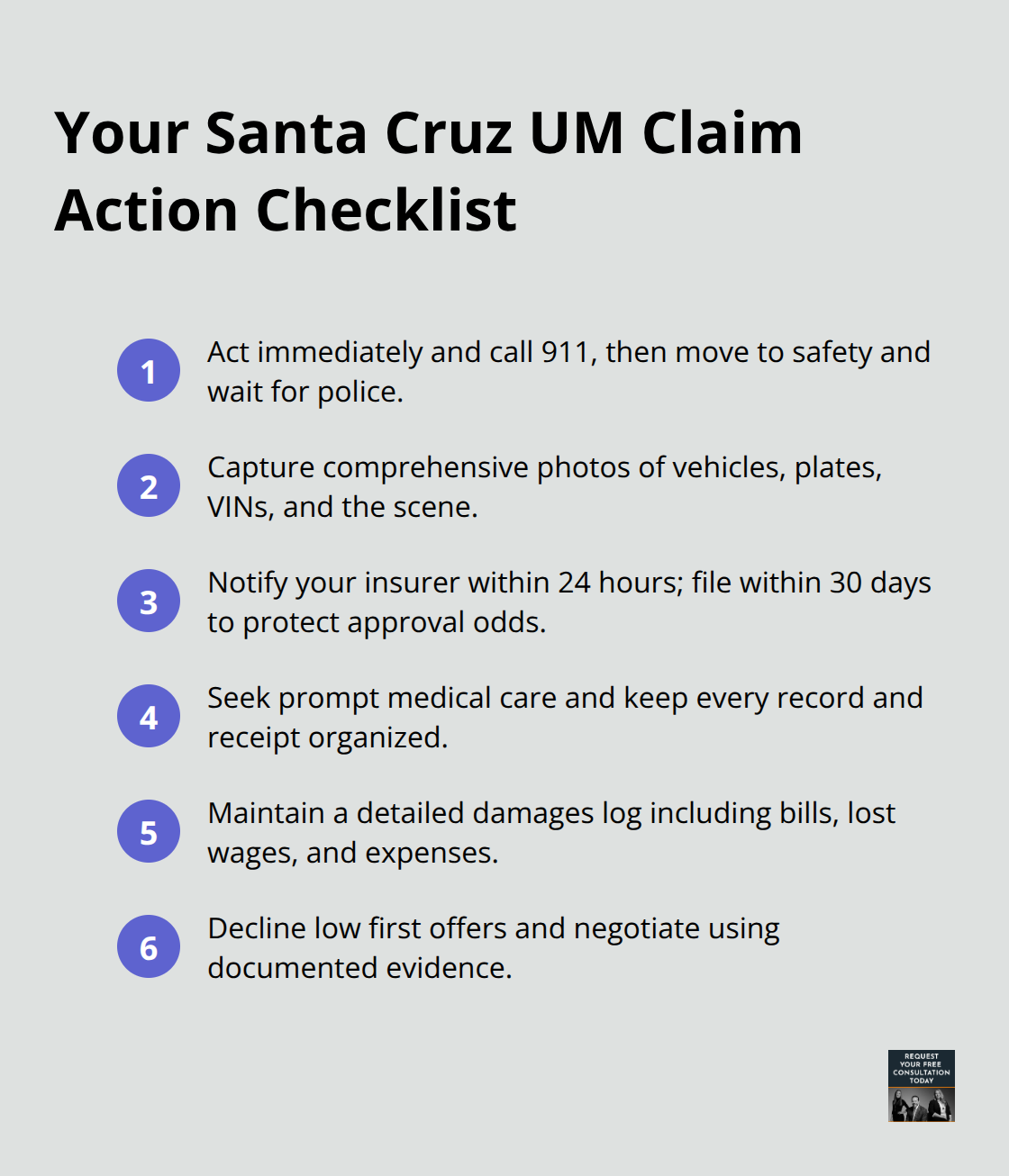

The first 24 hours after an accident determine whether your UM claim succeeds or stalls. Call 911 if anyone is injured, then move to a safe location and wait for the police. The California Highway Patrol’s accident report becomes the cornerstone document for your entire claim-insurers scrutinize police-documented accidents far more seriously than claims lacking official documentation. Before leaving the scene, photograph the other vehicle’s license plate, VIN, and damage from multiple angles. Collect the at-fault driver’s name, address, license number, and insurance information, or note if they claim to be uninsured.

Document Everything at the Scene

Photograph your own vehicle damage, the accident location, road conditions, and any visible injuries. Obtain contact information from at least two witnesses; their statements carry enormous weight when the other driver is uninsured or a hit-and-run occurs. Do not sign any statements admitting fault at the scene-document facts only and let the claims process handle liability. Notify your insurance company within 24 hours with accurate accident details and injury information; filing within 30 days improves approval odds by roughly 20% according to the California Department of Insurance. Delays or incomplete initial reports give insurers ammunition to deny or minimize payouts later.

Seek Medical Care and Build Your Records

Seek medical evaluation immediately, even if you feel fine. UCSF Medical Center research shows about 40% of accident victims experience delayed-onset symptoms that surface days or weeks later. Waiting to see a doctor weakens your claim because insurers argue injuries weren’t serious if treatment was delayed. Keep every medical receipt, bill, and treatment record in one organized folder. Document lost wages by notifying your employer and maintaining pay stubs showing missed work. Attend all medical appointments and follow prescribed treatment plans completely; gaps in care give adjusters reason to dispute injury severity.

Prepare for the Adjuster’s Investigation

Insurance adjusters will request recorded statements and may require an Independent Medical Examination by a doctor they select-this is standard practice, not a sign of trouble. Maintain a detailed damages log listing medical costs, rehabilitation, prescriptions, transportation expenses, income loss, car rental, and other accident-related costs. Claims with comprehensive documentation settle roughly 40% faster on average, so thorough evidence gathering pays dividends during negotiations. When the adjuster makes an initial settlement offer, resist accepting immediately. The insurance company’s first offer typically undervalues your claim, and you retain the right to negotiate further or pursue additional legal remedies.

Calculating What Your Claim Is Actually Worth

Your damages fall into two categories: economic losses you can document with receipts and invoices, and non-economic damages like pain and suffering that require careful calculation. Economic damages include medical expenses (every bill from the emergency room to physical therapy), lost wages (with pay stubs as proof), vehicle repair or replacement costs, rental car expenses, and prescription medications. The California Department of Insurance notes that claims with comprehensive documentation settle roughly 40% faster on average, which means you should invest time now to organize receipts and bills-doing so directly accelerates your payout. Non-economic damages-pain and suffering, emotional distress, loss of enjoyment-are harder to quantify but absolutely recoverable under California law.

How Insurers Calculate Pain and Suffering

Insurers use multiplier formulas (typically 1.5 to 5 times your economic damages) to estimate non-economic damages, though the exact multiplier depends on injury severity and your policy limits. UCSF Medical Center data shows that about 40% of accident victims experience delayed-onset symptoms, which often increases the total cost of treatment and strengthens your non-economic damage claim. Calculate your total damages by adding medical bills plus lost wages plus pain and suffering multiplier, then compare this figure against your UM policy limits.

Why Initial Offers Fall Short

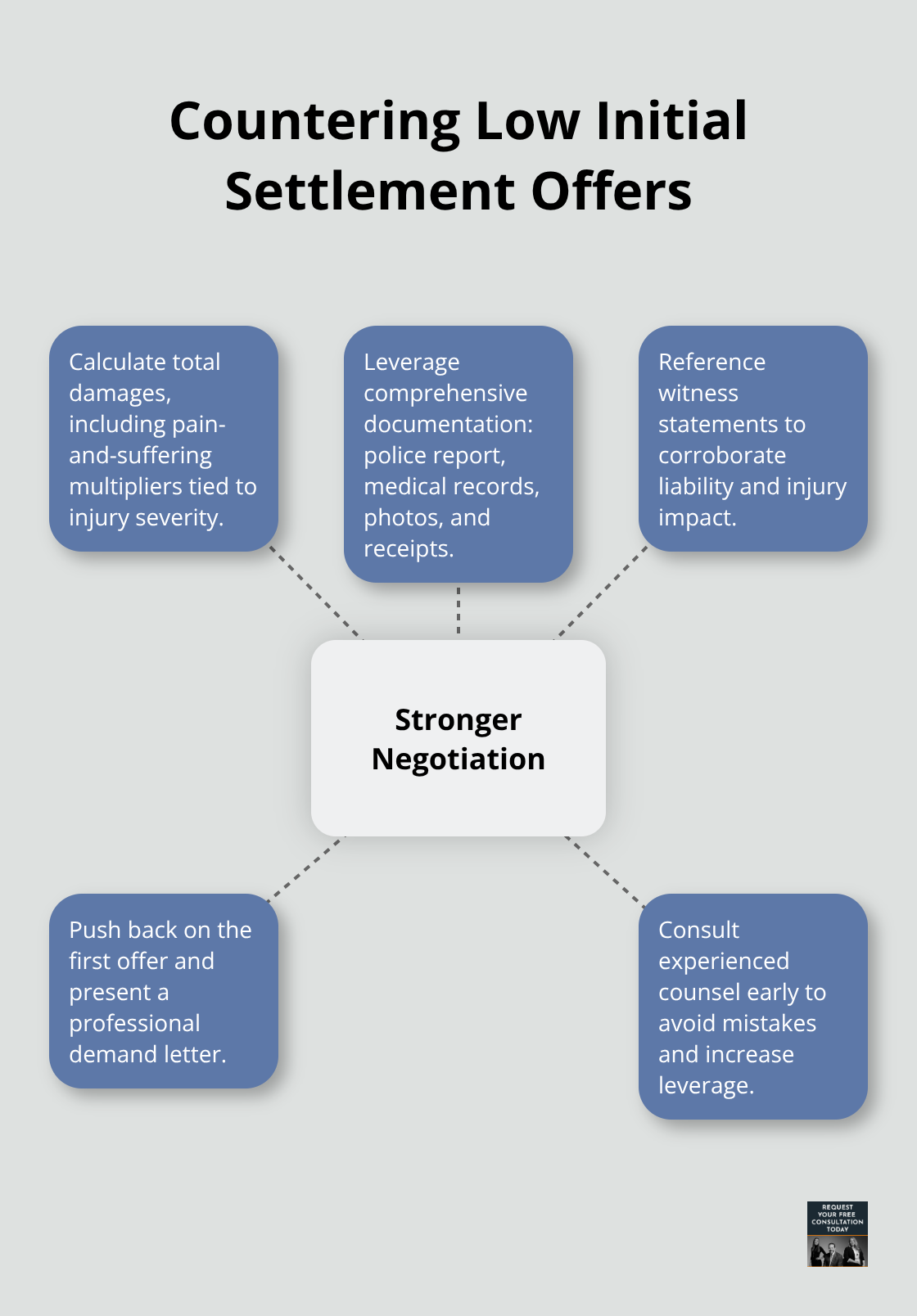

Most insurers will make an initial offer well below your calculated amount-expect their first proposal to undervalue your claim by 30 to 50 percent. The insurance company knows most injured people will settle quickly to pay bills, so their opening bid reflects that assumption rather than fair market value for your injuries. Do not accept the first offer.

Responding with a Professional Demand

When the adjuster presents a settlement proposal, respond with a formal demand letter that references your documented damages, cites the police report, includes witness statements, and explains your injury timeline with medical records attached. Insurance companies respond to organized, professional pressure far more seriously than to casual negotiations. If the adjuster’s counteroffer still falls short of reasonable value, you face a critical decision: accept a lower payout or pursue litigation with legal representation.

The Case for Early Legal Representation

This is where the distinction between handling a claim alone and working with experienced counsel becomes decisive. Many Santa Cruz attorneys work on a contingency basis-you pay nothing unless they win-which removes financial risk from pursuing maximum compensation. Litigation typically takes 6 to 18 months, but insurers often settle for significantly higher amounts once they see you have retained counsel and filed a lawsuit. The decision to hire an attorney should happen early, ideally within 30 days of your accident, because early legal involvement prevents costly mistakes during the adjuster’s investigation and recorded statement requests. An attorney ensures you do not sign away rights, do not accept inadequate medical examination results, and do not miss critical deadlines. California law gives you two years to file a personal injury lawsuit, but waiting until near that deadline weakens your negotiating position because insurers know time pressure forces settlement discussions. The strongest claims are those handled with legal guidance from the beginning, when evidence is fresh and witness memories are sharp.

Final Thoughts

A Santa Cruz uninsured motorist claim succeeds when you act fast, document thoroughly, and resist accepting the insurer’s first offer. The first 24 hours after your accident determine whether your claim moves forward or stalls, so file within 30 days, seek immediate medical care, and organize every receipt and bill into one folder. These actions accelerate settlement timelines and prevent insurers from exploiting gaps in your evidence.

Most insurers will offer significantly less than your calculated damages in their opening proposal, counting on injured people to accept quickly out of financial pressure. A formal demand letter backed by police reports, medical records, and witness statements forces insurers to take your Santa Cruz uninsured motorist claim seriously and often results in substantially higher settlements. Resist the pressure to settle early, and instead respond with professional documentation that demonstrates the full value of your case.

Early legal representation separates successful claims from underpaid ones, and many Santa Cruz attorneys work on contingency so you pay nothing unless they win. We at Schaar & Silva LLP handle the legal complexities while you focus on recovery, and our team provides medical bill assistance and property damage claim evaluation tailored to your situation. Contact us for a free case evaluation to discuss your uninsured motorist claim and learn how we can maximize your compensation.